Opinion | The Ethereum EIP-1559 Proposal Is Futile and Offers No Benefits

TechFlow Selected TechFlow Selected

Opinion | The Ethereum EIP-1559 Proposal Is Futile and Offers No Benefits

EIP-1559 cannot make transaction fees more predictable (since demand is unpredictable) nor reduce gas prices, so it doesn't really create a better user experience.

Author | ajian1984

Source | Ethereum Enthusiasts

I. Introduction

The name "EIP-1559" is probably familiar to most people by now. Proposed in March 2019, this proposal introduced a mechanism that burns transaction fees (thereby reducing ETH supply), and was hailed by David Hoffman as "the final piece of Ethereum's monetary policy" and "a key component for ETH to gain monetary premium." It has since attracted growing attention.

About a year and a half ago, after reading an introductory article on EIP-1559 written by its co-author Eric Conner, I wrote a strongly worded critique arguing that the proposal fails to solve the very problems it aims to address, and instead introduces more transaction frictions. My friend Elisa kindly translated my article into English, but unfortunately it received little response.

Times have changed. Recently, support for EIP-1559 has resurfaced repeatedly—driven either by hopes for a deflationary Ethereum or by frustration over high gas prices—making such arguments increasingly popular.

Yet I still haven't seen a convincing argument. These supportive views either misunderstand how fee markets actually work (they are effectively and necessarily "first-price auctions," where owners set reserve prices and the highest bidder wins), or only examine partial effects of EIP-1559 while ignoring its broader impacts. In short, none offer a complete analysis.

Below are several recent articles supporting EIP-1559 that I’ve collected:

-

Analysis of EIP-1559 (Chinese version)

-

What if ETH had a fee burn 5 years ago

-

EIP-1559 51% Attacks: Should you live in fear (Babbitt Chinese translation)

-

Ethereum fee market reform: EIP-1559 as a question of fairness (Chinese translation)

I deeply respect the intellectual effort these authors have invested. Indeed, without their analyses, we wouldn’t be able to see the full picture. But in my view, they jump to conclusions too quickly, fail to adequately justify key claims, or focus narrowly on proving the new mechanism cannot be manipulated—without demonstrating that it performs better than the current system (I will refer to these articles below using "#" followed by numbers).

I will begin with basic economic reasoning, then systematically examine the flaws in these articles.

II. Basic Economic Reasoning

Suppose a good is trading at a high market price. Do you think depriving producers (sellers) of their income from this good would make it cheaper to obtain?

Clearly not. Prices are determined by supply and demand. Reducing seller income discourages production incentives and disrupts the price signal (profit margin), which deters potential new entrants and limits future supply growth. Without increased supply, no amount of discussion changes anything.

But this is exactly what EIP-1559 asks you to believe: cutting miners’ revenue from gas fees will lower gas prices. How could that possibly work?

Imagine going to a hospital and finding doctor consultation fees extremely high. You feel it’s too expensive. Which of the following approaches would help you get better value (same cost for better service, or same service for lower cost)?

A. Lobby the government to cap consultation fees, classify doctors by tier, and set maximum fees per tier;

B. Launch social media campaigns accusing doctors of being greedy, immoral profiteers who don’t care about patients;

C. Government imposes taxes on consultation fees or increases tax rates;

D. The government taxes consultation fees but reassures everyone: “Don’t worry—the tax revenue won’t be spent. I’ll put it in a public account and never touch it, creating deflation for everyone”;

E. Government caps consultation fees while subsidizing doctors, and still taxes the fees;

F. Government taxes consultation fees but says the tax will go into a fund earning interest, eventually returning principal plus interest to doctors proportionally.

Which approach works? None of them.

#A: Price controls (clearly forcing fees down) cause demand to surge while supply dwindles, resulting in appointment caps, longer queues, and scalpers. Average consultation time per patient also drops. Do you really benefit? No—your monetary cost may fall, but your time cost (waiting) rises. More fundamentally, it prevents patients from expressing urgency through pricing, shifting resource allocation toward those with lower time value. In industry jargon, high-quality medical resources get DoS-ed.

#B: This doesn’t need explanation—it’s like imposing a negative price on doctors’ compensation.

#C: For each consultation, doctors earn less, so they naturally invest less effort. And remember: all taxes are ultimately paid by both buyers and sellers. When margins become too thin, transactions simply won’t happen.

#D: Those with clear eyes should recognize this is essentially EIP-1559: combining taxation (#C effect) with monetary deflation. Deflation can increase currency value, but don’t be fooled by appearances: if destroying part of your own property made you better off, why don’t we see people routinely burning their money? (Assuming deflation proportionally increases currency value—an obviously flawed assumption—this becomes a simple math problem.) Under the “tax + deflation” combo, doctors receive fewer nominal dollars, but each dollar is worth more. Even without detailed analysis, one must say “one up, one down—it’s unclear.” If this truly increased their income, why haven’t taxed industries collectively lobbied governments to destroy tax revenues?

#E: Some argue #E reflects EIP-1559’s real-world case because miners earn block rewards in addition to gas fees. But there’s no meaningful difference: block rewards incentivize proof-of-work provision, not gas supply. Just like replacing doctors’ consultation fees with government subsidies incentivizes showing up for work, not treating patients. Have you heard of primary care doctors who only issue referral slips and never actually consult patients?

The key logic linking EIP-1559 to these analogies is simple: EIP-1559 is fundamentally a tax. Why?

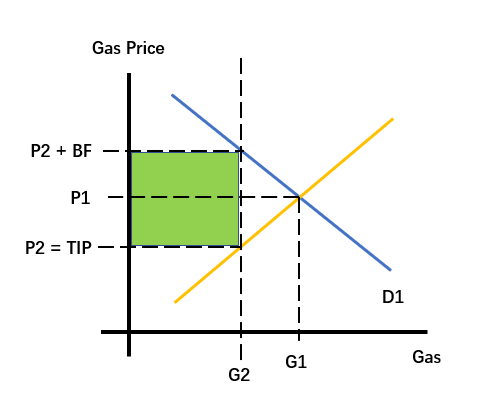

EIP-1559’s core feature is making what users (buyers) pay unequal to what miners (sellers) receive. Total payment splits into base fee and tip (what miners actually get). You pay 10 yuan, miner gets 5 yuan—where does the other 5 go? Never mind where it goes—it’s clearly a consumption tax! - Source: Economic Analysis of EIP-1559 -

- Source: Economic Analysis of EIP-1559 -

Once you recognize it as a specific consumption tax, recall two fundamental principles of tax economics: (1) Consumption taxes are never borne solely by producers—they extract surplus from both consumers and producers. As shown in the green area of the graph, above P1 and below the blue demand curve, consumers enjoy benefits by paying less than their willingness-to-pay (“Gas fee only costs 1%, acceptable”) despite being willing to pay much more (“Yield farming offers 100% daily ROI, let’s do it!”). This gap is called “consumer surplus”; similarly, there’s “producer surplus.” Taxes don’t just eat into producer surplus—they erode both. (2) Every consumption tax creates deadweight loss: some mutually beneficial trades fail because combined surpluses are insufficient to cover the tax. That’s the triangle between supply and demand curves to the right of the green rectangle. In other words, EIP-1559 reduces both gas supply and consumption.

Many claim EIP-1559 improves user experience, clearly failing to grasp this point. Once understood, I can’t fathom how anyone could assert improved UX. At minimum, users’ total payment hasn’t decreased.

As for the deflation it creates, I’ve already addressed that. Deflation raises currency value, but unless it can reasonably prove miners will earn higher income from gas, it cannot show miners will be more motivated to optimize networks and nodes or provide more gas (i.e., increase gas supply), thus cannot prove it lowers gas prices.

Moreover, it achieves this deflation at the expense of ETH’s property rights.

Next, I will analyze the errors in the aforementioned articles.

III. Wise Men May Err

In this section, I respond to several foundational concepts and theories used in the four articles above, primarily drawn from #1, #3, and #4. This is because #2 offers little actual argumentation—it merely extracts historical gas usage and gas price data, arbitrarily assumes a burn rate, and calculates hypothetical burned amounts. However, a blockchain implementing EIP-1559 cannot plausibly maintain the same smoothness and transaction volume as one without it.

(1) #1 and the Slack Mechanism

#1 argues that EIP-1559 increases block size elasticity, allowing sudden demand spikes to be accommodated—some blocks can temporarily grow larger without becoming a permanent burden. This argument holds merit. EIP-1559 defines two gas capacity concepts: target gas capacity and maximum gas capacity. The former determines whether base fee increases or decreases based on actual usage; the latter sets the absolute upper limit of gas per block. Thus, when demand suddenly surges, miners can pack larger blocks short-term without requiring lengthy consensus processes.

I failed to mention this in my previous article—a lapse on my part.

But this benefit isn’t free. Suppose demand suddenly crashes, and users’ willingness-to-pay falls below the base fee rate. Then Ethereum must produce empty blocks, waiting for base fee downward adjustments.

(2) #3 and EIP-1559 Security

#3 strives to prove EIP-1559 is manipulation-resistant—even a 51% PoW attack cannot control it.

In my view, this entire argument misses the point—or rather, claims a non-exclusive advantage.

Miners simply don’t need to manipulate it. How miners earned before EIP-1559 is how they’ll earn afterward—only the label changes. Previously called Gas Fee, now called Tip. Different names, same reality. As long as miners retain block-packaging power, no one can force them to include transactions that would cause losses (i.e., tips insufficient to cover opportunity costs), meaning they still autonomously determine gas supply.

Don’t misunderstand me—I agree EIP-1559 is hard to manipulate; the cost exceeds any gain. But since miners don’t need to manipulate it anyway, this supposed benefit vanishes.

(3) #4 and the “Commons”

I must admit, what shocked me most was #4’s “commons” doctrine. In the section “Who owns Ethereum's blockspace,” the author claims miners’ network protection work is already fully compensated via block rewards, and transaction processing costs aren’t borne solely by miners—therefore miners cannot claim ownership of Ethereum’s blockspace, nor rightful claim to transaction fees.

The conclusion: Ethereum’s blockspace is a “commons,” and miners are “rent-seekers on the commons.”

Truly astonishing. My astonishment lies not only in the author’s apparent misunderstanding of Proof-of-Work (PoW)—overlooking PoW’s core function in distributed systems: transaction ordering. It’s precisely because PoW enables transaction ordering in distributed environments that we need it. This ordering function is fundamentally the same as what the author calls “securing the network.” From an individual perspective, yes, miners provide PoW for block rewards. But from the network’s perspective, transaction packaging and ordering are PoW’s core functions. Losing this function—whether banned by protocol or disincentivized—harms the protocol itself: it either becomes centralized, damages the monetary property of the protocol token (non-transferable assets are worthless), or forces users to pay in non-monetary forms (highly inefficient). (Want to guess which project this describes?)

On the other hand, I’m amazed the author came so close to truth. Yes—if we accept the author’s logic that Ethereum’s blockspace is a commons, then they should realize the first principle of commons governance is privatization, direct or indirect. In our case, this means defining property rights via competitive advantage—allocating shares and earnings based on transaction collection and packaging efficiency among mining pools.

The author calls miners rent-seekers. I say, of course they are! What else could they be? Anyone pursuing “producer surplus” is, by definition, a rent-seeker. The crucial point is: “All under heaven hustle for profit.” If you deny them rental income, the land turns barren—and end users ultimately receive even less.

(4) #1, #4 and “Improved Security”

Both #1 and #4 present an argument: when transaction fees become miners’ primary income source, fee volatility causes fluctuating miner hashpower investment, leading to unstable network security—a dangerous scenario for Ethereum. EIP-1559 supposedly eliminates this risk permanently by reducing miners’ fee income while maintaining block reward value, stabilizing hashpower input.

Whether supporters realize it or not, this is the most sophisticated and ultimate argument in favor. It integrates Ethereum community understanding of network security policy (i.e., monetary policy) and identifies a paramount interest.

Here’s how I’d formalize the analysis:

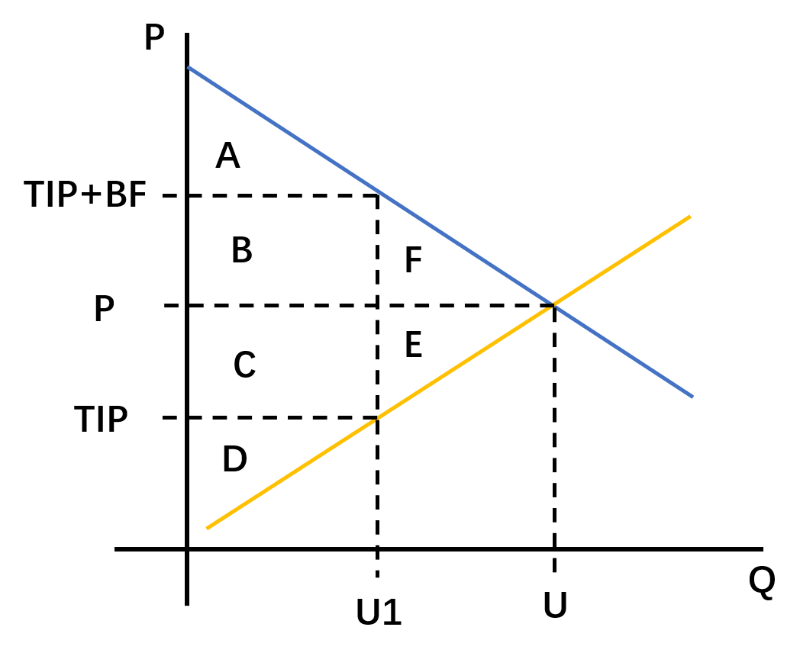

As shown above, horizontal axis = gas quantity, vertical axis = gas price. The downward-sloping blue line is the demand curve: users’ willingness-to-pay declines per additional unit of gas because urgent needs are prioritized. The upward-sloping orange line is the supply curve: miners require higher prices per additional gas unit due to increasing uncle block risks with longer block propagation times—as correctly noted in #4. Without EIP-1559, market gas price settles at P, with usage U (temporarily ignoring possibility of U exceeding block capacity). With EIP-1559, when users pay base fee, miners receive only tip, while users pay tip + base fee, resulting in actual gas usage U1.

(1) Assume base fee = 0: gas usage consistently below target, causing base fee to decay to zero (mechanism detailed in prior article). Here, base fee disappears, and gas usage/payment mirrors pre-EIP-1559 conditions.

Miner revenue = C + D + E + block reward

Under these conditions, EIP-1559 provides no security benefit—miner revenue equals pre-EIP-1559 levels.

(2) Assume base fee > 0: network gas usage occasionally exceeds target.

Even without EIP-1559, gas usage wouldn’t reach U because U exceeds protocol Gas Limit. But miner revenue = C + D + part of E + part of B + part of F + block reward. Gas price would also exceed P, consistent with intuition: users compete via pricing. Miner revenue likely exceeds mere C+D+E+block reward; otherwise, miners would collectively raise Gas Limit.

Now consider post-EIP-1559:

Miner revenue = D + block reward**

Why “block reward**”? Because although nominal block reward stays constant, deflation increases its value—gained precisely from tax-absorbed portions B and C. (While in reality, deflation uniformly appreciates all ETH, here I assume appreciation concentrates entirely on block rewards for simplicity.)

Thus, miner revenue = C + D + B + block reward

Notice anything? If base fee > 0, proponents claiming EIP-1559 enhances security are effectively asserting B > E.

If B < E, EIP-1559 actually reduces security; if B = E, security remains unchanged.

Regardless of actual values, users permanently lose F.

So beneath surface differences, EIP-1559’s core idea aligns with the current system: users pay miners. The difference? Current fee structure involves no middlemen—direct payments with transparent monetary cost. EIP-1559 is stealthy transfer payment: users pay covertly and permanently forfeit a portion of surplus.

As for relative sizes of B and E, that’s inherently beyond theoretical resolution.

IV. Conclusion

In summary, I’ve demonstrated that current arguments supporting EIP-1559 lack solid scientific foundation. EIP-1559 neither makes transaction fees more predictable (since demand is unpredictable) nor lowers gas prices, hence cannot improve user experience. Moreover, recent pro-EIP-1559 arguments either misunderstand ecosystem mechanics or fail to provide comprehensive analysis.

To date, no core developer has announced plans to implement EIP-1559 on PoW Ethereum. Instead, researchers working on Ethereum 2.0 suggest a similar mechanism might appear in Phase 1.

What concerns me more is whether PoW Ethereum will adopt this mechanism due to prevailing support. If such opinions stem merely from incomplete understanding of cause and effect, that’s forgivable. I worry more about those who fully understand the implications yet support this unjust proposal because they themselves belong to unaffected groups.

Let me reiterate: I deeply respect all intellectual contributions made on this topic. Without their voices, I couldn’t have advanced my own analysis or written this article. I keep emphasizing: someone should have said this earlier. It doesn’t require extraordinary genius—yet no one spoke. So I had to say it myself.

One final personal note: Since recorded human history, no system has better stimulated production than market economies, none has lowered costs more effectively—because alternative systems induce people to profit from non-productive activities.

Blockchain is no exception. Check any block explorer: six months ago, Ethereum’s block utilization hovered around 80%; recently, it’s consistently above 95%. Why? When transaction fees are too low, many mining pools prefer packing empty blocks. But when gas prices soar—when skipping one transaction means losing 0.0x or even 0.x ETH—mining pools that haven’t optimized their nodes and networks face the grim fate of watching others feast while being abandoned by miners.

This fact points us toward the right path.

Author’s Afterword

My analysis in Section III.4 is incomplete—I only examined two cases. In reality, a network post-EIP-1559 should exhibit five states:

I. Natural market equilibrium > target gas usage, < max gas usage; base fee = 0;

II. Natural market equilibrium > target gas usage, < max gas usage; base fee > 0, but not high enough to reduce actual usage to target;

III. Natural market equilibrium > target gas usage, < max gas usage; base fee > 0 and high enough to constrain actual usage to target;

IV. Natural market equilibrium < target gas usage, base fee > 0; (corresponds to second case analyzed above)

V. Natural market equilibrium < target gas usage, base fee = 0. (corresponds to first case analyzed above)

(Assuming target gas usage equals pre-EIP-1559 block gas limit)

Readers should realize: (I) corresponds to sudden demand spikes; (II) reflects rising base fee during adjustment; (III) shows completed adjustment, constraining usage to target; (IV) reflects falling demand with base fee still adjusting downward; (V) shows base fee reset to zero after demand drop.

Once you grasp my earlier logic—that miners adjust security investments based on self-interest, allowing comparison of security inputs pre- and post-implementation via supply-demand curves and geometry—you can perform similar policy impact analyses.

It can be shown that under (I), EIP-1559 reduces security (though gas supply increases, giving users temporary gains); assuming all tax revenue fully crystallizes into miners’ block rewards (a favorable assumption for EIP-1559 supporters), we can say EIP-1559 makes no difference under (III) and (V). But under more realistic assumptions, EIP-1559 still reduces security.

As for (II) and (IV), further examination of miner gains under EIP-1559 is required.

This finer-grained analysis also allows measuring user gains under Hasu’s proposed slack mechanism (applicable in cases I and II). In both scenarios, users gain net benefits: part of what would’ve gone to miners under EIP-1559 would, in a non-EIP-1559 world, still accrue to miners via gas price competition—so users lose nothing (I) or even gain (II), plus additional benefits from increased gas supply. (This analysis truly touches on the economic concept of “rent”: benefits attackers wouldn’t relinquish even at loss. High market demand creates such rents via Gas Limit constraints.)

Original link: https://ethfans.org/topics/33308

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News