Grayscale Research Report: HYPE’s P/E Ratio of 14x—How Much Upside Remains Relative to Robinhood?

TechFlow Selected TechFlow Selected

Grayscale Research Report: HYPE’s P/E Ratio of 14x—How Much Upside Remains Relative to Robinhood?

Based on valuation multiples of comparable traditional exchange companies, HYPE’s current P/E ratio of approximately 14x still has room for expansion.

Authors: Michael Zhao, Zach Pandl

Translation: TechFlow

TechFlow Intro: Grayscale Research has released an in-depth report on Hyperliquid. This DeFi project—having raised zero venture capital—generated approximately $800 million in revenue in 2025 and ranks third or fourth globally by open interest in perpetual futures. Grayscale believes that, as the U.S. regulatory framework gradually clarifies, Hyperliquid is poised to evolve from a blockchain-based derivatives exchange into a full-service financial platform. For HYPE holders, the most critical signal in this report is that, relative to valuation multiples of comparable traditional exchanges, HYPE’s current ~14x P/E ratio still offers room for expansion.

Imagine a startup entering an intensely competitive industry—and doing so in under three years. Last year, it generated roughly $800 million in revenue, targeting a massive total addressable market. Its team is lean, and its operating leverage is exceptionally high. And it achieved all this while remaining inaccessible to users in major markets like the United States.

This is Hyperliquid.

Caption: Exhibit 1 — Hyperliquid is a breakout player in today’s digital asset industry

At its core, Hyperliquid is a decentralized exchange (DEX) dedicated exclusively to perpetual futures—a type of derivative with no expiration date. Crypto perpetuals are already a large business: industry-wide daily trading volume reached ~$200 billion in 2025. This market has long been dominated by centralized exchanges (CEXs) such as Binance, OKX, and Bybit. Hyperliquid is the first decentralized project to meaningfully capture market share in both trading volume and open interest.

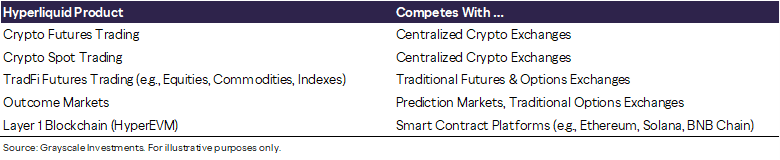

Simply expanding further within the perpetuals market alone would be sufficient to drive substantial platform growth. Yet Hyperliquid’s ambitions extend far beyond that. Although perpetuals remain its primary revenue source, Hyperliquid today functions as a multi-vertical financial services platform.

Caption: Exhibit 2 — Hyperliquid’s diversified financial services landscape

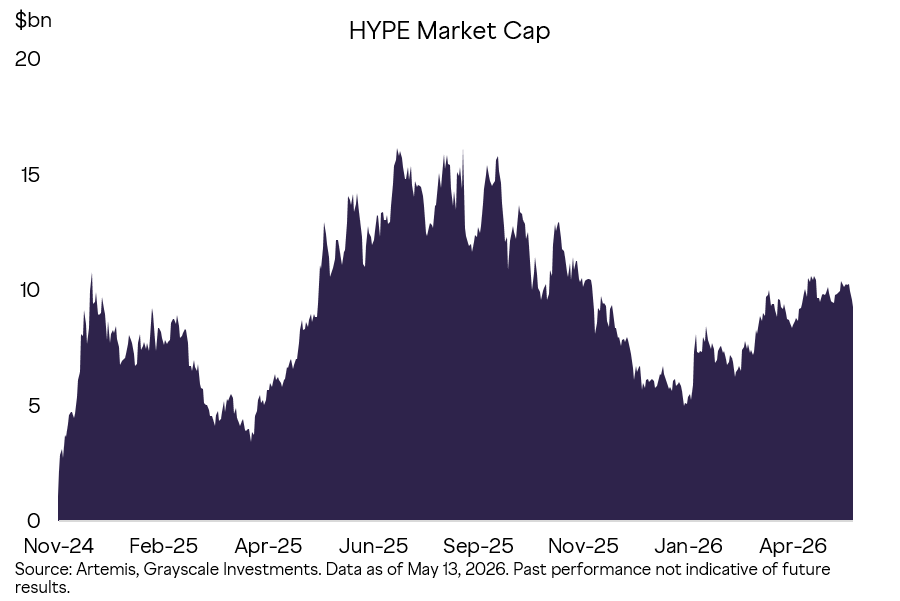

Like other blockchain protocols, Hyperliquid is not a company and does not issue equity. Its token powers the entire network and captures value from trading activity. With a circulating market cap of ~$13 billion, HYPE ranks #8 among all crypto assets by market capitalization. Relative to comparable public companies, HYPE’s valuation multiples are not elevated. Given the platform’s user growth, vast addressable market, and anticipated regulatory tailwinds, we believe Hyperliquid retains significant upside potential.

Caption: Exhibit 3 — HYPE’s market cap trajectory since launch

Perpetual Futures Fundamentals

Although Hyperliquid has broader aspirations, it rose to prominence through decentralized perpetual futures trading—a product born in crypto, which Grayscale believes will ultimately permeate traditional finance deeply.

Traditional futures contracts have expiration dates. For example, an oil futures contract obligates delivery of a specified quantity of oil on a given date. Participants holding positions until expiry must either deliver or receive the underlying asset. To maintain pure financial exposure without physical settlement, users must “roll” their positions—i.e., close expiring contracts and open new ones with later maturities—before expiry.

Perpetual futures have no expiration date and never settle physically. They are designed specifically to provide hedgers and speculators with pure financial exposure to the underlying asset—typically trading 24/7.

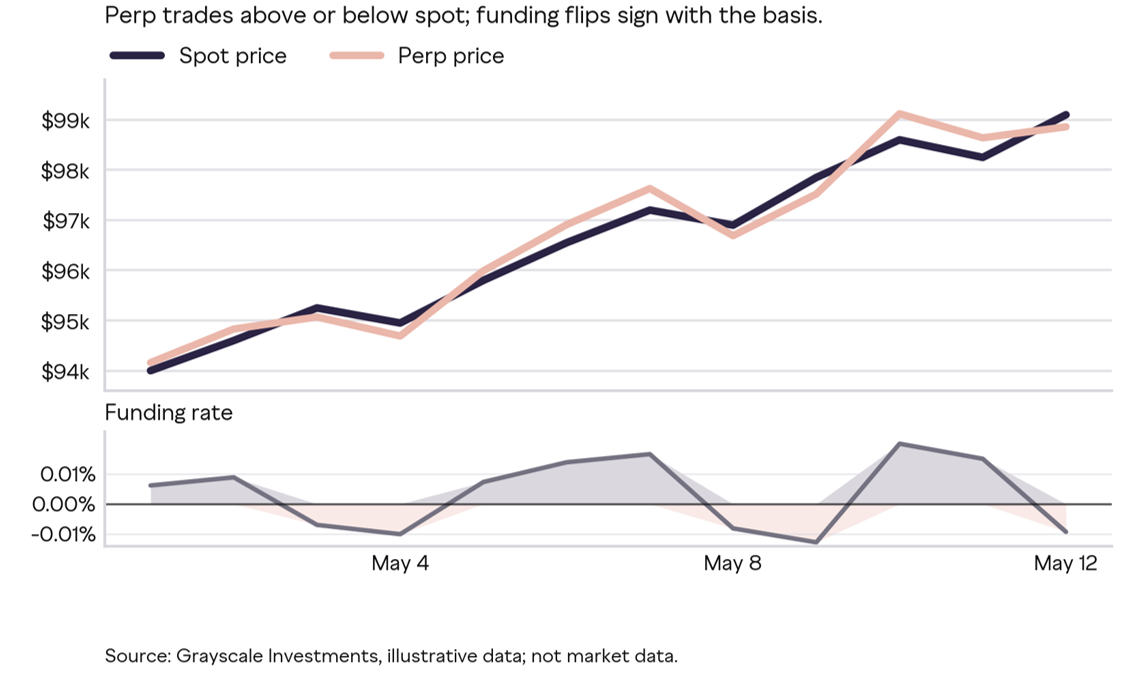

Traditional futures anchor to spot prices because physical delivery is enforced at expiry. Since perpetuals never expire, what keeps them tethered to spot? The answer lies in the funding rate mechanism: periodic small payments between longs and shorts. When the perpetual price trades above spot, longs pay shorts; when below spot, shorts pay longs. The larger the deviation, the higher the payment.

Caption: Exhibit 4 — The funding rate mechanism anchors perpetual prices to the underlying asset

Perpetuals are a natural fit for crypto markets. Crypto assets trade 24/7; retail and professional speculators demand robust access; and new assets emerge far faster than traditional futures exchanges can list them. Perpetuals offer traders a simple way to express directional views, hedge spot exposure, and use leverage around the clock. Today, they are one of crypto’s core price discovery venues.

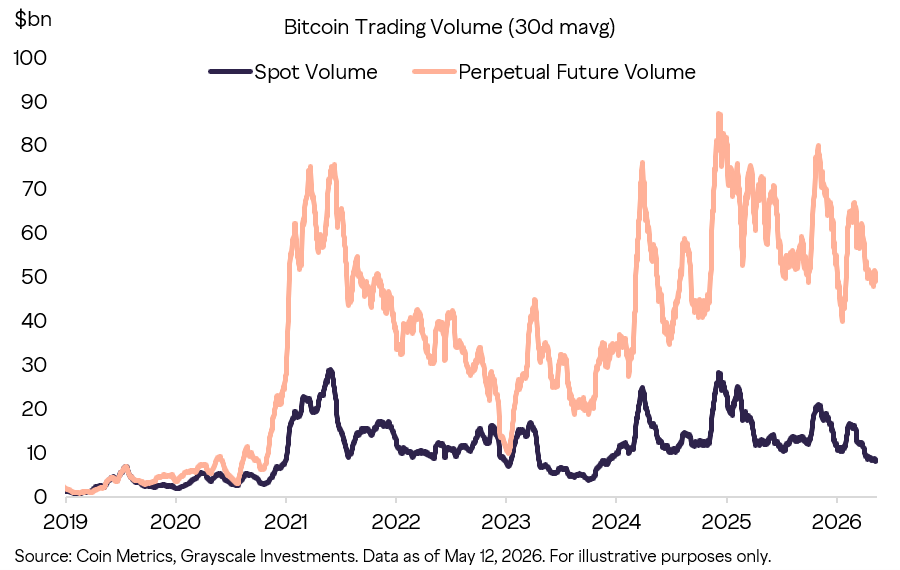

Caption: Exhibit 5 — Global Bitcoin perpetual vs. spot trading volume

Retail investors have many avenues to access leverage: margin accounts with traditional brokers, expiring futures, options, leveraged ETFs. Crypto market experience shows that, when presented with all these choices, retail overwhelmingly prefers perpetuals—largely due to their simplicity. A similar migration is expected once broader traditional-market participants gain access to perpetuals.

Hyperliquid’s Breakthrough

Hyperliquid achieved a foundational breakthrough: CEX-grade performance + blockchain transparency and self-custody.

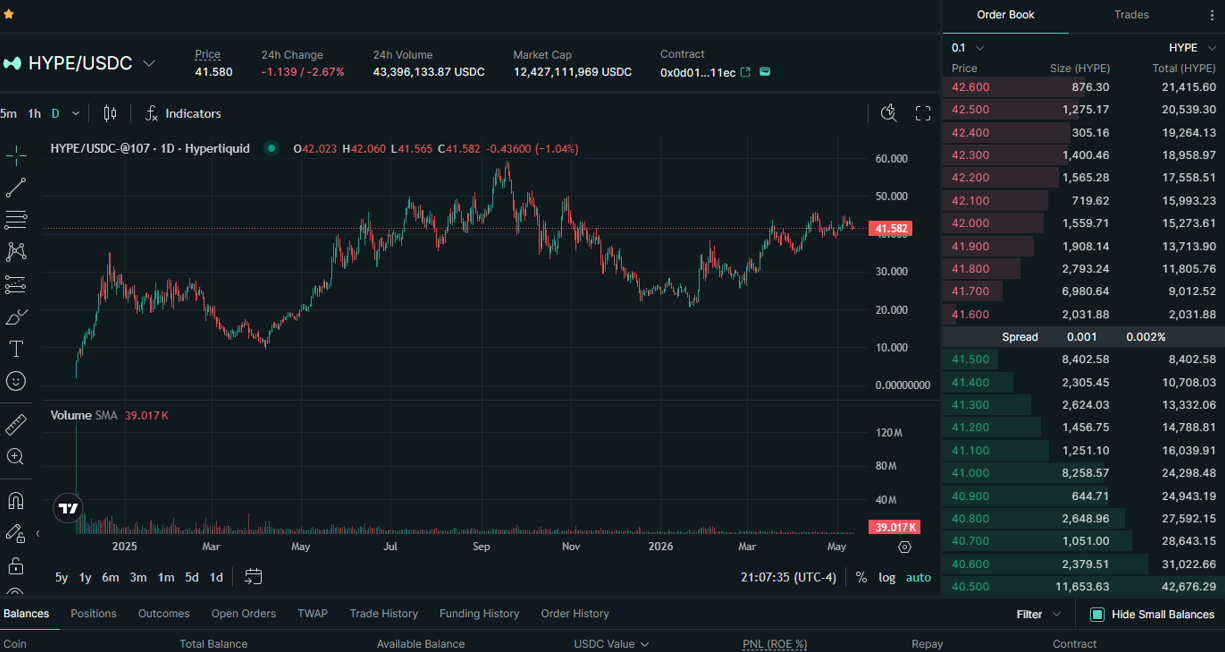

From a trader’s perspective, Hyperliquid feels nearly identical to a CEX: deep order books, rapid execution, and familiar position management interfaces. Yet every Hyperliquid trade—including liquidations—is recorded on-chain, and users retain full self-custody.

Caption: Exhibit 6 — Hyperliquid’s trading experience closely mirrors that of centralized exchanges. Source: app.hyperliquid.xyz screenshot, May 12, 2026

Leveraged trading is arguably the most fiercely contested niche in crypto—where users are exceptionally demanding. Hyperliquid’s success stems entirely from product excellence.

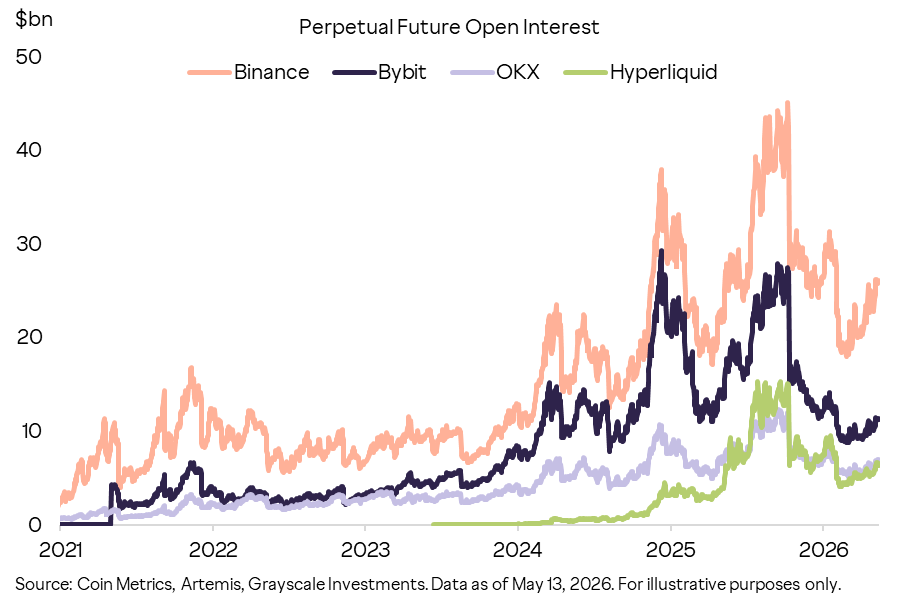

The numbers speak volumes: $2.9 trillion in perpetual futures trading volume in 2025, ~$7 billion in current open interest—ranking Hyperliquid third or fourth globally among perpetual futures exchanges by open interest. Trading volume, open interest, fee revenue, and market attention have all grown in tandem, and the platform has begun expanding beyond purely crypto-native assets.

Caption: Exhibit 7 — Hyperliquid ranks among the top three or four crypto perpetual futures exchanges

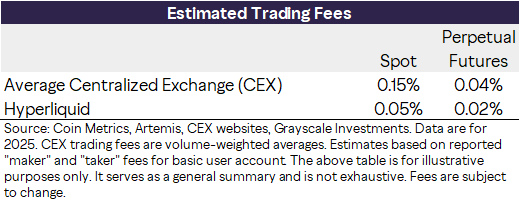

In terms of fees, Hyperliquid holds a cost advantage over CEXs. Based on 2025 BTC and ETH trading data, the weighted average CEX fee is ~15 basis points (bps) for spot and ~4 bps for futures; Hyperliquid charges just 5 bps and 2 bps, respectively.

Caption: Exhibit 8 — Weighted trading fee comparison. Note: Estimates based on publicly available maker/taker fees for standard user accounts; excludes tiered fee structures, discounts, and order book depth effects

More significantly, Hyperliquid has expanded its product suite beyond crypto perpetuals via an open architecture model.

New features are typically introduced through Hyperliquid Improvement Proposals (HIPs), with products deployed by third-party developers—not by the Hyperliquid team itself.

HIP-3 enables developers to deploy new perpetual markets—including non-crypto assets such as equities, commodities, and indices. These markets have gained strong traction among users and have begun serving as after-hours price discovery venues for traditional assets. Bloomberg directly references this framework to describe Hyperliquid’s commodity perpetuals, noting that its crude oil, gold, and silver perpetuals “may foreshadow how these markets respond once mainstream trading resumes.” In another article, Bloomberg characterizes Hyperliquid as “a 24/7 leveraged commodity trading venue.”

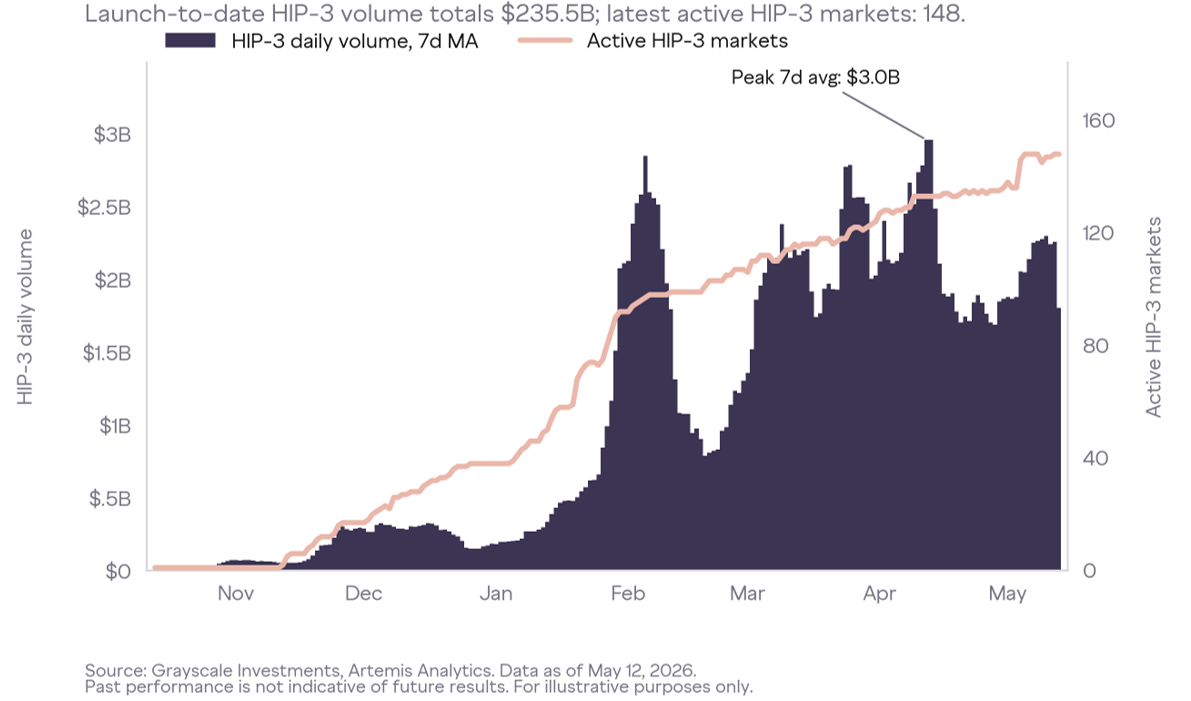

Trading volume data confirms this positioning. During silver’s February surge, the HIP-3 silver perpetual reportedly exceeded $4 billion in daily volume. On February 5, at one point, HIP-3 silver perpetual nominal volume reached ~1% of COMEX silver volume. During Middle East oil volatility, the HIP-3 crude oil perpetual posted over $4 billion in 24-hour volume on April 9—briefly surpassing Bitcoin perpetual volume. An officially licensed S&P 500 perpetual is now also live on Hyperliquid via HIP-3—including weekend trading. Since launch, HIP-3 cumulative volume exceeds $230 billion, with over 140 actively traded pairs.

Caption: Exhibit 9 — HIP-3 expands Hyperliquid beyond crypto perpetuals into broader asset classes

HIP-4 extends further into outcome markets—binary options akin to prediction market contracts. These are likewise deployed by third-party developers, yet all trading activity still generates fee revenue for Hyperliquid.

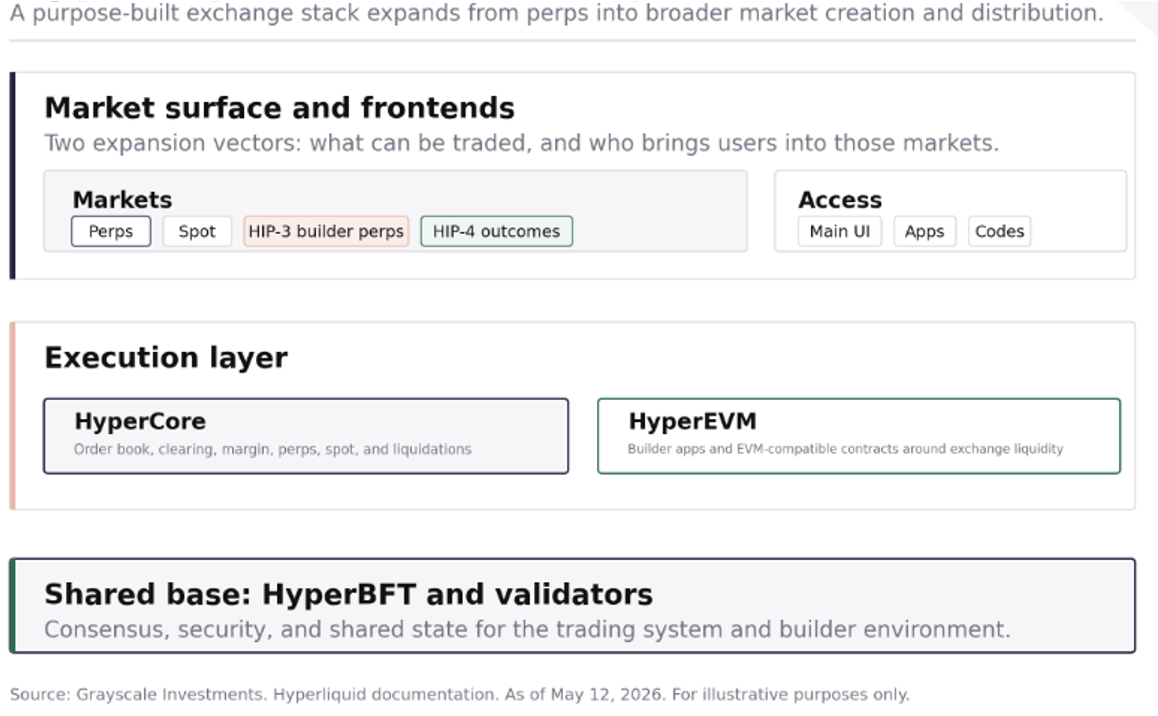

Hyperliquid’s Technical Architecture

The underlying architecture centers on two core components:

HyperCore is the trading system, housing the order book, clearing engine, perpetuals, spot, margin, and liquidation logic. This is the primary interface traders interact with directly.

HyperEVM is the developer-facing environment, providing an EVM-compatible development interface tightly integrated with the Hyperliquid system. The strategic intent is to enable applications to build atop Hyperliquid’s existing liquidity, user base, and asset infrastructure—not on a cold, financially inert chain.

HyperBFT is the delegated Proof-of-Stake (dPoS) consensus layer securing network safety.

The key design choice: Hyperliquid is not an application built atop a general-purpose public chain—it is a purpose-built chain and execution stack optimized for exchange performance, engineered to make on-chain trading competitive with centralized infrastructure.

Caption: Exhibit 10 — Hyperliquid’s architecture as a market platform

Five Pillars of Success

Hyperliquid launched publicly in August 2023—before the U.S. Bitcoin ETP listing—and amid a broader DeFi downturn. Its success is not a speculative bubble but the result of solving a concrete problem better than most crypto infrastructure projects: making on-chain trading genuinely viable for high-frequency traders.

Five critical factors:

Product Focus. Hyperliquid was built around the perpetuals trading use case—not as one feature among many. This allowed the product to prioritize what active traders care about most: fast order entry, reliable execution, clear position display, and a familiar exchange UI.

Market Selection. Hyperliquid captured attention by launching markets traders “most wanted to trade right now”—especially long-tail, high-demand assets beyond BTC and ETH.

Platform Flexibility. HIP-3 empowers developers to deploy new perpetual markets directly, transforming the listing process from a centralized gatekeeper model into an open market creation system.

Distribution Network. Hyperliquid’s builder code and frontend model give third parties a compelling reason to route users to a single liquidity pool rather than fragmenting them across isolated venues. Economic incentives are already substantial: Phantom earned ~$19.7 million in routing fee revenue by integrating Hyperliquid perpetuals via builder code.

Community. Hyperliquid’s token distribution rewards platform users—not VCs or pre-selected insiders. This created a distinct early holder composition: traders, market participants, and developers who inherently had reasons to follow the project. In a sector defined by scarce trust, this matters.

No single advantage is decisive—but together, they explain why Hyperliquid stands among the few crypto applications whose success can be measured by real usage—not just vision.

Hyperliquid can reinforce its competitive moat through the interplay of liquidity, distribution, and developer incentives. Higher volume improves liquidity and execution quality, attracting more users and third-party frontends. Builder code and HIP-3 provide external developers with economic incentives to route activity back to the same liquidity pool. This forms a potential network effect difficult for newcomers to replicate: liquidity attracts distribution, distribution drives more volume, and volume strengthens the protocol’s economic foundation.

HYPE Token

The HYPE token powers the entire Hyperliquid ecosystem.

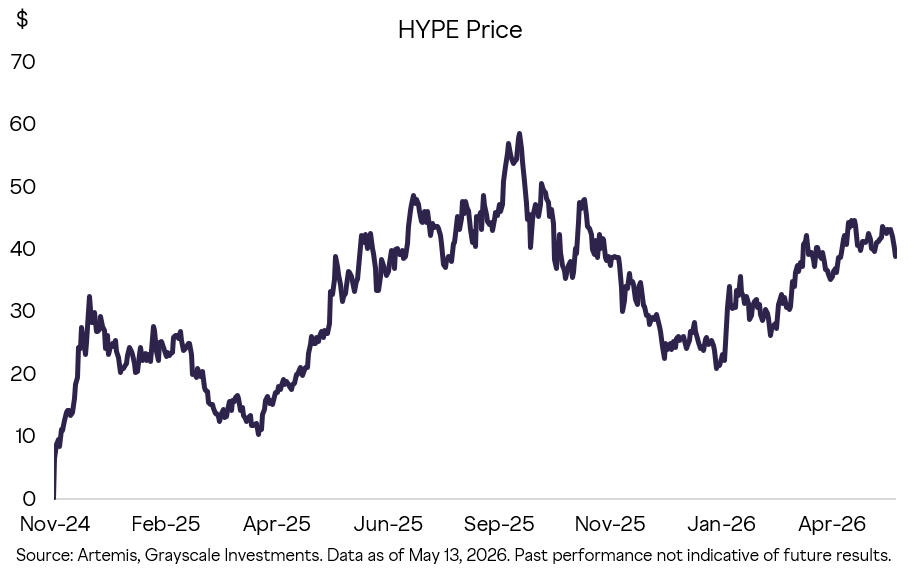

The project raised no traditional venture capital and airdropped ~30% of its token supply to early users. This shaped who cares about HYPE: the initial holder base is heavily skewed toward users who already understand the product—traders, market participants, and community members.

Caption: Exhibit 11 — HYPE’s price trajectory since launch

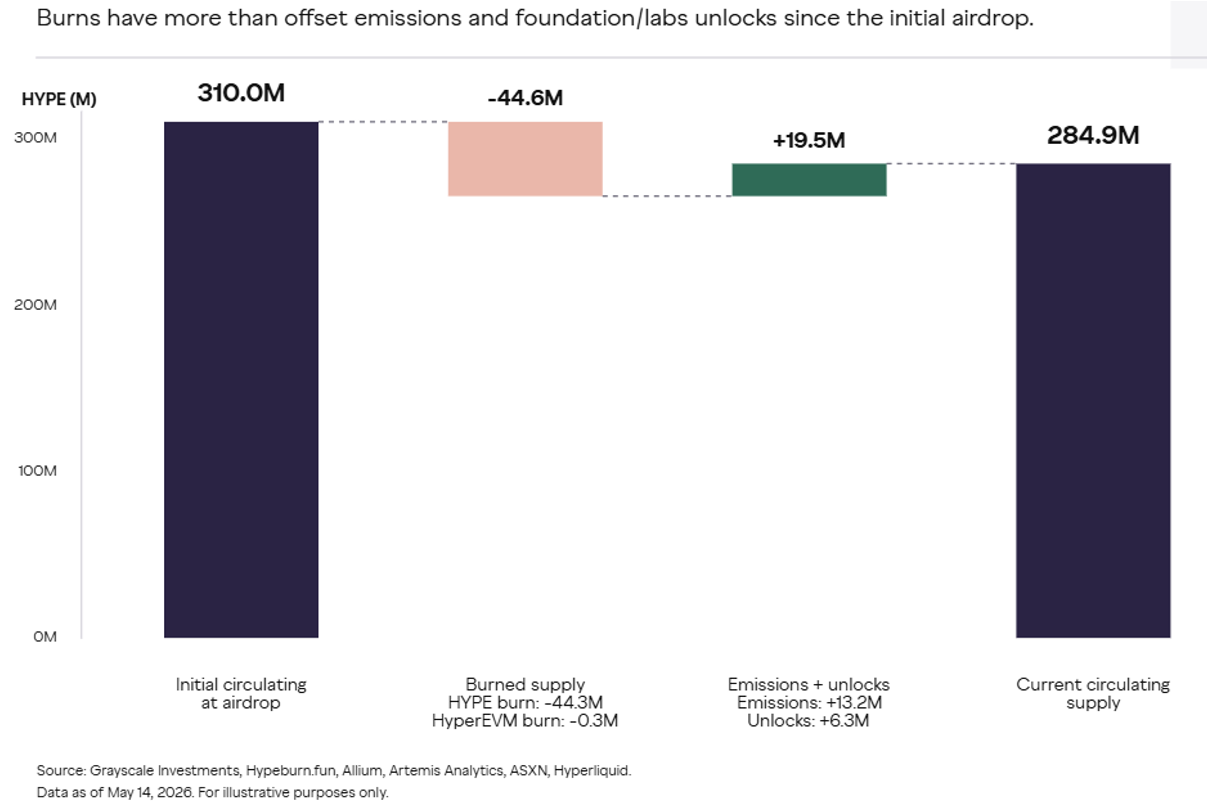

HYPE’s value accrues from trading fees and functional utility. Hyperliquid Labs confirmed that 99% of trading fees flow into an assistance fund, which converts those fees into HYPE and burns the tokens held. Token burning is analogous to share buybacks in traditional equity markets. Because burn volume exceeds new issuance, HYPE’s circulating supply has been steadily declining.

Caption: Exhibit 12 — HYPE burn, emission, and supply dynamics

HYPE’s ecosystem utilities include:

Staking and Validator Participation: HYPE secures network security via validator staking.

Gas Fees: It serves as the native gas token for HyperEVM; both base and priority fees on HyperEVM are burned.

Fee Discounts: Staking HYPE reduces trading fees.

Market Creation Collateral: HIP-3 deployers must maintain 500,000 staked HYPE to operate a builder-deployed perpetual market. This stake serves both as an alignment mechanism and a quality assurance safeguard. HIP-4 outcome markets are live; if permissionless deployment adopts a similar model, HYPE’s role may deepen further.

HYPE is anchored to a venue with measurable trading activity, fee revenue, and developer demand. The more volume the venue processes, the more critical its fee schedule, staking tiers, builder economics, and assistance fund mechanisms become. As HyperEVM, HIP-3, and HIP-4 expand the platform’s boundaries, HYPE’s utility—and potential value accrual—grows accordingly.

Valuation Upside

Hyperliquid is a unique platform offering a suite of financial services—making assessment of its upside challenging. Yet, using reasonable comparables, Grayscale believes both the platform and its token possess meaningful growth potential.

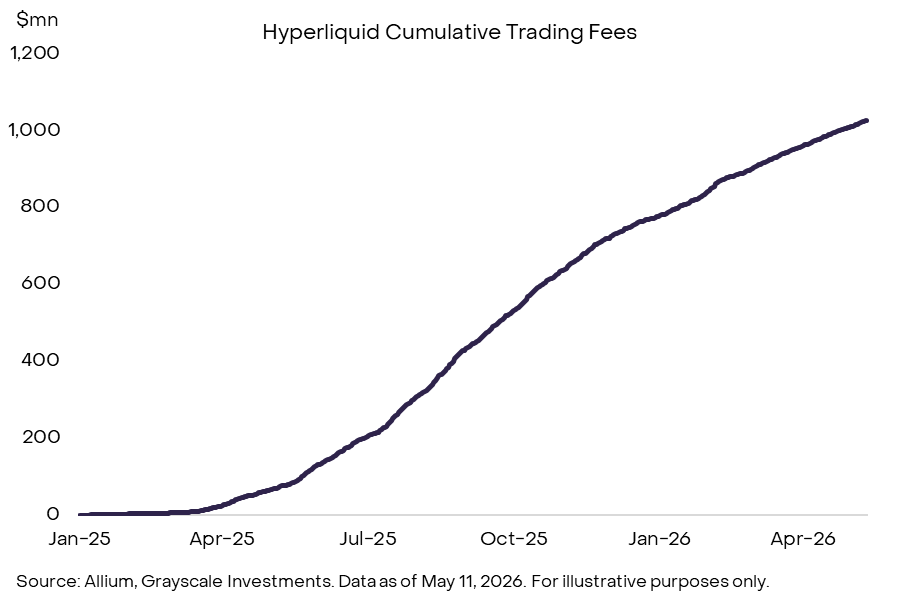

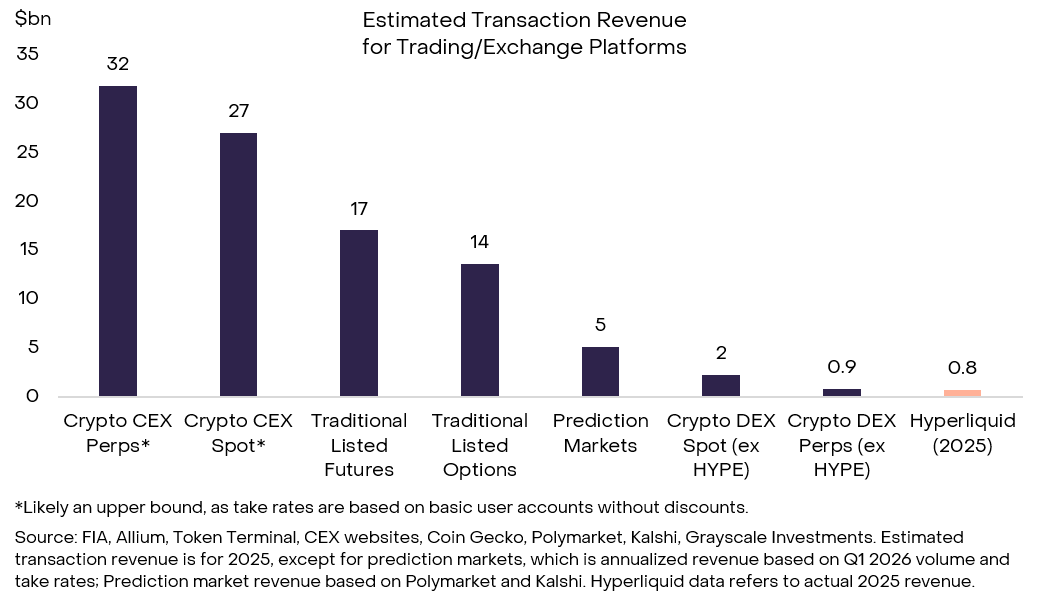

The chart below compares Hyperliquid’s revenue against a range of trading platforms—including centralized crypto exchanges, traditional spot and derivatives exchanges, and prediction markets. Hyperliquid’s ~$800 million in 2025 revenue is substantial, yet represents only ~2% of total crypto perpetuals trading revenue. If Hyperliquid’s non-crypto products sustain adoption, it could tap into the broader derivatives exchange industry’s annual revenue pool of ~$35–40 billion.

Caption: Exhibit 13 — Hyperliquid revenue vs. exchange industry benchmarks

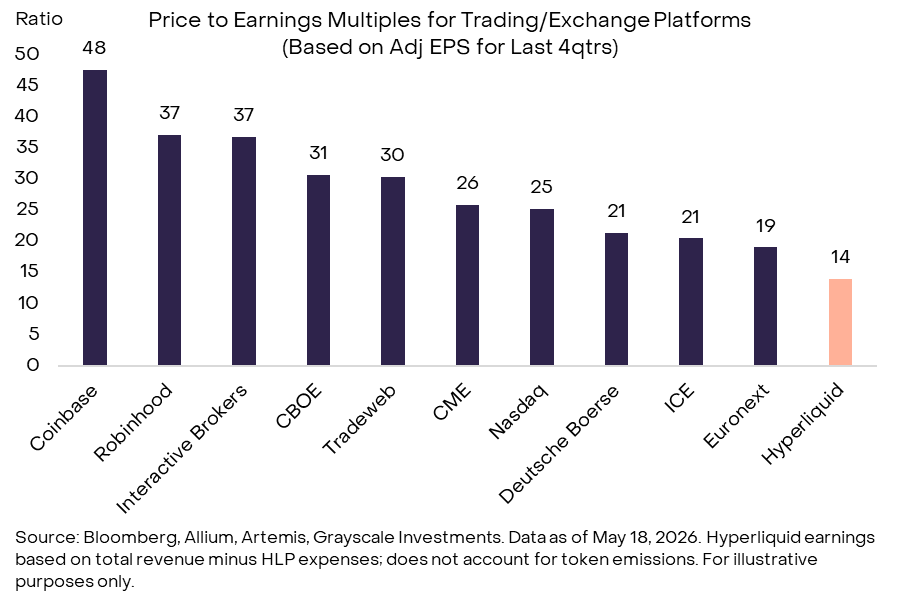

HYPE is not equity—but it can be loosely benchmarked against related public equities. Based on trailing four quarters’ earnings through Q1 2026, HYPE’s current valuation multiple is ~14x. Exchange-related public companies exhibit wide valuation dispersion, but high-growth firms like Interactive Brokers and Robinhood trade at 35–50x multiples.

Caption: Exhibit 14 — Hyperliquid’s valuation multiple sits below equity comparables

U.S. Regulation: Perpetuals Are Coming

Hyperliquid sits at the intersection of two U.S. regulatory gray areas: perpetual futures and decentralized exchanges. Both are now moving rapidly toward clearer frameworks.

Perpetuals have effectively been unavailable in the U.S. They are not explicitly banned—but they do not cleanly fit within the Commodity Exchange Act (CEA), the federal statute governing commodities and derivatives. The CEA imposes explicit requirements on clearing, margin, and registration of trading venues. This ambiguity has triggered enforcement actions against both centralized and DeFi platforms—and explains why Hyperliquid operates offshore and geo-blocks U.S. users.

Yet the landscape is shifting quickly. Recent CFTC statements—alongside initiatives by Coinbase, Kraken, Robinhood, and Kalshi—indicate regulators are actively working to enable perpetual-like products within compliant frameworks. The legal crux lies in classification: Under the CEA, are perpetuals treated as futures or swaps? How regulators clarify this—via rulemaking, guidance, or no-action relief—will determine timing and durability of market access.

In the near term, regulatory progress may benefit registered centralized venues first. But medium-term CFTC rulemaking, guidance, or no-action relief could pave a path for Hyperliquid to offer compliant perpetuals in the U.S., reducing reliance on purely offshore access.

Simultaneously, Hyperliquid’s exchange-like functionality places it squarely in the debate over how DeFi protocols should be regulated. The U.S. currently lacks a dedicated DEX rulebook. Regulators apply existing SEC and CFTC frameworks functionally—with the core principle being “decentralized ≠ exempt.”

For a derivatives-focused DEX, this implies heightened scrutiny and explicit barriers to direct institutional participation—currently occurring mainly through intermediaries or offshore channels. Pending legislation such as the CLARITY Act points toward a more structured, role-based digital asset market framework—clearly distinguishing protocol-layer activities, frontend operators, intermediaries, and registered trading venues.

This distinction is critical for Hyperliquid: As non-custodial infrastructure, its core protocol may ultimately receive regulatory treatment distinct from the interfaces or entities facilitating user access. These proposals do not yet create a fully viable regime for on-chain perpetuals—but they represent a pathway toward that goal—particularly if paired with targeted safe harbor provisions, clearer broker definitions, and rules tailored to on-chain market structures (e.g., margin, funding rates, 24/7 trading). The regulatory direction is innovation-enabled within guardrails—and Hyperliquid’s positioning—open, global, non-custodial—aligns well with policy discussions focused on preserving permissionless access while introducing appropriate market safeguards.

Risks

HYPE investors should be aware of both conventional risks and certain Hyperliquid-specific risks:

HYPE’s annualized price volatility is ~80%, roughly 40 percentage points higher than Bitcoin. Hyperliquid’s validator set is more concentrated than other blockchain networks, and it runs on closed-source software. Hyperliquid’s growth potential depends partly on evolving U.S. financial services regulation—if regulatory headwinds persist, the platform may remain confined to other jurisdictions, capping growth.

Conclusion

Hyperliquid has no direct counterpart in either crypto or traditional finance. It presents a compelling vision for blockchain-based finance: an open-architecture platform powered by permissionless innovation, upholding DeFi’s principles of transparency and self-custody—while building around an optimized core application proven successful by real user metrics. If it sustains execution discipline, retains and grows its community, and benefits from regulatory evolution, Grayscale believes Hyperliquid has the potential to become a financial services powerhouse.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News