Deep Dive | Is Blockchain More Like a Company or a Nation?

TechFlow Selected TechFlow Selected

Deep Dive | Is Blockchain More Like a Company or a Nation?

There is one department that has existed the longest but has never fit into this classification—it is blockchain protocols and platforms themselves.

Author: Nick Hotz

Translation: 0xbread, TechFlow

While Bitcoin has celebrated its 13th birthday, most of the digital assets we know today are still toddlers in comparison. The "DeFi Summer," which sparked the first wave of real blockchain applications, happened just a year and a half ago, and the majority of successful applications we now consider valuable have existed for less than three years.

At Arca, we’ve long argued that emerging sectors within the blockchain application landscape—such as DeFi, NFTs, gaming, and Web3, including its various sub-industries in file storage, cloud computing, and telecommunications—bear striking resemblance to traditional startups. However, one sector has defied this categorization despite its longevity: blockchain protocols and platforms themselves.

Layer 1 (L1) blockchains (e.g., Ethereum, Avalanche, Terra), and even Layer 2 (L2) solutions (e.g., Polygon, Ronin, Arbitrum), resist simple definitions or valuations. While we can agree their tokens hold value, they don’t offer users an easily definable demand proposition.

Take certain DeFi applications like Sushiswap, which simply facilitates token trading and offers profit-sharing to token holders—this creates a straightforward valuation model. In contrast, protocols like Avalanche resemble app stores on the internet or within Apple’s ecosystem, where developers build applications atop them. Yet because these protocols include native tokens governing their operation, valuation becomes far more complex.

Despite the complexity, people seem divided into two camps when thinking about blockchain value and structure. One camp, composed of practical, traditional, financially-minded individuals, supports Blockchain-as-a-Business (BaB), viewing blockchains as companies with definable cash flows, product-market fit, and business models.

The other camp consists of intellectually advanced dreamers who advocate Blockchain-as-a-Nation (BaN), seeing blockchains as sovereign nations complete with their own governments, economies, militaries, and tax systems.

These two distinct frameworks lead to fundamentally different views on blockchain value: BaB proponents focus on returns to token holders today, while BaN supporters prioritize new users and economic growth over direct compensation to token holders. This divide fuels debate, as each side relies on vastly different metrics to evaluate their preferred blockchains.

As someone straddling these warring factions, I’ve learned much from both sides—each offers valid insights when describing this segment of digital assets.

The Case for Blockchain as a Business (BaB)

From a traditional financial lens, blockchains resemble businesses quite closely. Perhaps Bankless’ Ryan Sean Adams put it best when he claimed: “Blockchains sell blocks.” Blocks can be sold B2C (to users) or B2B (to other blockchains), generating revenue either way.

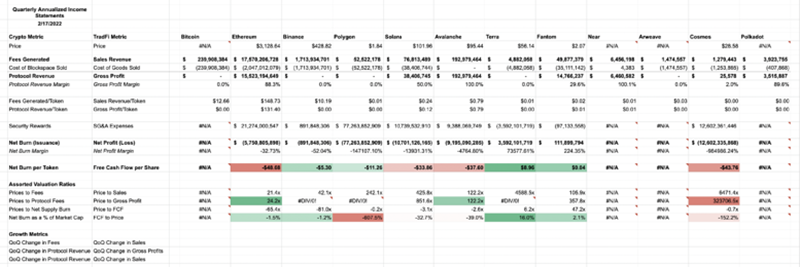

For a block-selling business, success means increasing both the number and price of blocks sold. BaB advocates emphasize fees generated (i.e., revenue earned by validators) as evidence of product-market fit. They aim to return value to token holders via fee mechanisms—either through deflationary monetary policy or other forms of free cash flow such as staking rewards. These metrics not only secure network economics but also signal strong investment potential.

Analysts like Ryan Allis attempt to value Layer 1s (in this case, Ethereum) using fundamental cash flow metrics that will become more relevant after Ethereum’s upcoming merge event. Allis finds Ethereum trading at a steep discount to its intrinsic value (over $10,000 per token), based on future cash flows from staking (akin to dividends) and supply contraction (similar to stock buybacks). Such discounted cash flow models, championed by analytically-driven BaB supporters, are viewed as heresy by the BaN camp.

Objectively, some blockchains run better businesses than others. L1s like Ethereum (or more narrowly, Binance Smart Chain) rake in daily profits thanks to relatively high transaction fees and full blocks. These represent real cash flows—proof for BaB advocates that current fundamentals justify solid investment.

Terra also fits here due to its historically deflationary monetary policy returning value to token holders (stablecoins are also a great business). In contrast, chains like Solana, Polygon, Cosmos, and Avalanche generate nominal fees and suffer from highly inflationary token supplies—undermining any superpowers BaB might attribute to them.

Token Terminal, a leading provider of digital asset metrics and research, applies similar methods, assigning fundamental indicators (like revenue, price-to-sales, and price-to-earnings ratios) to blockchains just as one would assess application-layer businesses like Sushi or Axie Infinity. However, given differing fee structures and heavy token issuance across many projects, this approach faces challenges in cross-comparison. For example, Terra’s deflationary mechanism returns value to native LUNA holders, yet Token Terminal cannot assign earnings or P/E ratios since it doesn’t account for coin burns.

Another key issue in treating blockchains as businesses is the currency in which they earn revenue. Unlike any real-world enterprise, blockchains earn income entirely in their own native tokens—not external currencies like the U.S. dollar.

Critics of BaB argue that calling this “earning revenue” is akin to defining Amazon buying back its own stock as “profit,” without counting new cash inflows. To bridge this gap, BaB proponents treat native tokens as a fundamentally new asset class—one combining traits of capital assets, consumable assets, and stores of value. When L1 native tokens are framed as a novel asset category, it becomes easier to overlook how exactly they generate income.

Fundamentally, BaB adherents anchor their framework in fiat currency—especially the U.S. dollar—as the global unit of account. Since consumers choose to spend their dollars in the blockchain space rather than elsewhere, the fees collected in native tokens carry real economic weight.

I don’t judge this view harshly—it may well be the more practical of the two. Still, there’s another radically different way to see things: one that frames blockchains not as businesses, but as nations.

The Case for Blockchain as a Nation (BaN)

To a financially-savvy newcomer in Web3, the tribalism between L1 communities seems bizarre. Bitcoin and Ethereum folks appear to despise each other; Ethereum advocates often maintain tense relations with proponents of newer L1s.

To those familiar with investing, such behavior is unprecedented in any other asset class. No one wages (social) wars over whether Coke or Pepsi is better; owning Goldman Sachs instead of JPMorgan doesn’t confer identity. Yet, for some reason, such dynamics dominate digital asset communities.

Though harder to detect in their native assets (possibly due to stability), patriotism abounds among “citizens” of specific communities. Extreme Ethereum loyalists and diehard Solana fans might clash within the blockchain world, yet unite against traditional finance to promote blockchain’s efficacy.

This mirrors two countries that might fight over borders but band together in New York City against foreign cultures. As people deeply engage with their communities, passion grows. When their social, economic, and personal well-being feels threatened, they’re willing to drop everything to defend their values.

In fact, a closer look reveals that blockchain social structures resemble those of nations. When a nation first forms, it’s a blank canvas with infinite potential—but little real economic value beyond “future optionality.”

Over time, as society builds roads, schools, and enterprises, GDP and tax revenues begin to grow. Blockchains follow a similar path—from early formation and speculative value to thriving metropolises with apps and transaction income. Validators conduct “elections” and determine societal rules; miners and stakers act as armies, securing the nation against potential attackers.

Yet, when rebels reach critical mass, brutal civil wars can erupt within a chain. On-chain goods (NFTs) and services support a diversified economy, while deeply decentralized financial systems and trade routes (bridges) connect it all. Most activity occurs in the nation’s native token—the primary medium of exchange—and used to pay mining “taxes” that fund public goods benefiting all users.

To the BaN camp, measuring a token’s value solely by taxes paid by citizens seems short-sighted. The native token is a currency, and a currency’s greatest strength lies in widespread use within a large, dynamic economy. Reserve currency status eventually emerges, but in early blockchain development, everyone can play. Growth matters more than current value; in the long run, what truly drives price is capital flowing into the domestic economy—not tokenomics favoring holders.

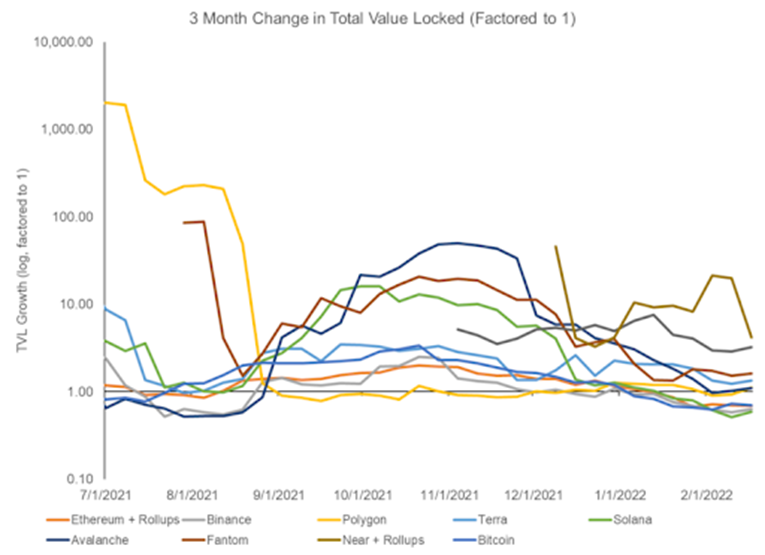

When growth is paramount, charts like the one below matter far more than understanding fees or profitability:

We see past eight months’ winners—Polygon, Solana, Avalanche—emerge as rapid growers, while Ethereum, Binance, and Bitcoin advance slowly and steadily. Network effects appear weak in the nascent world of digital nations envisioned by BaN; current leaders have little room for complacency. Ethereum (and to a lesser extent, Binance Smart Chain) continues charging high fees, creating opportunities for other chains to compete with lower “tax rates,” attracting users and capital to their “nations.”

Natasha Che of Tascha Labs firmly backs this view, arguing L1 blockchains resemble governments more than businesses, with tokens serving as native currencies appreciating as their economies’ “GDP” expands. She authored a bearish report on Ethereum, suggesting its relatively slow growth and shift toward Layer 2s (which severs direct user relationships) could leave it behind compared to other L1s.

Dragonfly’s Haseeb Qureshi shares similar views, likening blockchains to cities that grow until they become too crowded and expensive, prompting new ones to emerge. Expensive yet culturally iconic Ethereum is New York City, but adventurous souls head west, settling in Los Angeles (Solana), Chicago (Avalanche), and San Francisco (Near). Haseeb’s city analogy powerfully defends a multi-chain future (a world with only one city is unthinkable) and suggests these “cities” can coexist—or even cooperate—rather than destroy each other.

a16z’s Chris Dixon, though occasionally extending olive branches to BaB, is also a poetic proponent of the “BaN gospel.” He compares Web3 to a chaotic yet vibrant city, while Web2 resembles Disneyland—clean and beautiful, but overly planned and unnatural. To Dixon, blockchains enable composable digital economies where anyone can create new goods and services and trade freely. These are far more than just profitable ventures designed to enrich token holders like a theme park.

While this framework may better describe blockchain structure, BaB critics rightly note its limited practicality. Because money can’t be fundamentally valued, the only investment strategy under BaN is to follow momentum—tracking where financial value and citizens migrate across chains. While community natives may strongly believe in a chain’s technical or social architecture, investors may struggle to feel confident relying solely on such qualitative judgments.

To bring the world into these systems, we must help people understand blockchains in ways that resonate. For some, the analogy to traditional businesses is intuitive; for others, the revolutionary vision of blockchain as a nation makes more sense. Both frameworks offer strengths in explaining Web3’s emerging world and assessing its most valuable assets. Which one resonates with you? Your answer may reveal blind spots you didn’t know you had—and help explain why so many are passionate about this space.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News