Bitcoin drops below $80,000: Will it spell doom for MicroStrategy?

TechFlow Selected TechFlow Selected

Bitcoin drops below $80,000: Will it spell doom for MicroStrategy?

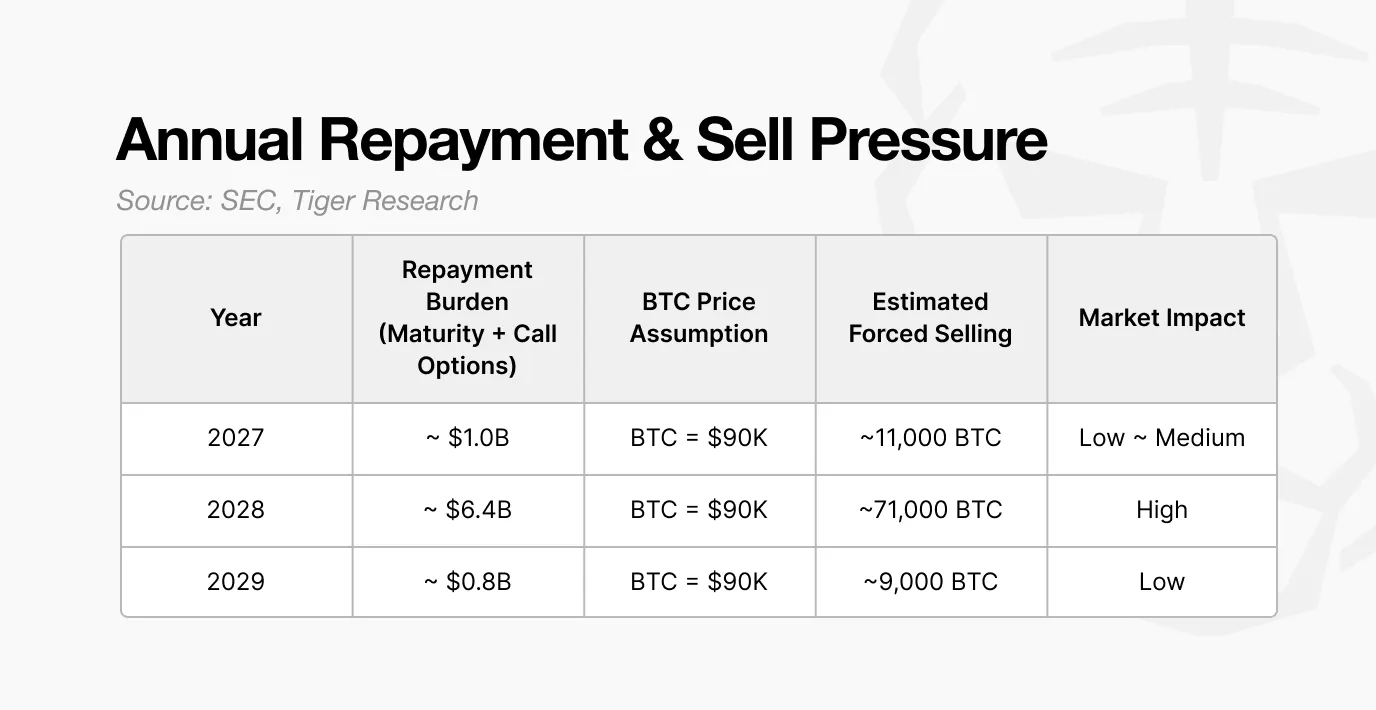

If refinancing fails in 2028 and assuming a Bitcoin price of $90,000, Strategy may need to sell approximately 71,000 bitcoins.

Translation: TechFlow

As Bitcoin prices fall, market attention has shifted to DAT companies holding large amounts of Bitcoin. Among them, Strategy (MicroStrategy) is one of the most prominent players. The key questions are how this company accumulated its assets and how it manages risk amid increasing market volatility.

Key Takeaways

-

Strategy's (MicroStrategy) estimated static bankruptcy threshold in 2025 is approximately $23,000—nearly double the $12,000 level seen in 2023.

-

In 2024, the company changed its capital-raising model, shifting from simple cash and small convertible bonds to a diversified structure including convertible bonds, preferred shares, and ATM issuance (At-The-Market Issuance).

-

Investor-held call options allow for early redemption. If Bitcoin prices decline, investors may exercise these options, making 2028 a critical risk window.

-

If refinancing fails in 2028, assuming a Bitcoin price of $90,000, Strategy (MicroStrategy) might need to sell about 71,000 Bitcoins—equivalent to 20%–30% of daily average trading volume—exerting significant pressure on the market.

1. Questions About Strategy’s (MicroStrategy) Stability

Bitcoin’s recent decline has led to roughly a 50% drop in stocks of DAT companies, raising a core market question: Can Strategy (MicroStrategy) remain stable when both its stock price and core asset value are falling? Concerns intensified after JPMorgan pointed out that Strategy (MicroStrategy) could be removed from the MSCI index.

The focus extends beyond stock performance. The amount of Bitcoin held by Strategy (MicroStrategy) is substantial enough to impact the entire market, far exceeding that of a typical “whale.” This raises two key questions:

-

At what Bitcoin price level would Strategy’s (MicroStrategy) balance sheet collapse?

-

When and under what conditions could the company affect the market?

This report analyzes filings with the U.S. Securities and Exchange Commission (SEC) to explore Strategy’s (MicroStrategy) effective bankruptcy threshold, periods of heightened risk, and potential market impacts under stress scenarios.

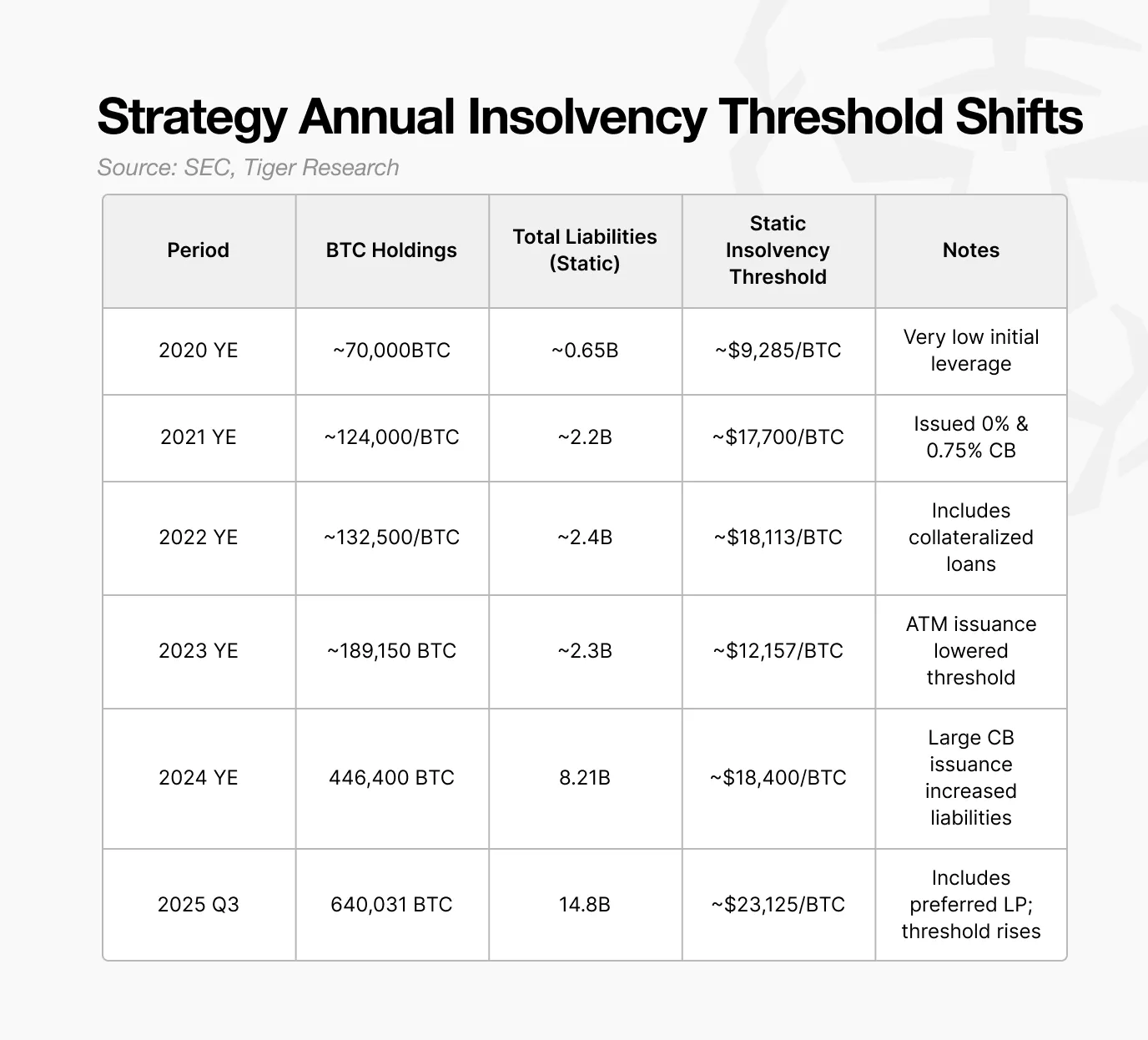

2. Is Strategy (MicroStrategy) at Risk? The $23,000 Threshold

Before diving into analysis, we must clarify the concept of "static bankruptcy." Static bankruptcy occurs when a company cannot repay its liabilities even after liquidating all its assets.

In simple terms, static bankruptcy happens when assets are less than liabilities. For example, if a company named Echo owns real estate worth 1 billion KRW and holds 100 million KRW in cash, but owes 1.2 billion KRW, it is insolvent on a balance sheet basis. The situation is similar for DAT companies: if Bitcoin’s price drops below a certain level, book equity turns negative, and the company can no longer meet its debt obligations. This price point is known as the "static bankruptcy threshold."

To determine Strategy’s (MicroStrategy) static bankruptcy threshold, we first need to understand how the company built up its Bitcoin holdings.

Strategy (MicroStrategy) has held Bitcoin as a strategic asset since 2020, but its accumulation strategy changed after 2023. Prior to that, the company mainly relied on cash reserves and small-scale convertible bonds to purchase Bitcoin. Holdings remained around 100,000 BTC, with relatively limited refinancing obligations.

Starting in 2024, the company altered its funding approach. By issuing preferred shares, implementing an ATM stock program (At-The-Market Stock Program), and launching large-scale convertible bond offerings, Strategy (MicroStrategy) increased its leverage to fund additional Bitcoin purchases.

This strategy led to rapid growth in Bitcoin holdings. It created a cycle: rising Bitcoin prices boost the company’s market cap, enabling higher leverage and further purchases.

While its goal remains unchanged, the mix of funding sources and associated risk profile have evolved. This structural shift now forms the core factor increasing Strategy’s (MicroStrategy) bankruptcy risk.

Based on estimates, Strategy’s (MicroStrategy) static bankruptcy threshold in 2025 is around $23,000. Below this level, the value of its Bitcoin holdings would fall below liabilities, leaving the company insolvent on a balance sheet basis.

A crucial point is that this threshold is rising. In 2023, the company could withstand Bitcoin prices around $12,000; by 2024, this rose to $18,000, reaching $23,000 in 2025. As Strategy (MicroStrategy) expands its Bitcoin holdings, its critical threshold rises accordingly.

Thus, $23,000 represents the minimum Bitcoin price required for the company to maintain stable operations. This implies Bitcoin would need to fall about 73% from current levels before triggering bankruptcy risk.

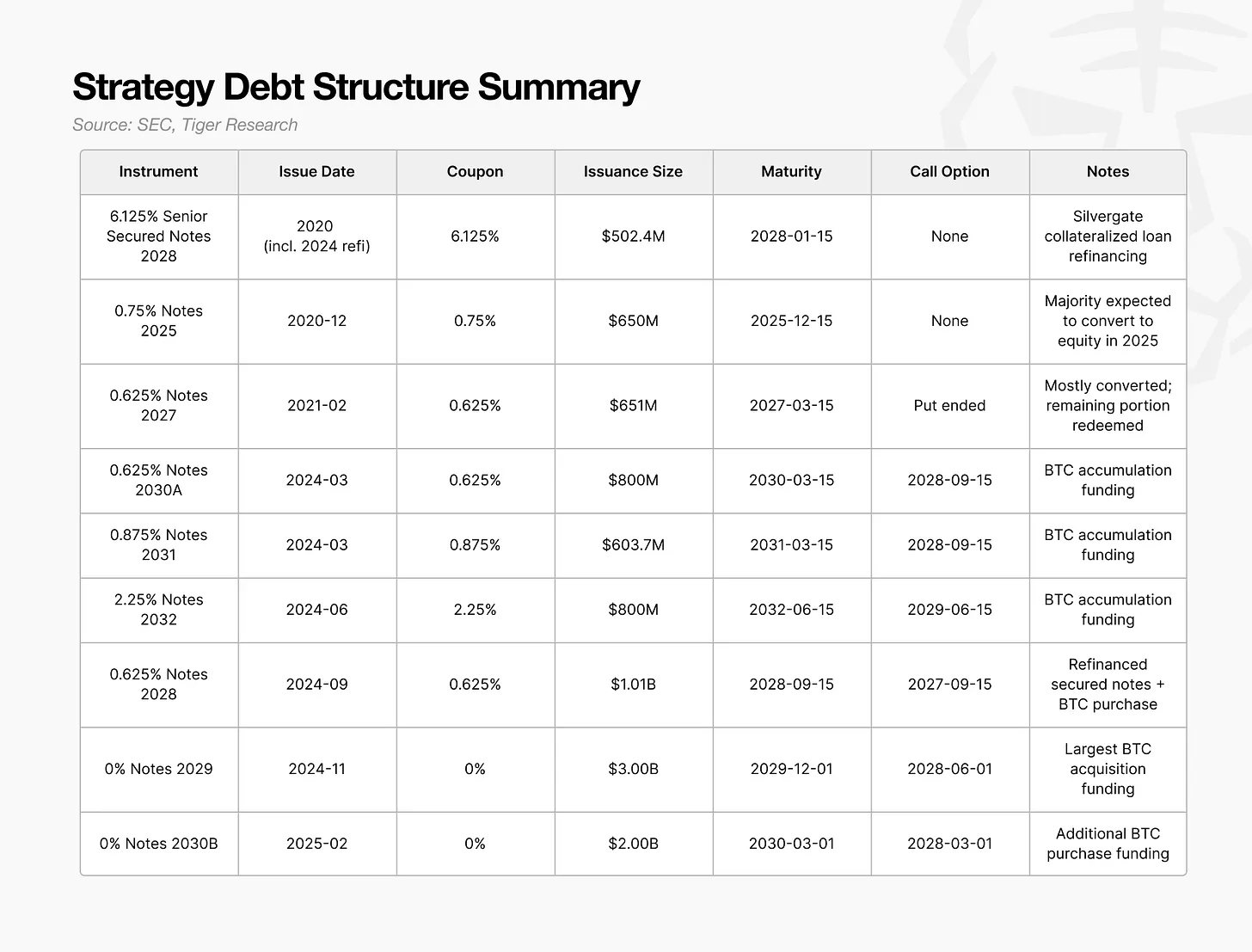

3. Convertible Bonds: The Issue Lies in Investor Put Rights, Not Maturity Dates

As previously mentioned, Strategy’s (MicroStrategy) static bankruptcy threshold has risen to $23,000 because its liabilities have grown faster than its Bitcoin holdings. The next question is how these debts were structured.

Between 2024 and 2025, Strategy (MicroStrategy) adopted a new capital-raising model combining convertible bonds, preferred shares, and an ATM stock program (At-The-Market Stock Program). Among these instruments, convertible bonds make up the largest portion and have the most significant market impact.

The key issue is not the size or maturity dates of the convertible bonds, but the timing of investor put rights

Holder put rights allow investors to demand early repayment, which the company cannot refuse. Most of the large convertible bonds issued between 2024 and 2025 have put dates concentrated in 2028, making 2028 a critical year for Strategy (MicroStrategy) to demonstrate refinancing capability.

If Bitcoin prices approach the bankruptcy threshold in 2028 or market conditions deteriorate, investors are likely to exercise their put rights rather than wait for maturity. A wave of such exercises would force Strategy (MicroStrategy) to raise billions of dollars in cash immediately.

The problem is that nearly all funds raised via these convertible bonds were used to buy Bitcoin. Had they been invested in productive assets generating cash flow, the company would have a natural source of repayment. But since funds were concentrated in Bitcoin accumulation, the company has little cash available for redemption.

Therefore, repayment funds would have to come from asset sales. If the put window opens during a period of low Bitcoin prices, Strategy (MicroStrategy) could face immediate liquidity shortages. Forced Bitcoin sales would further depress prices, push up the bankruptcy threshold, and potentially trigger a negative feedback loop.

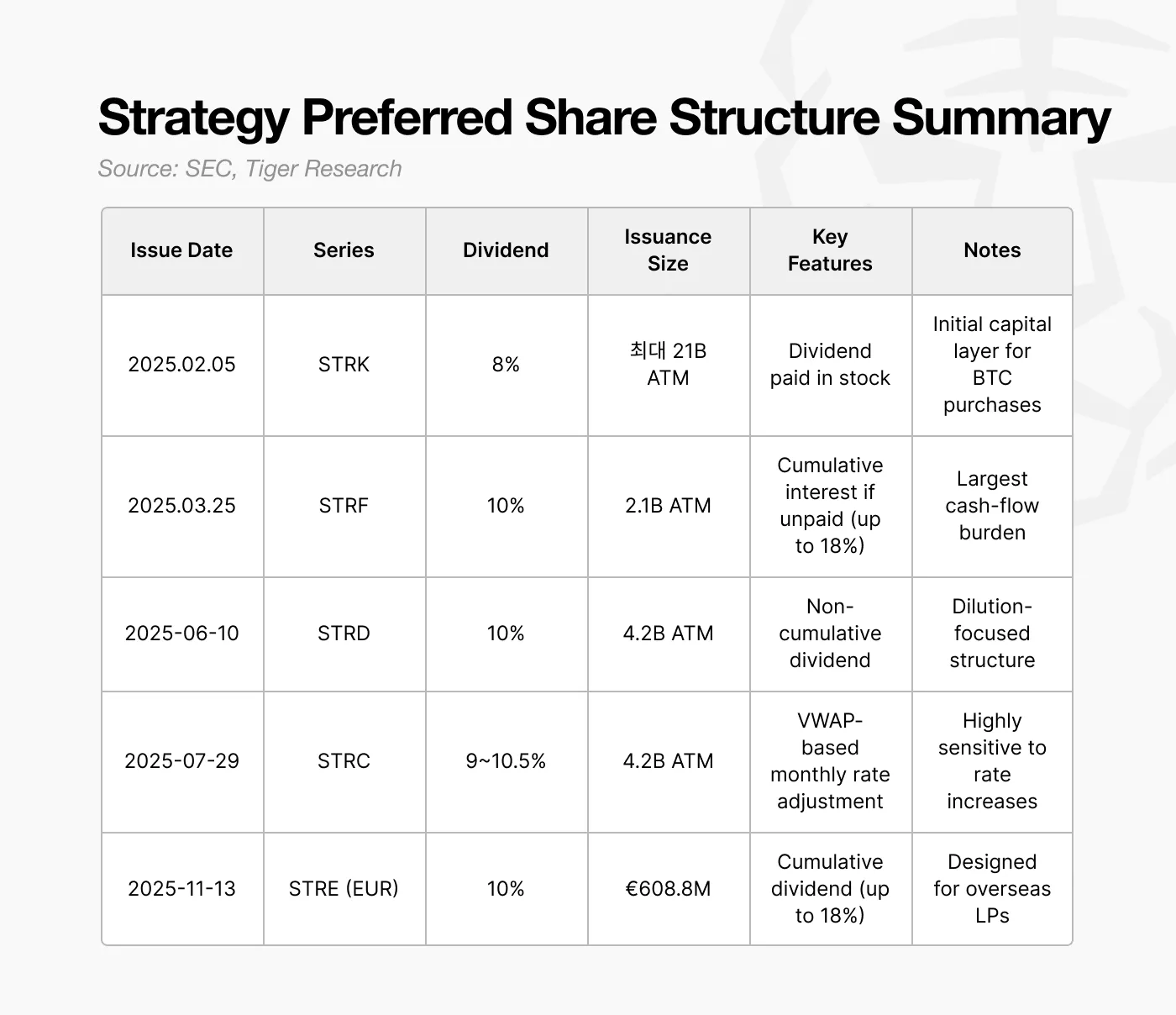

4. Preferred Shares: Why Accept a 10% Dividend Burden?

Starting in 2025, Strategy (MicroStrategy) stopped issuing near-zero coupon convertible bonds and instead began issuing preferred shares with dividend rates of about 10%. On the surface, this appears to be a more expensive option.

However, this decision reflects growing refinancing pressures expected between 2027 and 2028. The risk of concentrated investor put rights (Holder Put) in 2028 significantly increases mid-term repayment risks. During this period, any ongoing cash outflows could heighten bankruptcy risk.

A key feature of preferred shares is that dividends do not need to be paid in cash. Strategy (MicroStrategy) designed a flexible structure allowing dividend payments in stock when necessary. This enables the company to raise capital without immediately burning cash while fulfilling dividend obligations without cash disbursement. Effectively, preferred shares help Strategy avoid being forced to sell Bitcoin due to short-term cash shortages during the critical 2027–2028 period.

Although a 10% dividend rate seems costly, the ability to pay in stock makes it an effective tool for preserving liquidity and avoiding short-term cash crises.

Nonetheless, this structure introduces new challenges. Paying dividends in stock leads to continuous dilution for common shareholders. Strategy (MicroStrategy) already faces dilution risks from future conversion of convertible bonds, and preferred shares add further equity pressure.

Moreover, preferred shares carry priority claims. If the company faces simultaneous pressure from debt repayments and operating costs, preferred shareholders' claims must be satisfied before those of common shareholders. While preferred shares lack fixed maturity dates, their dividend obligations effectively act as structural fixed costs, influencing the company’s effective bankruptcy threshold.

By 2024–2025, Strategy (MicroStrategy) had transitioned from a model reliant on low-cost convertible bonds to a hybrid structure combining convertible bonds, preferred shares, and ATM issuance (At-The-Market Issuance). This shift drove rapid expansion of Bitcoin holdings in the short term.

5. What Happens If Strategy (MicroStrategy) Fails?

If Strategy (MicroStrategy) fails to refinance in 2028, its market impact can be estimated based on its repayment obligations.

The large convertible bonds issued between 2024 and 2025 will create a potential repayment demand of about $6.4 billion in 2028. If market conditions worsen, rendering financing channels like preferred share issuance, ATM issuance (At-The-Market Issuance), and new convertible bonds unavailable, the company would have no choice but to sell Bitcoin.

Assuming a Bitcoin price of $90,000, Strategy (MicroStrategy) would need to sell approximately 71,000 Bitcoins to meet these obligations. This scale of sale far exceeds typical institutional sell-offs.

Current spot market daily trading volume is around $20–30 billion. Selling 71,000 Bitcoins at $90,000 equals about $6.4 billion—20% to 30% of daily trading volume. Completing such a sale within a short timeframe would almost certainly exert significant downward price pressure.

Greater concern lies in the fact that such selling would not be a one-time event. As Bitcoin prices fall, the value of Strategy’s (MicroStrategy) assets declines immediately, weakening its financial ratios. This further limits fundraising ability and may force additional Bitcoin sales.

The end result could be a vicious cycle: failed refinancing leads to forced selling, declining Bitcoin prices further erode asset values, pushing the company toward more mandatory sales. Even if this dynamic lasts only a few quarters, it could deteriorate the balance sheet beyond recovery.

Therefore, Strategy’s (MicroStrategy) structural risk is concentrated in 2028. Outside this window, its leverage model appears manageable, but a failure to refinance in 2028 could trigger sell-off pressure strong enough to affect the entire Bitcoin market.

Hence, 2028 is not just a pivotal survival year for Strategy (MicroStrategy), but also a potentially significant volatility node for the broader Bitcoin ecosystem.

6. Strategy (MicroStrategy) Is Relatively Stable, But Late Entrants Face Higher Risks

The market often simplifies DAT company risk into one question: Can the company survive each Bitcoin downturn? However, this analysis shows that survivability does not depend on short-term price moves or stock volatility, but rather on the design of the company’s balance sheet and capital structure.

Therefore, evaluating DAT companies should not rely solely on stock prices or Bitcoin price drops. Key indicators include the position of their static bankruptcy threshold, timing of cash repayment pressures, and the financial instruments used to fill funding gaps. These factors provide insight into structural resilience, not short-term noise.

Of course, not all risks are predictable. ETF fund flows, macroeconomic conditions, and regulatory changes can alter the market environment at any time. Still, the most reliable assessment remains rooted in financial data reflecting bankruptcy thresholds and the company’s cash flow mechanisms.

In this regard, Strategy (MicroStrategy) holds a clear advantage. It entered the Bitcoin market in 2020, weathered the 2022 market slump, and accelerated asset accumulation through leveraged financing in 2024. Its combination of convertible bonds and preferred shares creates multi-layered buffers.

Thus, Strategy (MicroStrategy) has a relatively stable foundation. In contrast, newer entrants have yet to establish proven DAT frameworks, making their ability to withstand major price declines highly uncertain.

This report aims to provide a foundation for assessing DAT companies using quantifiable signals rather than fear or optimism, highlighting the structural risks that truly matter.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News