Bitget UEX Daily Report | All Three Major Indices Rise to New Highs for MU; U.S.-Iran Negotiations Continue Progressing; Earnings Season Enters Critical Window

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | All Three Major Indices Rise to New Highs for MU; U.S.-Iran Negotiations Continue Progressing; Earnings Season Enters Critical Window

Overall, the short-term market will be shaped by the interplay among negotiation progress, macroeconomic data, and earnings reports. Investors are advised to adopt a flexible allocation strategy, balancing growth potential with valuation alignment.

I. Top News

Federal Reserve Updates: Officials Emphasize Data-Dependence and Monitor Geopolitical Developments’ Impact on Policy

- Multiple Federal Reserve officials recently reiterated their data-dependent approach, indicating the current interest rate range will remain unchanged for now—though disagreements persist regarding the inflation trajectory.

- Some officials noted that further de-escalation in the Middle East could ease energy price pressures, thereby helping to alleviate broader inflationary concerns.

- Markets expect the Fed to maintain a cautious, wait-and-see stance in the near term.

This posture provides market participants with expectations of policy continuity. Combined with positive geopolitical signals, it may support risk assets—though inflation data remains the decisive variable.

Global Commodities: U.S.-Iran Negotiations Boost Market Confidence, Oil Prices Volatile

- Trump stated negotiations are progressing smoothly, with the U.S. and Iran nearing a framework agreement focused on reopening the Strait of Hormuz and liberalizing oil sales.

- Despite sporadic conflict reports, overall sentiment remains optimistic, leading WTI and Brent crude prices to decline.

- Investors are closely watching whether agreement details can be implemented swiftly.

Positive negotiation progress has eased concerns over energy supply disruptions, offering short-term tailwinds to global growth expectations. However, geopolitical risks have not been fully eliminated, and oil prices remain volatile.

Macroeconomic Policy: Markets Focus on Earnings Season and Macro Data Releases

- This week, multiple tech and consumer giants will report earnings; investors are monitoring AI-related capital expenditures and consumption resilience.

- U.S. consumer confidence data is due soon; both geopolitical developments and economic indicators will jointly shape market sentiment.

- Regulators remain cautious toward integration between crypto and traditional finance.

Earnings performance will serve as a key catalyst for short-term market direction. If results exceed expectations, the current rebound may gain further traction.

II. Market Recap

Commodities & FX Performance

- Spot Gold: +0.3%, at $4,520/oz.

- Spot Silver: +0.27%, at $77.20/oz.

- WTI Crude: -1.16%, at $92.76/bbl.

- Brent Crude: -0.95%, at $95.85/bbl.

- U.S. Dollar Index: -0.05%, at 99.09.

Cryptocurrency Performance

- BTC: -1.01%, trading near $76,000.

- ETH: -0.91%, trading near $2,100.

- Total Crypto Market Cap: -0.6%, at $2.62 trillion.

- Liquidations: $303 million liquidated in past 24 hours, including $199 million in long positions.

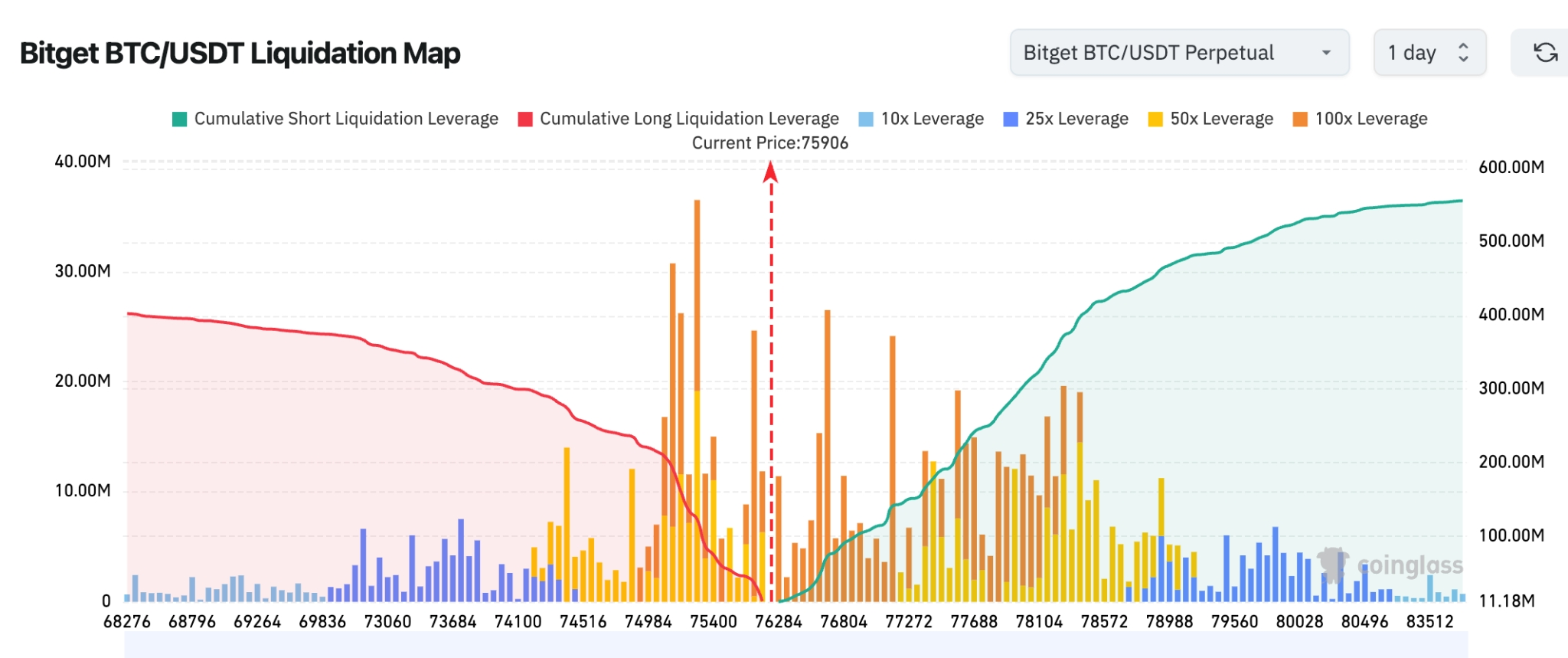

- Bitget BTC/USDT Liquidation Map: Current BTC price ~$75,906. Significant high-leverage short liquidation pressure accumulates above the $76,500–$78,500 range, suggesting strong near-term upward “short-squeeze” momentum. A sustained breakout above $77,000 could trigger cascading short liquidations, accelerating price movement toward the $79,000–$80,000 zone.

- Spot ETF Net Inflows/Outflows: BTC spot ETFs recorded $141 million net outflow yesterday—the seventh consecutive day of outflows.

- BTC Inflows/Outflows: Spot markets saw $59 million net outflow; derivatives markets saw $359 million net outflow.

U.S. Equity Index Performance

- Dow Jones Industrial Average: Down 0.23% at 50,461.68. Early gains driven by easing geopolitical tensions were offset by profit-taking late in the session; index remained in a high-level consolidation pattern.

- S&P 500: Up 0.61% at 7,519.12—setting a new closing high. Defensive sectors and tech stocks rotated in support.

- Nasdaq Composite: Up 1.19% at 26,656.18. Strong performance from tech and semiconductor stocks, with AI themes continuing to drive gains.

Tech Giants’ Performance

- Apple (AAPL): Closed at $308.33, down 0.16%. Its defensive characteristics attracted some inflows, but broader sector rotation led to a modest pullback.

- Microsoft (MSFT): Closed at $416.03, down 0.61%. Long-term AI and cloud business fundamentals remain solid, though short-term profit-taking pressure was evident.

- NVIDIA (NVDA): Closed at $214.86, down 0.22%. AI themes continue to dominate market sentiment, yet elevated valuations triggered profit-taking and fund rotation.

- Amazon (AMZN): Closed at $265.29, down 0.39%. Core e-commerce and AWS cloud businesses remain resilient; anticipated AI infrastructure investments provide a buffer.

- Meta (META): Closed at $612.34, up 0.34%. Positive ad revenue outlook and continued AI-driven content recommendation optimization bolster investor confidence.

- Alphabet (GOOGL): Closed at $382.97, down 1.21%. Russell Index rebalancing reinforced its pure-growth positioning; long-term potential in AI search and cloud services remains widely recognized.

- Tesla (TSLA): Closed at $433.59, up 1.78%. Renewed EV delivery momentum, coupled with energy business and Robotaxi progress, attracted renewed investor attention.

Overall performance was mixed. AI remains the dominant theme—but high-valuation names face mounting profit-taking pressure, resulting in clear fund rotation between defensive and high-growth assets.

Sector Movement Observations

Semiconductor Sector: Mixed Performance

- Key Stocks: Qualcomm (QCOM) surged 11.60%, closing at $238.16; AMD rose 4–8%, recording multiple strong single-day gains recently.

- Catalysts: Demand for AI PCs, data center chips, and automotive semiconductors continues to exceed expectations. Qualcomm’s expanded Snapdragon collaboration with Stellantis—and its AI data center custom silicon project—served as direct triggers. Russell Index rebalancing further highlighted the appeal of growth-oriented stocks. Divergence within the sector stems largely from valuation disparities and fund rotation: AI remains the core theme, yet mature-process players face intensifying competition and softening demand.

- Market Impact: Short-term sentiment across the semiconductor supply chain is significantly boosted. However, caution is warranted following sharp rallies in names like Qualcomm, given upside risks from profit-taking. Longer term, AI’s “super-cycle” should sustain demand for HBM memory and advanced nodes—global semiconductor sales are projected to grow over 26% YoY in 2026. This trend resonates with improved risk sentiment from U.S.-Iran talks, providing additional tailwinds for tech growth equities.

Defensive & Europe-Focused Sectors: Modest Strength

- Key Stocks: European defense firms—including Rheinmetall and BAE Systems—performed steadily; U.S. healthcare and consumer defensive stocks posted modest gains.

- Catalysts: Optimism around advancing U.S.-Iran negotiations accelerated the “post-war trade” theme. Easing energy risks prompted fund flows away from pure safe-haven assets into sectors likely to benefit from reconstruction, stability, and increased European security spending. Rising defense spending as a share of GDP across multiple European countries—combined with growing U.S. defense exports—provides structural upside.

- Market Impact: This rotation reflects asset reallocation amid improving risk appetite—helping reduce overall market volatility and broaden the rally. Should negotiations stall or backslide, defensive sectors may regain safe-haven appeal. Investors may consider cross-allocations combining undervalued European assets and healthcare innovation—particularly within the dual context of geopolitical easing and AI capex expansion.

III. Deep Dive: U.S. Equity Highlights

1. Qualcomm (QCOM) – ByteDance Deal Drives AI Chip Breakthrough

Event Summary: Qualcomm’s stock surged 11.60% on May 26, closing at $238.16—a recent high. The company secured a multi-million-unit AI data center chip supply agreement with ByteDance, expanded its Snapdragon automotive chip partnership with Stellantis, and continues to see robust demand for AI PC chips. Market Interpretation: Analysts view Qualcomm as rapidly diversifying beyond smartphone chips into AI edge computing and data centers. Morgan Stanley notes the ByteDance order validates its competitiveness in AI custom silicon, while rising AI PC penetration is expected to fuel a new growth cycle. Yet long-term market share defense against Intel and MediaTek remains a watchpoint. UBS raised its target price, highlighting strengthened pricing power and an improving revenue mix. Investment Takeaway: Capitalize on short-term elasticity from AI PC cycle initiation and large-customer order execution; position long-term as a core holding in AI edge computing—but dynamically monitor supply-chain stability and competitive evolution.

2. Dell (DELL) – AI Server Orders & Earnings Catalyst

Event Summary: Dell has outperformed recently, fueled by strong AI server orders. Its Q4 FY2026 AI-related server revenue surged YoY, accelerating its data center business transformation. Its earnings report releases this week, drawing intense market focus on its AI server backlog. Market Interpretation: Investment banks favor Dell’s entrenched position in the AI server supply chain. Goldman Sachs observes that hyperscaler capex acceleration reinforces Dell’s “data center + endpoint” dual-engine logic and offers meaningful gross margin upside. UBS cautions that a temporary macro-driven IT spending slowdown could pose near-term headwinds—but the long-term AI infrastructure trend remains intact. Investment Takeaway: Closely monitor this week’s earnings for validation of AI server order strength; hold long-term as a direct beneficiary of AI infrastructure buildout—balancing valuation with earnings delivery timing.

3. Micron (MU) – HBM Capacity Fully Booked Through 2026

Event Summary: Micron’s HBM capacity is fully booked through end-2026 and backed by long-term supply agreements extending into 2027. Its Q2 revenue and gross margin rose sharply, pushing shares to record highs and surpassing a $1 trillion market cap. Market Interpretation: Banks uniformly highlight Micron’s HBM pricing power and supply-demand imbalance. UBS raised its target price to $1,625, forecasting AI-driven memory shortages through 2028 and Micron’s transition from a cyclical player to a strategic AI infrastructure supplier—with 2027 EPS expected near peak levels. Still, institutions warn that slower AI capex growth could trigger price corrections. Investment Takeaway: Track HBM4/HBM4E capacity ramp-up and pricing trends short-term; hold long-term as a core position in the AI memory segment—capturing high growth amid tight supply-demand balance—while setting rational take-profit levels to manage valuation volatility.

4. Broadcom (AVGO) – Dual Leadership in AI ASICs & Networking Chips

Event Summary: Broadcom’s AI custom ASIC chips are gaining steady share among major customers; VMware synergies are emerging, and demand for networking chips and server interconnects is strengthening. Market Interpretation: Institutions emphasize Broadcom’s deep technical moats in AI network infrastructure and custom chips. UBS forecasts high double-digit revenue growth in FY2026 and standout free cash flow generation. JPMorgan highlights its diversified portfolio (semiconductors + software) as enhancing resilience—though concentrated supply chains and geopolitical friction remain long-term risks. Investment Takeaway: Watch for new order execution and earnings catalysts short-term; hold long-term as a stable growth pillar within AI full-stack infrastructure—ideal as a core anchor in tech growth portfolios.

5. AMD – Expanding Data Center GPU Share

Event Summary: Strong demand for AMD’s MI-series GPUs and AI PC processors drove significant YoY growth in data center revenue. Russell Index rebalancing further cemented its growth profile. Market Interpretation: Banks applaud AMD’s differentiated追赶 (catch-up) against NVIDIA in GPUs and EPYC processor penetration. Goldman Sachs notes that the confluence of AI PC adoption and data center capex should lift margins. Yet NVIDIA’s high-end dominance and supply constraints require AMD to consistently demonstrate cost-performance advantages and ecosystem maturity. Investment Takeaway: Focus short-term on new product launches, order progress, and earnings verification; capture long-term opportunities from expanding AI compute market share—while diversifying holdings to hedge against technology iteration risk.

IV. Crypto Project Updates

1. After lying dormant for 11 years, 107 BTC (~$8.3 million) were sent to a burn address. Yesterday, five wallets collectively transferred 107 BTC to a burn address—most having been inactive for 11 years.

2. According to official announcements, FTX has set the estimated registration date for its next round of creditor distributions as June 16, 2026, for users holding approved FTX claims and equity interests. The next distribution is scheduled to begin on July 31, 2026. Preferred shareholders’ next payment will also be made on that date, with the same June 16 registration deadline. Approved NFT customer claim holders may initiate NFT distribution processes starting June 30, 2026.

3. Yesterday (Eastern Time, May 26), the HYPE spot ETF recorded total net inflows of $20.45 million. The Bitwise Hyperliquid ETF (BHYP) led inflows with $19.05 million—bringing its cumulative net inflows to $55.00 million.

4. TD Cowen stated that, amid worsening U.S. political conditions, the likelihood of the CLARITY Act passing this year is diminishing. Jaret Seiberg, Managing Director of TD Cowen’s Washington Research Group, noted recent developments involving President Trump make it harder for Democrats to support the bill unless it includes conflict-of-interest provisions.

5. U.S. President Trump posted on social media publicly supporting his appointee, CFTC Chair Michael Selig, in efforts to expand regulatory authority over prediction markets—calling the issue “critical.”

6. Asset management firm Strive acquired 1,109 BTC for approximately $85.4 million ($76,988 per BTC). The firm disclosed its current BTC holdings now total 16,500 BTC, with QTD returns at 11.0% and YTD returns at 23.4%; its Bitcoin return amplification ratio stands at 45.2%.

V. Today’s Market Calendar

Upcoming Data Releases

Key Event Preview

May 28 (Thursday)

- Major U.S. Earnings: Dell (DELL), Costco (COST) — after-market release ★★★★★;

- Q1 2026 GDP revision, initial jobless claims, and durable goods orders released simultaneously;

- April Core PCE (the Fed’s preferred inflation gauge) ★★★★★

May 29 (Friday)

- U.S. May Chicago PMI

- Speech by Kansas City Fed President Jeffrey Schmid—the 2028 FOMC voting member

- Speech by Fed Governor Michelle Bowman

*This Week’s Key U.S. Equity Themes:

Heightened volatility expected amid the critical U.S.-Iran ceasefire window, April Core PCE data, and the final stretch of Q1 earnings season—including Marvell and Salesforce.

Institutional Views: Leading investment bank analysts note that advancing U.S.-Iran negotiations have injected optimism into markets. Though isolated flare-ups persist, prospects for reopening the Strait of Hormuz support lower oil prices and reduced inflationary pressure—creating space for Fed policy flexibility. J.P. Morgan and others observe broad-based gains in equity index futures, signaling restored risk appetite. AI capex and earnings beats remain primary supports. Goldman Sachs emphasizes that the “post-war trade” theme warrants attention to defensive, healthcare, and European assets. In crypto, easing geopolitics lifts sentiment—but ETF outflows warrant vigilance. Overall, near-term markets will navigate competing forces of negotiation progress, macro data, and earnings—suggesting flexible allocation strategies that balance growth exposure with valuation discipline.

Disclaimer: The above content was compiled via AI search and verified manually prior to publication. It does not constitute investment advice. Data herein may contain inherent discrepancies; please rely on real-time market data for decision-making.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News