Deconstructing Circle’s Q1 Earnings Report: After the Interest Rate Windfall Fades, USDC Prepares Its Next Big Move

TechFlow Selected TechFlow Selected

Deconstructing Circle’s Q1 Earnings Report: After the Interest Rate Windfall Fades, USDC Prepares Its Next Big Move

Circle’s Q1 financial report showed slightly lower-than-expected revenue, but USDC’s on-chain transaction volume surged 263% year-on-year, and non-interest income continued to hit new highs. Coupled with the accelerated rollout of diversified initiatives—including Arc Network and Agent Stack—Circle is evolving from a “stablecoin issuer” into an infrastructure operator underpinning the dollar-based internet.

Author: Odaily Planet Daily

Before U.S. market open on May 11, stablecoin issuer Circle officially released its Q1 2026 financial results.

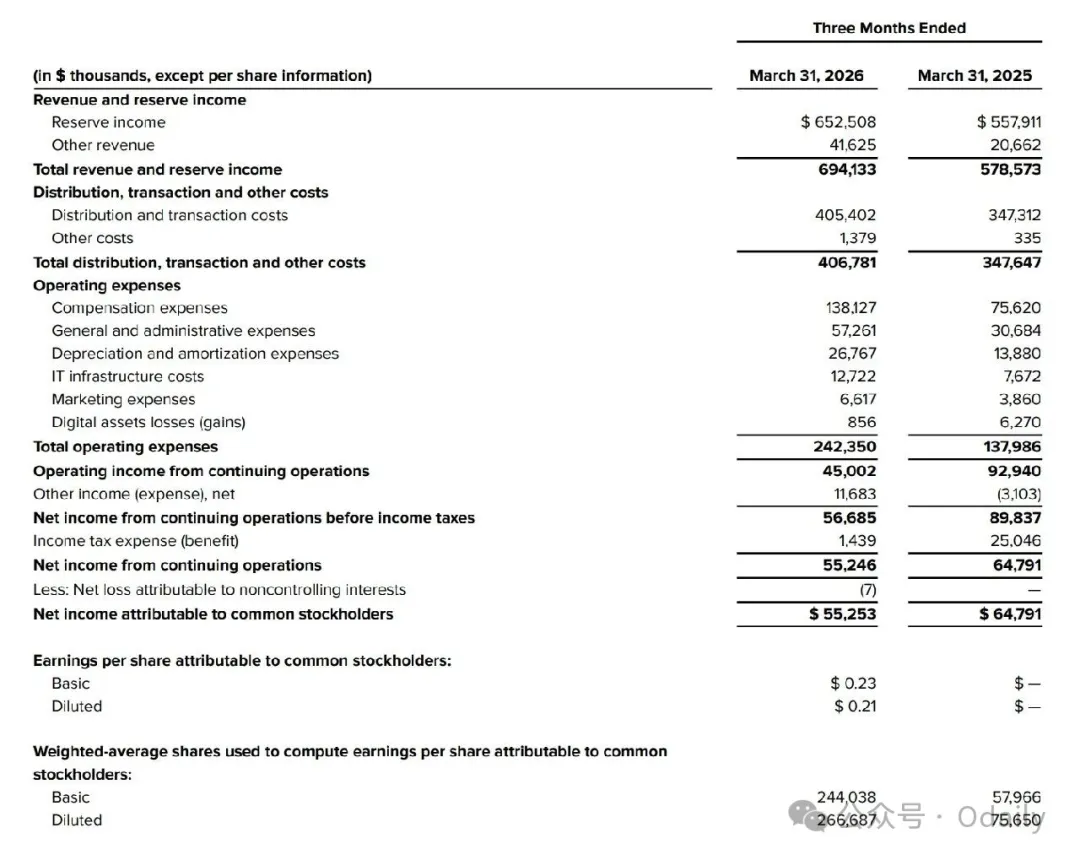

The report shows that Circle’s total revenue and reserve income for Q1 amounted to $694 million—slightly below the market expectation of $715 million. EPS stood at $0.21, exceeding the consensus estimate of $0.18. Adjusted EBITDA reached $151 million, up 24% year-on-year; net income totaled $55 million, down 15% year-on-year.

Following the earnings release, CRCL experienced significant pre-market volatility: an initial pre-market gain of nearly 6% was gradually erased amid fluctuations. As of 10:00 p.m., CRCL plunged sharply in after-hours trading but quickly rebounded into positive territory, currently trading at $115.74—a 2.52% gain on the day.

Key Data Interpretation

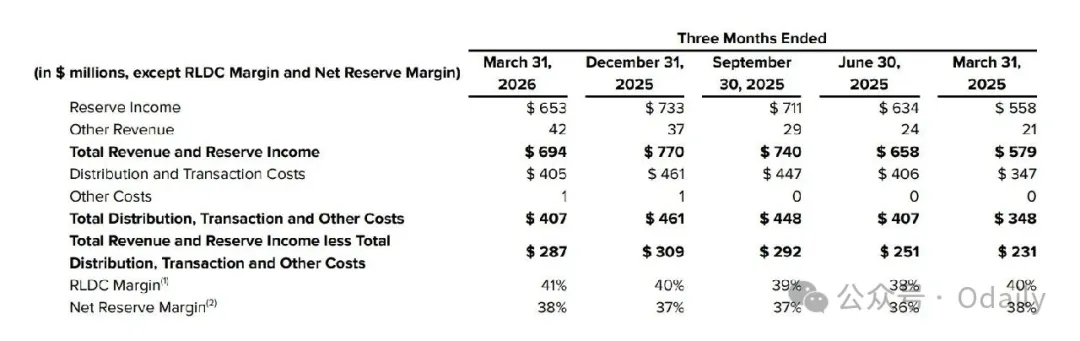

As reflected in the report, Circle’s total revenue and reserve income for this quarter stood at $694 million—up 20% year-on-year, yet breaking a prior streak of consecutive quarterly growth (from $579 million → $658 million → $740 million → $770 million → $694 million) and falling short of market expectations.

Circle attributed the slowdown in revenue growth to a decline in its reserve return rate. On December 10, 2025, the Federal Reserve lowered its target federal funds rate range by 25 basis points to 3.5%–3.75%, compressing yields on Circle’s U.S. Treasury-dominated reserve assets.

Despite relatively soft top-line performance, several encouraging indicators emerged from this earnings report.

First, Circle’s “other revenue”—i.e., revenue excluding reserve income—reached a new high of $42 million, reflecting continued sequential growth (from $21 million → $24 million → $29 million → $37 million → $42 million).

As noted earlier today in our article “Earnings, Legislation, and the Fed… Circle Faces Three Major Tests This Week” (https://www.odaily.news/zh-CN/post/5210700), this signals growing revenue diversification for Circle: its platform services, API tools, and payment products are generating tangible commercial returns, reducing reliance on interest income.

Another noteworthy metric is RLDC Margin—the margin derived from revenue minus distribution costs—which reflects core business profitability after deducting distribution expenses and is widely regarded as Circle’s most critical profitability indicator. This quarter, Circle’s RLDC Margin reached 41%, marking four consecutive quarters of growth (36% → 39% → 40% → 41%), indicating increasingly efficient control over distribution costs.

Turning to expenses: Distribution and Transaction Costs remain Circle’s largest expense line item, totaling $405 million this quarter—an increase of 17% year-on-year. These costs are primarily tied to Circle’s USDC distribution agreement with Coinbase, which expires in August this year. The terms of renewal—particularly any adjustment to the revenue-sharing ratio—will significantly impact Circle’s future expenses and profitability.

Excluding distribution costs, Total Operating Expenses surged from $138 million last year to $242 million this quarter—a staggering 76% year-on-year increase. The primary driver was Compensation Expenses, which rose from $75.62 million to $138 million—nearly doubling. Circle attributes this mainly to stock-based compensation expenses and related tax impacts following its IPO.

Due to this sharp rise in expenses, Circle’s operating profit declined from $92.94 million in the prior-year period to $45 million this quarter; net income attributable to common shareholders fell from $64.79 million to $55.25 million; and EPS came in at $0.23, or $0.21 on a diluted basis.

Other Operational Highlights

Beyond core financial metrics, Circle highlighted several operational achievements in its Q1 report.

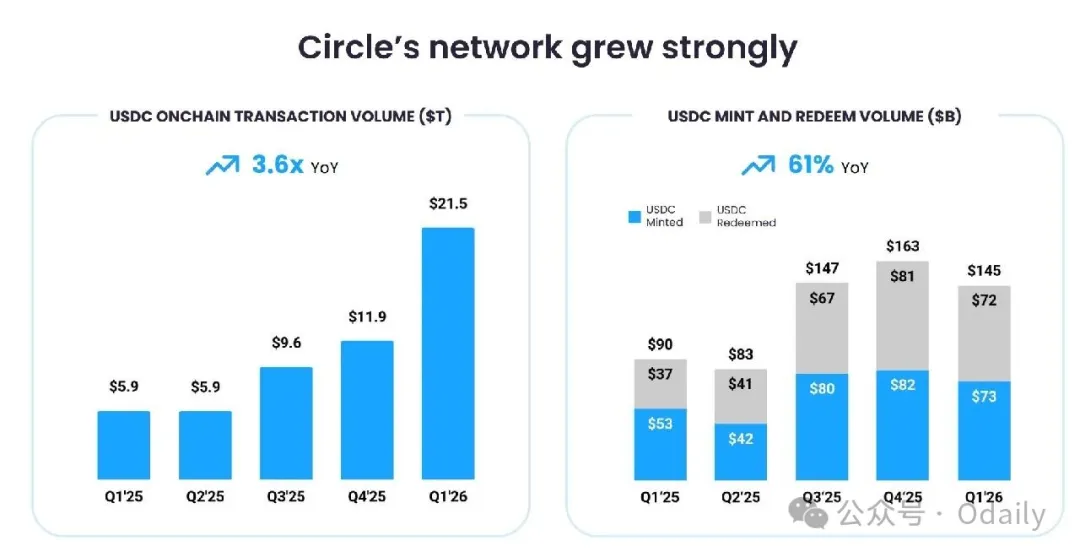

The most critical figure is USDC’s circulation supply, which reached $77 billion at the end of Q1—a 28% year-on-year increase. Meanwhile, USDC’s on-chain transaction volume for Q1 hit an astonishing $21.5 trillion, surging 263% year-on-year. According to Visa Onchain Analytics, USDC accounted for 63% of total stablecoin transaction volume across all networks during Q1.

The far stronger growth in transaction volume relative to circulation supply indicates a dramatic increase in the frequency with which each USDC unit is transacted and applied on-chain—USDC is no longer sitting statically in wallets but is being actively and frequently used in real-world applications such as payments, DeFi, and cross-border settlements.

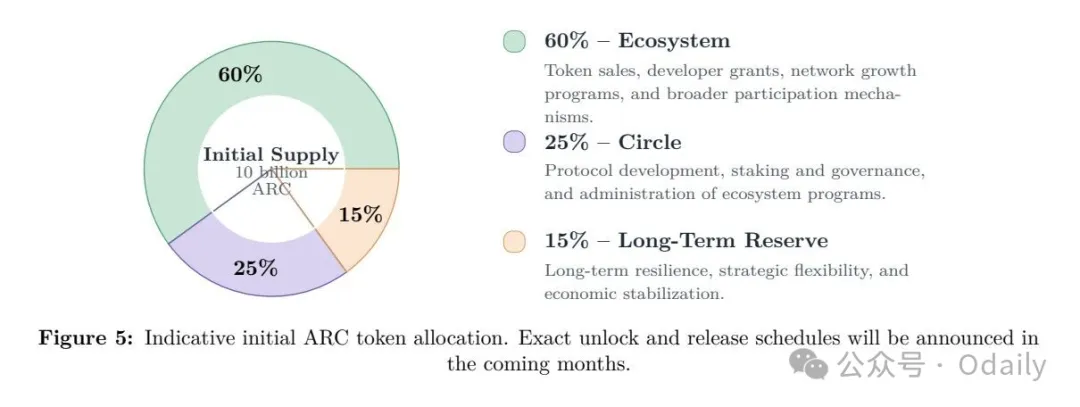

Another key highlight is Circle’s disclosure that its payment network Arc Network has completed a $222 million ARC token presale, valuing the project at $3 billion. Backers include prominent institutions such as a16z, BlackRock, Intercontinental Exchange (ICE), Standard Chartered, and SBI. Today’s published ARC token whitepaper reveals that 60% of tokens will be allocated to the ecosystem (token sale, developer grants, network growth); 25% to Circle (protocol development, staking, and governance); and 15% to long-term reserves (strategic flexibility and economic stability).

Additionally, Circle’s institutional payment service Circle Payments Network (CPN) achieved an estimated annualized transaction volume of $8.3 billion, extrapolated from 30-day data through March 31. In April, Circle launched “Managed Payments,” a new offering designed to expand its payment product suite—enabling financial institutions to launch stablecoin payment services without managing digital assets themselves.

To prepare for an AI Agent–driven commercial future, Circle also announced the launch of Agent Stack—a comprehensive infrastructure service and toolkit tailored for the AI Agent economy, empowering autonomous AI Agents with high-speed, low-cost financial services. Jeremy Allaire, Circle’s Co-Founder and CEO, commented: “With the ARC token presale, the growing momentum behind Arc Network, and the launch of Agent Stack, we are building trusted infrastructure for AI-native economic activity and a more programmable internet financial system.”

Circle’s New Strategic Playbook

Against the macro backdrop of fading high-interest-rate tailwinds (with Waller expected to prioritize “rate cuts + balance sheet reduction” upon succeeding Powell at the Fed), Circle clearly aims to reduce its dependence on Fed policy—and has quietly shifted strategic focus toward diversifying non-interest income.

As detailed in this quarter’s report, having rolled out CPN, Managed Payments, Agent Stack, and Arc Network in succession, Circle’s ambition has evolved beyond being merely a “stablecoin issuer.” Its goal is now to establish USDC as the foundational dollar network of the internet era. Under this new vision, Circle’s target users extend well beyond exchanges and crypto-native participants—to encompass cross-border payments, corporate settlements, and even the AI Agent economy.

Circle’s ambition is unmistakable: transforming USDC from a “static reserve asset” into “flowing economic blood.” This may well be the grand strategy Circle is truly pursuing.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News