Why HYPE is not a good investment option now?

TechFlow Selected TechFlow Selected

Why HYPE is not a good investment option now?

Repurchase has been the primary mechanism supporting the HYPE price; however, future token unlocks should not be overlooked.

Author: Dave

Summary

HYPE has implemented a strong buyback mechanism (approximately $1.3 billion to date, accounting for about 46% of all token buybacks in 2025) and is backed by solid revenue. I believe nearly every researcher is bullish on this token, but today I'll offer a contrarian view: several structural and macro factors make HYPE a less "sweet" trade.

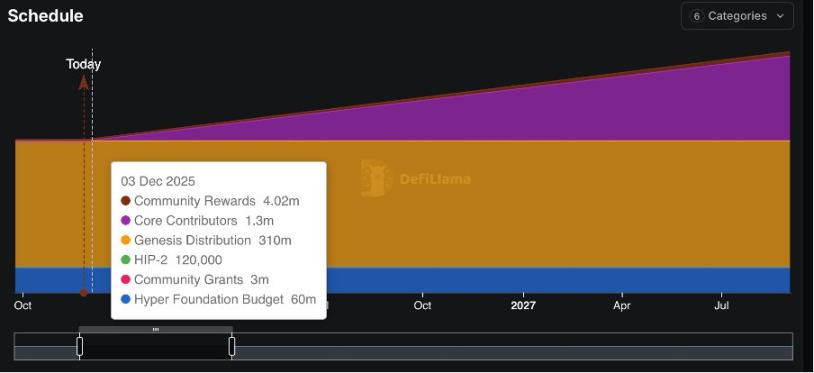

1. Buybacks vs. Token Unlocks

Buybacks have been the primary mechanism supporting HYPE’s price, a point often highlighted by many KOLs. However, future token unlocks cannot be overlooked.

Starting from November 29, 2025, 373 million HYPE tokens (approximately 37% of total supply) will be unlocked, averaging around 215,000 HYPE per day over a 24-month period. At current prices, this represents a potential monthly supply pressure of approximately $200 million.

In comparison, the total buyback amount for 2025 is $644.64 million, averaging about $65.5 million per month, funded by 97% of trading fees. Daily buybacks can only cover 25–30% of the daily unlock volume. Even with continued strong revenue growth, the buyback capacity will struggle to absorb such a large-scale unlock, inevitably leading to price compression.

2. Market Cycle Risk & Valuation Vulnerability

Currently, almost all valuations of HYPE (including the widely cited P/E ratio, which actually uses a trailing twelve months model) are based on strong data from the past few months during a bull market. But as someone who lived through the 2022 bear market, I believe macro cycle factors must be included as key variables. In the foreseeable future, the probability of a bear market is no lower than that of a bull market—core assumptions and metrics are under challenge.

2.1 Current Snapshot

The current revenue metrics indeed appear very strong:

-

· Annualized revenue: $1.2 billion

-

· Fully diluted valuation (FDV): $31.6 billion

-

· Circulating supply: $20 billion (source: Defillama)

-

· Trailing P/E ratio ≈ 16.67

· Monthly compound revenue growth from December 2024 to August 2025: +11.8%

These figures may seem attractive compared to most U.S. equities, but therein lies the problem—HYPE could face a more severe case of the "double whammy" effect during an upcoming bear market than other projects.

2.2 Bear Market Scenario and the Double Whammy Effect

Backtesting shows that the correlation coefficient between perpetual contract trading volume and BTC price exceeds 0.8 (across cycles).

-

· 2022 Bear Market: Perpetual contract trading volume dropped 70% from its 2021 peak.

-

· Revenue dependency: 91% comes from trading fees, making it highly vulnerable to volume shocks.

-

· Withdrawal delays: HLP treasury requires a 4-day lockup; withdrawals from centralized exchanges take 24–48 hours.

This is a classic double whammy setup: falling crypto asset prices → reduced trading volume & fees, coupled with shrinking valuation multiples → creating a vicious cycle.

The valuation of $HYPE is largely based on performance during the past year's bull market. Yet in Web3, revenue is highly cyclical. We should adjust our fundamental assumptions accordingly.

Unlike U.S. equities, where the S&P has shown near-smooth growth since 2008 when viewed long-term, cryptocurrency markets still exhibit boom-and-bust cycle characteristics. While macro market factors are indeed hard to quantify, the ability to navigate these cycles is precisely what distinguishes good traders from top-tier ones in the space.

2.3 Native Crypto Metrics

We know that even in traditional finance, P/E is not the only metric—others include EV/EBITDA, P/FCF, ROIC. For HYPE, additional important metrics should also be considered:

-

TVL: $4.3 billion, but showing a clear downtrend from its peak of $6.1 billion in September 2025.

-

P/TVL: 2.0 (Solana: 1.5).

Market share: Has declined from a peak of 80% to 70%, credit to dark horse Aster. And there are others like lighter edgex, etc.

3. Is Dave Just FUD-ing HYPE? Not Exactly

Although I currently do not support investing in HYPE, my bearish stance applies only from a medium-term perspective. If we look at a 2–5 year long-term investment horizon, HYPE is absolutely worth investing in. That needs no further explanation.

A complete investment decision depends on multiple factors, including position sizing, risk tolerance, and investment objectives, among others.

All projects face pressure during bear markets—what’s the way out?

Prediction markets may currently offer higher cost-effectiveness. Research from @a16z indicates that prediction markets have a correlation of only 0.2–0.4 with the broader market, compared to >0.8 for $HYPE.

Moreover, 2026 will feature multiple high-attention events such as the World Cup (likely the last for aging stars like Messi and Ronaldo), the U.S. midterm elections, the Winter Olympics, the League of Legends World Championship, and numerous game, film, and anime releases like GTA6. A gambling boom is foreseeable, with substantial off-chain capital likely flowing into this sector—potentially even impacting the Nasdaq. Therefore, if riding the mid-term trend, prediction market projects deserve attention.

Conclusion:

From a medium-term perspective, the risks posed by large-scale unlocks, revenue cyclicality, and shifts in the macro environment outweigh the returns implied by current valuations. This article does not constitute any investment advice. All investments carry risk. NFA, DYOR.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News