Digital banks have long stopped doing traditional banking business—the real goldmine lies in stablecoins and identity verification

TechFlow Selected TechFlow Selected

Digital banks have long stopped doing traditional banking business—the real goldmine lies in stablecoins and identity verification

The market is gradually moving away from fragmented KYC processes across platforms, shifting toward portable verified identity systems that can be used across services, countries, and platforms.

Author: Vaidik Mandloi

Translation: Chopper, Foresight News

Where Is the Real Value in Digital Banking Heading?

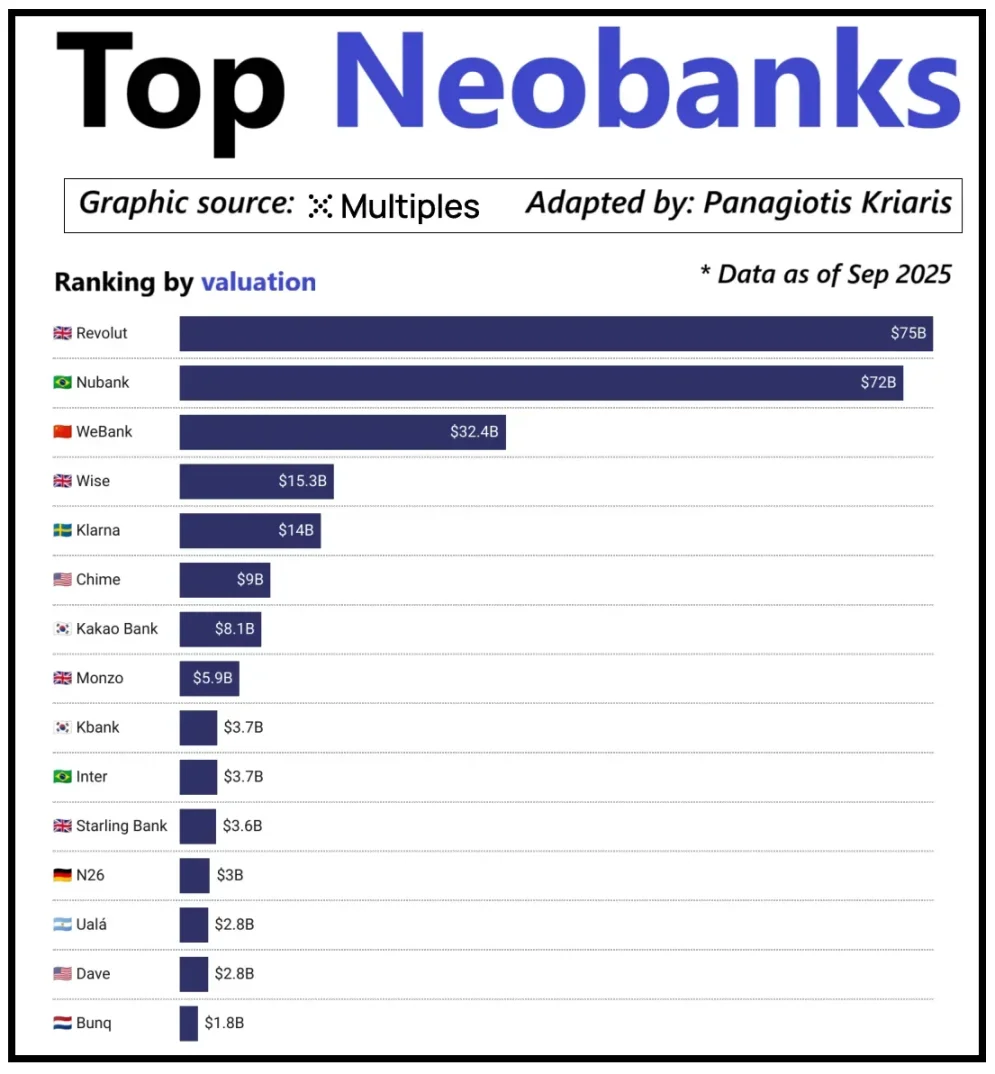

Looking at the world's leading digital banks, their valuations are not simply determined by user scale, but rather by per-customer revenue generation. Revolut is a classic example: although it has fewer users than Brazil’s Nubank, its valuation surpasses Nubank's. The reason lies in Revolut’s diversified revenue streams—spanning foreign exchange trading, securities trading, wealth management, and premium membership services. In contrast, Nubank primarily expands its business through credit operations and interest income, not card fees. China’s WeBank has taken yet another differentiated path, achieving growth through extreme cost control and deep integration into Tencent’s ecosystem.

Valuations of Leading Emerging Digital Banks

Today, crypto-native digital banks are reaching a similar inflection point. A “wallet + debit card” combo can no longer be considered a viable business model—any institution can easily launch such a service. The real competitive edge now lies in the core monetization strategy each platform chooses: some earn interest from user account balances; others profit from stablecoin payment volumes; and a few place their growth potential on stablecoin issuance and management, which is currently the most stable and predictable revenue source in the market.

This also explains why the stablecoin sector is becoming increasingly critical. For reserve-backed stablecoins, the core profit comes from investment returns on reserves—interest generated by allocating reserves into short-term Treasuries or cash equivalents. This income flows to the stablecoin issuer, not to digital banks that merely offer users stablecoin holding and spending functionality. This profit model isn’t unique to crypto: in traditional finance, digital banks cannot earn interest from user deposits either—the actual yield goes to partner banks that hold the funds. Stablecoins make this “separation of income rights” more transparent and centralized: entities holding Treasuries and cash equivalents earn interest, while consumer-facing apps focus on user acquisition and experience optimization.

As stablecoin adoption grows, a contradiction emerges: platforms responsible for user onboarding, transaction facilitation, and trust-building often cannot profit from the underlying reserves. This value gap is pushing companies toward vertical integration, moving beyond being mere front-end tools to controlling fund custody and management—the core layers of the system.

It’s precisely for this reason that companies like Stripe and Circle are intensifying their involvement in the stablecoin ecosystem. They’re no longer content with just distribution—they’re expanding into settlement and reserve control, which are the true profit centers. For instance, Stripe launched its own blockchain, Tempo, specifically designed for low-cost, instant stablecoin transfers. Instead of relying on existing public chains like Ethereum or Solana, Stripe built its own transaction channel, giving it full control over settlement processes, fee pricing, and throughput—all directly translating into better economics.

Circle has adopted a similar strategy, building Arc, a dedicated settlement network for USDC. With Arc, institutional USDC transfers settle instantly without congesting public chains or incurring high fees. In essence, Circle has created an independent backend system for USDC, freeing itself from reliance on external infrastructure.

Privacy is another key driver behind this move. As Prathik explained in his article "Making Blockchains Great Again", public blockchains record every stablecoin transfer on a transparent ledger. While suitable for open financial systems, this poses issues in corporate use cases like payroll, vendor payments, and treasury management—where transaction amounts, counterparties, and payment patterns are sensitive.

In practice, the transparency of public chains allows third parties to use blockchain explorers and on-chain analytics tools to reconstruct a company’s internal financial activities. Arc enables institutions to settle USDC transfers off-chain, preserving the speed of stablecoin settlements while ensuring transaction confidentiality.

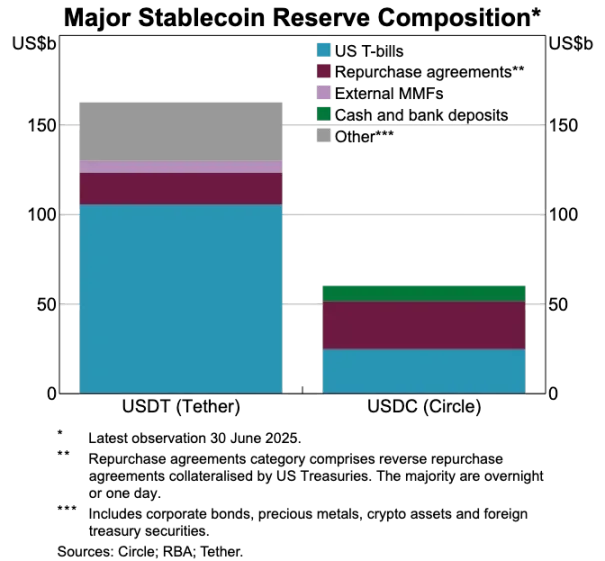

Reserve Composition Comparison: USDT vs USDC

Stablecoins Are Disrupting the Old Payment System

If stablecoins represent the real value center, then the traditional payment system appears increasingly outdated. Current payment flows involve multiple intermediaries: payment gateways collect funds, processors route transactions, card networks authorize them, and the banks of both parties complete final settlement. Each step adds cost and causes delays.

Stablecoins bypass this entire chain. Transfers don’t require card networks or acquirers, nor do they wait for batch settlement windows—instead, they enable peer-to-peer direct transfers via the underlying network. This shift profoundly impacts digital banks, as it redefines user expectations: if users can achieve instant transfers elsewhere, they won’t tolerate slow, expensive internal bank transfers. Digital banks must either deeply integrate stablecoin transfer channels or risk becoming the least efficient link in the payment chain.

This transformation is reshaping digital banking business models. In the traditional system, digital banks earned steady interchange fees because payment networks controlled the core transaction flow. But in a stablecoin-dominated system, that revenue is severely compressed: peer-to-peer stablecoin transfers have no fees, leaving card-reliant digital banks competing in a zero-fee environment.

Thus, the role of digital banks is shifting—from card issuers to payment routing layers. As payments evolve from cards to direct stablecoin transfers, digital banks must become central nodes in stablecoin transaction flows. Those capable of efficiently processing stablecoin traffic will dominate the market, because once users adopt them as the default transfer channel, switching becomes unlikely.

Identity Is Becoming the Next-Gen Account Layer

As stablecoins make payments faster and cheaper, another bottleneck becomes apparent: identity verification. In traditional finance, identity verification is a separate process—banks collect documents, store data, and conduct backend reviews. But in a world of instant wallet transfers, every transaction depends on a trusted identity system. Without it, compliance checks, anti-fraud controls, and basic access management collapse.

For this reason, identity verification and payment functions are rapidly converging. The market is moving away from fragmented, platform-specific KYC processes toward portable identity systems that work across services, countries, and platforms.

This shift is already underway in Europe, where the EU Digital Identity Wallet is entering implementation. Instead of requiring every bank and app to run independent verifications, the EU is launching a government-backed universal identity wallet usable by all residents and businesses. Beyond storing identity, it holds verified credentials (age, residency, licenses, tax info), supports e-signatures, and includes payment functionality. Users can complete identity verification, selective data sharing, and payments in one seamless flow.

If the EU Digital Identity Wallet succeeds, it will reshape European banking: identity—not bank accounts—will become the primary gateway to financial services. Identity will become a public utility, eroding distinctions between banks and digital banks unless they build value-added services atop this trusted identity layer.

The crypto industry is moving in the same direction. On-chain identity experiments have been ongoing for years. While no perfect solution exists yet, all efforts converge on one goal: enabling users to prove identity or specific facts without locking their data within a single platform.

Key examples include:

-

Worldcoin: Building a global proof-of-personhood system that verifies human identity without compromising privacy.

-

Gitcoin Passport: Aggregating reputation and verification signals to reduce Sybil attacks in governance and reward distribution.

-

Polygon ID, zkPass, and ZK-proof frameworks: Allowing users to prove specific facts without revealing underlying data.

-

Ethereum Name Service (ENS) + off-chain credentials: Enabling crypto wallets to display not just assets, but also social identities and verified attributes.

Most crypto identity projects share the same goal: letting users self-sovereignly prove identity or facts without being locked into any single platform. This aligns perfectly with the EU’s vision—a single credential that moves freely across apps without repeated verification.

This trend will likewise transform digital banking operations. Today, digital banks treat identity verification as a core control point: users register, platforms review, and accounts are created within the platform. But when identity becomes a portable, user-controlled credential, digital banks shift to being service providers plugged into this trusted identity layer. This simplifies onboarding, reduces compliance costs, eliminates redundant checks, and positions crypto wallets—not bank accounts—as the primary carriers of user assets and identity.

Future Outlook

In summary, once-core advantages in digital banking are losing relevance: user scale is no longer a moat, debit cards are no longer a moat, and even clean UIs are no longer a moat. True competitive differentiation now hinges on three dimensions: the monetization product chosen, the fund movement channel relied upon, and the identity system integrated. Everything else will gradually converge and become increasingly interchangeable.

Future successful digital banks won’t be lightweight versions of traditional banks, but wallet-first financial systems. They’ll anchor themselves around a core profit engine, which directly determines their margin and defensibility. Broadly speaking, there are three types of core profit engines:

Interest-Driven Digital Banks

Their competitive advantage lies in becoming the preferred destination for users to hold stablecoins. By aggregating large user balances, these platforms generate revenue through interest on reserve-backed stablecoins, on-chain yields, staking, and restaking—without needing massive user numbers. Their strength? Earning from asset holding is far more efficient than earning from asset movement. These platforms may appear consumer-facing, but they’re essentially modern savings platforms disguised as wallets, competing on seamless yield-generating deposit experiences.

Payment-Flow-Driven Digital Banks

Their value stems from transaction volume. They become the primary channel for users to send, receive, and spend stablecoins, deeply integrating payment processing, merchants, fiat-crypto on/off ramps, and cross-border payments. Their revenue model resembles that of global payment giants: tiny margins per transaction, but substantial total income if they become the default money movement channel. Their moat? User habit and reliability—being the go-to choice whenever users need to move funds.

Stablecoin Infrastructure-Driven Digital Banks

This is the deepest and potentially most lucrative layer. These banks aren’t just stablecoin conduits—they aim to control stablecoin issuance or at least its core infrastructure, covering issuance, redemption, reserve management, and settlement. Profit potential here is highest, since control over reserves dictates who captures yield. These banks blend consumer features with infrastructure ambitions, evolving from apps into full-stack financial networks.

In short, interest-driven banks profit when users deposit coins, payment-flow-driven banks profit when users transfer coins, and infrastructure-driven banks profit regardless of what users do.

I predict the market will split into two camps: the first comprises consumer-facing platforms that integrate existing infrastructure, offering simple, user-friendly products with very low switching costs. The second moves toward core value aggregation—focusing on stablecoin issuance, transaction routing, settlement, and identity integration.

The latter will no longer be just apps, but infrastructure providers wearing consumer-facing clothing. They’ll achieve high user stickiness by quietly becoming the foundational systems for on-chain fund movement.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News