Morgan Stanley Research Report Analysis: Nvidia's Biggest Problem Is No One to Take Over

TechFlow Selected TechFlow Selected

Morgan Stanley Research Report Analysis: Nvidia's Biggest Problem Is No One to Take Over

Against the backdrop of a compute shortage, this could be the starting point for NVIDIA's next phase of valuation restructuring.

Written by: Rita

TechFlow Guide

Growth of 95% last quarter, management says it's accelerating, next year free cash flow yield exceeds 5%, over half may be returned to shareholders. This is the performance Nvidia delivered. But the stock price just won't rise. After intensive exchanges with Jensen Huang and the CFO during last week's roadshow, Morgan Stanley gave a counter-intuitive judgment: the problem is not in fundamentals, but in buyers. Nvidia's market cap is already so large that there isn't enough incremental capital to take over, and the largest potential buyer group may come from a crowd that rarely bought semiconductors in the past. Meanwhile, Nvidia is trying a new business model, exchanging credit support for revenue sharing of cloud services, creating recurring income with 100% gross margin beyond hardware. If this model works, the market's valuation logic for Nvidia needs to be rewritten.

Nvidia's Buyer Dilemma

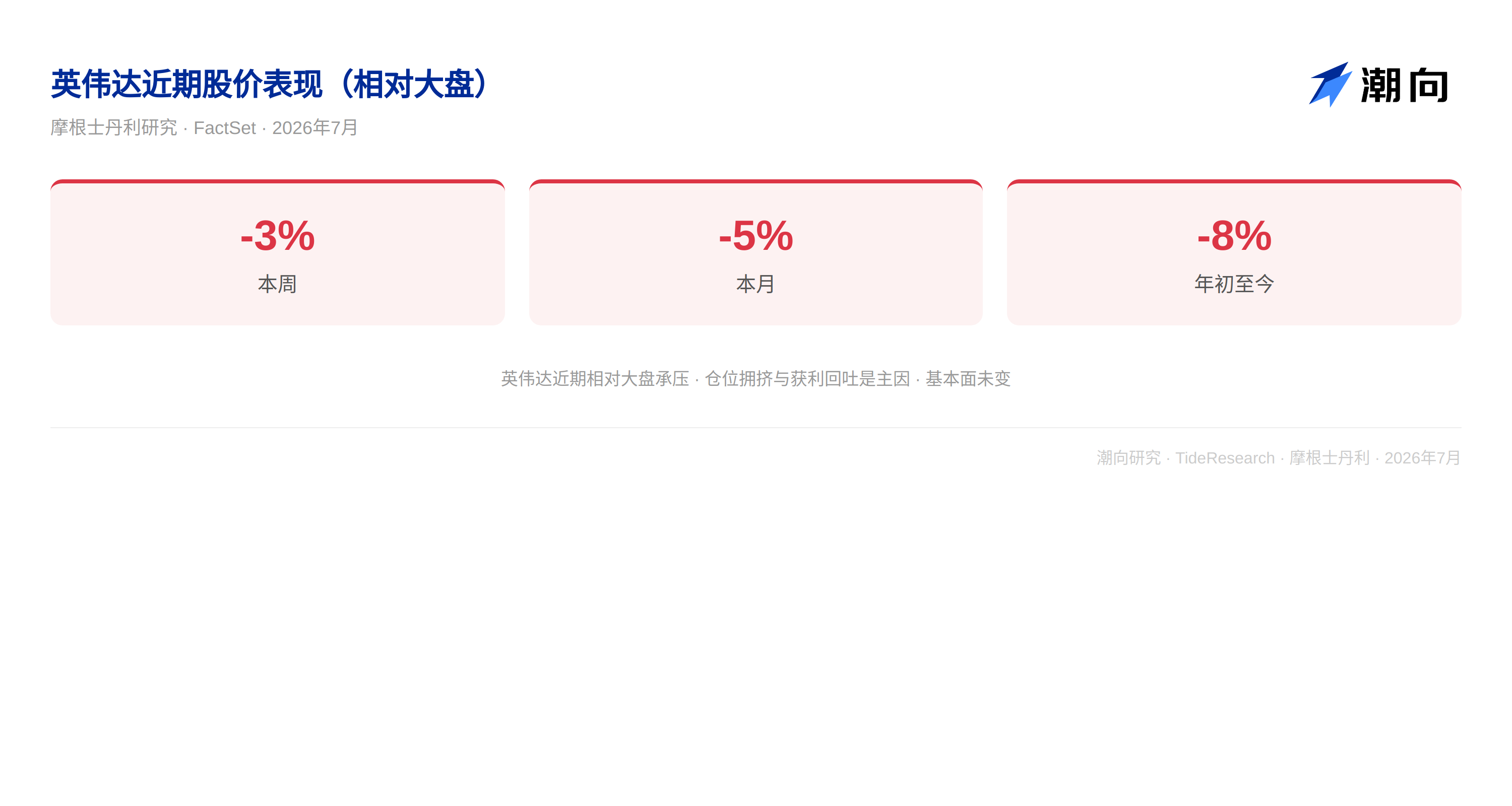

After the roadshow, Morgan Stanley communicated with dozens of investors and found the core problem is: there is no lack of consensus on fundamentals, but a lack of new buyers. When peers generally receive significant buying orders, Nvidia cannot find incremental funds. The reason is straightforward, the size is too large. Value investors and income funds may be the antidote. Quarterly growth of 95%, management says growth is accelerating, next year free cash flow yield exceeds 5% and over half may be returned to shareholders, these indicators naturally fit value capital, while they rarely bought semiconductors in the past. Morgan Stanley believes this is one of the key variables to unlock Nvidia's undervalued value.

Nvidia is Becoming a Computing Power Bank

The NeoCloud financing support model proposed by Nvidia in its blog may be the next big topic. Specific practice: provide credit endorsement for NeoCloud providers in exchange for cloud service revenue sharing, creating recurring income streams beyond hardware sales. Credit support involves costs and risks, but Morgan Stanley points out that against the background of current computing power shortage, the market focus is shifting from "what could go wrong" to "what good results could happen". If it works, this will be recurring income with 100% gross margin. The market hasn't calculated this account clearly yet, because the costs and risks of credit support are not on the income statement.

Memory Shortage Extends the Cycle

Nvidia expects memory shortage to last for several years and is trying to complete tasks with less memory. Morgan Stanley interprets this as a long-term positive for the memory cycle: suppressing price increases in the short term, but extending the high prosperity cycle. Looking at the current memory cycle with area thinking rather than peak thinking, the "total area under the curve" is still quite considerable. At the same time, global computing power and electricity shortages are prompting countries to reserve resources for their domestic enterprises, localization of AI data centers is accelerating, and new deployments are appearing after approval.

TechFlow Perspective

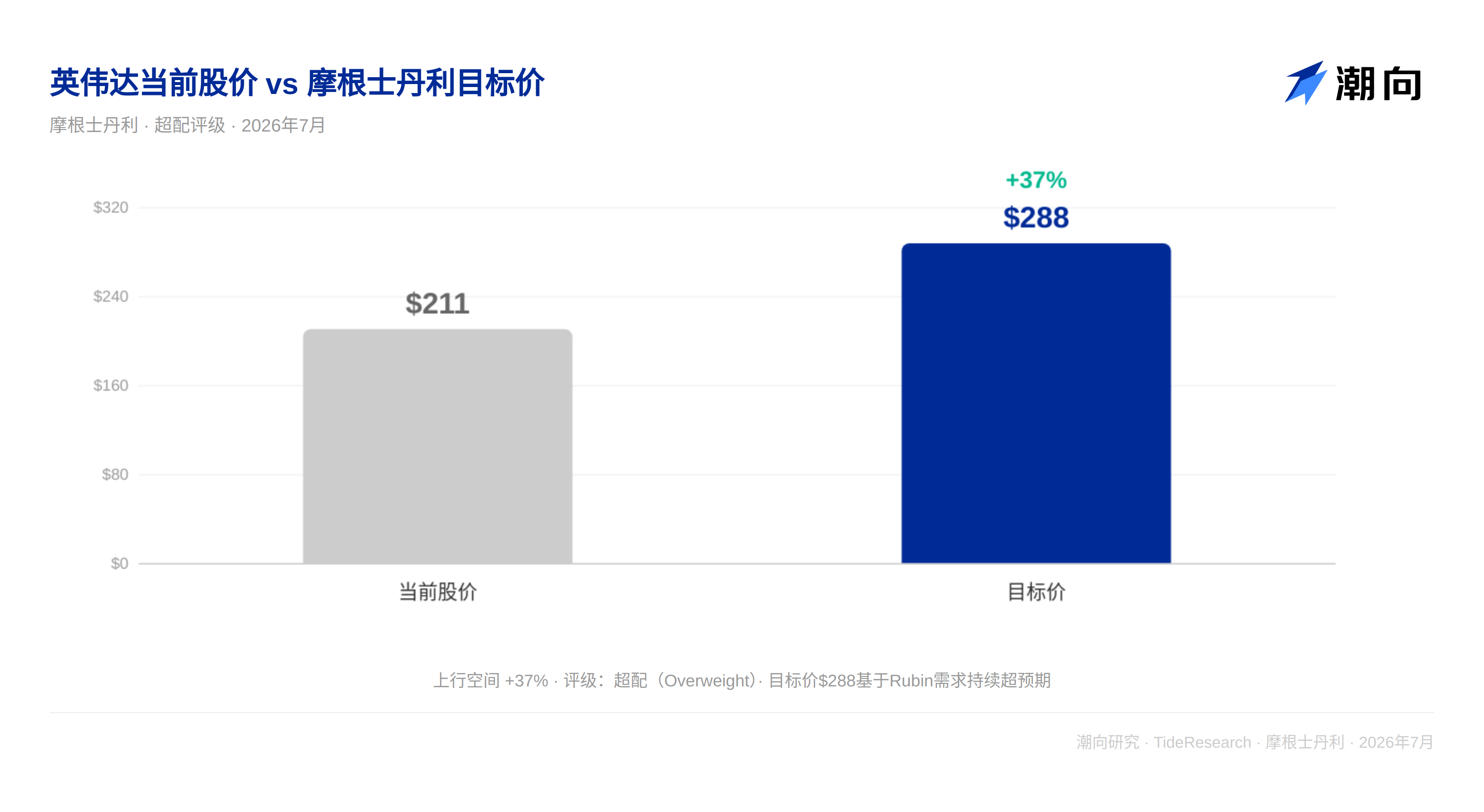

Nvidia's valuation logic is shifting from "selling chips" to "selling credit". The NeoCloud financing support model turns Nvidia from a hardware supplier into a market maker for computing power financialization, providing credit endorsement, exchanging for revenue sharing, and obtaining recurring income with 100% gross margin. If this transformation can work, the valuation anchor will no longer be quarterly GPU shipments, but the yield of the asset pool. Against the background of computing power shortage, this may be the starting point for Nvidia's next phase of valuation restructuring. Morgan Stanley maintains an Overweight rating on Nvidia, with a target price of $288.

Disclaimer

This article is a compilation and interpretation by TechFlow Research of a third-party securities firm research report (Morgan Stanley, July 13, 2026). The ratings, target prices, earnings forecasts, and related judgments cited in the text are the views of the analyst of that securities firm, represent only the position of their affiliated institution, do not represent the views of TechFlow Research, and do not constitute any investment advice.

The market has risks, decisions need to be independent. This article should not be used as a basis for buying or selling any securities.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News