Circle’s Worst Single Day in History: Regulatory Draft Targets Core Revenue, Wiping Out $5 Billion in Market Cap

TechFlow Selected TechFlow Selected

Circle’s Worst Single Day in History: Regulatory Draft Targets Core Revenue, Wiping Out $5 Billion in Market Cap

Bullish sentiment still has its rationale.

Author: Mario S.

Translated and edited by TechFlow

TechFlow Intro: Circle’s largest single-day plunge since its IPO—20%—was no isolated incident. Rather, it was the simultaneous detonation of three forces: regulatory pressure, business model fragility, and on-chain freezing.

This analysis clearly lays out Circle’s revenue structure—95.5% reliant on interest from USDC reserves—and explains why the impact of this bill runs far deeper than it first appears.

Full text below:

On Tuesday, CRCL plunged 20%—its largest intraday drop since going public—erasing $5 billion in market capitalization in a single day. Trading volume hit 56.4 million shares, nearly four times its 90-day average. Coinbase fell 11% the same day.

The entire stablecoin yield landscape was re-priced within hours. The trigger was a new draft of the “Clarity Act,” which would effectively end passive yields on stablecoins.

This is more than just a story about one bad day. It reflects a confluence of regulatory maneuvering, a structural flaw in Circle’s business model, and a wallet freeze event—three factors converging to ignite an already-smoldering stock.

The “Clarity Act” Bomb

On March 20, Senator Thom Tillis (R-NC) and Senator Angela Alsobrooks (D-MD) announced a bipartisan agreement-in-principle on stablecoin yield provisions, backed by the White House. The full text was disclosed to industry leaders during a closed-door meeting on Capitol Hill on Monday.

Core provision: Passive yields earned solely by holding dollar-pegged tokens will be explicitly prohibited. Exchanges, brokers, and their affiliates are banned from offering stablecoin balance yields—directly or indirectly—or any form of return “economically equivalent to interest.”

Activity-based rewards tied to payments, transfers, or platform usage remain permitted. The SEC, CFTC, and Treasury Department will jointly define permissible reward structures and anti-circumvention rules within one year. Notably, the SEC and CFTC recently announced a historic interagency memorandum ending years of jurisdictional disputes.

Congress has now formally drawn—in writing—the line that bank lobbying groups have pursued for two years: stablecoins may serve as payment instruments, but not as deposit substitutes.

According to an internal stakeholder email obtained by Eleanor Terrett, an industry leader who attended the closed-door meeting described the text as a “departure” from prior discussions with the White House. He warned that the deliberately vague phrasing of the “economically equivalent” standard leaves room for future regulators to interpret it more stringently.

The Blow Hits Circle Harder Than Anyone Else

Circle currently derives 95.5% of its revenue from interest earned on USDC reserves—explaining the market’s extreme reaction.

CRCL issues USDC and holds reserves in short-term U.S. Treasuries and overnight repurchase agreements, earning the spread. In Q4 2025, reserve income totaled $711 million—a 60% increase year-on-year—driven by a 97% growth in average USDC supply. Full-year 2025 revenue reached $2.7 billion, up 64% year-on-year.

The Clarity Act does not directly target Circle’s reserve income (which CRCL itself earns). Instead, it strikes at Circle’s core demand engine. Currently, platforms like Coinbase pass stablecoin yields through to users as an incentive to hold USDC. Coinbase’s stablecoin revenue reached $1.35 billion in 2025—up from $910 million in 2024. If exchanges can no longer offer yield on USDC balances, users’ incentive to hold USDC over traditional bank deposits will significantly weaken.

Fewer yield-sharing programs → lower USDC adoption → smaller reserve size → reduced interest income for Circle.

Timing compounds the problem. As the Fed cuts rates, reserve yields have already declined—from 4.49% in Q4 2024 to 3.81% in Q4 2025. Though markets no longer expect rate cuts this year, Circle’s interest income was already under pressure before this bill surfaced.

USDC Fundamentals Have Never Been Stronger

The stock crash occurred on the same day that USDC’s underlying metrics hit all-time highs:

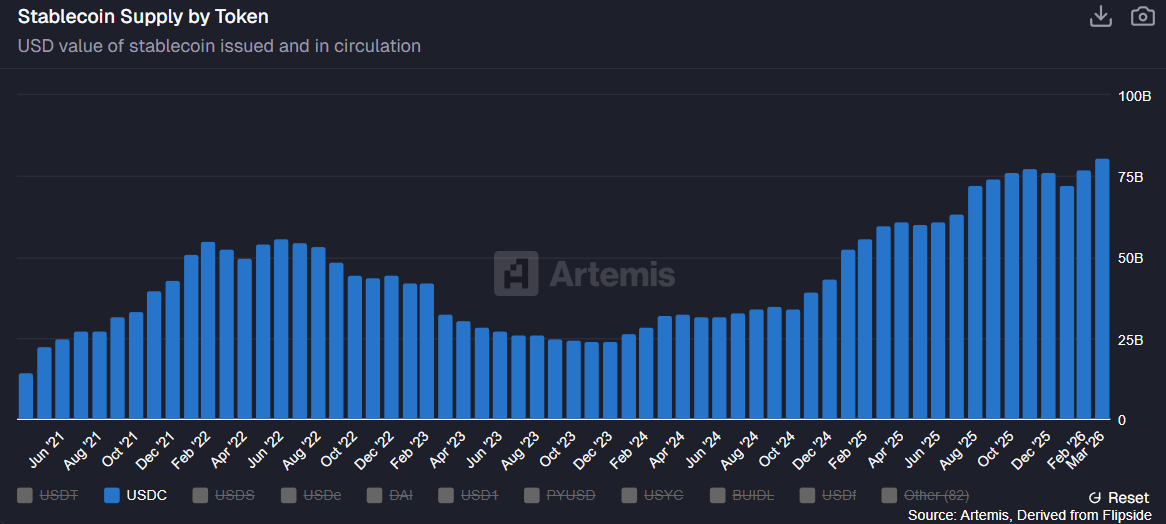

Circulating supply: Reached $81 billion by late March—up from $76 billion at year-end 2025.

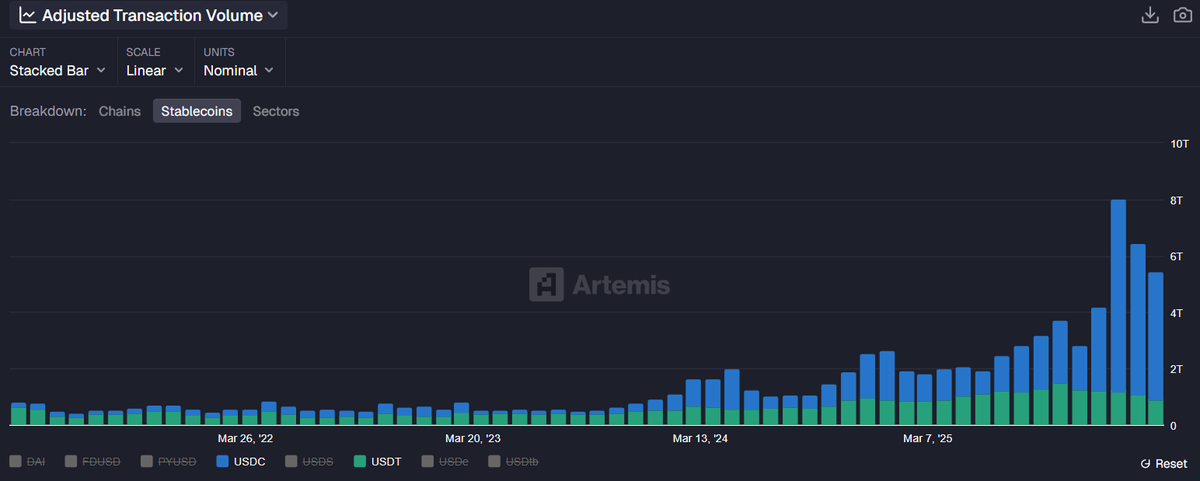

On-chain transaction volume: Adjusted Q4 2025 volume hit $6.8 trillion—more than tripling year-on-year.

Market share vs. USDT: USDC transaction volume has exceeded Tether’s USDT every month since August 2025; its 2026 market share has surpassed 80%.

Q4 earnings beat expectations: Revenue of $770 million—above the $745 million forecast; EPS of $0.43—23% above consensus.

Circle also recently announced its entry into Africa via a partnership with Sasai Fintech and secured a major integration with Intuit.

The Wallet Freeze Added Fuel to the Fire

On Monday night, Circle froze USDC balances across 16 corporate hot wallets—impacting multiple exchanges, casinos, and FX platforms, including FxPro, Pepperstone, AMarkets, and HeroFX.

The freeze reportedly stems from an undisclosed U.S. civil case. @zachxbt raised sharp concerns, noting that basic on-chain tools reveal these were operational wallets processing thousands of transactions daily. He warned that opaque freezes based on undisclosed civil litigation risk turning USDC into a “politicized censorship tool.”

The authority to freeze—and even wipe balances from frozen addresses—is explicitly encoded in USDC’s smart contract. Yet on a day when markets are already questioning the risks of centralized stablecoins, the optics of this action could hardly be worse.

Bullish Arguments Remain

This selloff priced in the most pessimistic interpretation of the Clarity Act—but several counterpoints warrant attention.

Activity-based rewards remain permitted. The bill draws a clear line between prohibited passive yields and allowed transaction-based incentives. Platforms like Coinbase are already exploring workarounds: marketing incentives, activity-based payments, and issuer partnerships designed to blur the line between interest and rewards. The vagueness of the “economically equivalent” standard means lawyers will inevitably seek loopholes.

Coinbase’s P&L impact may be limited. Most of Coinbase’s stablecoin revenue is passed directly to users—so this revenue line is typically offset by corresponding expenses. Analysts believe the direct profit impact is modest. The bigger question is whether restrictions will dampen USDC’s long-term adoption.

The bill is not yet law. Committee review is expected only after the Easter recess ends in late April. Lobbying, amendments, and negotiations still lie ahead. Brian Armstrong has remained conspicuously silent on the latest text—but his prior stance suggests Coinbase will mount a vigorous fight over the “economically equivalent” language.

Non-reserve revenue is growing rapidly. Platform services, transaction processing, and other non-reserve income surged 15.3x year-on-year in Q4 2025 to $37 million; total non-reserve revenue for 2025 reached $110 million. While still small relative to interest income, the logic of revenue diversification is now firmly established.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News