From Limit Up to Limit Down, Is It All the Fault of Quant Trading?

TechFlow Selected TechFlow Selected

From Limit Up to Limit Down, Is It All the Fault of Quant Trading?

Long March 10B Successfully Recovered, Yet Commercial Aerospace Sector Plummets Due to Quantitative Harvesting—When Will the Disconnect Between Industrial Breakthroughs and the Market End?

Author:Gelonghui

July 13, late summer, the commercial aerospace sector surged and then fell back, plummeting across the board.

CETC Blue Sky fell over 10%, while Aerospace Power, Waven Communication, and Tongyu Communication all declined. The Shenzhen Component Index and ChiNext Index both dropped more than 2%. The previously hot AI sector repaired and rebounded, while funds were sucked out of the aerospace sector in one go.

Just one weekend prior, on July 10, news of the successful maiden flight of the Long March 10B and the world's first rocket net recovery had just ignited the entire sector. More than 30 individual stocks hit the limit up. Two hundred-billion giants, China Satellite and China Satcom, went straight to the limit up.

Friday was a limit-up tide. Monday was a sell-off day.

With styles so extremely fragmented, what exactly happened?

01. Who Is Pricing?

The Long March 10B was not an ordinary launch.

At 12:15 on July 10, this rocket, 63 meters in full length with a takeoff thrust of 890 tons, lifted off from the Hainan Commercial Launch Site. About 6 minutes after first-second stage separation, the first stage returned vertically and was caught by the flexible arresting net of the "Pioneer" recovery platform—China's first controlled recovery of a heavy-lift rocket first stage, and the world's first net recovery. China became the second country to master this technology after the United States.

Such solid news only lasted a weekend.

Interestingly, the market buzzed with discussion, with fingers almost unanimously pointing at quantitative trading.

The root of this emotional cycle of "sharp drop → sharp rise → pullback" lies not in the news. It lies in the structure of money.

According to Securities Times, public funds and social security funds have long underconfigured or even zero-configured commercial aerospace. For Sirui New Materials and Information Development, which rose over 100%, there is still no sign of public mutual funds among the top ten circulating shareholders. Although institutions participated in Aerospace Power and Aerospace Development, the overall position size was limited.

Thus, institutional funds have not yet formed a large-scale, systematic heavy-position pattern, and the capital structure remains generally scattered. Without long-term bottom positions to support it, the sector becomes an unanchored ship. When it rises, everyone swarms in; when it falls, no one catches it.

Data shows that quantitative funds account for 20% to 30% of A-share turnover. In sectors lacking institutional bottom positions, its influence is multiplied—there is no ballast stone to counter its algorithmic instructions.

The underlying logic of quantitative trading is volatility arbitrage; it needs to create volatility to profit. The limit-up tide and the sell-off day are two sides of the same strategy for it. When a hot spot arrives, algorithms push the stock price up before retail investors; after retail investors follow, the algorithms turn around and smash.

This system runs especially smoothly in the commercial aerospace sector. Because there are not enough long-term counterparties here to catch its selling pressure. Commercial aerospace, this sector absent of public funds, is precisely where the reshuffle is most intense.

On July 10, the dragon-tiger list for Aerospace Development showed Shenzhen Stock Connect, institutions, and hot money business departments from Buy 1 to Buy 5. Prominently listed in Sell 5 was East Money Lhasa Tuanjie Road First Business Department. On the limit-up day, institutions' net buy-in was 85.71 million, while Lhasa retail investors' net sell-out was 18.06 million.

Furthermore, this company has been listed 8 times in the past half year, with an average drop of 10.66% in the 5 days after listing. Funds entering on the limit-up day averaged losses of over 10% after five days.

This is not an individual phenomenon of a certain stock; the entire sector lacks long-term capital anchoring and is repeatedly cut by algorithms according to a metronome.

But in sharp contrast to the disorder of the secondary market is the continuous betting of the primary market.

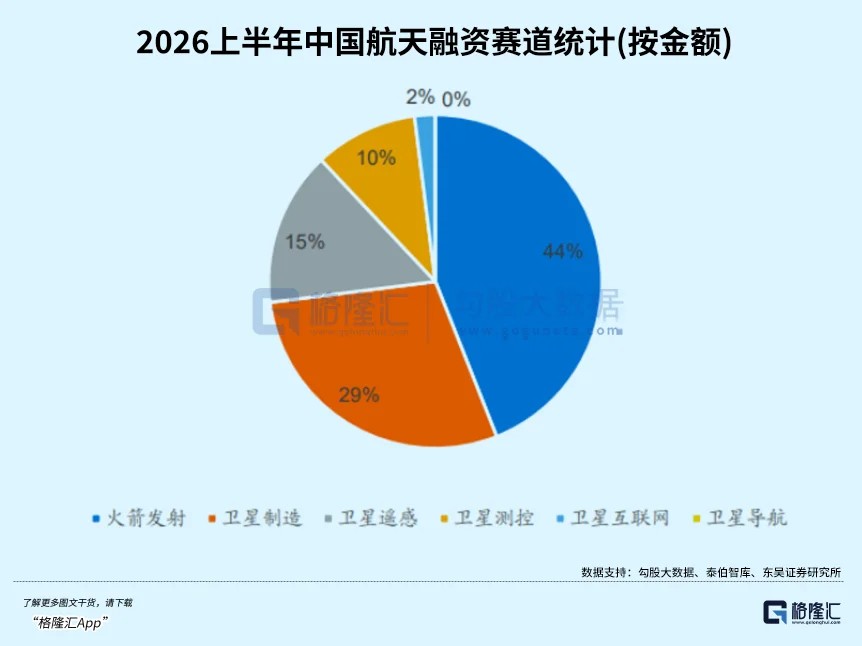

At the industrial capital level, according to Taibo Think Tank statistics, in the first half of 2026, there were 89 publicly disclosed financing events in domestic commercial aerospace, with financing amounts reaching 15.13 billion yuan. Among them, the rocket launch sector accounted for 44% of the financing amount, making it the sub-sector with the largest capital investment. National and local guiding funds are the main force of patient capital, and the industry is shifting from "spontaneous exploration" to "national systematic guidance".

SpaceX is the best example. After listing this year, its market cap surged to 1.77 trillion USD, while it had a net loss of 4.94 billion USD in 2025. A company that lost nearly 5 billion was given a valuation of nearly 2 trillion by the market.

The money in the primary market invests in the long-term space of the entire space economy—a market size of 2.83 trillion (CCID Think Tank), the certain demand to launch tens of thousands of satellites within five years, and the cruel rule of "first come, first served" for orbital resources.

However, this pricing logic and the secondary market are not yet on the same timeline. The primary market allows a company to lose 4.94 billion USD, as long as its rockets can be recovered 34 times, Starlink users exceed 9 million, and tens of thousands of satellite positions are already occupied in orbit. It looks at who has launch capacity in five years and who occupies the orbit in ten years. The income statement can wait; the orbital window does not.

It's just that under the current structure dominated by retail investors and quantitative trading in the secondary market, the real progress of the industry is submerged by short-term algorithmic gaming.

The question is, when will the secondary market catch up with the pricing logic of the primary market.

02. Valuation System Faces Test

If looking only at one day's stock price, commercial aerospace is just a round of quantitative harvesting. But if stretching the time to nearly two years, things are completely different.

In the past two years, this sector has experienced several market rounds.

The first wave, early 2025. China submitted frequency and orbital resource applications for 203,000 satellites to the International Telecommunication Union at once, covering 14 constellations. Before this, China had never declared orbital resources at this magnitude. The market rose in response, speculating on the "China's SpaceX" concept. China Satellite's P/E ratio surged to 2400 times. China Satcom itself issued an announcement warning that the "hot potato effect was very obvious".

But its significance lies not in the rise—it lies in embedding the cognition that "space is a scarce resource" into the market for the first time.

The second wave, late 2025. The National Space Administration established the Commercial Aerospace Department, the first national-level specialized regulatory agency. The STAR Market's fifth listing standard was introduced, clearing financing obstacles for unprofitable rocket enterprises. LandSpace sprinted for the A-share "First Stock of Commercial Aerospace". The driving factor upgraded from concept to policy.

But the recovery tests for Zhuque-3 and Long March 12A failed. Before technology was verified, the market trend was forced to recede.

The third wave, spring 2026. Reusable rockets entered a dense testing window. Zhuque-3 Y2 completed static ignition, Lijian-2 succeeded in its maiden flight, and Long March 10B was originally scheduled for its maiden flight in April. At the same time, Q1 financial reports revealed the profit structure of the industrial chain for the first time—upstream earned hugely, downstream lost hugely, the scissors difference was glaring. The drive upgraded again: from policy to technology verification.

But Tianlong-3 experienced flight anomalies after ignition and lift-off, failing its maiden flight. The explosion on April 3 cooled the market down again.

In the three trading days prior, the commercial aerospace sector fell consecutively by 8%, Shenjian Shares hit the limit down, and multiple individual stocks fell over 10%. Until noon on July 10, when Long March 10B lifted off from Hainan, successfully realizing the full process closed loop of "orbit insertion launch + controlled recovery" for the first time, becoming the second country to master heavy-lift reusable rockets after the United States.

Whether this means a new round of market trends has started, no one can guarantee. But one thing is certain:

After several rounds of market trends, the upgrade path of driving forces is very clear: concept → policy → technology verification.

The pricing power of the capital market seems to be walking on another line. From the first wave dominated by hot money, to the second wave resonance of hot money plus retail investors, to the recent rounds where the influence of quantitative models is becoming heavier.

This dislocation is unsustainable. Because the logic on the industrial side is becoming clearer, clear enough to be expressed with simple arithmetic.

Take the core reusable technology for example.

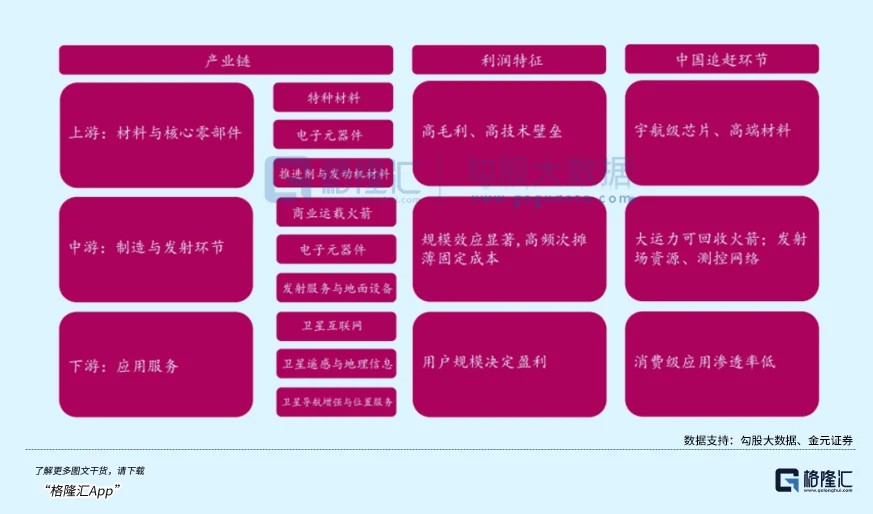

The first stage body accounts for more than 70% of the rocket cost. Recovering it saves 70% of the manufacturing cost. SpaceX's Falcon 9, through 34 reuses, pressed the unit orbit insertion cost down to 19,000 to 28,000 RMB per kilogram. The current domestic launch quote is 50,000 to 100,000 per kilogram. LandSpace's Zhuque-3 target is below 20,000 per kilogram. If reusable technology truly matures, industry estimates suggest it can eventually drop to below 1,000 yuan per kilogram.

Behind this is a simple supply-demand mismatch. The GW Constellation plans 12,992 satellites, the Qianfan Constellation 13,904 plus 1,296 satellites, with a total plan exceeding 50,000 satellites. But there are only 18 commercial launch pads nationwide, with another 7 under construction. The average queue is one month. Many satellites, few rockets; rocket launch capacity is a strategic resource.

Yuanhe Chenkun clearly ranked investment priorities in the "Low Earth Orbit Satellite Internet Industry Research Report": whole rockets greater than satellite operators, greater than whole satellites, greater than satellite components. The logic given is that whoever conquers recovery first and brings costs down holds the main valve of the constellation market. The private rocket sector may ultimately accommodate only two to three top players.

In the second half of the year, this industrial logic will also face a concentrated stress test.

The recovery test of Zhuque-3 Y2 is the most recent exam paper. If successful, it will become the first liquid rocket of a private enterprise to achieve orbital-level recovery. The maiden flight of Pallas-1 is imminent, and Tianlong-3 will also fly again in the second half of the year after failing in April. Long March 10B will attempt its first reusable flight before the end of the year—from "can recover" to "can reuse", this step's difficulty is no less than the maiden flight.

Moves on the capital side are also accelerating synchronously. After listing, SpaceX's market cap surged to 1.77 trillion USD, already setting a reference line for global commercial aerospace. LandSpace's STAR Market IPO has advanced to the inquiry stage, with CAS Space close behind. These domestic rocket companies about to land on the capital market will have their valuation systems face public market testing for the first time.

The interim report window is also at hand. China Satellite just disclosed its first-half earnings forecast on July 12: net profit of 30.5 million to 36.5 million, turning a loss year-on-year. A satellite manufacturing leader with a market cap of 100 billion, with half-year profit just over 30 million.

Meanwhile, upstream Zhenlei Technology's Q1 single-quarter revenue exceeded 400 million, with a profit margin of 31%; BLT's Q1 revenue increased 40.5%, and net profit doubled. Downstream SpacePI's Q1 revenue plummeted 86%, and it is already *ST.

These catalysts are interlinked. Successful rocket verification, IPO landing, reusable flight, batch orders, interim report realization—every step of verification adds weight to the industrial logic and also affects the time window for the transfer of pricing power.

03. Epilogue

Rocket lift-off and capital entry are not the same countdown.

The successful recovery of Long March 10B is a historic breakthrough for China's commercial aerospace. Reusable technology has crossed the most important threshold, and the path for cost reduction has been opened. From an industrial perspective, this is a clear good signal.

Commercial aerospace is a track with a long slope and thick snow. Industrial trends cannot be achieved overnight but evolve gradually; last week's technological breakthrough is just a key step in this long process.

But good signals from the industry do not equal immediate market recognition.

Whether funds have fully confirmed that this track has reached an inflection point remains to be verified. Currently, the sector's volatility remains extremely intense—limit up on Friday, plummet on Monday, the pricing system dominated by quantitative trading has not yet exited. The profit divergence of upstream earning and downstream losing has not converged either.

Investors wanting to allocate to this track must recognize: between the industrial inflection point and the pricing power inflection point, there is still a not short distance.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News