Which companies has NVIDIA’s “three-track architecture” investment system invested in?

TechFlow Selected TechFlow Selected

Which companies has NVIDIA’s “three-track architecture” investment system invested in?

To understand how NVIDIA weaves the AI ecosystem through capital, one must start with its investment system’s “three-track architecture.”

By Ada, TechFlow

Recently, NVentures—the venture capital arm of NVIDIA—announced a new investment in French quantum computing company Alice & Bob, focusing on fault-tolerant quantum computing.

A common misconception is that all of NVIDIA’s external investments fall under NVentures. In reality, this VC unit, founded in 2021, made just 30 investments last year—a total far smaller than even a single strategic investment by NVIDIA’s Corporate Development team. For instance, its $2 billion equity investment in Synopsys at the end of 2025 alone was several times NVentures’ cumulative investment volume over the past three years.

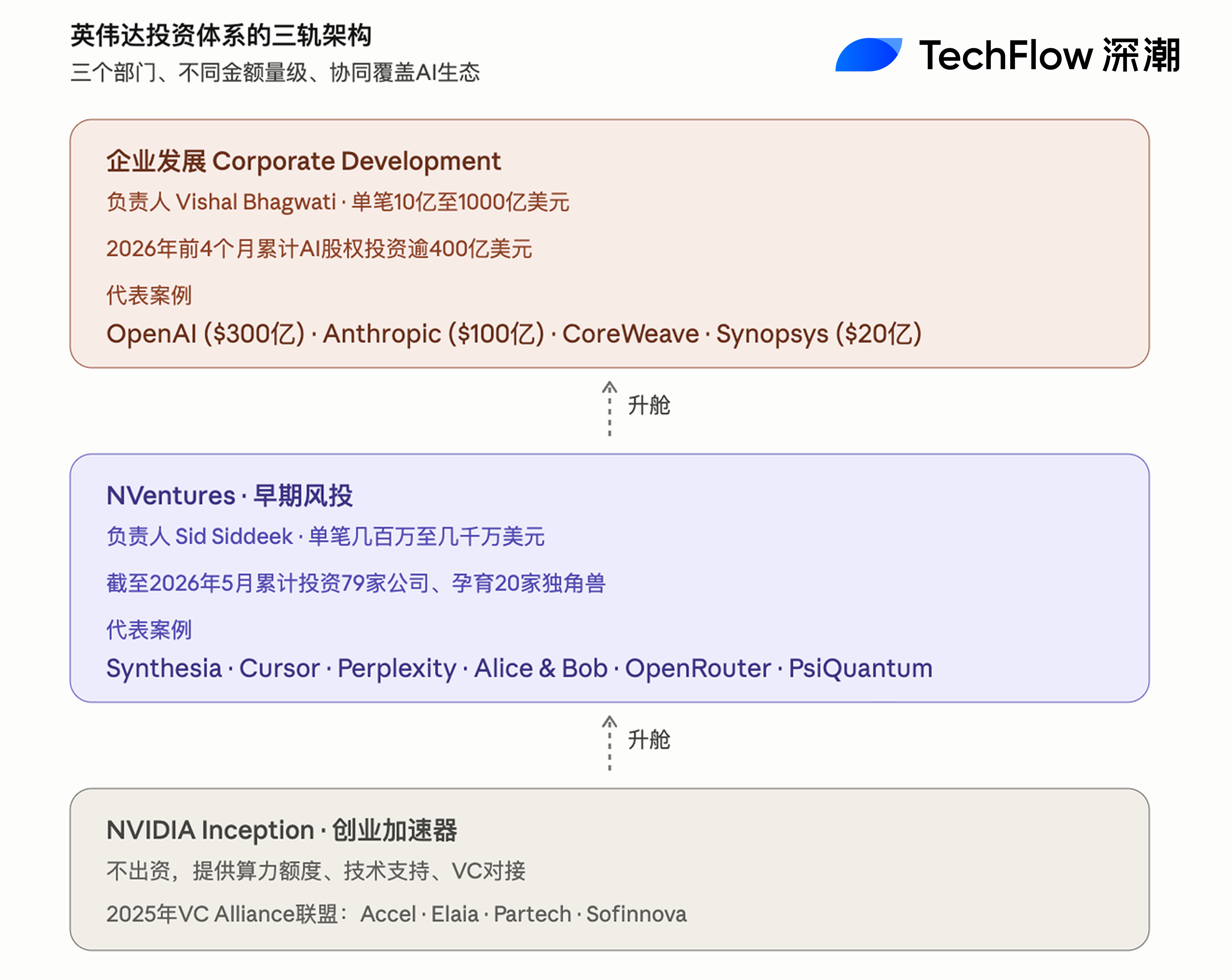

To understand how NVIDIA deploys capital to build its AI ecosystem, one must start with its “three-track” investment architecture: the Corporate Development team handles multi-billion- to trillion-dollar strategic investments and acquisitions; NVentures focuses on early-stage, sector-agnostic financial investments; and NVIDIA Inception functions as a startup accelerator—providing resources but no direct funding. Together, these three tracks form the largest and fastest-moving capital deployment machine in Silicon Valley history—and also the central target of short-seller accusations of “circular financing.”

The Real NVentures: A Two-Person Team, 79 Portfolio Companies, 20 Unicorns

Although branded under NVIDIA, NVentures is surprisingly lean internally. According to private market data firm Tracxn, as of May 2026, the entire team comprises just two people. It has invested in 79 companies to date, 20 of which have achieved unicorn status—including AI video generation platform Synthesia, clinical AI company Abridge, and quantum computing firm PsiQuantum. Over the past 12 months, the team completed 43 new investments; in the first five months of 2026 alone, it made 20 investments—signaling an accelerating pace.

NVentures is led by Mohamed “Sid” Siddeek, NVIDIA’s Vice President and Head of NVentures. Siddeek’s career itself reflects NVIDIA’s strategic positioning of this unit. He joined Morgan Stanley in the late 1990s and accompanied Jensen Huang during NVIDIA’s IPO roadshow; later served nearly a decade as head of TMT and telecom investments at Mubadala Investment Company, Abu Dhabi’s sovereign wealth fund; then led enterprise software and healthcare investments at SoftBank Vision Fund; and rejoined NVIDIA in 2021 to establish NVentures.

Siddeek describes NVentures’ investment criteria succinctly: “There are only two filters: First, any area NVIDIA can meaningfully reach; second, which sectors are investable.” In an interview with Global Corporate Venturing, he clarified that this means horizontal coverage across virtually every industry AI can transform—healthcare, manufacturing, robotics, autonomous driving, quantum computing—and vertical coverage from foundational tools to applications.

The Three-Track Architecture: Corp Dev for Strategy, NVentures for Early-Stage, Inception for Ecosystem

NVIDIA’s external investment system consists of three clearly delineated components.

The first track is Corporate Development, led by Vishal Bhagwati, responsible for all strategic-level large-scale investments, joint ventures, and acquisitions. Deal sizes here operate on a completely different scale from NVentures. Representative deals between H2 2025 and H1 2026 include: NVIDIA’s lead $30 billion investment in OpenAI in February 2026 (as part of a ~$110 billion funding round), with a commitment to increase its stake up to $100 billion; a $10 billion commitment to Anthropic in November 2025; a $2 billion injection into Synopsys at year-end 2025; a $2 billion follow-on investment in CoreWeave in early 2026, alongside a $6.3 billion cloud capacity procurement agreement; a $2 billion investment in Nebius in March 2026; and a $2 billion equity commitment (up to) to xAI.

According to CNBC, Corporate Development’s AI-related equity investments alone exceeded $40 billion in the first four months of 2026. NVIDIA’s total investment in private companies and infrastructure funds reached $17.5 billion in fiscal year 2025.

The second track is NVentures, led by Sid Siddeek, positioned as a traditional venture capital fund focused on financial returns. Individual check sizes range from several million to tens of millions of dollars, targeting Seed to Series B rounds. Siddeek explicitly told Global Venturing: “NVentures primarily focuses on early-stage investments, while Corporate Development handles larger, more directly strategic investments.” Behaviorally, NVentures predominantly co-invests—leading only about one-eighth of its deals—more often joining top-tier VCs like Accel, a16z, and Sequoia as a co-investor backed by NVIDIA’s brand.

The third track is NVIDIA Inception—a startup accelerator program that does not provide direct funding but instead offers startups NVIDIA hardware credits, technical support, marketing assistance, and VC matchmaking. NVIDIA’s 2025-upgraded “VC Alliance” initiative, partnering with Accel, Elaia, Partech, and Sofinnova, distributes NVIDIA DGX Cloud Lepton compute vouchers to portfolio companies of those firms—an extension of Inception into Europe.

A clear “funnel” relationship exists among the three tracks. Inception identifies early-stage startups and integrates them into NVIDIA’s ecosystem; those with investment potential enter NVentures’ radar and may receive early-stage checks ranging from several million to tens of millions of dollars; when a company grows large enough to impact NVIDIA’s strategic posture—as a key customer, critical supplier, or potential acquisition target—it “graduates” to Corporate Development, entering multi-billion- or even trillion-dollar collaboration frameworks.

NVentures’ Recent Moves: Quantum, Inference Routing, AI Security

NVentures’ activity surged in May 2026. Within the past month alone, four deals were publicly disclosed: On May 22, French quantum computing firm Alice & Bob announced NVentures’ participation in its €100 million Series B extension round. Alice & Bob’s core technology centers on a fault-tolerant quantum computing architecture based on “cat qubits,” deeply integrated with NVIDIA’s quantum-classical hybrid stack—including CUDA-Q, cuQuantum, Dynamiqs, and NVQLink. On May 26, AI model routing platform OpenRouter closed its $113 million Series B round, with NVentures co-investing alongside Google CapitalG and Snowflake. OpenRouter provides developers a unified interface to access APIs from dozens of global model providers. On May 28, AI inference infrastructure startup Tensormesh raised a $20 million seed extension round, with NVentures co-investing alongside CoreWeave and AMD. On May 6, AI cybersecurity firm Xbow closed its $35 million Series C extension round, with NVentures participating.

In terms of investment themes, NVentures has recently tilted decisively toward three directions: quantum computing (Alice & Bob, Quantinuum, PsiQuantum), AI-driven biopharma (Relation Therapeutics, Genesis Therapeutics), and AI agents/inference layer (OpenRouter, Tensormesh, etc.). This aligns precisely with Siddeek’s stated principle of investing “anywhere NVIDIA can meaningfully reach”—and matches NVIDIA’s current R&D priorities in next-generation software stacks such as CUDA-Q, CUDA-X, and Triton.

Geographically, NVentures’ European footprint is expanding rapidly: it executed 14 European investments in 2025—double the seven made in 2024.

A Holistic View of the Three-Tier Portfolio

Mapping all three tiers’ portfolios onto a single landscape reveals NVIDIA’s “capital radiation” across the AI ecosystem, structured across five primary quadrants.

The foundational model layer includes OpenAI, Anthropic, xAI, Mistral, Cohere, Thinking Machines Lab, Reflection AI, and Black Forest Labs. This tier is funded primarily by Corporate Development, with NVentures occasionally co-investing smaller stakes.

The cloud and infrastructure layer includes CoreWeave, Nebius, Lambda, Crusoe, Nscale, and Firmus Technologies. Here again, Corporate Development leads—with individual investments routinely reaching billions of dollars, often accompanied by long-term compute procurement agreements.

The application and developer tools layer includes Cursor, Perplexity, Synthesia, Runway, Lovable, Together AI, and Weka. NVentures participates heavily here, though with relatively modest check sizes.

The robotics and autonomous driving layer includes Figure AI (latest valuation: $39 billion) and Wayve (valuation: $8.6 billion). These involve joint investments by both Corporate Development and NVentures.

The quantum computing and biotech layer includes PsiQuantum, Quantinuum, Alice & Bob, and Relation Therapeutics. These are predominantly early-stage investments led by NVentures—representing NVIDIA’s hedging strategy for post-GPU computational paradigms.

According to VC research firm F4 Fund, between 2025 and early 2026, at least 10 companies in which NVIDIA (Corporate Development + NVentures) participated crossed the $1 billion valuation threshold—including OpenAI, Anthropic, xAI, Mistral, Figure AI, Cursor, Perplexity, Scale AI, and Wayve.

The Controversy: Burry’s Short Thesis and the “Circular Financing” Question

Yet NVIDIA’s expansive external investment map is drawing mounting scrutiny. The most prominent critique comes from Michael Burry—the hedge fund manager famously portrayed in *The Big Short*.

According to Scion Asset Management’s Q3 2025 13F filing, Burry initiated short positions in NVIDIA and Palantir by September 30, 2025—including put options on approximately one million shares of NVIDIA, representing a notional exposure of roughly $187 million at prevailing prices; and 50,000 put option contracts on Palantir (each covering 100 shares), costing about $9.2 million in premiums. On his X account “Cassandra Unchained,” Burry posted a still from *The Big Short*, captioned “Sometimes, we see bubbles,” then shared Bloomberg’s chart on NVIDIA’s “circular financing,” directly targeting NVIDIA’s capital deployment model.

Burry’s specific allegation is technical. In a Substack post, he estimates that between 2026 and 2028, cloud vendors—including Microsoft, Google, Oracle, and Meta—will collectively understate depreciation by approximately $176 billion by extending the accounting depreciation period for NVIDIA GPUs. This accounting adjustment, he argues, artificially inflates their reported profits—creating higher “paper earnings” to absorb larger capital expenditures. Meanwhile, NVIDIA’s equity investments in those same customers directly supply them with capital to purchase NVIDIA hardware.

Similar concerns are accumulating at the institutional level. In March 2026, the European Commission’s competition authority explicitly added “circular spending risk” within NVIDIA’s investment framework to its review scope. Seaport Research estimates that for every $1 NVIDIA invests in equity, it generates approximately $3.50 in downstream chip procurement revenue. Bloomberg’s March 2026 special report on “AI circular transactions” maps dense interconnections among NVIDIA, CoreWeave, OpenAI, Oracle, and Anthropic: NVIDIA holds ~7% of CoreWeave; CoreWeave uses NVIDIA GPUs as collateral for financing, then spends that cash to buy more NVIDIA GPUs; NVIDIA simultaneously signs a $6.3 billion cloud capacity procurement agreement, committing to absorb CoreWeave’s excess capacity through 2032; NVIDIA pledges up to $100 billion to OpenAI, which commits to purchasing NVIDIA hardware and building a $300 billion data center via Oracle—which then buys NVIDIA GPUs; NVIDIA invests $10 billion in Anthropic, which commits to deploying Claude on Microsoft Azure, which in turn procures NVIDIA Grace Blackwell and Vera Rubin systems.

Counterarguments exist. Asset manager Janus Henderson characterizes this model as a “virtuous cycle,” arguing that in an era of extreme compute scarcity, binding supply and demand via “equity + long-term procurement contracts” is sound commercial practice. Morningstar analysis notes that NVIDIA’s commitment to absorb CoreWeave’s excess capacity effectively transfers inventory risk to NVIDIA itself—thereby acting as a brake against short-term hardware sales pressure.

Within this debate, NVentures occupies a delicate position. Its early-stage, small-check, co-investment–dominant, and sector-diversified approach stands in stark contrast to Corporate Development’s “circular transaction” pattern. Companies NVentures backs—like Alice & Bob, Tensormesh, and OpenRouter—are too small to create the “both customer and investee” feedback loop; their investments follow conventional corporate VC logic. Yet from the perspective of NVIDIA’s overall investment architecture, does NVentures serve, to some extent, as a “venture capital compliance veneer”—making NVIDIA’s broader investment activity appear more like standard VC behavior rather than systemic vendor financing? That is the unspoken but implicit question behind Burry’s thesis and the EU regulator’s inquiry.

NVIDIA’s consistent official stance is that all investments are based on independent commercial judgment and are not tied to hardware sales. But market observers increasingly cite a rhetorical question: In an era of compute scarcity, whether to believe that “the entanglement of equity and procurement contracts is coincidental” is, in itself, a matter of trust.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News