How much ETH will EIP-1559 burn?

TechFlow Selected TechFlow Selected

How much ETH will EIP-1559 burn?

ETH could truly become better money.

Source: Bankless

Translation: TechFlow

In the words of UFC commentator Bruce Buffer: It's time.

EIP-1559 has finally gone live, two and a half years after its initial proposal! Activated as part of a hard fork, EIP-1559 marks an extremely significant protocol upgrade in Ethereum’s history—one that completely reforms the fee market and improves the user experience of paying for the network’s valuable block space.

Critically, EIP-1559 also introduces a burning mechanism—a portion of transaction fees paid to miners or validators will be permanently removed from circulation.

Every time someone uses the Ethereum network—whether trading on Uniswap or rushing to mint the latest NFT—ETH holders essentially benefit through this burning mechanism.

Fee burning, combined with a dramatic reduction in block reward issuance after The Merge to proof-of-stake, could lead to a deflationary ETH supply and fulfill long-standing speculation about ETH becoming ultra-sound money.

While we’re still some way off experiencing its final form, there could already be substantial ETH burned during this interim period.

This raises several questions. How many tokens will actually be burned? What impact will it have on issuance? Is ETH poised to become a deflationary asset?

These are exactly the answers we’re going to explore.

The Mechanics of EIP-1559

Before examining how much ETH might be burned, let’s take a moment to understand the mechanics behind EIP-1559.

EIP-1559 overhauls Ethereum’s fee market. Currently, mining fees paid by users on the network are determined via a so-called “first-price auction.” Under this system, multiple users bid for block space, and transactions with the highest fees get included in a block.

This system can result in frustrating user experiences. You may have personally experienced situations where gas fees spike either while your transaction is sitting in the mempool or just before confirmation, leaving you stuck waiting because you underpaid. Being stuck is incredibly frustrating, often forcing users to manually input higher gas fees.

EIP-1559 addresses these issues in multiple ways. First, it temporarily expands block size during periods of high network usage to accommodate greater demand for block space. Second, it replaces the “everyone pays the same first-price auction” model and changes the fee structure—which is our main focus here.

Instead of paying a single mining fee, today’s fees now consist of two components. The first is the “base fee,” algorithmically determined and adjusted per-block based on network utilization.

The second component is the “priority fee,” a tip set by the user to incentivize miners to include their transaction.

Sophisticated users can also set a maximum fee—the most they’re willing to pay to get their transaction into a block—and any difference between this cap and the sum of base and priority fees is refunded.

The base fee represents the portion of the transaction fee that gets burned. We can therefore easily infer that during periods of high network activity (i.e., when gas prices rise and block space is scarce), more ETH tokens will be removed from circulation (and vice versa).

Moreover, we see a direct link between value accrued to ETH holders and demand for using Ethereum.

Burn Rate of Fees

Now that we understand how EIP-1559 works, let’s examine how fee burning impacts ETH supply and issuance.

When making these estimates, remember that the base fee fluctuates from block to block. Tim Beiko, a developer who played a leading role in implementing EIP-1559, has indicated that the base fee is expected to account for 25–75% of total transaction fees.

Since manually calculating historical base fees for every single block would be extremely difficult, we’ll use his projected rates of 25%, 50%, and 75% as worst-case, base-case, and best-case scenarios for the proportion of total fees burned.

Thus, these estimates may not be perfectly accurate.

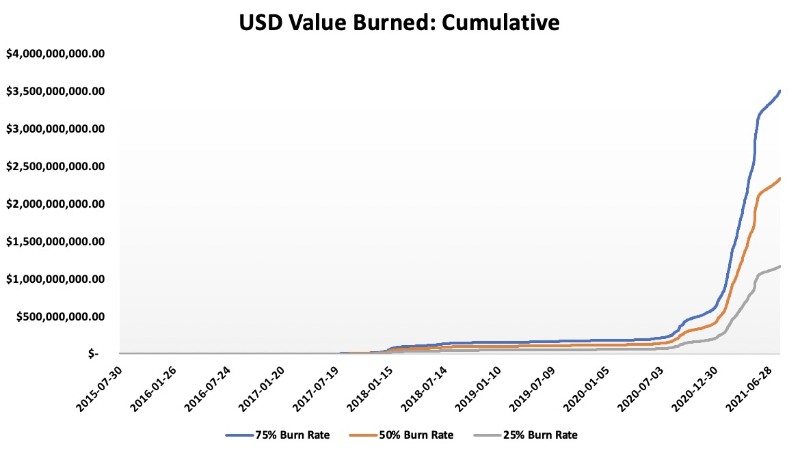

Cumulative ETH Burned

Let’s first consider how much ETH would have been burned if EIP-1559 had been implemented since Ethereum’s inception.

Currently, ETH’s total supply is approximately 116.9 million.

If EIP-1559 had been implemented when Ethereum launched on mainnet in August 2015, cumulative burns under 75%, 50%, and 25% base fee assumptions would amount to 2.9 million, 1.9 million, and 994,000 ETH respectively.

This means the theoretical ETH supply would range between 114 million and 115.9 million.

While these numbers may not seem enormous at first glance, they represent a meaningful reduction relative to total issuance—ETH supply would decrease by 0.85%, 1.70%, and 2.55% respectively.

When measured in USD, the cumulative burn appears even more staggering. Assuming constant rates, between $1.16 billion and $3.5 billion worth of ETH would have been burned over Ethereum’s entire lifetime. To put this in perspective, even the lower end exceeds SushiSwap’s entire market cap, while the upper end surpasses the combined valuations of Yearn and Compound.

From the chart above, we can also observe that ETH burning began accelerating sharply starting in the second half of 2020.

This makes perfect sense. The start of DeFi Summer led directly to explosive demand for Ethereum, ushering in the era of persistently high gas fees that continues today.

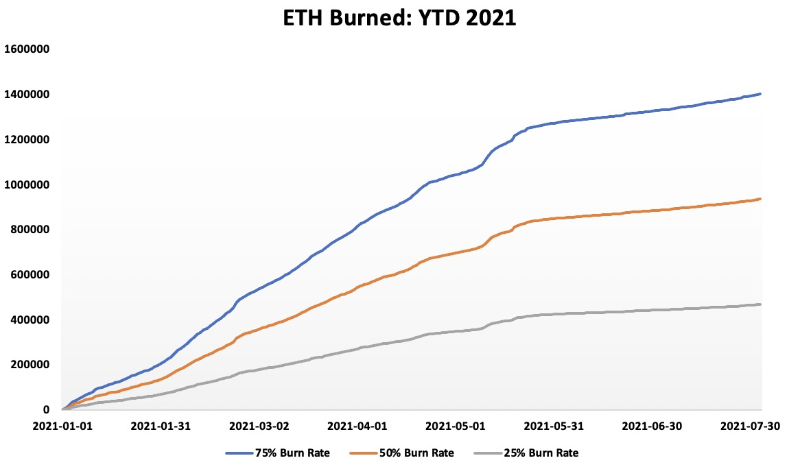

ETH Burned Since Early 2021

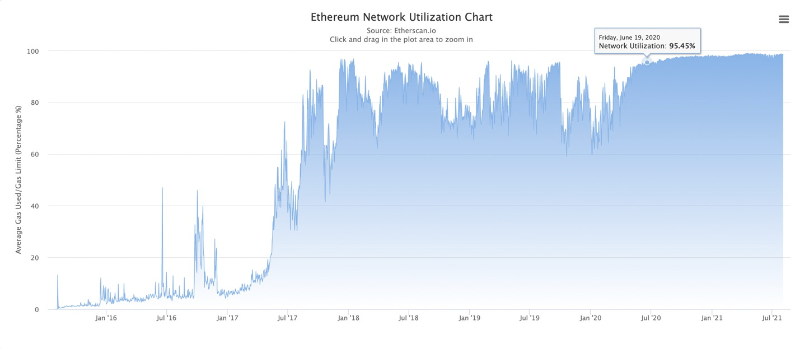

Let’s now zoom in on fees generated since the beginning of 2021. This year is particularly important, as it likely provides the most accurate picture of network utilization and future burn levels.

We can see that the past year spans DeFi Summer in 2020, the bull run through fall and winter of 2021, and the NFT craze of summer 2021—during which Ethereum operated consistently near peak capacity.

If you're a Bankless reader, you probably expect this trend to continue into the foreseeable future, meaning fees generated this year help form reasonable expectations about future burn rates.

Using the same 75%, 50%, and 25% burn rate assumptions, if EIP-1559 had been active, over 1.4 million, 930,000, and 467,000 ETH would have been burned since the start of 2021. Projecting annually, we’d expect 1.8 million to 2.4 million ETH burned in 2021.

From this data, we can see the strong impact of high network utilization on fee burning—over 48% of annual ETH burn has already occurred in just the first seven months.

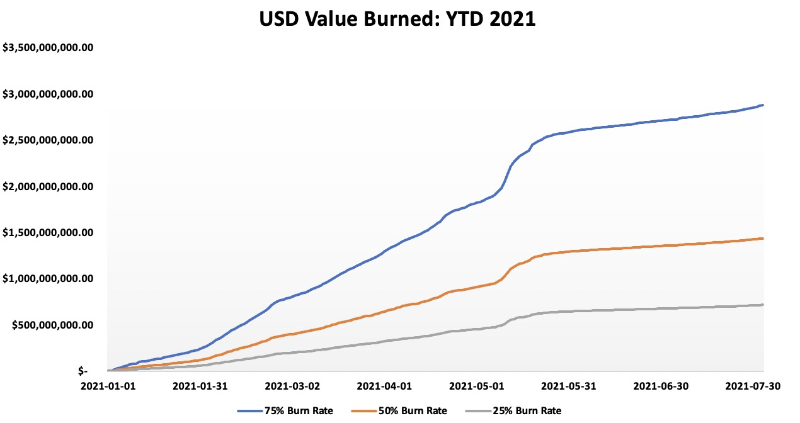

In dollar terms, assuming the same base fee ratios, this translates to $959 million to $2.8 billion worth of ETH burned.

On an annualized basis, the value of ETH burned ranges from $1.6 billion to $4.8 billion. These are staggering figures. For context, the ETH burned this year alone already exceeds the market cap of MakerDAO’s MKR. In the best-case annual scenario, the value of burned ETH would rank among the top 25 largest crypto assets by market cap.

However, note that ETH burn values in USD can sometimes be misleading, as they depend heavily on ETH’s price. This helps explain the discrepancy between the percentage of ETH burned in ETH terms versus USD terms in 2021.

As discussed earlier, the former is 48%, while the latter exceeds 80%.

Impact of EIP-1559 on ETH Issuance

Now that we’ve seen how much ETH has been burned this year, a key question arises: Has ETH become deflationary? To determine this, we need to look at ETH’s total issuance in 2021 and subtract the hypothetical fee burn.

As shown, 2.24 million ETH were issued in the first seven months of 2021, averaging 10,418 ETH per day. On an annualized basis, this implies a 3.8 million increase in ETH supply—an inflation rate of 3.33%, growing from 114.09 million to 117.89 million.

Applying our previous data, if EIP-1559 had been active with base fee assumptions of 75%, 50%, and 25%, the amount of ETH burned would have been 1.4 million, 935,000, and 467,000—equivalent to daily burns of 6,511, 4,348, and 2,172 ETH respectively.

From this, we find that under EIP-1559, daily net issuance ranges from 3,907 to 8,246 ETH—a reduction of 20% to 62%. On an annualized basis, net issuance falls between 1.44 million and 3.04 million, implying a net inflation rate of 1.26% to 2.66%.

While outright deflation hasn’t yet occurred, the amount of new supply entering the market has significantly decreased. ETH’s inflation rate is now lower than pre-Merge levels. Similar to Bitcoin, selling pressure on ETH is effectively halved.

Miners previously had to sell ETH to cover electricity and hardware costs. EIP-1559 transforms this sell pressure into buy pressure, transferring value from miners to ETH holders.

Making ETH Better Money

The supply shock from EIP-1559 sets ETH on the right path to becoming better money post-Merge.

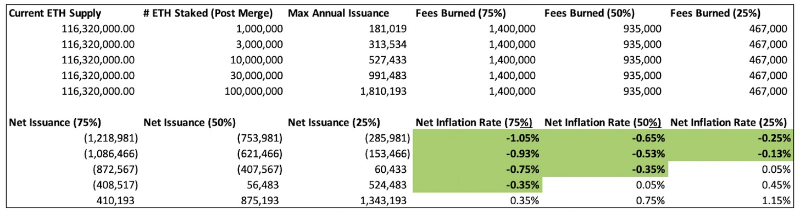

Proof-of-stake drastically reduces the issuance needed for network security. According to ETH Hub, even if 100 million ETH were staked (which is economically unrealistic), the maximum issuance of 1.81 million would still be only 52% of the projected 2021 issuance.

Based on current supply and 2021 burn data (both of which will change and serve only as rough parameters), after transitioning to proof-of-stake, ETH is highly likely to become deflationary—with inflation potentially dropping to -1.05% based on burn rates.

No, this is not a drill.

ETH truly has the potential to become better money.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News