Price discovery on-chain

TechFlow Selected TechFlow Selected

Price discovery on-chain

Why should the ability to discover fair asset prices depend on your time zone or what day of the week it is?

Author: Charlie.hl, desh_saurabh

Translation: Block unicorn

Introduction

The New York Stock Exchange is open five days a week for just 6.5 hours per day—only 27% of the total weekday hours. For the remaining 73% of each weekday, the trading system sits idle. How do we address this?

For over 17 hours every business day, we have no way to know “what someone globally would pay for this asset right now,” because the infrastructure for price discovery has been deliberately shut down. This creates a fundamental paradox in modern trading: an asset that can be traded at any time is inherently more valuable than its counterpart restricted to six-hour trading windows—the value of liquidity. It’s valuable to be able to enter or exit positions when information emerges. As we’ll explain later, being unable to act on opportunities directly costs traders. Yet we’ve built multi-trillion-dollar markets on a system that blocks access to liquidity for over 70% of the time.

Strangely, the issue isn’t that technology cannot support continuous or extended trading hours. The gap between what technology enables and how markets actually operate has never been wider. We can instantly communicate with people on the other side of the planet and complete peer-to-peer payments in seconds. But if you're chatting with a friend late Saturday night about Tesla and its future, and your friend wants to buy Tesla shares at 3 a.m., it's simply impossible—not because there are no sellers, nor because the technology to facilitate trades is lacking, but because market operations are still built on systems designed for an era when information traveled by telegraph and settlement required physical certificates.

This matters because every hour the market is closed, information accumulates: earnings reports come out after hours, geopolitical events unfold overnight, company announcements drop over weekends. All this information holds value—and that value gets compressed into the first few minutes of the next trading session. The result? Price gaps, volatility spikes, and losses from inefficiency that aren't evenly distributed across market participants, but instead fall disproportionately on traders without tools to protect themselves.

The assumption that markets must close has become so ingrained that most participants never question it. Why should the ability to discover an asset’s fair price depend on your time zone or the day of the week? The answer reveals a system optimized for constraints decades old—one we'll explore here, along with solutions involving moving price discovery and markets on-chain.

The Overnight Gap Problem

The inefficiency of market closures manifests in data as a persistent, quantifiable drag on returns. Study after study documents the same anomaly: most of the U.S. stock market’s gains occur while the market is closed.

From 1993 to 2018, the S&P 500’s cumulative overnight return averaged 2.75 basis points higher per day than its intraday return. Compounded annually, that difference amounts to roughly 7.2%. That’s not trivial.

But during certain periods, the effect is even more extreme. Between 1993 and 2006, all of the U.S. equity premium was generated overnight. If you bought at close and sold at open, you captured all the gains. If you bought at open and sold at close, your return was zero—or negative. There were no gains during actual trading hours. All returns accumulated in price gaps.

Traders have known this for decades. Statistical arbitrage strategies exploiting overnight price movements have achieved annualized returns over 51%, with Sharpe ratios exceeding 2.38. Researchers documented 2,128 overnight gaps in the S&P 500 alone between 1998 and 2015. The consistency and exploitability of this pattern suggest risk is mispriced. If pricing were accurate, such opportunities wouldn’t persist.

Negative gaps are larger and more volatile than positive ones. When bad news drops after hours, markets overreact. Overnight declines are significantly steeper than gains, and the standard deviation of negative gaps is markedly higher than that of positive gaps. This introduces tail risks invisible during regular trading. Holding a position overnight exposes you to unhedgeable downside risk due to market closure.

This isn’t how efficient markets are supposed to work. In theory, prices should reflect all available information at all times. In reality, prices only update when the market opens. Market closures create blind spots. Information arrives, but prices can’t adjust until the market reopens—by which time, timing is lost and the opportunity to trade at fair value disappears.

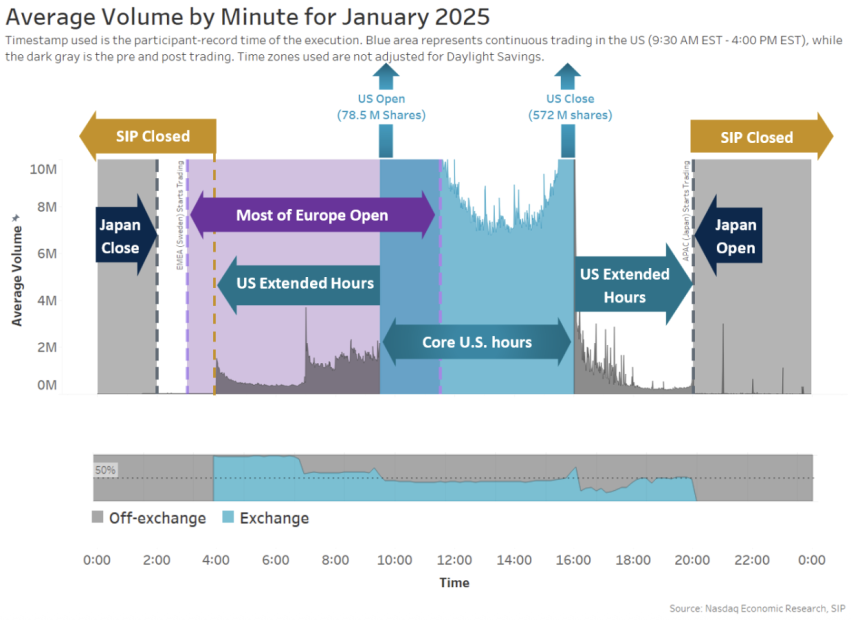

A small number of investors who can trade after hours face different issues. After-hours volume accounts for just 11% of daily total volume, and overnight trading from 8 p.m. to 4 a.m. makes up only 0.2% of market activity. This lack of liquidity leads to predictable costs.

NASDAQ minute-by-minute volume distribution, January 2025

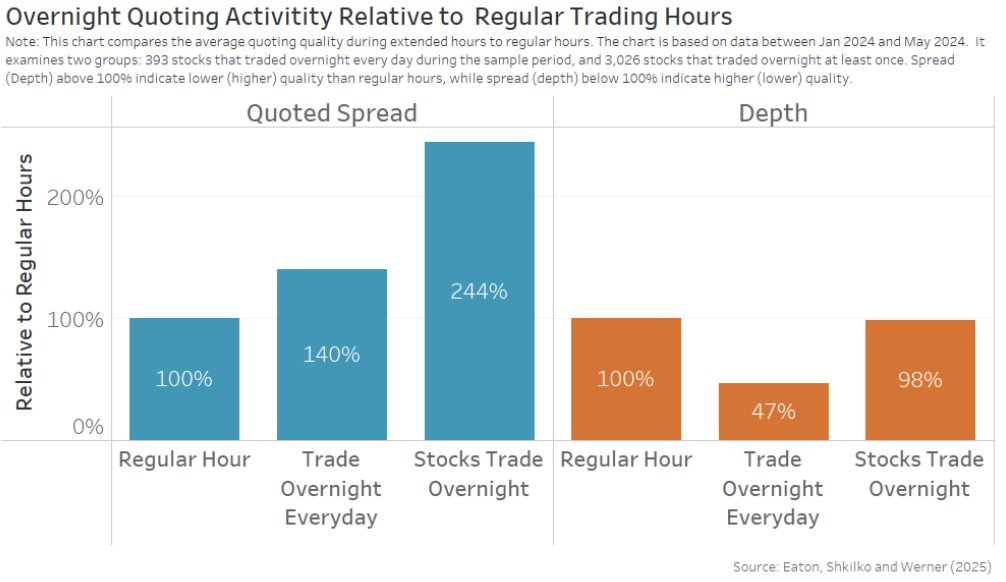

Spreads widen sharply after exchanges halt trading. For stocks traded overnight, bid-ask spreads expand by about 40% compared to regular hours. For less liquid stocks, spreads balloon by up to 144%. Market depth for the most active stocks drops to just 47% of normal levels. As a result, retail orders executed overnight face effective spreads three times wider than during the day, with price impact increasing sixfold.

Overnight quote study—Eaton, Shkilko, and Werner

Trading costs also differ dramatically. After-hours trading costs are four to five times higher than during regular hours. Most overnight trades execute at or below the best quoted price. Who trades under these conditions? According to Nasdaq data, about 80% of overnight volume comes from the Asia-Pacific region, half of which originates from South Korea. The remaining 20% consists largely of U.S. retail investors—individuals trying to respond to information in real time, paying multiples of normal trading costs to do so.

Retail investors suffer a double blow from this structural flaw. They lack robust pre-market trading infrastructure. They can’t adjust positions after hours without paying exorbitant spreads. When markets gap open due to overnight news, their positions move against them while they sleep. Professional traders with 24/7 infrastructure capture the gains, while retail bears the losses.

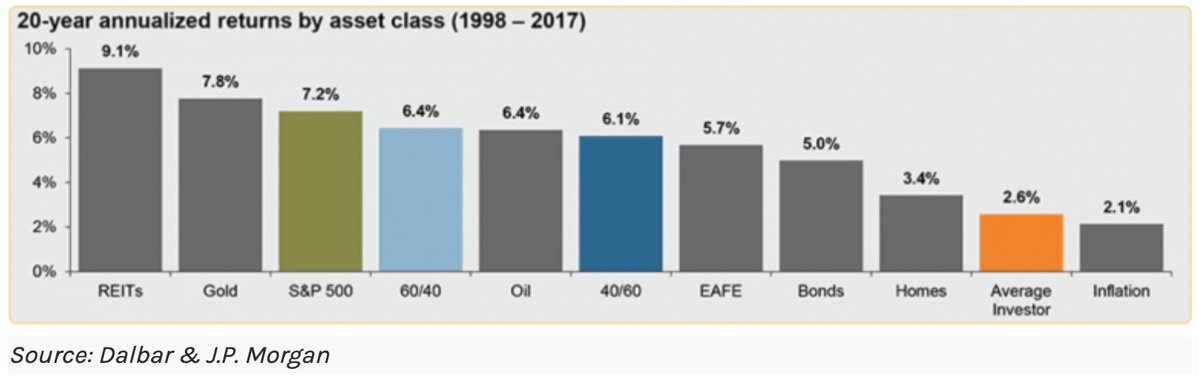

The scale of this wealth transfer is substantial. Retail investors underperform the S&P 500 by an average of 5.2% annually.

20-year annualized returns across asset classes—Dalbar and JPMorgan

When overnight returns consistently outpace intraday returns by 7%, retail investors systematically miss this premium due to their inability to optimize holdings. The long-term compounding effect is clear. This isn’t just about timing skill or stock-picking ability—it’s a structural disadvantage baked into the market architecture itself.

Geographic Fragmentation

Time fragmentation is only one side of the problem. Markets are also fragmented geographically. The same asset may trade at different prices across countries and regions—not just because some participants have better information, but because infrastructure impedes price convergence.

Between 2017 and 2018, Bitcoin traded at an average premium of around 10% on Japanese exchanges. We witnessed this firsthand during a Japan-based Bitcoin arbitrage strategy implemented before Sam Bankman-Fried founded FTX in 2018. These price differences stemmed entirely from outdated, disconnected infrastructure in an increasingly interconnected world.

The phenomenon was even more pronounced in South Korea. From January 2016 to February 2018, Bitcoin on Korean exchanges traded at an average premium of 4.73% above U.S. prices. In January 2018, the premium spiked to 54%. At peak prices, you could buy Bitcoin for $10,000 in the U.S. and sell it for $15,000 in Korea.

Why did this premium exist? South Korea imposes strict capital controls—money flows easily into the country, but getting it out requires navigating complex regulations aimed at preventing money laundering and capital flight. These restrictions make large-scale arbitrage difficult, even when opportunities are obvious. For most participants, the necessary infrastructure for arbitrage simply didn’t exist.

But this isn’t unique to crypto. Traditional equities show similar patterns. Dual-listed companies often exhibit persistent price discrepancies that last months or even years. For example, Royal Dutch Shell shares listed in Australia and London traded at a significant premium over their UK-listed counterparts. Rio Tinto, despite offering identical dividends and equity rights to shareholders, showed notable price differences between its Australian and London listings.

These gaps shouldn’t exist. In truly efficient, globally integrated markets, arbitrageurs would immediately eliminate any price differences—buy low, sell high, pocket the spread.

The reason lies in geographic fragmentation. An investor in Utah can’t buy Indian stocks at 2 a.m. Not because there are no Indian sellers, nor because the asset is inaccessible. Buyers want to buy, sellers want to sell—but infrastructure prevents frequent matching. Despite technology having eliminated any technical barriers to global instant trading, markets remain isolated by geography.

During the 2017–2018 surge in crypto trading volume, potential arbitrage profits between the U.S., South Korea, Japan, and Europe exceeded $2 billion. But existing infrastructure couldn’t capture those profits. That’s the cost of fragmentation. Price discovery happens in isolated pockets rather than globally. Liquidity is scattered across regions. Investors in the wrong place at the wrong time pay premiums simply because the market refuses to treat the same asset as equal everywhere.

Private Markets Are Worse

Public markets are closed 73% of the week. Private markets are never open.

As of June 2023, private equity assets under management had ballooned to approximately $13.1 trillion. Companies that once rushed to go public now stay private for a decade or longer. The average time from founding to IPO has stretched from four years in 1999 to over ten years today. By the time retail investors gain access via public markets, most value creation has already occurred behind closed doors.

Secondary markets for private equity do exist, but calling them “markets” is overly generous. Transactions typically take about 45 days to settle. In today’s environment, even T+2 equity settlement seems fast. Price discovery occurs through private negotiations between counterparties who may or may not possess accurate information about the underlying asset. In June 2024, some secondary buyers valued SpaceX at $210 billion—just six months after it traded at $180 billion.

Stripe experienced similar volatility. Secondary transactions placed its valuation anywhere between $65 billion and $70 billion, depending on buyer and timing. Without continuous price discovery, valuations drift rather than converge.

The cost of illiquidity shows up as persistent discounts. In Q1 2025, pre-IPO stock trades in the secondary market averaged a 16% discount to the latest funding round price. That’s the price you pay just to exit. Because continuous trading isn’t possible, each transaction demands giving up significant value to access your own capital.

Over $50 billion in capital is locked in pre-IPO companies. Money is invested but inaccessible. Valuations are uncertain, exit timelines unknown. The current system lacks the infrastructure to make these assets liquid. Investors hold positions they can’t price or sell, watching opportunities pass while their capital remains trapped.

The gap between what technology enables and what private markets deliver is even wider than in public equities. We have the capability to make any asset tradable, enable continuous price discovery, and eliminate geographic barriers. Yet we maintain a system where access depends on connections, pricing depends on backroom deals, and liquidity depends on gatekeepers’ decisions.

Infrastructure Mismatch

Inefficiency persists because the infrastructure was never designed for the world we live in today.

When the NYSE was founded in 1792, settlement required physical certificates. Buyers and sellers needed time to deliver paper documents, verify authenticity, and manually record ownership changes in ledgers. The settlement mechanism dictated market rhythm. Technology has advanced, but the underlying architecture has barely changed.

Today, stock purchases still require two business days to settle—known as T+2, shortened from T+3 in September 2017, as if cutting three days to two represented revolutionary progress. Trades execute instantly; your account reflects holdings immediately. But actual settlement—the formal transfer of ownership and finality of the trade—still takes 48 hours.

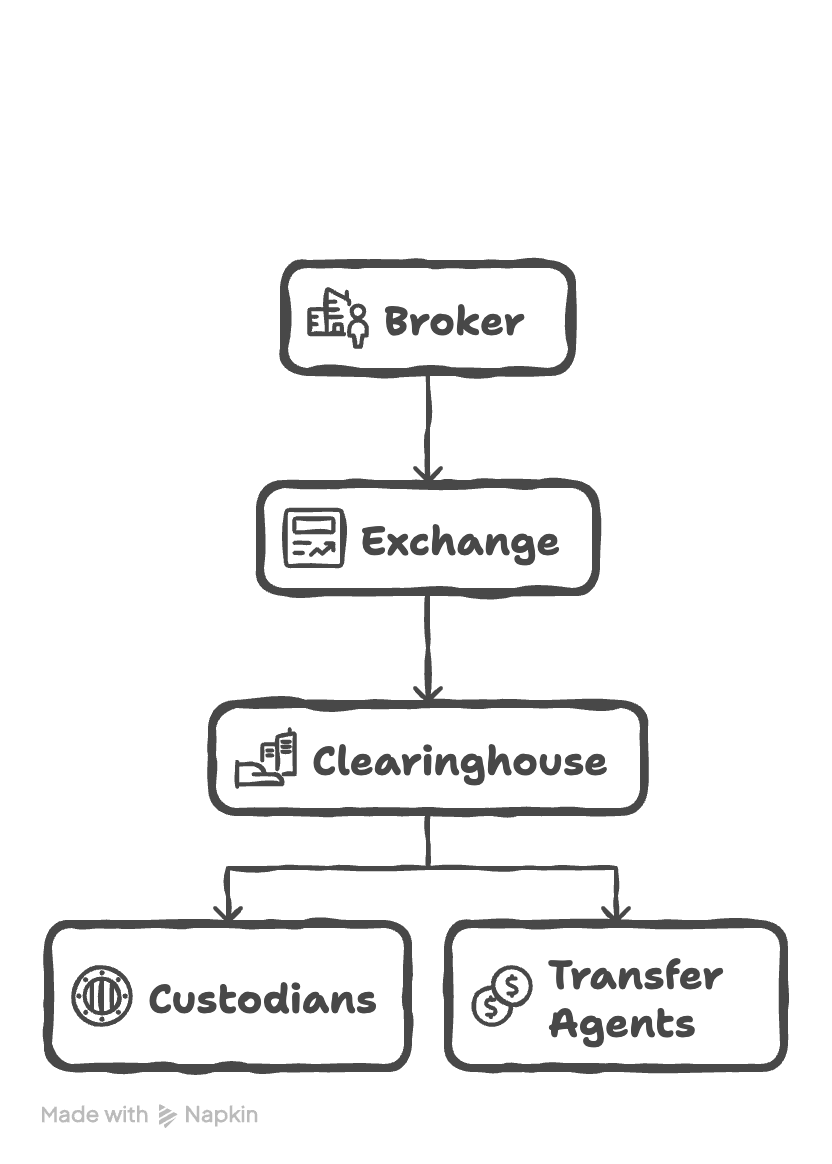

Given that instant settlement technology has existed for decades, why does this delay persist? Because the current system involves layers of intermediaries, each adding latency. Your broker sends the order to an exchange. The exchange matches buyers and sellers. Trade data flows to a clearinghouse. The clearinghouse becomes the counterparty to both sides, assuming default risk. Custodians hold the actual securities. Transfer agents update ownership records. Each institution runs its own systems on its own schedule, batch-processing trades rather than settling continuously in real time.

Layered infrastructure

This stacking of intermediaries also means stacking of costs. Clearinghouses charge fees, custodians charge fees, transfer agents charge fees. The infrastructure itself extracts value from every transaction. Capital sits idle that could otherwise be deployed. Transactions that should complete instantly are stretched over days and routed through multiple middlemen. The facade of a digital market hides the reality that settlement still follows a model designed for physical certificates and telegraph communication.

What would markets look like if settlement were truly instant? What if ownership transferred atomically the moment a trade executes? What if no intermediaries were needed between buyer and seller, because the trade itself—guaranteed cryptographically—ensured singular completion or failure? The infrastructure to build such a system already exists. The issue isn’t technological capability, but whether markets will migrate onto rails compatible with modern technology.

Architecture of Continuous Markets

The promise of continuous markets goes far beyond extending exchange hours. A true continuous market fundamentally redefines price discovery: trading infrastructure runs perpetually, unimpeded by business hours, geographic boundaries, or settlement delays.

In a continuous market, when news breaks at 3 a.m. Eastern Time, the market reacts immediately—no pressure buildup, no violent release at 9:30 a.m. The overnight gap problem vanishes because there is no “overnight.”

Settlement happens nearly instantly, not over the traditional two-day cycle. An investor closing a position at 2 p.m. eliminates their exposure immediately, rather than waiting 48 hours for settlement to finalize. This removes the risk window where portfolio exposure lingers despite execution. Capital previously locked in clearinghouse margins becomes instantly redeployable, rather than sitting idle for days.

On-chain infrastructure makes this possible by maintaining a globally synchronized ledger that runs continuously. Platforms like Hyperliquid demonstrate the feasibility of this technology at scale, with sub-second settlement finality and 24/7 operation. Their infrastructure handles hundreds of thousands of orders per second while ensuring full transparency for every transaction. Participants anywhere, at any local time, access the same liquidity. Settlement occurs via consensus, not days-long batch processing across intermediaries.

The key breakthrough is replacing the layered architecture of traditional markets with a unified execution layer. Modern exchanges coordinate brokers, clearinghouses, and depositories through systems designed for an era of physical stock certificates. On-chain systems collapse these layers into a single settlement mechanism, where trade execution and final settlement happen atomically. The same transaction that matches buyer and seller also transfers ownership with cryptographic finality.

This shift transforms how markets operate. Retail investors avoid the systemic disadvantages of overnight gaps, while institutional traders capture excess returns from post-market activity. At 10 a.m. Tokyo time, a Japanese pension fund rebalances its portfolio with the same liquidity available to a hedge fund operating in California at 5 p.m. Pacific time—both orders drawing from the same global pool of capital. This is the price discovery mechanism we want. No one in Korea should pay a 50% premium over someone in the U.S. just to buy Bitcoin.

Enabling Perpetual On-Chain Price Discovery

Existing infrastructure already supports applications beyond crypto-native assets. Tokenized firms like Ondo Finance have created blockchain versions of popular global equities including Tesla and NVIDIA. These tokenized versions trade 24/7 and settle instantly on-chain, while market makers arbitrage price differences against traditional venues to maintain 1:1 parity. This arbitrage keeps tokenized stock prices aligned with their off-chain counterparts. But as on-chain liquidity grows and updates faster than traditional markets, the direction of price leadership may reverse. Eventually, market makers will quote primarily based on on-chain pricing, rather than treating blockchain markets as derivative followers of traditional exchanges.

This shift eliminates the need for centralized ownership databases. Trusted platforms like Fidelity or Charles Schwab can build advisory services and user-friendly frontends atop blockchain infrastructure, while actual asset trading and settlement occur transparently in the background. Tokenized assets become productive capital—usable as collateral in lending markets or in yield-generating strategies—while maintaining perpetual tradability and transparent, universally accessible ownership records.

The implications extend further, into domains currently even less transparent than public equities. Private markets for secondary stock and pre-IPO assets suffer from information asymmetry largely driven by geography and distance from potential counterparties. Blockchain infrastructure enables global participation in these opaque markets and facilitates continuous price discovery.

Protocols built on Hyperliquid’s infrastructure now support perpetual futures contracts for both public and private equity. Ventuals offers leveraged perpetual exposure to pre-IPO companies like OpenAI, SpaceX, and Stripe, allowing traders to go long or short on these private assets with leverage. Felix Protocol and trade.xyz offer similar perpetual contracts for listed stocks, enabling 24/7 trading beyond exchange hours. These stock perpetuals settle on-chain with instant finality and transparent execution—just like crypto-native assets—eliminating the settlement delays and geographic constraints common in traditional equity derivatives.

Currently, these platforms rely on oracle systems that aggregate price data from various off-chain sources before uploading it on-chain for settlement. For pre-IPO assets, oracles consolidate fragmented data from secondary sales, tender offers, and recent funding rounds to establish reference prices. For listed stocks, oracles pull prices from traditional exchanges during trading hours and switch to a self-referential pricing model outside those hours. But as more stock trading migrates on-chain for primary execution, these oracle systems will become unnecessary. The on-chain order book itself will provide continuous price discovery, and perpetual contract platforms can offer leveraged exposure directly based on these transparent price feeds.

These applications share a common architecture. Traditional markets fragment liquidity across time zones, restrict access by geography or accreditation, and delay settlement through multi-party coordination. On-chain trading infrastructure unifies liquidity globally, offers open access to any internet-connected participant, and enables atomic settlement via cryptographic consensus. The result? Assets once priced only through opaque bilateral negotiations or sporadic trading within limited windows can now achieve continuous price discovery.

Market makers provide liquidity continuously across all hours, rather than withdrawing during volatile periods or scheduled maintenance. The infrastructure maintains order book depth at all times, rather than thinning when regional participation wanes. As a global pool of participants competes more intensely, bid-ask spreads narrow without isolated trading windows.

These capabilities already exist and operate at significant scale. The infrastructure processes hundreds of billions in trading volume monthly, maintaining sub-second settlement and continuous uptime. Extending this architecture from crypto-native assets to tokenized stocks, and eventually to private market instruments, requires primarily regulatory adaptation—not technological innovation. The technology proves that markets can function as unified global mechanisms, rather than collections of regional exchanges passing batons on a schedule.

Continuous markets eliminate artificial constraints on price discovery imposed by legacy infrastructure. They replace fragmented regional trading windows with perpetual global access, multi-day settlement cycles with instant settlement, and opaque private negotiations with transparent order books. This technology already exists and operates at scale, demonstrating that markets no longer need to close—and assets no longer need to trade in the dark. Bring price discovery on-chain.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News