A Brief Analysis of the Similarities and Differences Between DeFi Liquidity Mining and Bitcoin Mining

TechFlow Selected TechFlow Selected

A Brief Analysis of the Similarities and Differences Between DeFi Liquidity Mining and Bitcoin Mining

The way liquidity mining works is very similar to proof-of-work mining, with differences lying in priorities and implementation methods.

Author: Deribit Market Research

Translation: Moni

Although the concept of liquidity mining has existed for some time, it remained relatively quiet until recently.

That changed when the decentralized finance (DeFi) protocol Compound introduced a new mechanism and began distributing its governance token, COMP, to users—sparking widespread interest in liquidity mining.

As the name suggests, liquidity mining refers to rewards users receive for providing liquidity to lending and borrowing markets within DeFi protocols, in addition to their regular yield.

The DeFi community has coined quirky new terms for liquidity mining, such as "Yield Farming" and "Crop Rotation," among others.

Yet behind the scenes, you might find that the way liquidity mining works is actually quite similar to Proof-of-Work (PoW) mining.

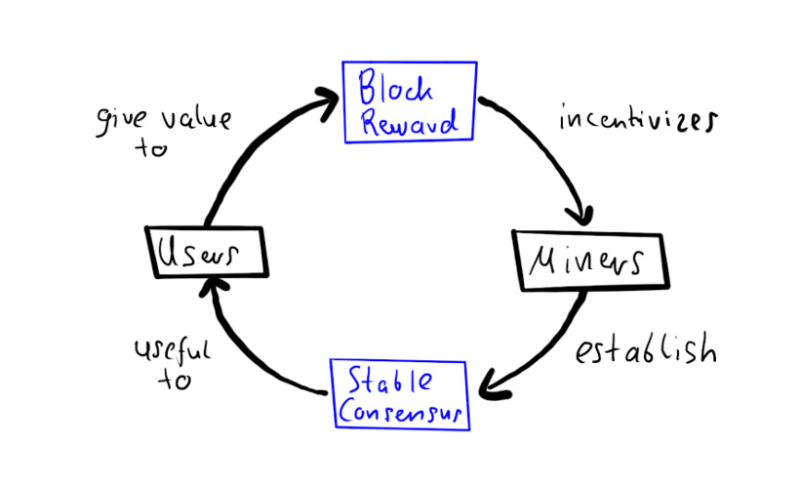

In both Bitcoin and Ethereum networks, Proof-of-Work (PoW) mining serves two primary functions:

-

Initial distribution of circulating tokens;

-

Rewarding miners for performing valuable services—specifically, proving blocks—which enables distributed consensus. This mechanism gives value to the bitcoins purchased by end users.

At a high level, the operation of liquidity mining resembles PoW mining: take Compound as an example, where 0.44 COMP tokens are distributed per Ethereum block to the market. This "reward" holds value for market participants—especially now that COMP has become a tradable asset. To earn these rewards, participants provide a highly valuable service to Compound: supplying liquidity.

Of course, there are also two key differences between PoW mining and liquidity mining:

-

Different priorities in objectives;

-

Different implementation mechanisms.

Let’s examine these differences in detail:

Different Priorities

In PoW mining, paying miners to validate blocks is arguably more critical than fairly distributing tokens in DeFi. Without block validation, there can be no distributed consensus or functional blockchain. Token distribution is essentially a side effect—one that can even be pre-mined (as seen with certain tokens on Ethereum)—yet still result in a working blockchain.

However, this priority is reversed in the Compound protocol. Technically speaking, Compound does not need to pay liquidity providers to function properly, which alleviates concerns that liquidity mining might resemble a Ponzi scheme. COMP tokens hold positive value because holders who participate in liquidity mining can earn future fees from the protocol. We can compare this distribution model to earlier practices in DeFi, where early investors would pre-mine tokens and later sell them on the open market.

Compound chose to distribute COMP tokens to a broader base of holders for several reasons:

-

Token distribution itself attracts new users—a dynamic similar to how CPU/GPU mining drew participants into the cryptocurrency space;

-

COMP tokens grant voting rights over proposed changes to the Compound protocol. With ownership widely distributed, the community is less likely to fall victim to Byzantine faults or implement short-sighted changes—issues historically common in highly centralized entities;

-

When users earn tokens through active participation rather than passive repayment to early investors, it becomes easier to convince regulators that COMP is not a security.

Different Implementation Mechanisms

First, it's important to note: both Bitcoin and Compound exert a degree of control over actions when distributing rewards. Through this "control," both systems create specific incentives for participants.

In Bitcoin, the incentive structure encourages miners to include as many transactions as possible and validate them promptly, while consistently building on the longest chain. Collectively, mechanisms like proof-of-work, block proposers, timestamps, and incentives make Bitcoin a trustless electronic cash system. Miners must follow this specific strategy to ensure network security—a framework known as "Nakamoto Consensus."

Properly designed incentives are crucial here. Nakamoto Consensus is clearly defined such that following the protocol should always be the most profitable strategy for miners. Satoshi may have assumed that a well-aligned mining protocol could resist collusion by minority groups and encourage miners to act according to the rules. In economic theory, rational individuals act in self-interest; if institutional arrangements can align personal gain with collective goals, the system achieves optimal outcomes.

However, in a 2013 paper, Eyal and others argued that Nakamoto Consensus isn't perfect, introducing a strategy called "Selfish Mining" that allows small mining pools to earn more than they would under honest behavior. This approach could destabilize Bitcoin and promote centralization. While clear evidence of selfish mining remains absent in practice, the risk persists.

By contrast, Compound has significantly evolved and improved its incentive design for liquidity providers. This flexibility exists because Compound offers multiple incentive strategies—users must spend COMP tokens to perform almost any action within the protocol.

Indeed, this design is intentional: unlike Bitcoin, whose goal is to incentivize a specific behavior (mining), Compound prioritizes broad token distribution over enforcing particular user behaviors.

Consider a counterexample: Synthetix, a DeFi protocol that uses its SNX token in a more targeted manner. To maintain the peg of its synthetic stablecoin sUSD, Synthetix rewards liquidity providers who add liquidity to Dai/USDC/USDT/sUSD pools on Curve.

For a period, however, BAT dominated COMP mining yields, nearly monopolizing liquidity provision. Generally, higher deposit rates lead to greater COMP mining efficiency. But miners strictly followed the incentive structure, as their COMP reward share was based on interest paid. Simply increasing BAT deposits wouldn’t raise rates, since interest rates depend directly on supply-to-borrow ratios. As a result, large BAT holders deposited other assets, increasing collateral until they borrowed out all previously deposited BAT—creating a "pay-interest-to-earn-interest" cycle. This drove up capital utilization but marginalized mainstream assets using real supply and demand, denying them fair incentives.

Conclusion

Compound quickly patched its distribution mechanism in response, yet the fundamental question remains: Is there a better alternative incentive strategy?

Indeed, Compound lacks a "Nakamoto Consensus"—there is no required strategy miners must follow. Still, ideally, at least some rewards should avoid capture by exploitative strategies. Simple users depositing USDC and USDT into Compound resemble the most accessible and stable sources of capital in traditional banking. Regardless, attracting billions in bank-like deposits into crypto represents a major success for systems like Compound.

Ultimately, both liquidity mining and Proof-of-Work require trade-offs.

Rather than designing one very specific incentive strategy and building a distributed protocol around it, we may need to prioritize the protocol from a mining perspective—enabling many types of activity to be rewarded and encouraging a wider range of potential incentive models.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News