Bitget UEX Daily Report | Mixed Signals from U.S.-Iran Negotiations; Fed Sounds Inflation Alarm; SpaceX IPO Triggers Liquidity Pressure

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Mixed Signals from U.S.-Iran Negotiations; Fed Sounds Inflation Alarm; SpaceX IPO Triggers Liquidity Pressure

Overall, the market is balancing macroeconomic data and geopolitical events; investors are advised to focus on the PCE data for guidance on interest rate expectations.

I. Top News

Federal Reserve Updates

Fed Officials Reinforce Warnings on Upside Inflation Risks

- Fed Governor Lisa Cook stated she stands ready to raise rates if inflation continues to deviate from the target; Vice Chair Philip Jefferson also warned that surging energy prices could further intensify inflationary pressures.

- Both officials emphasized that current risks are skewed toward higher inflation—not labor market weakness. Market impact: Their comments have reinforced market expectations for the Fed to maintain or tighten policy, potentially weighing on risk assets in the near term, while underscoring the critical role of energy prices in shaping monetary policy paths.

Global Commodities

U.S.-Iran Talks Accompanied by Military Action, Pressuring Crude Oil

- The U.S. military announced new strikes against Iranian military facilities and intercepted drones; Trump stressed that the U.S. would ensure the Strait of Hormuz remains open.

- While negotiations show signs of progress, key sticking points remain; Trump downplayed the likelihood of immediate sanctions relief. Market impact: Crude oil prices declined significantly, reflecting improved market expectations for a potential ceasefire and Strait stability—though geopolitical uncertainty may still trigger price volatility.

Macroeconomic Policy

Wall Street Funds Reserving Liquidity for Mega IPOs

- A Goldman Sachs report indicates passive funds are increasing cash holdings to meet index inclusion requirements for trillion-dollar IPOs such as SpaceX and OpenAI.

- Historical precedent shows funds often reduce existing positions ahead of large IPOs. Market impact: This may exacerbate selling pressure on some large-cap stocks; short-term liquidity tightening warrants attention, while also offering long-term capital potential for emerging sectors like aerospace.

II. Market Recap

Commodities & FX Performance

- Spot Gold: -0.13%, at $4,448/oz.

- Spot Silver: -0.19%, at $74.40/oz.

- WTI Crude: +1.86%, at $90/barrel.

- Brent Crude: +1.97%, at $94/barrel.

- U.S. Dollar Index: +0.07%, at 99.29.

Cryptocurrency Performance

- BTC: -1.95%, at $74,687.

- ETH: -2.59%, at $2,027.

- Total Crypto Market Cap: -1.5%, at $2.58 trillion.

- Liquidations: $438 million liquidated in the past 24 hours, with $389 million in long positions.

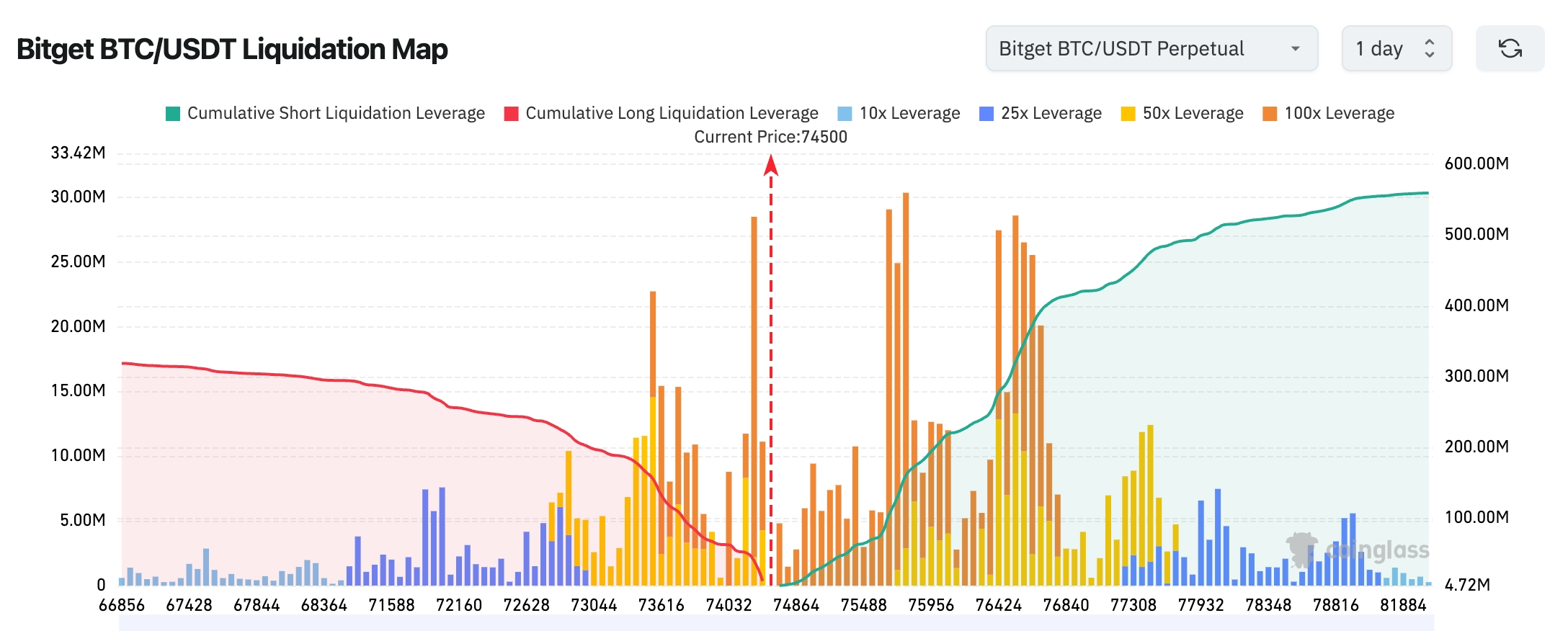

- Bitget BTC/USDT Liquidation Map: Current BTC price ~$74,500; a dense cluster of high-leverage short liquidations lies above $75,500–$76,500, suggesting strong technical rebound potential and short-squeeze demand. However, much of the downside long liquidity has already been swept; should BTC fail to reclaim $75,000 quickly, the market may continue trading sideways before choosing direction.

- Spot ETF Net Inflows/Outflows: BTC spot ETFs saw $206 million net outflow yesterday—the eighth consecutive day of outflows.

Market data shows BTC spot trading volume has dropped 81% since October 2025, amid broadly pessimistic sentiment.

U.S. Equity Index Performance

- Dow Jones Industrial Average: +0.36%, at 50,644.28—new record closing high.

- S&P 500: +0.02%, at 7,520.36—barely holding historic highs.

- Nasdaq Composite: +0.07%, at 26,674.73—narrow gain supported by tech-weighted components.

Tech Giants’ Updates

- NVIDIA (NVDA): -1.05%, at $212.60—AI chip demand remains robust, but short-term profit-taking is evident, compounded by concerns over valuation bubbles.

- Alphabet-A (GOOGL): -0.01%, at $388.83—search and cloud businesses remain stable; AI integration progress provides long-term support.

- Apple (AAPL): +0.82%, at $310.85—signs of recovering consumer electronics demand and hardware upgrade cycle expectations boost confidence.

- Microsoft (MSFT): -0.81%, at $418.57—cloud services and AI initiatives advance steadily, though short-term rotation dragged shares lower.

- Amazon (AMZN): +2.47%, at $271.85—AWS mega-contracts provided notable uplift; cloud infrastructure demand remains strong.

- Meta (META): +3.74%, at record highs—market welcomed its AI subscription service launch, clarifying monetization pathways.

- Tesla (TSLA): +1.56%, at $440.36—ongoing synergy expectations with SpaceX and commercial space sector momentum continue supporting shares.

Core Drivers: Rotation between aerospace and AI themes was pronounced; select stocks gained traction from earnings beats, large contracts, and strategic partnerships—tech heavyweights demonstrated resilience amid macro uncertainty.

Sector Momentum Observations

Aerospace/Space Stocks surged strongly

- Key names: Intuitive Machines (+15%), AST SpaceMobile (+8%), Astrotech (+459%).

- Catalysts: Imminent SpaceX IPO and lunar development news boosted optimism about long-term commercial space prospects.

Semiconductors/Memory showed partial strength

- Key name: Micron Technology (+3.63%).

- Catalyst: Sustained AI demand pushed its market cap above Berkshire Hathaway’s.

III. Deep Dives: U.S. Equity Highlights

1. Snowflake (SNOW) – AWS Mega-Contract & AI Strategy Overview: Snowflake committed to purchasing $6 billion in AWS services over five years, primarily for Graviton chips and AI GPU infrastructure; simultaneously reported Q1 FY2027 results—revenue of $1.39 billion (+33% YoY), adjusted EPS of $0.39—both substantially exceeding estimates—and acquired AI startup Natoma to strengthen its Agentic AI capabilities. Shares surged over 35% after hours. Market Interpretation: Analysts widely view this not only as reinforcing AWS’s leadership in cloud infrastructure, but also as a deepening strategic alignment and competitive enhancement for Snowflake within the AI data platform landscape. With enterprise AI workloads accelerating migration, synergies between cloud and data platforms are expected to drive continued growth in Snowflake’s remaining performance obligations, while broader adoption of AI-native features may accelerate revenue monetization. Investment Implications: Strong demand for AI infrastructure is evident; strategic collaboration between cloud providers and data platforms is becoming an industry norm—yet investors must remain vigilant about expansion risks at elevated valuations and margin pressures from intensifying competition.

2. Marvell Technology (MRVL) – Major Custom Chip Guidance Upgrade Overview: MRVL’s Q1 results beat across revenue and EPS, driven by robust data center business growth; the company significantly raised full-year guidance and forecast custom chip revenue to exceed $10 billion by FY2029 (some analysts see it surpassing $10 billion). Market Interpretation: Analysts believe MRVL is well-positioned amid cloud vendors’ efforts to diversify away from NVIDIA, thanks to its custom AI silicon and interconnect solutions. Expanded collaboration with NVIDIA and multi-generation XPU project rollouts further validate the sizable opportunity in customized AI infrastructure markets, clarifying its long-term growth trajectory. Investment Implications: The trend toward AI hardware diversification is clear; MRVL and similar beneficiaries warrant long-term tracking—but supply chain volatility, geopolitical risks, and evolving competitive dynamics could pressure gross margins.

3. Meta Platforms (META) – Launch of AI Subscription Service Overview: Meta launched its first paid subscription tier for Meta AI chatbot ($7.99–$19.99/month), aiming to partially offset massive AI investment costs; shares rose over 4% intraday following the announcement—a pivotal step in Meta’s AI monetization journey. Market Interpretation: Institutions regard this as a crucial transition from heavy AI investment to sustainable monetization, improving long-term profitability and reducing reliance on ad revenue. Leveraging its vast social platform user base, the subscription model could generate stable cash flow and fund further AI innovation. Investment Implications: Commercialization of AI applications is accelerating; consumer-facing monetization models are reshaping valuation frameworks for tech giants—investors may track replication potential of similar models across other platforms.

4. Amazon (AMZN) – Deepening AWS & Snowflake Partnership Overview: Amazon announced Snowflake’s $6 billion, five-year AWS procurement commitment (including Graviton and AI chips); coupled with solid Q1 cloud growth, the AWS mega-deal further validates demand strength. Market Interpretation: Wall Street sees this partnership reinforcing AWS’s leadership in enterprise AI cloud markets, especially through its custom silicon strategy, which helps insulate against competitive threats. Analysts have raised long-term growth forecasts for Amazon’s cloud business, viewing it as a key return on AI-related capital expenditures. Investment Implications: Cloud infrastructure remains a core growth engine for tech giants; investors should monitor how AWS ecosystem expansion supports Amazon’s overall valuation—while assessing the impact of heavy capital spending on short-term free cash flow.

5. Intuitive Machines (LUNR) – Sustained Commercial Space Momentum Overview: As a key proxy for the SpaceX IPO narrative, Intuitive Machines surged 15% on news of lunar development and broad commercial space sector catalysts. Market Interpretation: Analysts expect Intuitive Machines’ leadership in lunar landers and related services to amplify as NASA-private sector collaboration deepens and the SpaceX IPO draws nearer—underscoring the vast long-term market opportunity in commercial space. Investment Implications: Aerospace-themed equities offer high beta amid the convergence of AI and space economy trends—suitable for higher-risk-tolerance investors, though policy shifts and execution risks warrant caution.

IV. Cryptocurrency Project Updates

1. Monthly payment volume via crypto-linked debit and credit cards rose ~230% year-on-year, reaching $7.8 billion this month—reflecting rapid adoption of crypto payment products.

2. Elon Musk is reportedly exploring a potential merger between Tesla and SpaceX. A Tesla employee indicated internal expectations have long held that such a transaction would eventually occur. Overlapping interests in power infrastructure and AI computing are deepening collaboration. The proposed merger would also create one of the world’s largest corporate Bitcoin treasuries: public disclosures and blockchain treasury tracking show Tesla holds 11,509 BTC, while SpaceX holds 18,712 BTC.

3. With U.S. midterm elections approaching, the cryptocurrency industry’s substantial political funding is shifting toward Republican candidates. The super PAC Fairshake and its affiliates remain the dominant force behind crypto election influence—having invested tens of millions of dollars across multiple congressional races and secured victories.

4. Vitalik Buterin shared updates on his self-hosted large language model (LLM) setup, highlighting expanding intersections between Ethereum infrastructure and AI. He detailed how formal verification enhances code security, noting AI-assisted formal verification can deliver “end-to-end” security proofs for core components including STARKs, consensus algorithms, and the EVM.

5. Google security engineer Michele Spagnuolo was arrested for allegedly using internal Google search data to place bets on Polymarket.

6. The U.S. government transferred approximately $1.9 million in seized crypto assets—and $2.656 million in DAI—from the FTX/Alameda forfeiture to Coinbase. Assets include UNI, RNDR, SAND, MASK, AXS, and APE.

7. Alpha Compute—a Nasdaq-listed firm focused on confidential computing infrastructure for AI applications—completed its acquisition of mobile blockchain gaming platform GAMEE for ~$18 million.

V. Today’s Market Calendar

Data Release Schedule

Key Event Previews

- META Annual Shareholders Meeting: May 28, 1:00 AM (UTC+8) — Watch for latest AI strategy updates.

- FOMC Official Speeches: NY Fed President John Williams and others to speak — Key insights into monetary policy path.

May 28 (Thursday)

- Major U.S. Earnings: Dell (DELL), Costco (COST) — post-market release ★★★★★;

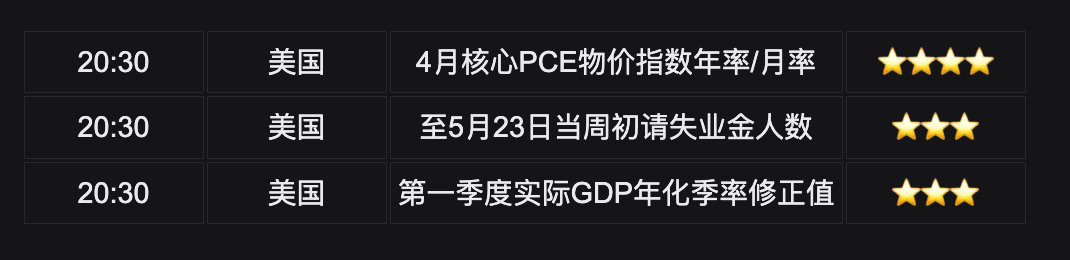

- Q1 2026 GDP revision, initial jobless claims, and durable goods orders released simultaneously;

- April Core PCE inflation data (Fed’s preferred gauge) ★★★★★.

May 29 (Friday)

- U.S. Chicago PMI for May

- Speech by Kansas City Fed President Esther George, 2028 FOMC voting member

- Speech by Fed Governor Michelle Bowman

*This Week’s Key U.S. Equity Focus:

Heightened volatility expected around the U.S.-Iran ceasefire window, core PCE data, and the tail end of Q1 earnings season—including Marvell and Salesforce.

Institutional Views:

Multiple investment banks note that although U.S.-Iran talks eased oil prices—supporting disinflation—hawkish Fed commentary reminds markets that energy price volatility remains a primary risk. While the S&P 500 holds near all-time highs, analysts project a year-end 2026 target of ~7,620—indicating modest optimism; prolonged geopolitical conflict could force the Fed to delay easing. Tech and aerospace stocks retain resilience amid IPO and AI tailwinds, yet liquidity management and valuation corrections remain concerns. Overall, markets balance macro data and geopolitical developments—investors should closely monitor PCE data for rate guidance.

Disclaimer: The above content was compiled via AI search and verified manually prior to publication. It does not constitute investment advice. Data herein may contain inherent discrepancies; please rely on real-time market data for decision-making.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News