Bitget UEX Daily Report | Ceasefire expectations rise, and all three major U.S. stock indices hit record highs; Dell’s earnings beat expectations, spurring a sharp overnight rally; Anthropic’s valuation surpasses OpenAI

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Ceasefire expectations rise, and all three major U.S. stock indices hit record highs; Dell’s earnings beat expectations, spurring a sharp overnight rally; Anthropic’s valuation surpasses OpenAI

Overall, AI and technology growth remain the medium-term core theme. Investors are advised to balance geopolitical risks with fundamental opportunities and seek structural investment opportunities amid market volatility.

I. Top News Highlights

Federal Reserve Updates: Fed Officials Warn Against Relying on AI to Ease Inflation

- St. Louis Fed President Musalem stated that productivity gains from AI cannot be relied upon to resolve current high inflation—contradicting Chair Waller’s view.

- He emphasized that current interest rates remain below neutral, the labor market is stable, yet inflation remains significantly above the 2% target and longer-term expectations are rising.

- PCE data showed a 3.8% year-on-year increase in April, reinforcing inflation concerns. Market impact: This commentary may constrain near-term rate-cut expectations, support the U.S. dollar, and pressure highly valued tech stocks—though AI-driven productivity gains could still alleviate long-term inflationary pressures if realized.

Global Commodities: Ceasefire Optimism Drives Oil Volatility; Gold & Silver Margin Requirements Reduced

- U.S.-Iran negotiations continue; Treasury Secretary Bessent reiterated red lines and warned Oman against imposing fees in the Strait of Hormuz. Iran has not formally endorsed the memorandum, but markets remain optimistic about a timely reopening of the Strait.

- Goldman Sachs estimates global crude oil inventories are nearing the 100-day warning threshold, with visible inventories even lower.

- CME reduced margin requirements for gold and silver futures. Market impact: Ceasefire optimism eases energy supply disruption risks, pressuring oil prices downward; volatility in precious metals may decline short-term, though geopolitical uncertainty continues to underpin safe-haven demand.

Macroeconomic Policy: EU Plans Massive Investment to Revitalize Chip Industry

- The EU intends to deploy €120 billion in public-private funding by 2035 via the “Chips Act 2.0,” prioritizing construction of new AI-focused semiconductor wafer fabs.

- The initiative aims to bolster domestic chip demand and manufacturing capacity, mitigating global supply chain risks. Market impact: This move may strengthen Europe’s tech supply chain and resonate with U.S.-China competition, exerting long-term influence on global semiconductor pricing and geopolitical tech dynamics.

II. Market Recap

Commodities & FX Performance

- Spot Gold: +0.01%, back to $4,500/oz.

- Spot Silver: +0.07%, at $75.70/oz.

- WTI Crude: -0.75%, at $88.22/barrel.

- Brent Crude: -0.55%, at $92.00/barrel.

- U.S. Dollar Index: +0.01%, at 99.007.

Cryptocurrency Performance

- BTC: -0.96%, at $73,826.

- ETH: -0.61%, at $2,015.

- Total Crypto Market Cap: -0.8%, at $2.56 trillion.

- Liquidations: ~$756 million liquidated in the past 24 hours, with $752 million in long positions.

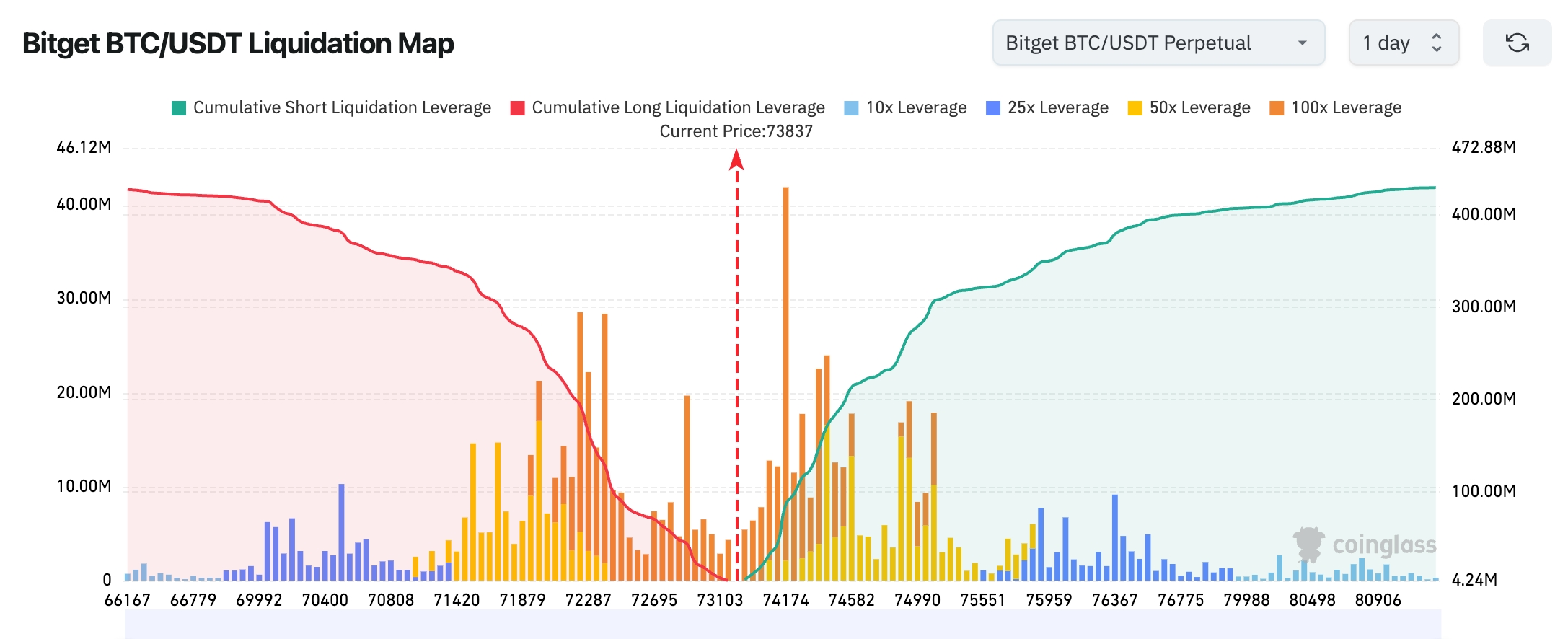

- Bitget BTC/USDT Liquidation Map: BTC is currently trading near $73,837. A dense cluster of high-leverage short liquidations lies between $74,100–$75,000; further upward momentum could trigger short covering and accelerate rallies. Conversely, heavy long leverage is concentrated near $72,000–$73,000; a breakdown below this zone may trigger cascading long liquidations, amplifying short-term volatility.

- Spot ETF Net Flows: BTC spot ETFs recorded $733 million in net outflows yesterday—the eighth consecutive day of net outflows.

U.S. Equity Index Performance

- Dow Jones Industrial Average: +0.05%, at 50,678.45—near an all-time high, supported by defensive sectors.

- S&P 500: +0.58%, at 7,563.28—setting successive record closing highs, clearly driven by tech and growth stocks.

- Nasdaq Composite: +0.91%, at 26,906.54—with AI-related sectors leading strength.

Tech Giants’ Performance

- Apple (AAPL): +0.53%, at $312.51—core consumer electronics business remains solid, with service revenue continuing to grow steadily.

- Microsoft (MSFT): +3.47%, at $426.99—strong Azure AI cloud demand lifts overall earnings expectations.

- NVIDIA (NVDA): +0.78%, at $214.25—AI chip demand remains robust, with data center operations as the primary growth engine.

- Google (Alphabet, GOOGL): +0.33%, at $390.13—search and cloud businesses steady, AI integration progressing visibly.

- Amazon (AMZN): +0.73%, trading in the $273–$274 range—e-commerce and AWS synergies driving notable cloud revenue growth.

- Meta (META): +0.01%, at $635.29—robust advertising business provides strong support; long-term investments in metaverse and AI continue.

- Tesla (TSLA): +0.40%, at $442.10—energy storage and autonomous driving draw investor attention, though delivery fluctuations affect short-term performance.

Summary: The Magnificent Seven broadly strengthened, with AI remaining the dominant driver. Microsoft and NVIDIA—core AI beneficiaries—led gains. Dell Technologies stood out after-hours following an earnings beat, surging over 30–38%. Geopolitical easing and Fed officials’ comments jointly shaped the current risk sentiment landscape.

Sector Rotation Observations

Semiconductors / AI Hardware: Up >2.8%

- Key names: Dell Technologies (DELL) +3.84% (up nearly 38–40% after-hours), NVIDIA (NVDA) +0.78%, Broadcom (AVGO) modestly higher.

- Catalyst: Dell’s Q1 results vastly exceeded expectations—AI server revenue surged 757% YoY to $12.1 billion, exceeding its full prior fiscal year’s total shipments. Its AI backlog stands at $14.4 billion, underscoring rapid enterprise-level AI capital expenditure acceleration. Market confidence in long-term AI infrastructure demand surged, lifting the entire semiconductor value chain.

Energy Sector: Down 1.5%–2.0%

- Key names: Exxon Mobil (XOM) -1.8%, Chevron (CVX) -1.6%.

- Catalyst: Optimism around U.S.-Iran ceasefire talks—and potential reopening of the Strait of Hormuz—eased supply disruption fears, weighing on oil prices and compressing energy stock risk premiums.

Defensive / Consumer Staples: Up modestly 0.6%–1.1%

- Key names: Procter & Gamble (PG) +0.9%, Coca-Cola (KO) +0.7%.

- Catalyst: Amid easing geopolitical tensions but persistent macro inflation concerns, investors partially rotated into more defensive, essential consumer goods seeking stability.

Other Notable Sectors:

- Industrials / Infrastructure posted moderate gains, buoyed by the EU’s Chips Act 2.0 investment plan—supply-chain-linked equities benefited.

- Overall market: Clear sector rotation—AI and growth themes remain strong, while cyclical sectors diverge due to shifting geopolitical expectations, reflecting investor caution amid improving risk appetite.

III. Deep Dive: U.S. Equity Analysis

1. Dell Technologies (DELL) – Earnings Beat Overview: Dell reported Q1 revenue of $23.4 billion (+5% YoY), with Infrastructure Solutions Group (ISG) revenue reaching $10.3 billion (+12% YoY). Server and networking revenue hit a record $6.3 billion (+16% YoY). AI server orders totaled $12.1 billion—exceeding its entire prior fiscal year’s shipment volume—and AI backlog reached $14.4 billion. The company guided $7 billion in AI server shipments for Q2, significantly raising prior forecasts—signaling a decisive shift from AI pilot phases to large-scale deployment. Market Interpretation: Goldman Sachs, Morgan Stanley, and others raised price targets substantially, citing Dell’s unique full-stack AI server integration capabilities and flexible financing/deployment services that lower enterprise transformation barriers. Analysts note that while memory supply constraints persist, the $14.4 billion backlog offers exceptional visibility; FY2026 AI server revenue is now expected to reach $15–16 billion—well above prior consensus. Investment Takeaway: The AI CapEx cycle has entered a validation phase. As a mid-tier integrator, Dell exhibits greater elasticity than pure-play chipmakers. Investors should closely monitor backlog conversion rates and gross margin trends as leading indicators of sustainable AI infrastructure demand—and avoid chasing momentum blindly at elevated valuations.

2. Super Micro Computer (SMCI) – Strong AI Server Demand Synergy Overview: As a core Dell partner, Super Micro is seeing accelerated order growth in liquid-cooled, high-density GPU servers—directly benefiting from the conversion of Dell’s $14.4 billion AI backlog. The company rapidly responds to custom requirements amid global data center expansion, with FY2026 Q3 revenue reaching $10.24 billion and AI server contribution rising steadily—reflecting tight supply conditions driven by dual demand from hyperscalers and enterprises. Market Interpretation: Investment banks widely applaud SMCI’s agility and delivery speed in AI server assembly, though they caution about supply chain stability and gross margin volatility. Institutions highlight the ecosystem loop formed with NVIDIA and Dell, expecting continued growth momentum through 2026–2027—especially as liquid cooling becomes industry-standard, potentially expanding SMCI’s market share further. Investment Takeaway: Mid-to-lower-tier players in the AI infrastructure stack offer higher beta and serve well as cyclical intensity barometers. Investors should dynamically assess demand authenticity using Dell’s order data alongside SMCI’s quarterly shipment volumes—and seek tactical allocation opportunities amid supply chain developments.

3. Microsoft (MSFT) – AI Cloud Services Driving Growth Overview: Microsoft shares rose ~3.47% to $426.99. Azure’s AI integration advanced faster than expected, with enterprise Copilot adoption and OpenAI model deployments accelerating. Azure grew 40% YoY in FY2026 Q3, with intelligent cloud revenue playing a standout role. Amid macro inflation concerns, its software subscription model demonstrated strong defensive qualities, with AI-related annualized revenue surpassing $37 billion. Market Interpretation: Goldman Sachs, Morgan Stanley, and others maintain top ratings, emphasizing Microsoft’s first-mover advantage in enterprise AI use cases and deep ecosystem lock-in via its OpenAI partnership—making it the most certain AI application-layer beneficiary. Some analysts caution about client acceptance of rising LLM training costs and potential antitrust scrutiny over cloud market concentration—but overall remain bullish on Microsoft’s pricing power as it transitions from “selling compute” to “selling solutions.” Investment Takeaway: Platform giants exhibit stronger cash flow stability and countercyclical resilience compared to hardware names during AI cycles. Investors should prioritize tracking Azure’s sequential growth and AI revenue share as key leading indicators of AI commercialization progress.

4. Broadcom (AVGO) – Semiconductor Supply Chain Synergy Overview: Broadcom rose modestly alongside the AI hardware sector, with robust demand for its custom AI accelerators and data center networking solutions. The company projects AI chip revenue to exceed $100 billion by 2027, having secured major TPU orders from Anthropic ($1 GW in 2026, $3 GW in 2027)—directly linked to Dell’s AI server orders—underscoring its strategic position in the HPC supply chain. Market Interpretation: Bernstein, Mizuho, and others maintain Strong Buy ratings, highlighting Broadcom’s moats in custom ASICs and 400G SerDes technology, plus its diversified customer base (cloud providers + enterprises) delivering countercyclical resilience. Analysts note that despite elevated short-term valuations, dual drivers—AI training and inference—will sustain long-term growth, amplified by significant supply chain scale advantages. Investment Takeaway: “Pick-and-shovel” players in the semiconductor value chain are gaining prominence as defensive AI core holdings. Investors should diversify across upstream/downstream names and focus on AI revenue share growth and gross margin stability to capture structural benefits as the industry evolves from hardware expansion toward application adoption.

5. NVIDIA (NVDA) – Sustained High AI Chip Demand Overview: NVIDIA rose 0.78% to $214.25. Q1 revenue totaled $44.1 billion (+69% YoY), with data center revenue hitting $39.1 billion (+73% YoY). Its Blackwell NVL72 AI supercomputer has entered mass production; AI inference token generation increased tenfold within a year, and sovereign AI infrastructure demand remains strong globally. Market Interpretation: Analysts broadly endorse long-term growth prospects—even amid stretched valuations—anticipating persistent AI compute supply-demand imbalances. Institutions cite NVIDIA’s end-to-end AI solution leadership—from GPUs to software ecosystems—as key to capturing global AI CapEx waves, though geopolitical export restrictions and competitor advances warrant monitoring. Investment Takeaway: AI hardware remains the medium-term theme, but downstream validation (via Dell, SMCI earnings) is critical. A core-plus-satellite portfolio strategy helps mitigate single-stock concentration risk; watch Blackwell ramp timing as a key near-to-medium-term catalyst.

6. Anthropic – Valuation Hits $96.5 Billion Overview: AI startup Anthropic’s latest funding round values it at $96.5 billion—surpassing OpenAI—to become one of the world’s most valuable AI companies, signaling intense investor enthusiasm for Claude models and their ecosystem. Market Interpretation: Multiple investment banks highlight Anthropic’s competitive edge in enterprise AI applications, though its lofty valuation sparks sustainability debates. Investment Takeaway: The AI space is increasingly fragmented, with premium valuations accruing to leaders—focus on actual revenue conversion capability.

IV. Cryptocurrency Project Updates

1. Julio Moreno, Research Head at CryptoQuant, noted that accumulation by Bitcoin “whales” (wallets holding 1,000–10,000 BTC, excluding exchanges and mining pools) and “dolphins” (wallets holding 100–1,000 BTC, primarily ETFs and corporate treasuries) has stalled, indicating sustained weak demand. Whale balances are contracting YoY at the fastest pace this year, while dolphin balances—though still positive YoY—have sharply decelerated, with both groups registering near-zero MoM growth. This signals a persistent slowdown in structural demand drivers. Although long-term holder supply reached a record 15.8 million BTC, this is not bullish—it reflects insufficient short-term demand to absorb tokens held by long-term holders.

2. Newly released official documentation shows Tether’s USAT supply rose nearly 540% MoM—from ~22 million in March to over 140 million in April—with total reserves concurrently increasing to ~$141 million. This implies a reserve surplus of ~$327,000 relative to circulating tokens.

3. Grayscale disclosed in an updated filing for its Hyperliquid ETF that it is negotiating with Hyper Holdings Global LP to make a seed investment of ~2 million HYPE tokens (~$115 million) in exchange for fund shares. The filing also changes the fund name from “Grayscale HYPE ETF” to “Grayscale Hyperliquid Staking ETF,” with Nasdaq ticker HYPG.

4. OTC whale 0xFB7 purchased another 20,000 ETH ($40.48 million) from FalconX and sent $50 million USDT to Wintermute—likely to facilitate further purchases.

5. SEC Chair Paul Atkins posted that regulators have long opposed new technologies and innovation—prompting crypto entrepreneurs to relocate overseas—but declared this era “over.” Under the Trump administration, he stated, the SEC will collaborate with the administration and Congress to deliver “much-needed regulatory clarity” for digital asset markets and advance legislative proposals—including the Digital Asset Clarity Act—to define compliance pathways and regulatory boundaries.

6. Digital asset management firm Grayscale—part of DCG and issuer of products including the Bitcoin spot ETF GBTC—has paused preparations for a U.S. public listing due to unfavorable current market conditions, with plans to resume no earlier than Q4 this year.

V. Today’s Market Calendar

Economic Data Release Schedule

Key Event Forecasts

- U.S.-Iran Negotiations: Monitor updates on the Strait of Hormuz reopening—directly impacting oil prices and risk assets.

- Earnings Season: More tech giants report results; AI remains the central theme.

May 29 (Friday)

- U.S. Chicago PMI for May

- Speech by Kansas City Fed President and 2028 FOMC voter Esther George

- Speech by Fed Governor Michelle Bowman

Institutional Views: Multiple investment banks observe that although geopolitical risks remain volatile, ceasefire optimism has markedly lifted risk sentiment—evidenced by record highs for all three major U.S. indices, reflecting confidence in soft landing and AI-driven growth. Goldman Sachs and others caution that low crude inventories combined with potential supply restoration will cap oil prices, while hawkish Fed commentary constrains rate-cut scope—keeping the dollar and U.S. Treasury yields range-bound. In crypto, post-leveraged-liquidation consolidation may bring short-term recovery, though ETF outflows signal ongoing caution among short-term capital. Overall, AI and tech growth remain the medium-term theme; investors are advised to balance geopolitical risks against fundamental opportunities and seek structural allocations amid volatility.

Disclaimer: The above content was compiled via AI search and verified manually before publication. It does not constitute any investment advice. Data herein may contain inevitable discrepancies; please rely on real-time market data for accuracy.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News