OKLink Research Institute: The Past and Present of the Central Bank Digital Currency DCEP

TechFlow Selected TechFlow Selected

OKLink Research Institute: The Past and Present of the Central Bank Digital Currency DCEP

DCEP adopts a loosely coupled form with bank accounts, meaning DCEP users' wallets do not need to be linked to bank accounts, and transactions and transfers do not rely on bank accounts.

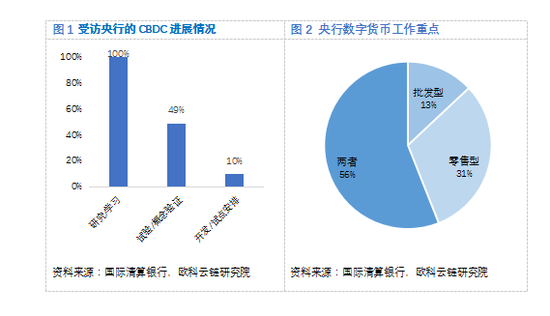

Currently, central banks in multiple countries around the world are conducting research on central bank digital currencies (CBDCs). According to Christian's survey of 63 central banks globally, all respondents have initiated theoretical and conceptual studies on digital currencies, approximately 49% have entered the trial or proof-of-concept phase, and about 10% have moved into development or pilot stages.

From the perspective of usage scenarios and target users, CBDCs are further categorized into general-purpose (also known as retail) and wholesale types. The former primarily serves the public, while the latter is mainly used between central banks and financial institutions. The survey shows that 13% of central banks are researching wholesale CBDCs, 31% are focusing on retail CBDCs, and 56% are studying both types simultaneously.

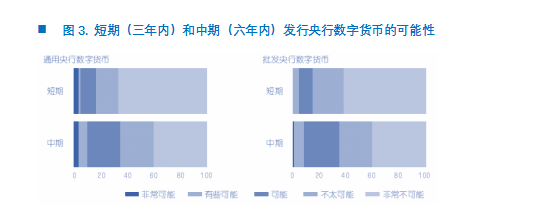

Most countries currently recognize the importance of CBDCs, yet they generally maintain a cautious stance toward issuing them. The survey indicates that in the short term (within three years), over 85% of central banks are unlikely or very unlikely to issue any form of CBDC, with only 3% planning to launch a retail CBDC shortly.

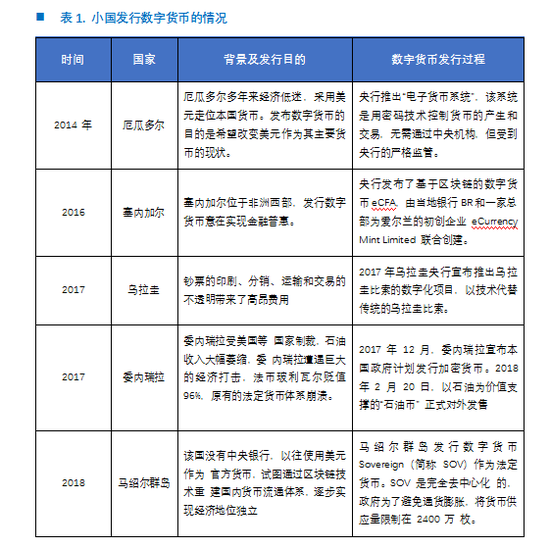

Most central banks planning near-term issuance are from smaller nations, often aiming to overcome economic difficulties or rebuild their national monetary systems. For example, Venezuela—affected by severe domestic inflation and U.S. economic sanctions—launched a cryptocurrency called the Petro in 2018 to escape its crisis. Each Petro was backed by one barrel of Venezuelan crude oil, priced at $60, with an initial supply of 100 million units.

In fact, since Bitcoin's emergence, the technology for issuing digital currencies has matured. Today, when even private entities and individuals can develop digital currencies, it is no longer technically difficult for central banks to issue their own. The key question lies elsewhere: What kind of CBDC do we actually need?

CBDCs bring not only increased complexity to currency operations but also broader impacts on the financial system. Blindly launching a CBDC may fail to achieve intended goals and could easily end in failure. As seen in Venezuela, after introducing the Petro, the country’s financial situation did not improve, U.S. sanctions were not avoided, and residents even began selling off large amounts of Petros.

A true CBDC involves much more than mere issuance. The real focus lies in how it can better serve socioeconomic development, support central bank policy objectives, and meet financial regulatory requirements during circulation and transactions. As Zhou Xiaochuan stated: "CBDC should reflect several principles: first, providing convenience and security; second, balancing privacy protection with maintaining social order and combating illegal activities; third, supporting effective implementation and transmission of monetary policy; fourth, preserving control over monetary sovereignty."

Currently, DCEP has largely completed top-level design, standard setting, functional development, and testing, with pilots conducted in cities such as Shenzhen and Suzhou. In terms of disclosed functionality and operations, China’s DCEP stands out as the first genuine CBDC in practice. Its specific design details are as follows:

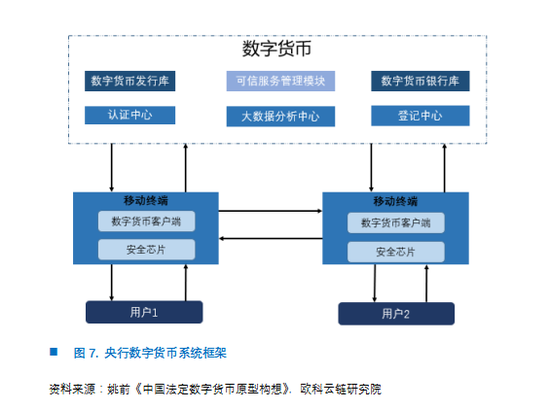

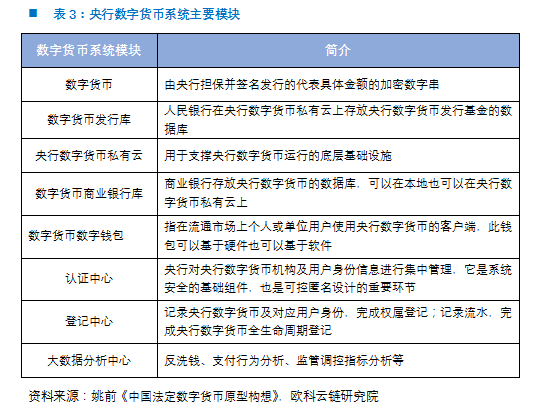

(1) Issuance Layer: One Coin, Two Wallets, Three Centers

As explained by Yao Qian in his article "Conceptual Design of China's Legal Digital Currency," the core framework of the CBDC system consists of "one coin, two wallets, three centers." Here, "one coin" refers to the central bank digital currency itself; "two wallets" refer to the digital currency issuance wallet and the commercial bank digital currency wallet; and "three centers" denote the certification center, registration center, and big data analysis center.

Based on publicly available information, DCEP has two major characteristics: first, it substitutes for M0; second, it bears no interest.

In monetary classification, M0 refers to cash in circulation, M2 includes M0 plus demand deposits, and M3 adds time deposits and savings deposits to M2. Classifying DCEP under M0 is appropriate because CBDC is essentially electronic cash—transforming the physical carrier of money from paper or metal into digital form.

DCEP does not accrue interest primarily to safeguard the stability of commercial bank deposits. Since DCEP is inherently safer than bank deposits, adding interest would incentivize people to shift funds from banks to personal digital wallets, triggering "financial disintermediation." However, if DCEP were to bear interest, it could help overcome the constraints of the "liquidity trap," making negative interest rate policies more effective—an option that cannot be ruled out in the future.

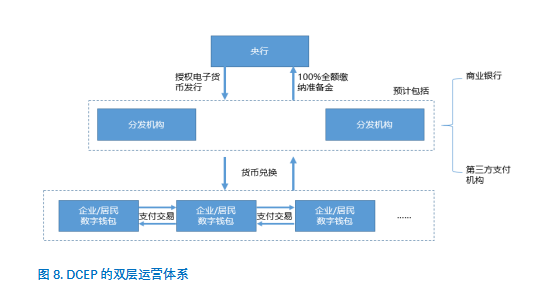

(2) Operational Layer: Two-Tier Operating System

For CBDC operations, DCEP adopts a two-tier system—"central bank to commercial banks/other operating institutions," meaning the central bank first exchanges DCEP with commercial banks or other designated institutions, which then distribute it to the public. This structure is based on three main considerations:

First, adopting a single-tier system would require the central bank to directly serve all DCEP users, reverting to the era of a monolithic, centrally controlled banking system under a planned economy. This contradicts modern central banking functions and hinders DCEP’s long-term development.

Second, commercial banks and payment institutions already possess mature IT infrastructure and service systems. A two-tier model encourages these institutions to conduct R&D on DCEP, fostering market competition and leveraging their talent and technological advantages.

Third, and most importantly, DCEP holds competitive advantages over traditional bank deposits. A single-tier system could lead directly to deposit outflows from banks, causing financial disintermediation. Hence, a two-tier system helps mitigate disruptions to the existing financial system.

Under this two-tier system, DCEP demonstrates two key features:

Commercial banks must deposit 100% reserves with the central bank before distributing DCEP, ensuring that DCEP represents real value, constitutes a liability of the central bank, is guaranteed by central bank credit, and qualifies as sovereign national currency.

DCEP uses a bank-account-deregulated wallet model—users’ wallets do not need to be linked to bank accounts, and transactions do not rely on bank account systems, marking a fundamental difference from third-party payment platforms like Alipay and WeChat Pay.

(3) Payment Terminals

At the user terminal level, DCEP exhibits three primary features:

First is the balance between privacy protection and crime prevention. DCEP protects users' legitimate privacy needs in daily economic activities through controllable anonymity. Traditional internet payments and card transactions cannot achieve anonymity due to their linkage with bank accounts, whereas DCEP enables it. At the same time, to combat money laundering and terrorist financing, transaction data will be disclosed to the central bank, and big data analytics will be employed to detect suspicious behavioral patterns.

Second is the dual offline payment capability. Unlike online banking or third-party payment tools such as Alipay, which require network connectivity, DCEP allows transactions even when both parties are offline—simply touching two phones together to exchange wallet keys completes the transfer.

Primarily designed for small-value retail use, DCEP imposes limits on transaction amounts and duration. While current technical patents from the central bank have not detailed how the "double-spending problem" is resolved under dual-offline conditions, this issue isn't solely solvable by technology. Legal frameworks and regulatory mechanisms can deter malicious behavior or enable recovery after double spending occurs. Additionally, restricting DCEP to low-value, time-limited retail scenarios helps prevent abuse. These limitations also aim to protect commercial banks and avoid financial disintermediation.

With these characteristics, DCEP differs significantly from familiar assets such as physical cash, third-party payment balances, bank deposits, and Bitcoin in terms of debt relationships, legal status, and risk-return profiles, as illustrated below.

Notably, in terms of function and form, since the People's Bank of China mandated full reserve deposits in 2019, Alipay and WeChat Pay balances have become closest to DCEP. However, industry practice still classifies Yu’e Bao and WeChat funds under M2 (deposits at non-deposit-taking financial institutions). There remain differences between them and DCEP regarding bank account coupling, user privacy protection, and offline payment capabilities.

Similarly, compared with stablecoins like Libra and USDT, CBDCs are issued by governments, whereas Libra and USDT are privately issued digital currencies backed by dollars or other fiat currencies. Legally, DCEP has unlimited legal tender status—merchants cannot refuse it as payment—while Libra and USDT lack such status and can be rejected by merchants.

Historically, money has always evolved alongside technological progress and economic development—from early commodity and precious-metal money to modern credit-based currencies—all natural adaptations to advancing commercial societies. As the previous generation of currency, paper money suffers from low technological sophistication and, considering security and cost, is inevitably destined to be replaced by new technologies and products. Especially given the rise of the internet and sweeping changes in global payment methods, establishing a digital currency issuance and circulation system plays a crucial role in strengthening financial infrastructure and driving economic efficiency and upgrading. It is believed that once officially launched, DCEP will have significant implications for China and the global economy.

Author Bio:

OKLink Research Institute is the research arm of OK Group, focusing on blockchain industry and digital currency research. It collaborates closely with governments, enterprises, and academic institutions and enjoys recognition within the industry. OKLink Group is a leading global blockchain company headquartered in Beijing, China, with subsidiaries or offices in over 10 countries including the United States, Europe, South Korea, and Japan. OKLink is listed on the Hong Kong Stock Exchange.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News