OpenUSD Besieges USDC, Is Circle's Moat Still Secure?

TechFlow Selected TechFlow Selected

OpenUSD Besieges USDC, Is Circle's Moat Still Secure?

Whoever controls the distribution channels controls the future.

Author: Tanay Ved

Compiled by: TechFlow

TechFlow Editor's Note:140 institutions jointly launch OpenUSD, distributing reserve interest to partner networks instead of the issuer keeping it all; Circle's stock price plummets 17% in a single day. But on-chain data shows USDC is deeply bound to core scenarios like Coinbase and Hyperliquid, settling 79% of the $38 trillion transfer volume in 2026. The essence of this war is not fighting for existing stock, but reallocating 'passive' reserve yields—whoever controls the distribution channel controls the future.

Key Points

OpenUSD challenges the traditional issuance model, distributing reserve yields to over 140 partner networks, compressing Circle's profit margins rather than directly seizing USDC's circulation volume.

USDC is a high-turnover stablecoin, settling 79% of approximately $38 trillion in on-chain transfer volume in 2026, anchoring liquidity in major exchanges, DeFi lending markets, and perpetual contract platforms.

Circle's distribution partnerships (such as Coinbase, Hyperliquid) and regulatory positioning strengthen USDC's network effects, making it the preferred dollar channel for many scenarios and use cases.

Introduction

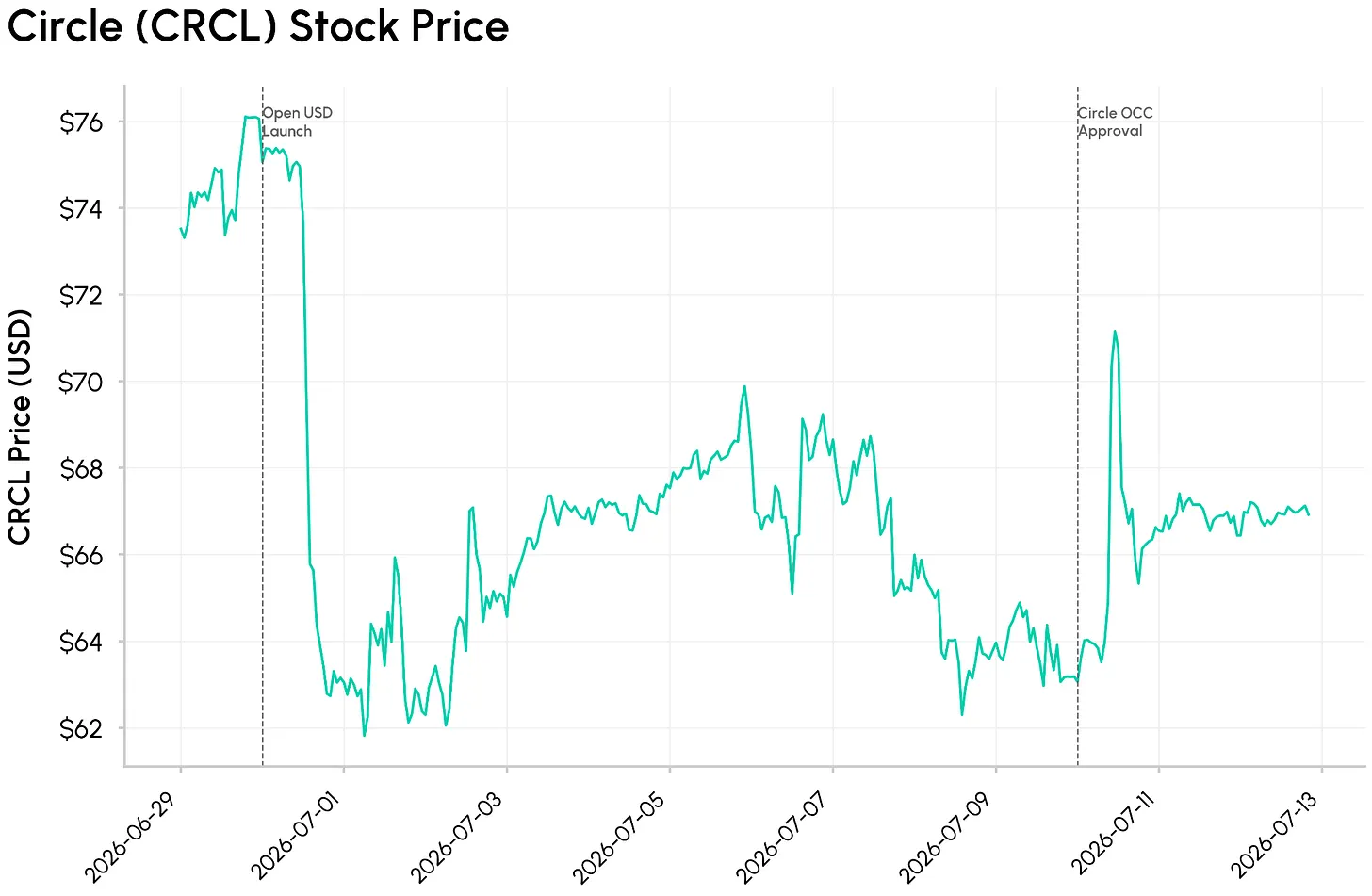

On June 30, the Open Standard consortium, composed of 140 payment companies and banks including Stripe, BlackRock, and Coinbase, announced the launch of OpenUSD (OUSD), a stablecoin backed 1:1 by US dollar reserves. Notably, OpenUSD distributes almost all reserve interest to over 140 corporate partner networks, rather than belonging to a single issuer like Tether or Circle.

The news triggered a plummet in Circle's stock price, with CRCL falling 17% on June 30. This is not just a new stablecoin launch; OUSD represents a direct challenge to the traditional issuance model—where reserve yields primarily belong to the stablecoin issuer. Does OUSD pose a real threat to Circle's profit margins and the deep-rooted network effects behind USDC's dominance?

In this issue of State of the Network, we explore whether the launch of OpenUSD poses a structural threat to Circle's business model and USDC network effects, or if on-chain data tells a different story than the stock market reaction.

Stablecoin Issuance Model: Who Captures the Float?

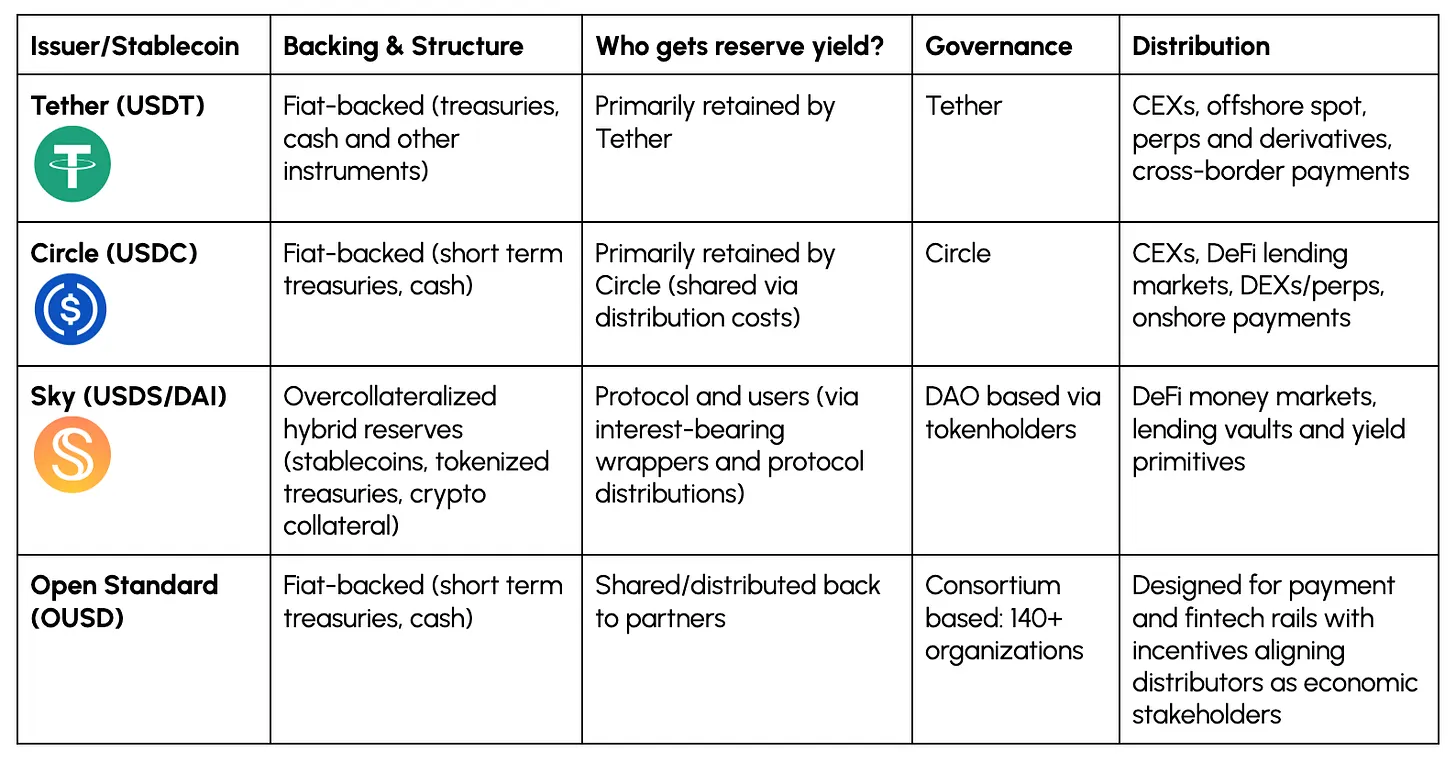

Below we sort out the economic models behind major stablecoins. One key differentiating factor is who captures the float, i.e., the interest income generated by their reserves.

For issuers like Tether and Circle, reserve income largely belongs to the issuer, driving the vast majority of their revenue. For Sky and Ethena, more value is passed to users. OUSD introduces a third model, pushing reserve income to the distribution network itself—companies controlling end-user distribution, such as fintech apps, exchanges, wallets, merchants, and payment processors.

This distinction becomes important because distribution is becoming one of the key differentiators for stablecoins. Circle's model is an example of the issuer sharing economic benefits with key partners (most notably Coinbase), while OUSD builds this into the model.

As mentioned in our previous scenario analysis, Circle's revenue is primarily driven by interest income from USDC balances. In fiscal year 2025, 96% of Circle's $2.7 billion revenue came from reserve income. A significant portion of this is shared with partners like Coinbase in the form of distribution costs. Therefore, Circle's Revenue After Distribution Costs (RDLC) is approximately $1.08 billion, a useful metric for measuring how much it retains after paying distribution fees.

The Coinbase relationship clearly demonstrates how stablecoin value is increasingly accruing to platforms holding the float, rather than the issuer itself. This raises the question: are economic power dynamics shifting from issuers to distributor networks?

Network Effects and Distribution Behind USDC

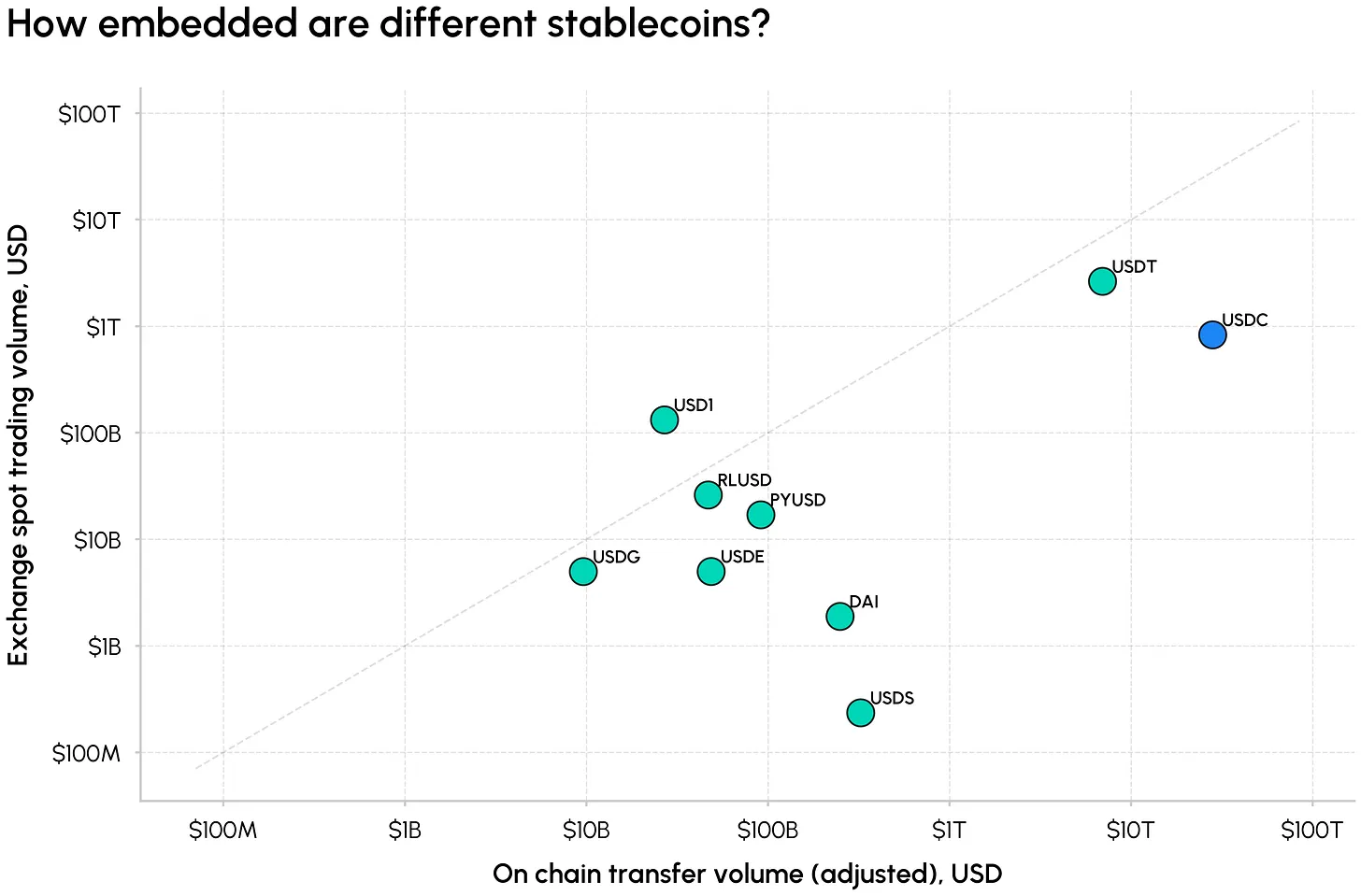

Although dozens of stablecoins have flooded the market in recent years, it remains a duopoly, with USDT and USDC occupying about 86% of the share. Circle's USDC accounts for about 23% of this, with a market cap of $73 billion. This scale was not achieved overnight but is a byproduct of deep liquidity, regulatory advantages, and broad coverage across chains and trading venues.

The chart below captures the scale of different stablecoins from two dimensions: (adjusted) on-chain transfer volume and exchange trading volume as of June 2026. USDT and USDC stand out with high settlement usage and deep trading activity, while USDS, USDe, and PYUSD occupy more niche positions in the grid. Global Dollar (USDG), another consortium-based stablecoin, has so far failed to gain similar traction.

USDC also settles the majority of on-chain transfer volume. In the first half of 2026, USDC settled about 79% of the $38 trillion in adjusted on-chain transfer volume, with Base accounting for 69%. USDT accounted for $7 trillion (about 18%), showing that despite lower USDC circulation, its turnover speed is higher than USDT.

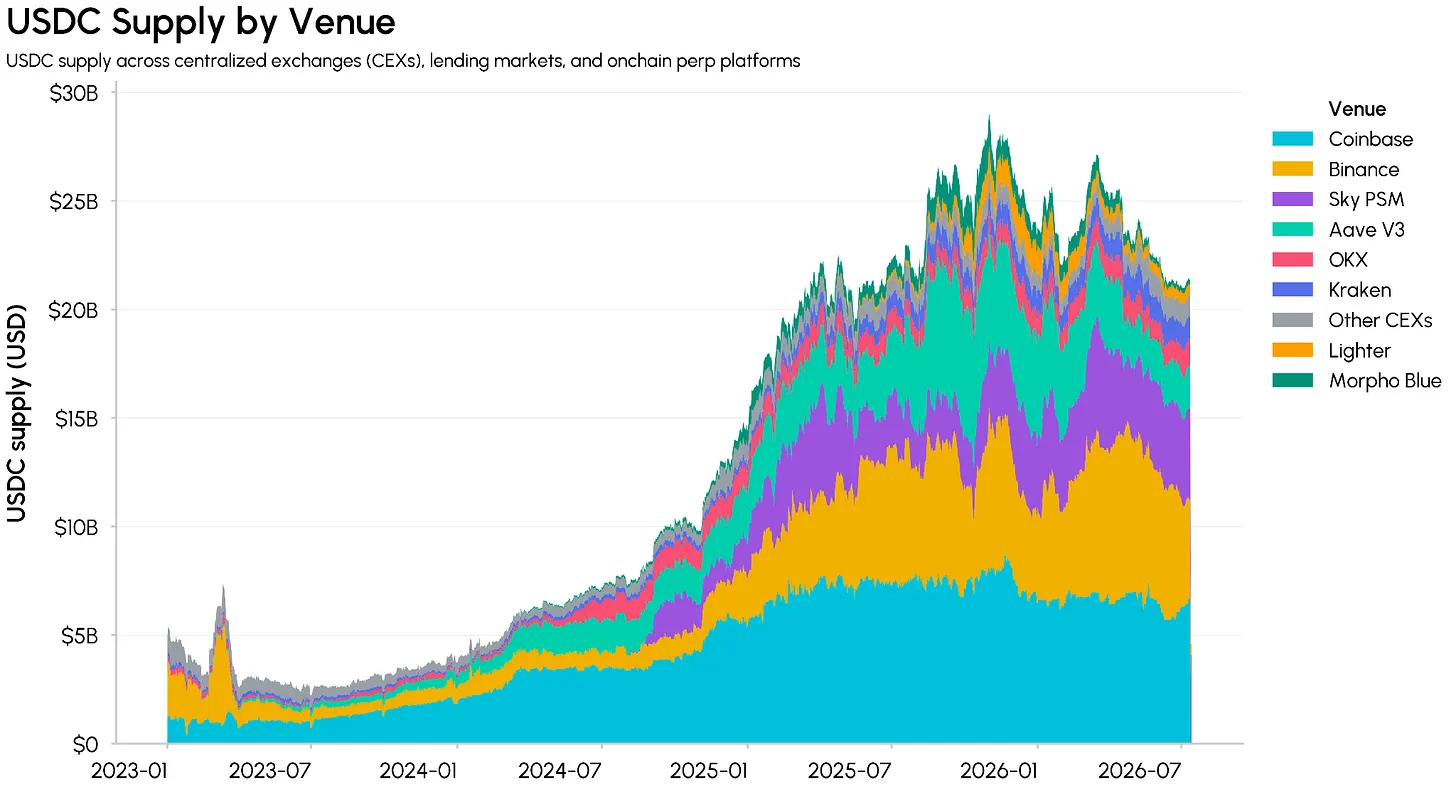

Where is the USDC Supply?

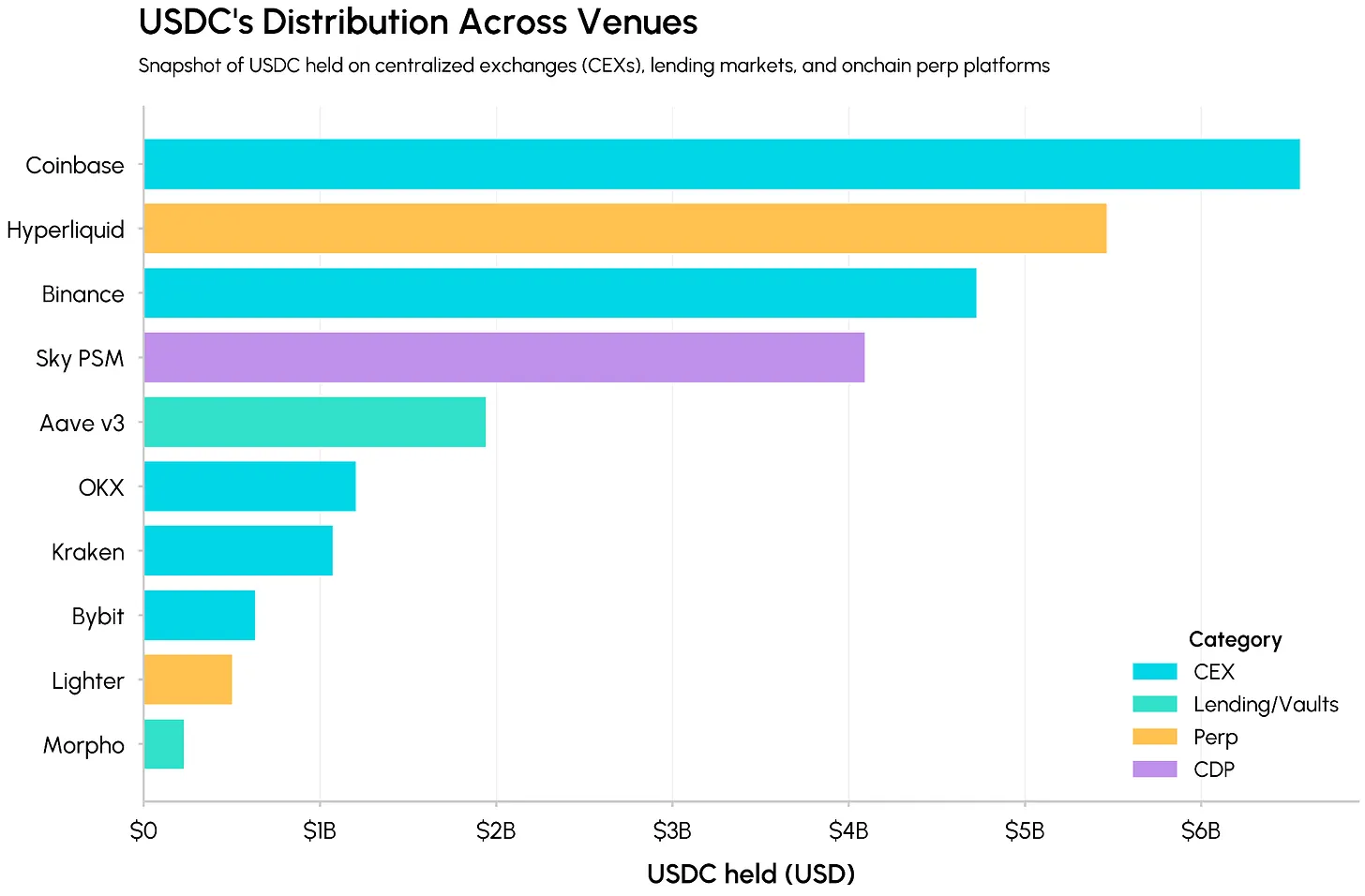

Below we look at where these USDC are actually stored. On centralized exchanges, USDC serves as the primary quoting and settlement asset, while in DeFi it is stored in money markets, vaults, DEX liquidity pools, and as collateral assets supporting other stablecoins. Exchanges like Coinbase and Binance hold billions in USDC, while Hyperliquid, Sky PSM, and Aave v3 occupy large on-chain balances.

Viewing from the perspective of the Circle and Coinbase relationship, the shift in issuer economics becomes clearer. As Coinbase reported in its Q1 2026 earnings, about 25% of USDC circulation is stored in Coinbase products. This coverage enables Coinbase to capture about half of the USDC economy, driving deeper integration and adoption rather than letting most of the value go to Circle.

Hyperliquid is one of the clearest examples recently. In May 2026, Coinbase became the official USDC vault deployer on Hyperliquid, with Circle as the technical deployer, reinforcing USDC's status as the platform's native stablecoin. Under AQAv2, Hyperliquid can capture up to 90% of the reserve yield generated by USDC balances on its platform, transferring an estimated $135-160 million in annual revenue from Circle and Coinbase to HYPE token buybacks and the protocol ecosystem.

This shows how USDC is embedded in the centers of fast-growing market activity, including on-chain perpetual DEXs like Hyperliquid and Lighter, where default quoting assets can shape liquidity, collateral preferences, and other integrations. It also illustrates how issuer and distributor economics are already intertwined: platforms like Coinbase and Hyperliquid are no longer just venues holding USDC, but key economic participants in USDC float.

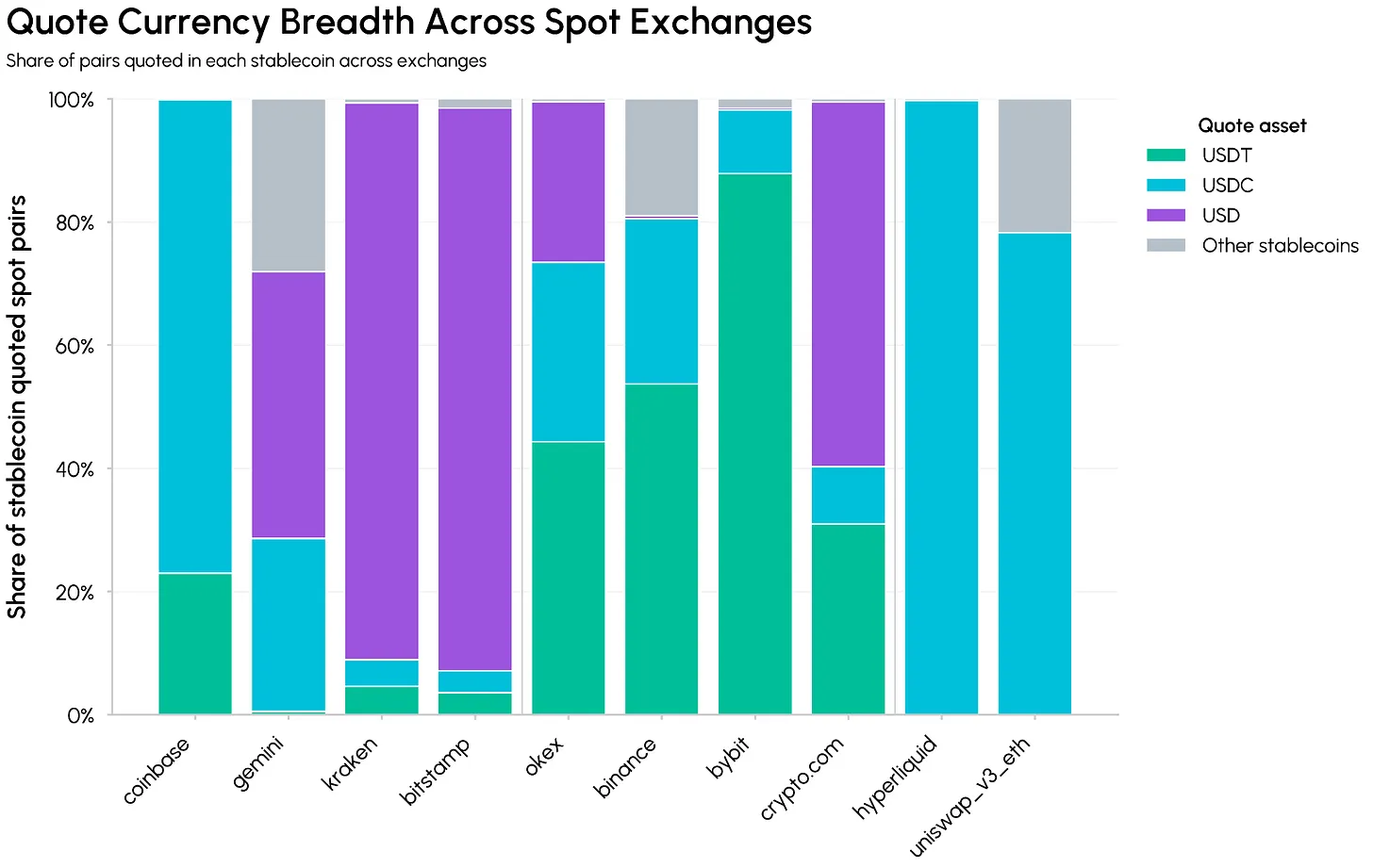

Onshore Dominance and Regulatory Advantages

Stablecoin dominance is also a result of liquidity depth and breadth. The chart below compares the breadth of quoting assets for USDT, USDC, and other stablecoins on spot exchanges. In offshore venues like Binance, Bybit, and OKX, USDT still anchors the vast majority of stablecoin-denominated markets.

Onshore and regulated exchanges such as Coinbase, Gemini, Kraken, Bitstamp, and Crypto.com rely heavily on USD and USDC trading pairs, with Coinbase unifying the USD/USDC order book. USDC is also the dominant quoting asset on on-chain venues like Hyperliquid and Uniswap v3, integrating it directly into perpetual contracts and DeFi liquidity.

Meanwhile, Circle has now received OCC approval to open Circle National Trust, a national trust bank that can hold and manage USDC reserves under federal regulation. This further consolidates Circle's regulatory advantage as a dollar channel around which exchanges, protocols, and payment providers are willing to build.

The competitive landscape of stablecoins is evolving around who earns reserve income, the depth to which different stablecoins are embedded in market infrastructure, and the regulatory frameworks surrounding them. OpenUSD is best understood as a consortium-governed shared yield network, rather than a direct attack on USDC's existing supply; it exerts pressure on the economics supporting that supply.

The core idea is that reserve income will shift from issuers to payment networks, wallets, exchanges, and other distribution channels driving adoption. Whether this shift is powerful enough to overcome USDC's deep liquidity, broad coverage, and regulatory advantages remains to be seen.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News