DIY blockchain trend

TechFlow Selected TechFlow Selected

DIY blockchain trend

When everyone builds their own highway, who will drive on them?

Author: Thejaswini M A

Translation: Block unicorn

Preface

You buy a few Philips Hue smart bulbs because they’re said to be the best. The app interface is clean, the colors are dazzling, and dimming them from your phone makes you feel like a tech-savvy pro—very high-end.

Then you decide your thermostat should be smart too. Nest has the strongest AI, so you go with that. A different app, a different account—but it’s fine, just one more feature.

Before long, your life descends into chaos. Your Ring doorbell can’t talk to your Alexa speaker, which can’t control your Apple HomeKit garage door, which in turn won’t connect to Samsung SmartThings. You need four separate apps just to turn on lights, adjust temperature, and lock the door. Every company promises you a “seamless smart home experience,” yet somehow your house feels dumber than before—just with more apps.

Are Circle and Stripe about to repeat this mistake in crypto?

Circle and Stripe

In August 2025, two major announcements dropped.

First, news emerged that $50 billion payments giant Stripe was partnering with crypto venture firm Paradigm to build Tempo, a “high-performance, payments-focused” blockchain. One day later, Circle—the company behind the $67 billion USDC stablecoin—announced Project Arc, a Layer 1 blockchain purpose-built for stablecoin payments, foreign exchange, and capital markets.

Inside Circle Arc: Circle built Arc specifically around its USDC stablecoin. Most blockchains require transaction fees in their native token—ETH on Ethereum, SOL on Solana. On Arc, you pay fees directly in USDC, eliminating the need to hold volatile assets just to use the network.

Arc includes a built-in foreign exchange engine. Instead of relying on external services or decentralized exchanges (DEXs) to swap currencies, Arc handles FX natively at the protocol level. Send USDC, the recipient gets EURC (Euro Coin), and the conversion happens automatically—no third-party service or extra fee.

Privacy controls are also baked in. Most public blockchains (Ethereum, Bitcoin, Solana) expose everything: addresses, amounts, timestamps. Privacy coins like Monero hide all by default. Arc offers selective privacy—organizations can hide transaction amounts while keeping addresses visible, with regulatory compliance features built-in. It’s designed for enterprises that need competitive privacy without full anonymity.

Inside Stripe Tempo: Stripe’s differentiation appears to be user experience abstraction. Other crypto payment solutions still feel like using crypto—connecting wallets, signing transactions, waiting for confirmations. Tempo seems designed so blockchain payments feel indistinguishable from credit card payments to end users.

EVM compatibility means it can leverage existing DeFi infrastructure and developer tools, but the real advantage lies in integration with Stripe’s vast merchant ecosystem. Millions of businesses already using Stripe could add crypto payments without changing checkout flows or learning new systems.

Most importantly, Stripe’s existing relationships with banks and regulators solve a major pain point. Most crypto payment solutions struggle at the “last mile”—getting funds off-chain into regular bank accounts. Stripe already has banking partnerships that other crypto firms spent years building.

Why I’m Still Uneasy

So we’re back to my fragmented digital home, where problems multiply like notification badges across my various smart home apps.

First: Where exactly is the demand for these specialized blockchains?

Circle and Stripe keep talking about stablecoin payments and enterprise features, but the real action with stablecoins is in DeFi. People use USDC to buy other crypto assets, participate in lending protocols, trade on DEXs, and interact with broader financial application ecosystems—all primarily happening on Ethereum.

It’s like building the world’s most advanced smart thermostat that only works in a house with no other smart devices.

Sure, the thermostat might be technically superior, but you’ve cut yourself off from the entire ecosystem where people actually want to use smart home features.

Second: What’s the point of reinventing the wheel?

Everything Circle and Stripe are chasing—faster transactions, lower fees, custom features, enterprise branding—can already be achieved via Ethereum Layer 2 solutions. You get Ethereum’s base-layer security, access to the largest DeFi ecosystem, and the ability to customize your network as needed.

Some Layer 1 blockchains have realized this. Celo, an independent blockchain focused on mobile payments, announced plans to become an Ethereum Layer 2. They did the math and concluded joining Ethereum’s ecosystem made more sense than trying to bootstrap network effects from scratch.

The more blockchains there are, the more bridges you need. And bridges are the problem—they move assets between chains, typically locking tokens on one chain and minting equivalents on another through complex smart contracts. But bridges get hacked. A lot. I swear on Ronin’s name. We’re not talking about the mild inconvenience of switching from the Philips Hue app to the Nest app. We’re talking about potential financial loss if bridge software fails.

User experience suffers. In my smart home, the worst moment is opening another app just to turn off the porch light. For enterprise blockchains, users may need different wallets, different gas tokens, different interfaces, and different security settings for each network. Most people struggle managing one crypto wallet. Imagine explaining why they need separate wallets for Stripe payments and Circle transfers.

But what truly baffles me is the absence of network effects.

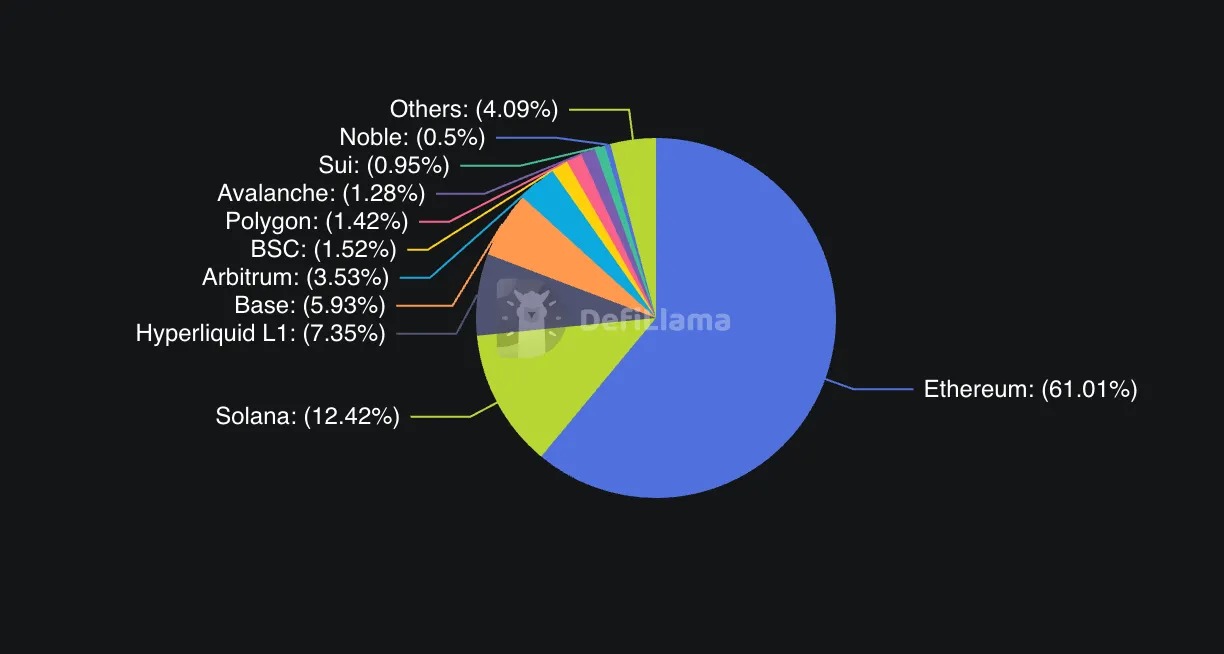

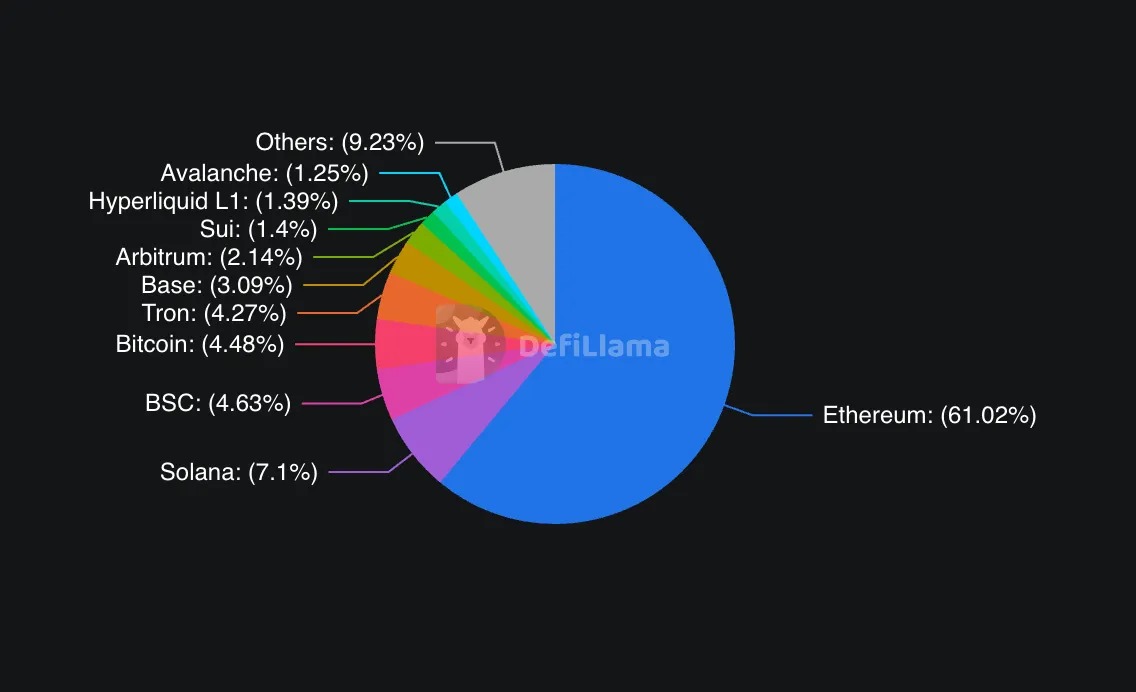

Payment networks grow exponentially in value as users and apps increase. Ethereum has the most developers, the most applications, and the most liquidity. As of mid-2025, Ethereum’s TVL (total value locked) stood at $96 billion, accounting for roughly 60–65% of DeFi activity. Solana, as a high-performance alternative, had $11 billion. Other major chains like Binance Smart Chain ($7.35B), Tron ($6.78B), and Arbitrum ($3.39B) split the remainder.

These corporate chains are opting out of that network effect to build isolated systems, hoping users will magically appear.

Would you build a perfect store on a deserted island? Sure, countries like the UAE built Dubai, and people came. But that was due to geographic constraints. They had no choice.

Finally, there’s the unspoken competition issue. Are these companies really trying to build better infrastructure—or just unwilling to share the sandbox with competitors? Looking at my own smart home mess, every company had rational technical reasons for their choices. But the real driver was often not wanting to rely on someone else’s platform or pay fees to rivals.

Maybe that’s the truth. Circle doesn’t want to pay Ethereum gas fees; Stripe doesn’t want to build on infrastructure it can’t control. That’s understandable. But let’s be honest: this isn’t about innovation or UX—it’s about control and economics.

The real king seems unfazed

Ethereum doesn’t seem worried. The network processes over a million transactions daily, dominates DeFi activity, and recently saw massive institutional inflows via its ETF. On one August day, Ethereum ETFs pulled in $1 billion net—more than Bitcoin ETFs did in an entire week.

The Ethereum community’s reaction to these corporate chains is telling. Some see it as validation. After all, both Arc and Tempo are EVM-compatible, essentially adopting Ethereum’s development standards.

But there’s a subtle threat. Every USDC transaction on Arc instead of Ethereum is revenue lost to Ethereum validators. Every merchant payment processed on Tempo rather than an Ethereum L2 is activity not feeding Ethereum’s network effect.

Solana might feel this competition more acutely. Positioned as Ethereum’s high-performance alternative, especially for payments and consumer apps, Solana’s “everything runs on one fast computer” thesis weakens when big payment players choose to build their own chains instead of adopting Solana.

The Corporate Blockchain Graveyard

History hasn’t been kind to companies attempting to build their own blockchains. As I mentioned earlier, Celo made the same move in 2023.

Remember Facebook’s Libra? Originally an ambitious plan for a global digital currency, it became Diem, then became unsustainable under regulatory pressure, and was eventually sold off. Notably, under today’s clearer rules—like the GENIUS Act, which defines how stablecoin issuers must operate—Facebook’s project might have actually succeeded.

JPMorgan’s blockchain efforts offer perhaps the most relevant cautionary tale. The bank spent years developing JPM Coin (a digital dollar), Quorum (its private blockchain network), and other blockchain initiatives. Despite near-infinite resources, regulatory access, and a massive customer base, these projects never gained meaningful adoption beyond JPMorgan’s own operations. JPM Coin processed billions in transactions, but mostly just for internal fund transfers between institutional clients.

Even attempts by large payment companies haven’t been inspiring. PayPal launched its own stablecoin (PYUSD) in 2023, becoming the first major U.S. fintech to enter the space. But PayPal chose to launch on existing networks like Ethereum rather than build custom infrastructure. The result? PYUSD’s market cap sits at just $1.102 billion—dwarfed by USDC’s $67 billion—and remains largely confined within PayPal’s own ecosystem.

This raises a question: If a company like PayPal—with vast reach and deep payment expertise—can’t make a dent with just a stablecoin, why do Circle and Stripe think building an entire blockchain will fare better?

The pattern suggests building a successful blockchain requires more than technical skill and financial muscle. You need network effects, developer enthusiasm, and organic adoption—things incredibly hard to manufacture even with corporate backing.

Will it be different this time?

There are reasons to believe Circle and Stripe might succeed where others struggled.

First, regulatory clarity has improved dramatically. The U.S. GENIUS Act provides a clear framework for stablecoin issuers, removing much of the uncertainty that plagued earlier corporate blockchain efforts. When Circle launches Arc, it won’t be operating in legal gray zones. It’s a publicly traded company operating under defined rules.

Second, both companies possess what JPMorgan lacked: massive user bases not primarily centered on crypto. Stripe processes over $1 trillion annually for millions of merchants worldwide and has systematically built its crypto infrastructure—acquiring Bridge ($1.1B, stablecoin infra) and Privy (crypto wallet tech)—to create an end-to-end payment stack. Circle’s USDC is already integrated into hundreds of apps and trading platforms. They’re not building a blockchain and hoping users come; they’re building infrastructure for users they already serve, with seamless onboarding tools.

Paradigm’s Matt Huang, describing Stripe’s strategy, emphasized how blockchain tech could “fade into the background” for average users. Imagine online payments with instant settlement, lower fees, and programmable features, but where merchant integration looks identical to Stripe’s current checkout. This is entirely different from asking people to download MetaMask and manage seed phrases. It’s Web2 UX with Web3 infrastructure. Users might not even notice any “blockchain flavor.”

Third, the technology itself has matured. When JPMorgan experimented with blockchain in 2017–2018, the infrastructure was primitive. Today, building a high-performance blockchain with institutional-grade features is challenging but not unprecedented. Circle acquired the Malachite consensus team, giving it battle-tested sub-second finality tech. Stripe’s partnership with Paradigm brings deep crypto expertise to complement its payments know-how.

Cost dynamics have also shifted drastically. In 2017, launching a new blockchain typically cost $1M–$5M and took 1–2 years or more. By 2025, the average cost to launch a functional blockchain app is $40K–$200K, usually taking just 3–6 months—thanks to better developer tools, consensus engines, and blockchain-as-a-service platforms. Modern deployments can be up to 43% cheaper than centralized apps in some areas due to efficiency gains and infrastructure scale.

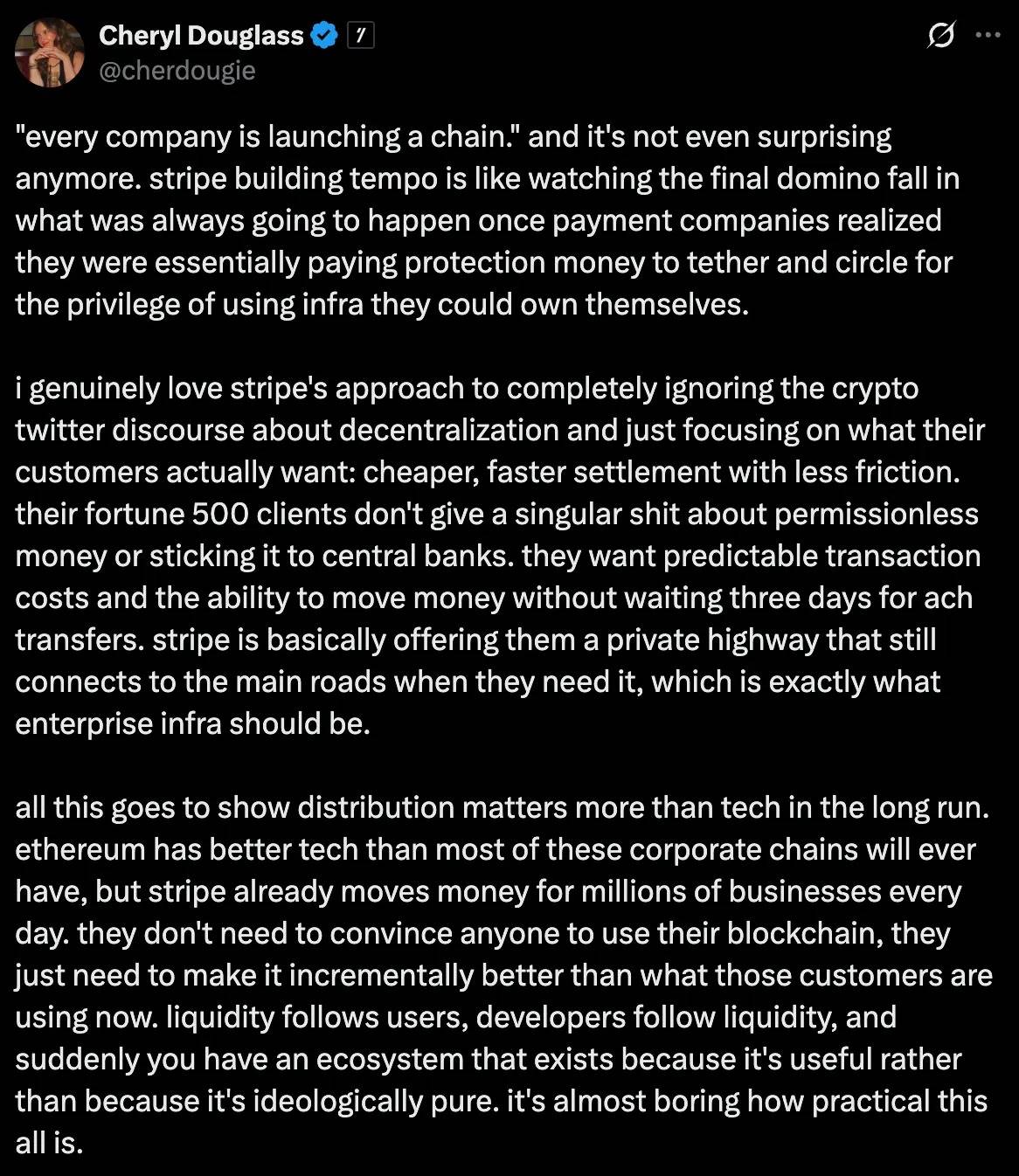

Payment companies realize they’re paying others for infrastructure they could build themselves. Rather than paying Circle for USDC transactions or relying on Ethereum’s fee structure, companies like Stripe can now build their own stack at a fraction of the long-term cost of paying third parties.

This is the classic “build vs. buy” decision, where “build” has dropped from millions to tens of thousands.

The Coexistence Question

So where does this leave us? Are we headed toward a fragmented future where every big company runs its own blockchain, or will market forces drive consolidation and interoperability?

Early signals suggest a pragmatic coexistence—not winner-take-all competition. Circle explicitly stated Arc will complement, not replace, its multi-chain strategy. USDC will continue running on Ethereum, Solana, and dozens of other networks. Arc is positioned as an additional option for users needing specific features like institutional privacy, guaranteed settlement timing, or built-in FX capabilities.

Stripe’s approach appears similar. Tempo isn’t meant to fully replace existing payment channels but to offer alternatives where blockchain functionality clearly outperforms traditional systems—cross-border payments, programmable money, merchant settlements.

User experience will ultimately determine whether this fragmentation becomes a feature or a flaw. If “chain abstraction” technologies deliver on their promise, users might unknowingly use different blockchains. Your payment app could automatically route transactions via the fastest, cheapest network.

My hunch—if I’m slightly optimistic—is that we’ll see both outcomes, but in different market segments.

For institutions and enterprises, multiple specialized blockchains may thrive. A multinational shifting $100 million between subsidiaries cares about compliance features, settlement guarantees, and integration with legacy financial systems. They don’t care about gas price volatility, whether their blockchain hosts the coolest NFT project, or the hottest DeFi protocol. A chain that connects directly to traditional banking rails, offers built-in regulatory reporting, or guarantees settlement times will be far more appealing than Ethereum’s general-purpose infrastructure.

Arc may indeed serve these users better than Ethereum.

Stable fees, instant settlement, and built-in compliance may matter more to a CFO than access to the latest DeFi protocol.

For retail users and developers, network effects remain paramount. Blockchains with the most apps, liquidity, and developer activity will continue attracting more of the same. Today, that’s still Ethereum—and these corporate chains aren’t directly challenging that dominance.

One wildcard is whether these corporate blockchains stay enterprise-focused. If Stripe enables merchants to offer faster, cheaper payments without customers realizing they’re using blockchain, it could spill beyond enterprise use cases.

But the key to infrastructure is this: the best kind is invisible. When you flip a light switch, you don’t think about power plants or transmission lines. When these blockchain experiments succeed, it will be because the underlying technology disappears completely.

Whether that truly happens remains to be seen. For now, we’re in a land-grab phase—everyone wants a piece of the future financial infrastructure.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News