Bank of America Research Report Analysis: NVIDIA's Lowest Valuation in Seven Years, Market May Have Misjudged 30% Earnings Discount

TechFlow Selected TechFlow Selected

Bank of America Research Report Analysis: NVIDIA's Lowest Valuation in Seven Years, Market May Have Misjudged 30% Earnings Discount

BofA believes this discount is unreasonable, as NVIDIA remains a high-quality growth stock in the AI computing power sector with pricing power, economies of scale, and supply chain barriers.

By: Rita

TechFlow Guide

On July 7, Bank of America released a research report on Nvidia, reiterating a buy rating with a target price of $350, compared to the current stock price of $195.55, implying approximately 79% upside potential. BofA's core argument is: Nvidia is currently trading at 15.7x expected earnings per share for 2027, the lowest level in seven years. Market concerns regarding HBM cost pressures, custom ASIC competition, and crowded positioning may have been overpriced, implying an earnings discount of approximately 30-35%. BofA believes this discount is unreasonable; Nvidia remains a high-quality growth target with pricing power, scale effects, and supply chain barriers in the AI computing power sector.

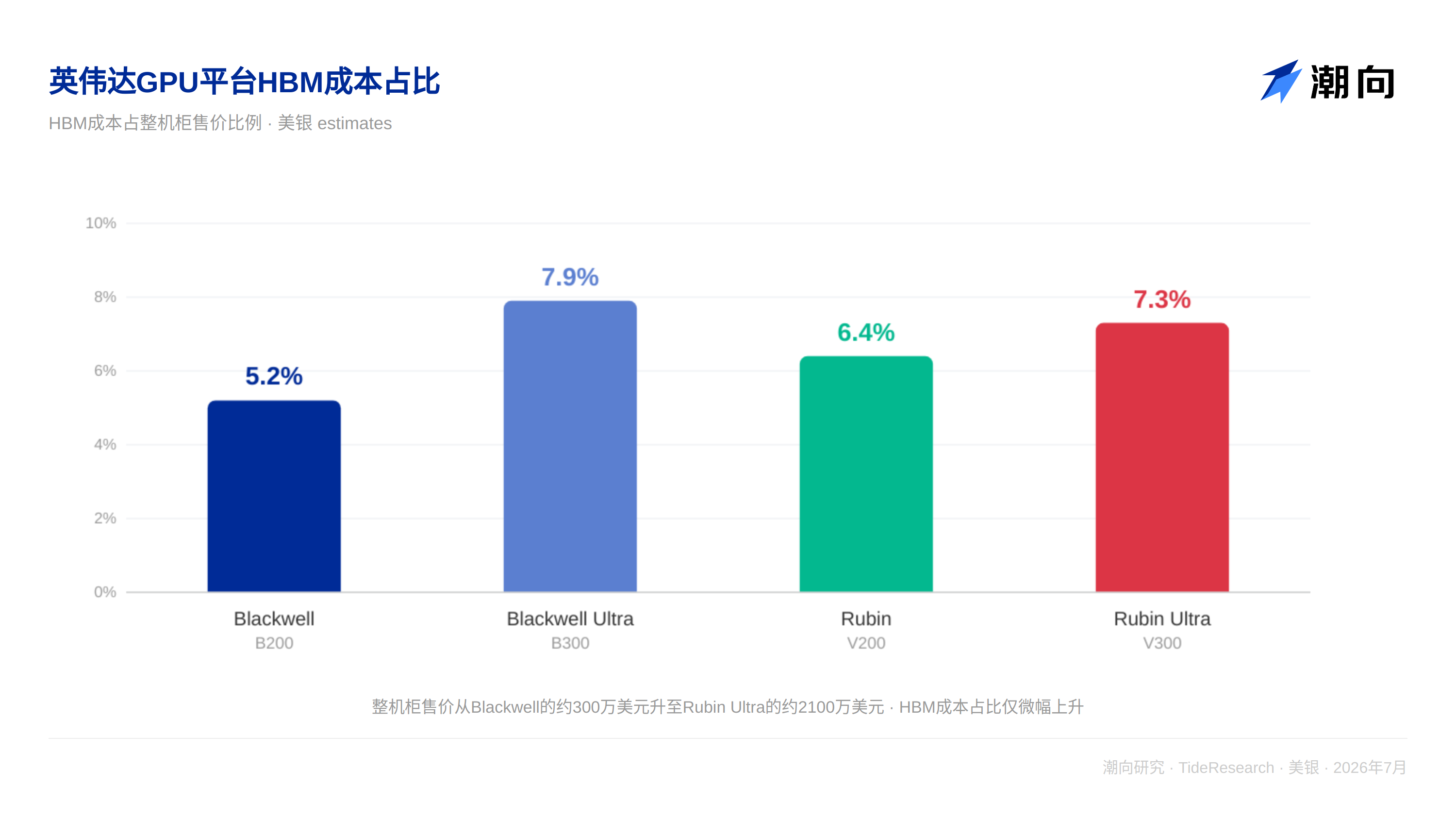

HBM Costs Are Pressure, But Pricing Power Is a Stronger Force

The market worries that rising HBM prices will compress Nvidia's gross margin. BofA did the math: from Blackwell to Rubin, the HBM cost per cabinet increased by approximately $200,000-300,000, but the selling price of the entire cabinet increased by $2 million-3 million. This is because Nvidia upgraded multiple components simultaneously in each generation of products, including computing chips, NVLink networking, software stacks, etc.

Compared to Blackwell, Vera Rubin offers a 10x improvement in inference performance per watt, a 3.3x improvement in inference performance, and a 5x improvement in training performance. These performance upgrades allow Nvidia to pass costs on to customers. BofA expects Nvidia's gross margin to remain around 75%.

ASIC Competition Is Nothing New, Nvidia Won by 700 Times

Google TPU was launched in 2015, Amazon Trainium in 2020, and Meta MTIA in 2023; custom ASICs have existed for nearly a decade. However, Nvidia's GPU accelerator revenue grew 700 times during this period.

The reason is simple: ASICs are narrow-purpose chips, capable of running only specific workloads, and available only to specific cloud vendors. Nvidia's GPUs are a general-purpose platform with a complete software ecosystem and supply chain support. Nvidia's sales to hyperscale customers increased by 115% year-over-year, almost twice the growth rate of cloud capital expenditure, indicating that Nvidia's "wallet share" among cloud vendors is still expanding. BofA expects Nvidia to maintain a share of over 65-70% in AI capital expenditure.

Crowded Positioning and Ecosystem Investment: Risks Are Real, But Absorbed by Valuation

Nvidia's weight in the S&P 500 Index is 1.15 times, and 78% of actively managed funds hold Nvidia. Crowded positioning is real, but this itself is a reflection of the market's view on Nvidia's industry status, not a signal of a bubble.

Nvidia's total investment in ecosystem partners is approximately $65 billion, including OpenAI, Anthropic, Intel, CoreWeave, etc. BofA calculates that these investments account for only about 35% of 2026 free cash flow and about 17% of 2027 free cash flow, and will not affect the company's ability to continue repurchasing shares and paying dividends.

TechFlow Perspective

The core logic of this BofA report is: Nvidia is priced by the market as a "cyclical stock," but its business model has "growth stock" attributes, with product iterations driving unit price increases, scale effects bringing cost advantages, and software ecosystem forming customer stickiness.

But there is a question worth asking: If Nvidia is mispriced by 30%, why has this mispricing persisted for so long? Crowded positioning and ecosystem investments are only surface reasons; the deeper reason is investors' skepticism about "whether AI capital expenditure is sustainable." The capex-to-EBITDA ratio of hyperscale vendors has already exceeded 70%, and the market worries that any capex cuts will directly impact Nvidia's revenue. BofA responded to this concern with "Nvidia's wallet share among cloud vendors is still expanding," but did not directly answer "if total capex shrinks, can expanding wallet share offset it."

For investors, the most valuable part of this report is not the buy rating itself, but that it provides a thinking framework for how to distinguish which risks are real and which have been fully absorbed by valuation when market concerns about a high-quality growth stock are overblown.

Disclaimer

This article is a compilation and interpretation by TechFlow Research of a third-party broker research report (Bank of America, July 7, 2026). The ratings, target prices, earnings forecasts, and related judgments cited in the text are the views of the broker's analysts, represent only the position of their affiliated institution, do not represent the views of TechFlow Research, and do not constitute any investment advice.

The market carries risks, decisions must be independent. This article should not be used as a basis for buying or selling any securities.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News