Circle’s Earnings Report Revealed: Who Quietly Took the Stablecoin Profits?

TechFlow Selected TechFlow Selected

Circle’s Earnings Report Revealed: Who Quietly Took the Stablecoin Profits?

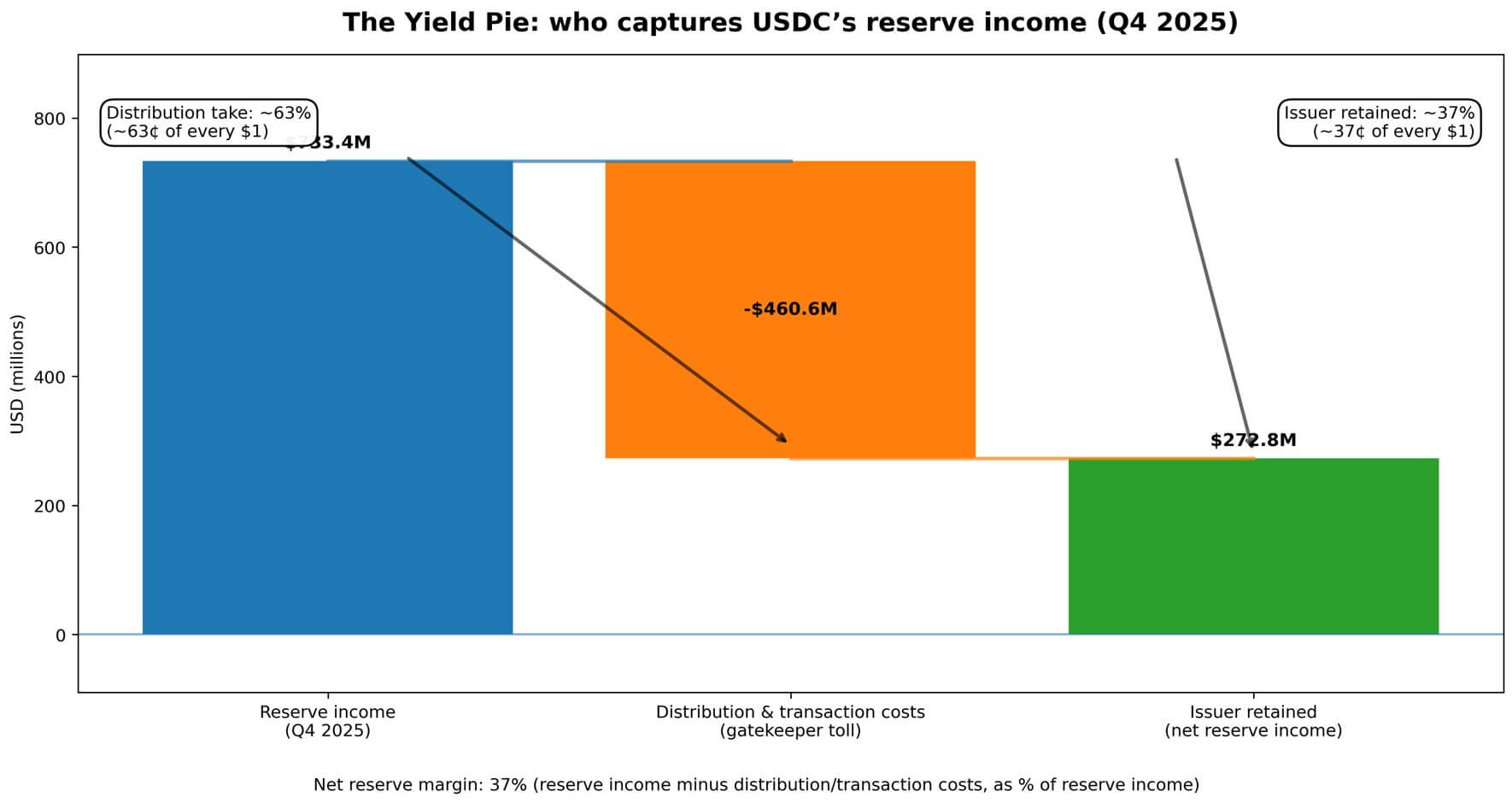

Circle’s Q4 financial report shows $733 million in reserve income, 63% of which was distributed to channel partners.

Author: CryptoSlate / Gino Matos

Translated by TechFlow

TechFlow Intro: Circle’s Q4 data looks impressive on the surface—USDC supply grew 72% year-on-year, and reserve income quintupled. Yet the income statement reveals a harsher reality: for every $1 of reserve income earned, $0.63 flows to exchanges and wallet providers—the gatekeepers controlling user access. This article analyzes the power dynamics among stablecoin issuers, distribution partners, and users through the lens of revenue allocation—and how this system will strain under falling interest rates.

Full Text Below:

Circle’s Q4 earnings tell a story the company hopes investors interpret through a growth lens: USDC circulation grew 72% year-on-year to $7.53 billion; reserve income surged 69%; and adjusted EBITDA grew fivefold.

Yet the income statement tells another story—one where issuers generate revenue, only to immediately cede most of it to platforms controlling user access.

The numbers are stark. Circle’s reserve income for the quarter totaled $733.4 million.

Of that, $460.6 million was consumed by distribution and trading costs—roughly $0.63 of every $1 earned, drawn from investment returns on customer deposits.

Total revenue plus reserve income amounted to $770.2 million, with distribution costs accounting for nearly 60% of all revenue flowing through the business.

What remains for Circle is what’s left after paying the “gatekeepers.”

This isn’t buried in footnotes. Circle reports “Revenue Less Distribution Costs” (RLDC) as a core performance metric—publishing RLDC margin alongside profitability and net income each quarter.

The message to investors is clear: revenue exists—but accessing it requires paying a “shelf fee.” At its core, stablecoin economics is a negotiation between issuers and exchanges, wallets, and fintech channels that control where balances actually reside.

Who Splits the Revenue Pie?

Stablecoins generate revenue via a straightforward mechanism.

Users deposit USD or exchange crypto for stablecoins. Issuers hold those funds as reserves—primarily investing in short-term Treasuries and similar instruments—and earn the prevailing interest rate.

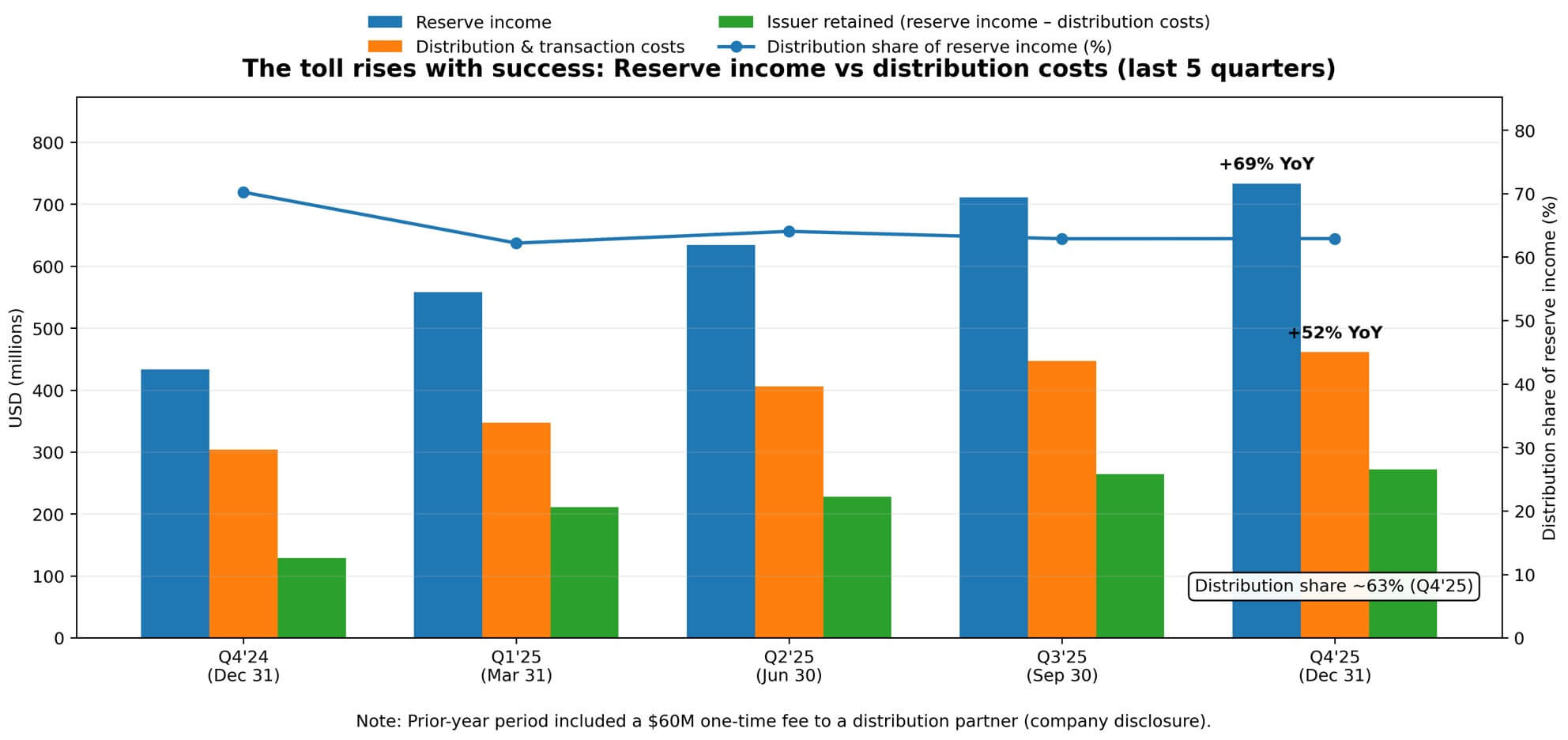

Circle reported a Q4 reserve yield of 3.8%, down 68 basis points year-on-year, reflecting evolving Fed policy. Yet even as rates declined, reserve income rose—because average USDC circulation doubled from $3.81 billion to $7.62 billion.

Scale overwhelmed rate decline. This dynamic lies at the heart of the 52% year-on-year rise in distribution costs.

Circle explicitly attributes this growth to “increased distribution payments,” noting that the prior-year period included a disclosed one-time expense of $60 million.

Excluding that one-time payment, the underlying growth in distribution economics accelerated further. The bigger the pie, the faster the toll rises.

Circle’s net reserve margin—the share of reserve income remaining after deducting distribution and trading costs—held steady at 37% in Q4.

In other words, for every $1 of total reserve income earned, Circle retains roughly $0.37; the rest flows to distribution partners.

This cost structure does not scale easily.

Distribution payments aren’t technology expenses nor fixed overhead dilutable with transaction volume. They’re negotiated economic arrangements tied to channel positioning and fund flows—making them sticky, and potentially rising further as gatekeepers’ bargaining power strengthens.

Distribution “Oligopoly” as Market Structure

“Oligopoly” here is metaphorical—not accusatory. It refers to a small number of gatekeepers who control user access and extract commensurate economic value based on their bargaining power.

Circle’s own risk disclosures state this plainly. The company warns it may “fail to maintain existing relationships with financial institutions and similar enterprises—or establish new ones.” It also highlights the risk of being forced to accept “less favorable financial terms,” and notes “dependence on a limited number of key distributors” as a structural constraint.

These words matter—they position distribution relationships as power negotiations, not supplier engagements. Circle reports a metric called “USDC on Platform,” tracking the share of total USDC held on partner platforms.

That figure reached $12.5 billion at year-end—a 459% year-on-year increase—and averaged 17.8% of total circulation on a daily weighted basis. The company is clearly monitoring where balances concentrate—reinforcing again: whoever controls the channel decides who captures the revenue.

The battleground isn’t stablecoin technology or reserve management—it’s access.

Exchanges, wallets, and payment platforms sit between issuers and users—and monetize that position. Circle can build better products, secure regulatory clarity, optimize reserve returns.

But if a major distributor changes incentives—or threatens to promote a competitor—the economic landscape shifts instantly. Issuer margins hinge entirely on gatekeepers’ terms.

What Happens When Rates Fall?

This structure functions well in an environment where rates hover near a 3% median—where reserve portfolio returns comfortably support both issuer and distributor economics, while still allowing room for margin expansion.

But rates have direction—and the Fed’s path is pivotal. As of late February 2026, Treasury yields—the anchor rate for Circle’s reserve portfolio—remain near the 3% median range. Yet markets anticipate potential rate cuts over the coming quarters.

In a falling-rate environment, if distribution costs remain sticky, issuer economics will deteriorate faster than distributor shares decline.

In one plausible scenario, a 100-basis-point rate cut—with distribution payments fixed or declining slower than reserve income—would further pressure Circle’s RLDC margin.

A second 100-basis-point cut could push issuer economics toward zero—or even negative—under sticky distribution contracts, forcing renegotiation or industry consolidation.

This isn’t speculation. Circle’s guidance already reflects expectations of margin compression relative to Q4’s 40% RLDC margin. The company is pricing for a world where distribution costs do not fall proportionally with reserve income.

This dynamic intensifies competition for the residual spread—driving the entire category toward more aggressive “pay-to-play” arrangements—or structural resets.

The Political Economy of Float

Stablecoins exhibit an unusual political economy.

Users provide float—in Circle’s case, $75 billion—but in most implementations, they receive no direct yield. Issuers earn reserve income but cede most of it to distributors. Distributors capture economic value by controlling access—but bear no balance-sheet risk.

So long as users prioritize convenience and stability over yield, this arrangement holds. But once stablecoins achieve mainstream scale, the question of who should capture that yield becomes increasingly unavoidable.

The GENIUS Act is cited in Circle’s disclosures as legislation relevant to its regulatory environment. As regulatory frameworks formalize, the question of who earns the yield grows harder to sidestep.

If stablecoins function as deposit substitutes, why shouldn’t users earn interest? If they serve as payment rails, why do gatekeepers command such outsized economic shares? If they act as reserve instruments, why can’t issuers retain a larger portion of the spread?

These aren’t rhetorical questions—they’re the foundation for future renegotiations among issuers and distributors, platforms and users, and the industry and regulators.

Circle’s current margin structure reflects its bargaining power at a specific moment—a power that shifts with market share, regulatory posture, and alternative access channels.

The Real Risk Isn’t a Run

Circle’s balance sheet can withstand large-scale redemptions. Reserves are liquid, audited, and conservatively managed.

The operational risk Circle discloses isn’t a classic bank run—but distributor switching: a major partner altering incentives, promoting a competitor, or building its own stablecoin infrastructure.

This risk manifests very differently from credit or liquidity risk. It’s a market-structure risk tied to how stablecoins reach users.

If a top-tier exchange prioritizes another stablecoin, fund flows shift instantly. If a fintech platform integrates a competitor’s rail, distribution economics rebalance.

Issuers have few options: pay more to retain channel placement, accept margin compression, or build direct-to-user distribution channels—a capital-intensive, time-consuming alternative path.

Circle tracks “USDC on Platform” precisely because it must monitor this concentration.

Where balances concentrate determines who holds bargaining leverage. The more USDC concentrates on specific platforms, the more those platforms can demand in negotiations.

An issuer’s margin is simply the residual claim left after distributors take their cut.

The Endgame Question

The shape of stablecoin competition resembles a bidding war for access.

Market share is won not primarily through technical or regulatory advantage—but by establishing and maintaining distribution relationships.

This structure favors issuers with capital to pay channel fees—and distributors with large enough user bases to dominate economies of scale.

Consolidation pressure is obvious.

Falling rates compress issuer margins. When distributors can extract better terms from concentrated relationships, their willingness to support multiple stablecoins declines. Users gravitate toward default options embedded in platforms they already use.

The entire category trends toward fewer issuers, stronger distributors—and compressed margins across both sides as the revenue pie shrinks.

Circle’s Q4 results reflect exactly this logic at scale.

The company generated $733 million in reserve income—and paid $461 million to buy user access. What remains for the issuer before operating expenses is $272 million.

This is the economic reality of stablecoins: they are not just digital dollars—or just interest-rate trades.

They are quarterly negotiations between issuers and gatekeepers over who captures the spread—stakes determined by float size and interest-rate levels.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News