Speculative coins are dead, equity coins should rise

TechFlow Selected TechFlow Selected

Speculative coins are dead, equity coins should rise

In a world where tokens cannot rely on a constant stream of buyers driven by speculation, they must stand on their own intrinsic value.

Author: Patrick Scott | Dynamo DeFi

Translation: TechFlow

The reckoning day for the crypto industry has finally arrived.

Over the past five years, tokens have enjoyed what I politely call “speculative demand far exceeding fundamentals.” Less politely, they've been severely overvalued.

The reason is simple: there aren’t many liquid assets in crypto with solid fundamentals. As a result, investors gain exposure through whatever assets they can access—typically Bitcoin or altcoins. Add to that retail investors inspired by stories of “Bitcoin millionaires,” hoping to replicate those returns by investing in newer, smaller tokens.

This led to demand for altcoins vastly exceeding the supply of those with real, solid fundamentals.

First-order effect

When market sentiment hits rock bottom, you can buy almost any asset and achieve remarkable returns years later.

Second-order effect

Most business models in the industry (if you can even call them that) revolve around selling their own tokens, rather than relying on actual revenue streams tied to their products.

In the past two years, the altcoin market has experienced three events with disastrous consequences:

-

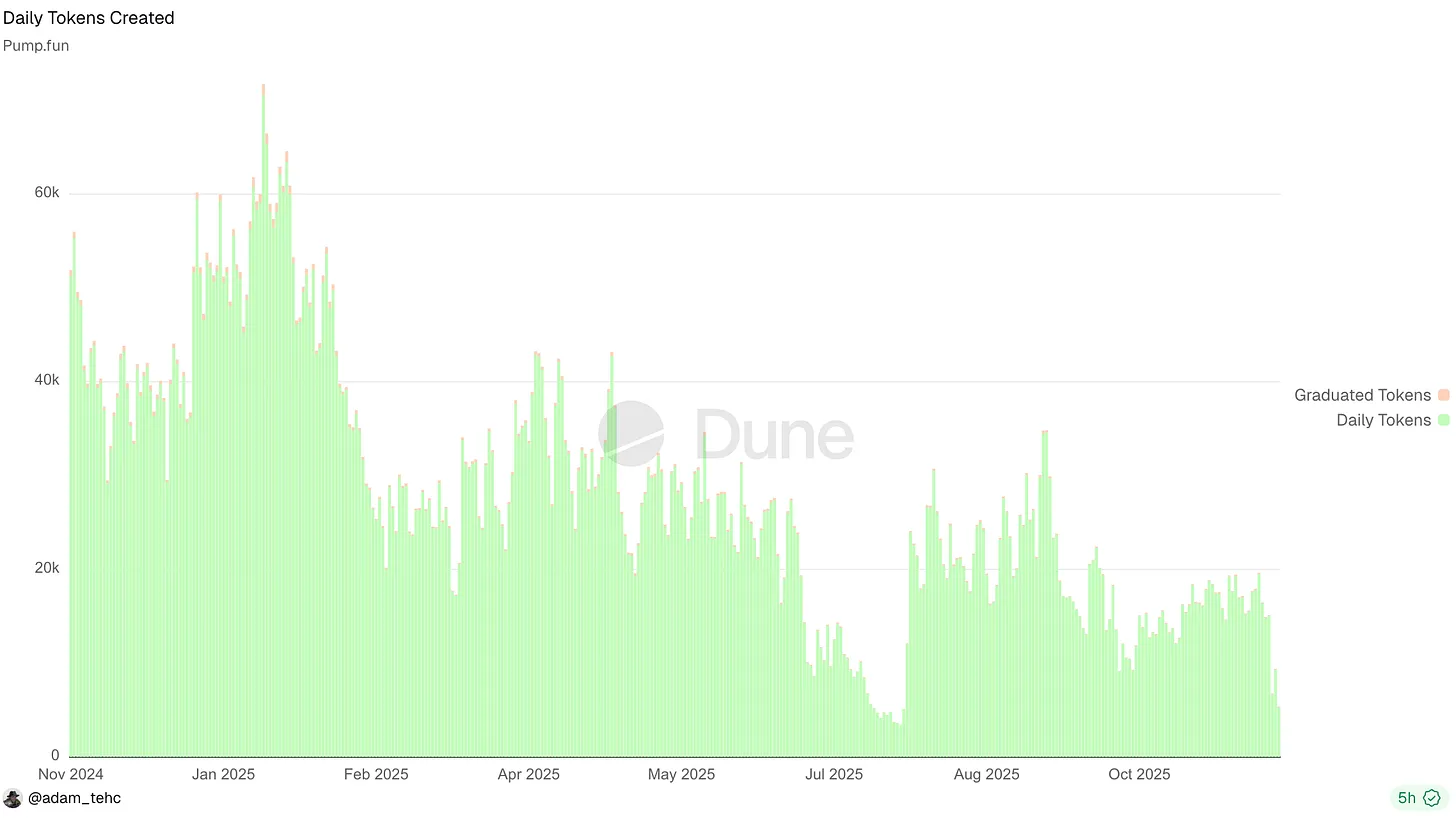

The rise of "Pump fun" and other token launch platforms

These platforms have "commoditized" new token launches—making them overly common—diverting attention across millions of assets. This fragmentation has prevented the top few thousand tokens from continuing to attract concentrated capital inflows and disrupted the wealth effect typically driven by Bitcoin halvings.

-

On many days earlier this year, Pump platforms launched over 50,000 tokens per day.

-

Some crypto assets are beginning to develop real fundamentals

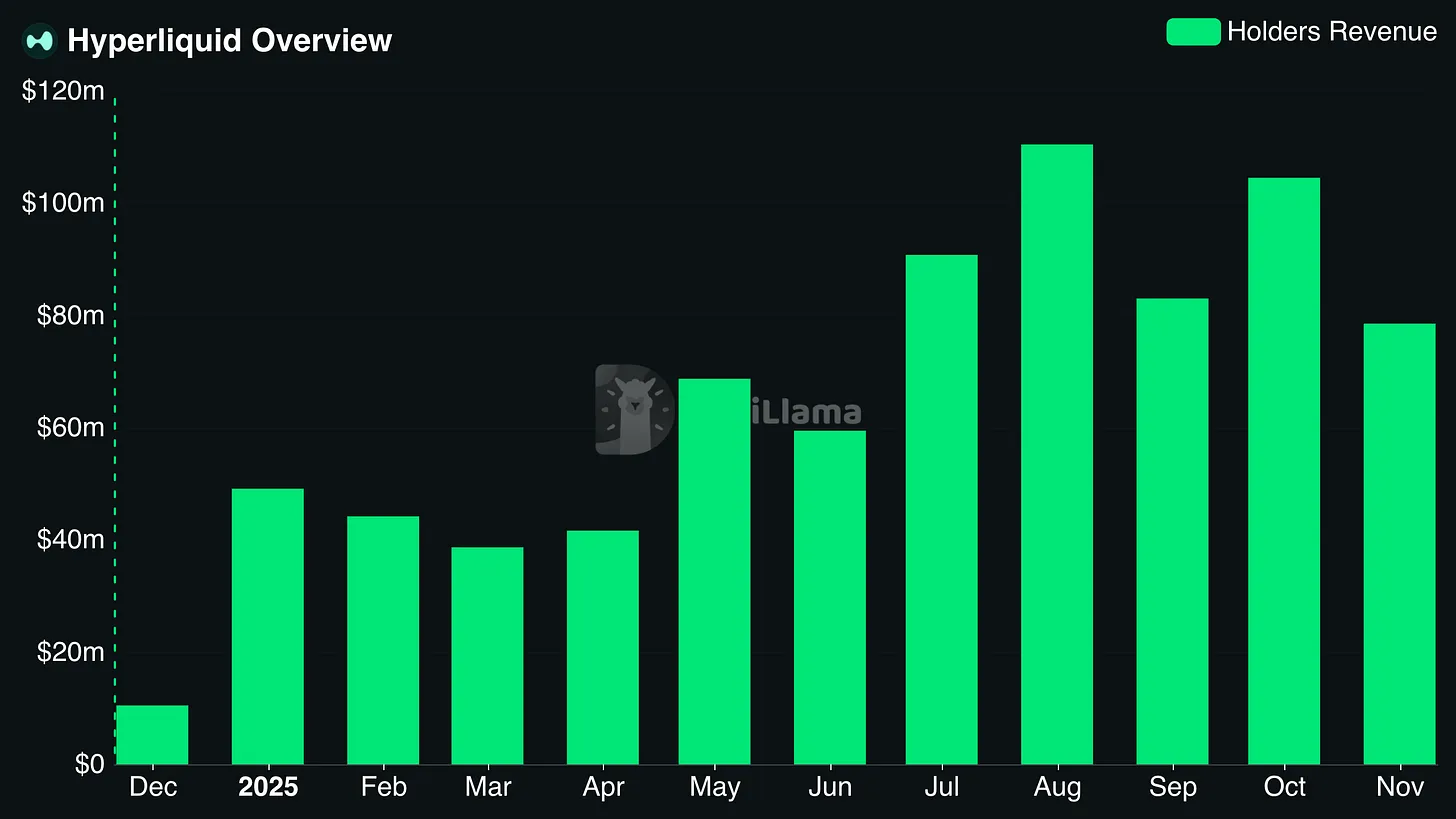

Certain tokens (like HYPE) and new IPO projects (like CRCL) are starting to show genuine fundamentals. Once assets backed by fundamentals emerge in the market, it becomes difficult to justify betting on tokens supported only by whitepapers.

Monthly revenue for Hyperliquid holders often exceeds $100 million

-

Meanwhile, tech stocks have outperformed the crypto market. In many cases, equities related to artificial intelligence, robotics, biotechnology, and quantum computing have delivered better returns than crypto. This leaves retail investors wondering: why take risks on altcoins when “real” companies offer higher returns and appear less risky? Even the NASDAQ has outperformed both Bitcoin and altcoins this year.

What’s the result?

-

Poor-performing altcoins have become a graveyard;

-

Teams are fiercely competing for increasingly scarce capital;

-

Even seasoned crypto investors are now directionless, flailing around like headless chickens.

Ultimately, tokens either represent an equity stake in a business or they are worthless. They aren't some magical new thing whose mere existence grants value.

If you stop viewing tokens as incomprehensible entities and instead treat them as assets representing future cash flows from businesses, everything becomes clearer.

You might object: “Dynamo, some tokens don’t grant rights to future cash flows! Some are utility tokens! Some protocols have both tokens and equity!” But you’re wrong. These tokens still represent future cash flows; it's just that the cash flows they're tied to happen to be $0.

In the end, tokens either provide an equity stake in a business or they are worthless. They do not automatically gain value simply by “existing” or having a “community” (as many believe).

Note: This view does not apply to network coins like Bitcoin (BTC), which are more akin to commodities; we're discussing protocol tokens here.

In the near future, the only DeFi tokens with real value will be those that function as pseudo-equity and meet two conditions:

-

Claim on protocol revenue;

-

The protocol generates sufficient revenue to make it an attractive value proposition.

Retail Investors Break Up With Crypto

Retail investors have temporarily walked away from the crypto market.

Some top KOLs shout “crime is legal,” yet express surprise when people don’t want to become victims of that “crime.”

For now, retail has lost interest in the vast majority of tokens.

Besides previously mentioned reasons, another key factor is: People are tired of losing money.

-

Overblown promises: The value of many tokens is built on commitments that cannot be fulfilled.

-

Token supply glut: Due to the rise of memecoin launch platforms, the market is flooded with an oversupply of tokens.

-

Predatory tokenomics: The industry’s tolerance for valueless tokens leads retail investors to rightly believe they are destined to be the “bagholders.”

Result? Those who would have bought crypto assets are now turning to other outlets for their “gambling urge,” such as sports betting, prediction markets, and stock options. These alternatives aren’t necessarily wise, but buying most altcoins isn’t a great idea either.

But can we really blame them?

Some KOLs talk about “crime being legal” while expressing shock that people don’t want to be victims.

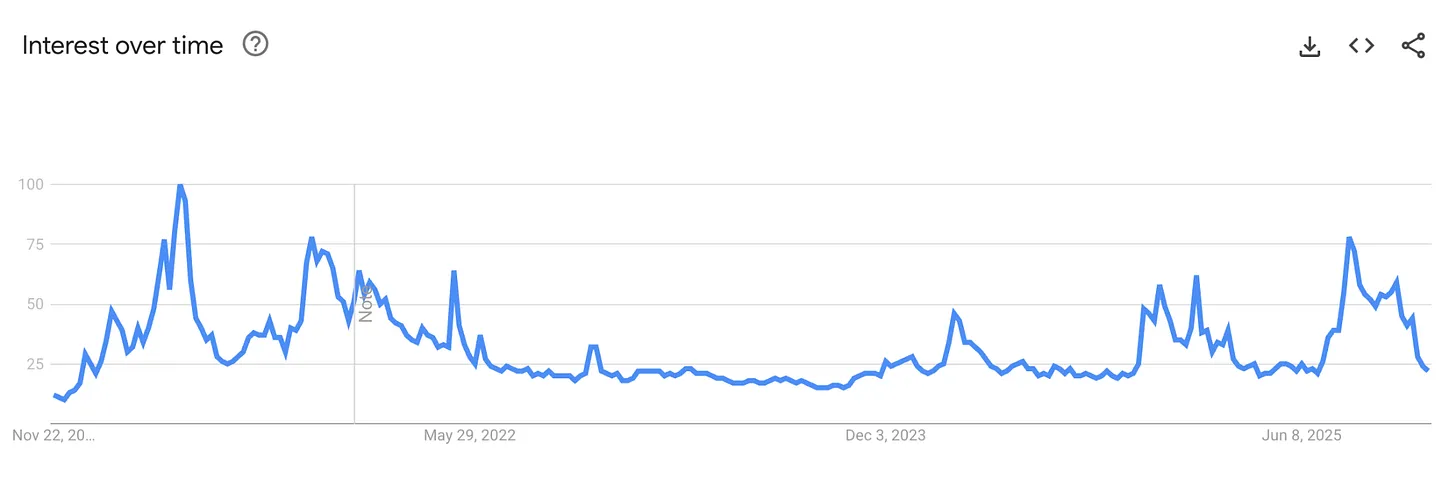

This public apathy toward crypto is also reflected in waning industry interest. Enthusiasm this year is nowhere near the 2021 peak, despite current fundamentals being stronger and regulatory risks lower than ever before.

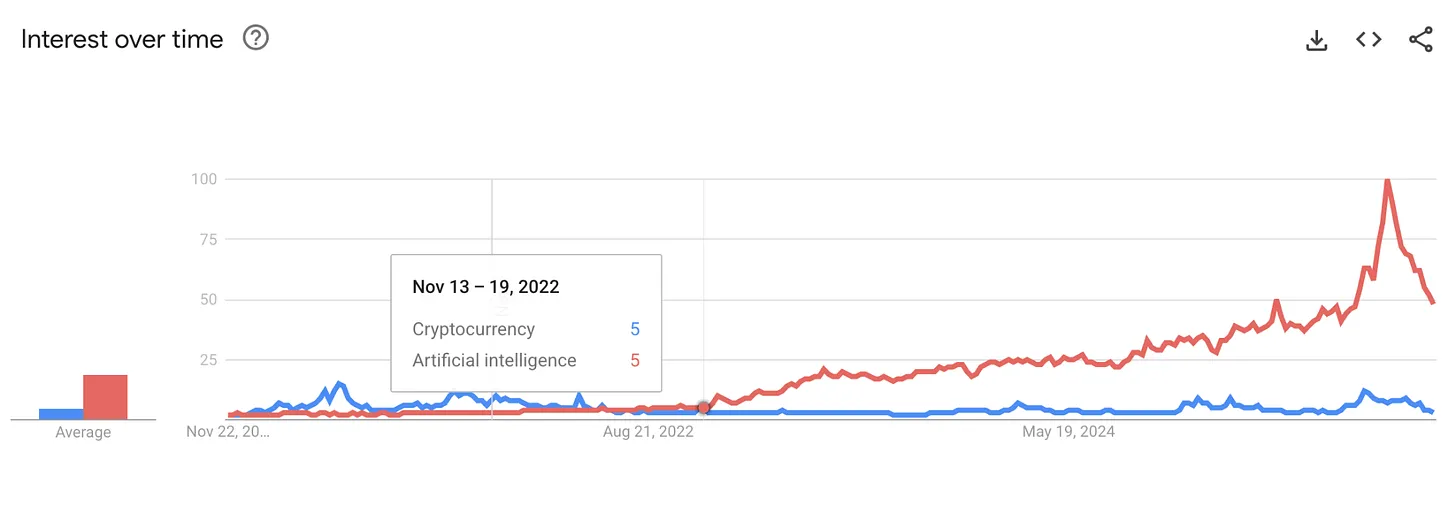

I also believe that ChatGPT and the ensuing AI boom have dampened enthusiasm for cryptocurrency, as they’ve shown a new generation what a true “killer app” looks like.

For the past decade, crypto enthusiasts have claimed the industry is experiencing a new “Dot-Com Moment.” But when people see AI reshaping their world in tangible, visible ways every day, that argument becomes harder to accept.

The gap between crypto and AI in search engine interest is clear. The last time crypto surpassed AI in Google search interest was during the FTX collapse:

Will retail return to crypto?

Answer: Yes.

Retail has arguably already returned to a form of prediction market—but they’re buying binary options on questions like “when will the government shutdown end,” not altcoins. To bring them back en masse into altcoin investing, they need to feel they have a reasonable chance of profiting.

Core Source of Token Value: Protocol Revenue

In a world where tokens can no longer rely on an endless stream of speculative buyers, they must stand on their intrinsic value.

After five years of experimentation, the painful truth has emerged: the only meaningful form of token value accumulation is claim on protocol revenue (past, present, or future).

All forms of genuine value accumulation ultimately boil down to claims on protocol revenue or assets:

-

Dividends

-

Buybacks

-

Fee Burns

-

Treasury Control

This doesn’t mean a protocol must execute these mechanisms today to have value. In the past, I was criticized for saying I preferred protocols I followed to reinvest revenue rather than conduct buybacks. But protocols must have the ability to activate these value accumulation mechanisms in the future, ideally through governance votes or clear triggering criteria. Vague promises are no longer enough.

Luckily, for savvy investors, this fundamental data is now easily accessible on platforms like DefiLlama, covering thousands of protocols.

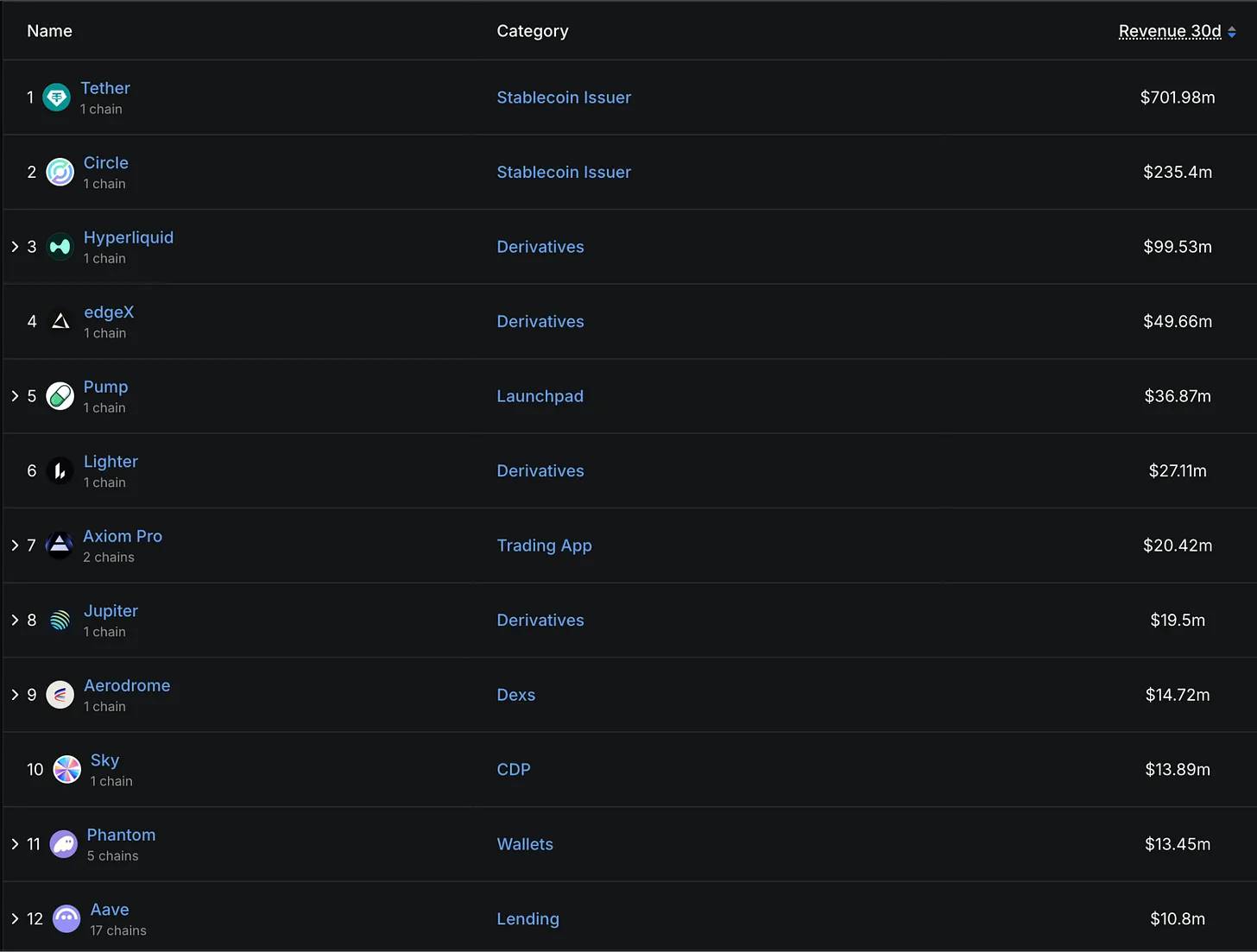

A quick look at the top protocols by revenue over the past 30 days reveals a clear pattern: stablecoin issuers and derivatives platforms dominate, with notable presence from launchpads, trading apps, CDPs (collateralized debt positions), wallets, decentralized exchanges (DEXs), and lending protocols.

Key observations:

-

Stablecoins and perpetual contracts are currently the two most profitable businesses in crypto

-

Trading-related businesses remain highly profitable

-

Overall, trading-supporting businesses are highly lucrative. However, if the market enters a prolonged bear phase, trading-related revenues could face significant risk unless protocols pivot to trading real-world assets (RWAs), as Hyperliquid is attempting.

-

-

Controlling distribution channels is as important as building core protocols

-

I suspect some hardcore DeFi users may strongly oppose trading apps or wallets becoming top revenue generators, arguing users can directly use protocols to save costs. Yet in reality, apps like Axiom and Phantom are extremely profitable.

-

Some crypto applications generate tens of millions of dollars in monthly revenue. If your favorite protocol hasn’t reached that level yet, that’s okay. As someone responsible for DefiLlama’s revenue tracking, I know it takes time to build a product the market is willing to pay for. But the key is, there must be a clear path to profitability.

The era of playing around is over.

Toward a Value-Oriented Crypto World: An Investment Framework

Looking ahead to the next few years, high-performing tokens must meet these criteria:

-

Claim on protocol revenue or a clear, transparent path to such a claim

-

Stable and consistently growing revenue and earnings

-

Market cap at a reasonable multiple relative to past revenue

Rather than theorizing, let’s examine concrete examples:

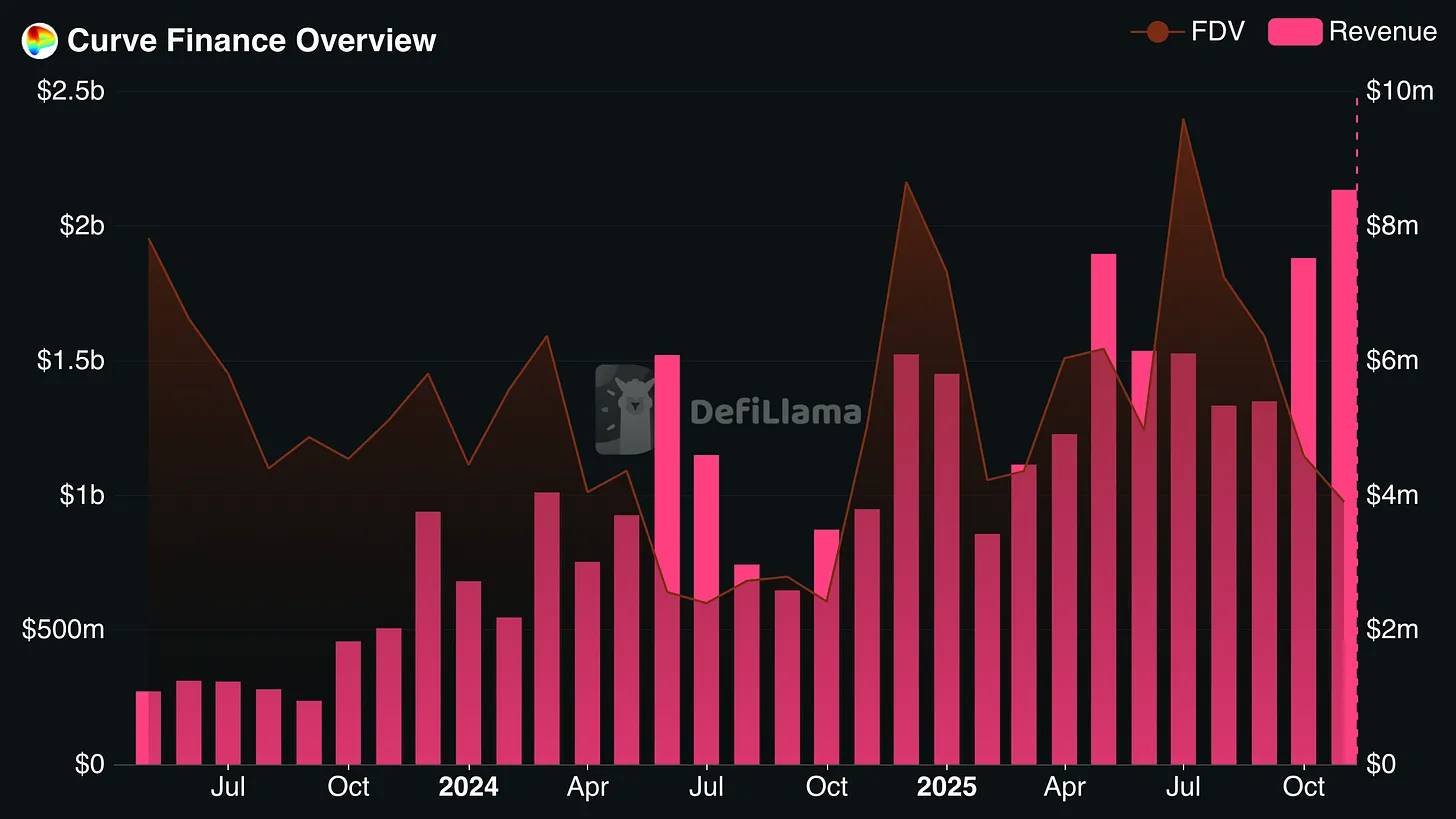

Curve Finance

Curve Finance has achieved stable and consistent revenue growth over the past three years, even as its fully diluted valuation (FDV) declined. Ultimately, its FDV has dropped to less than 8x its annualized revenue over the past month.

Given that stakers of Curve tokens receive bribe rewards and the token release schedule is long, the actual yield for token holders is significantly higher. The key question going forward is whether Curve can maintain its revenue levels in the coming months.

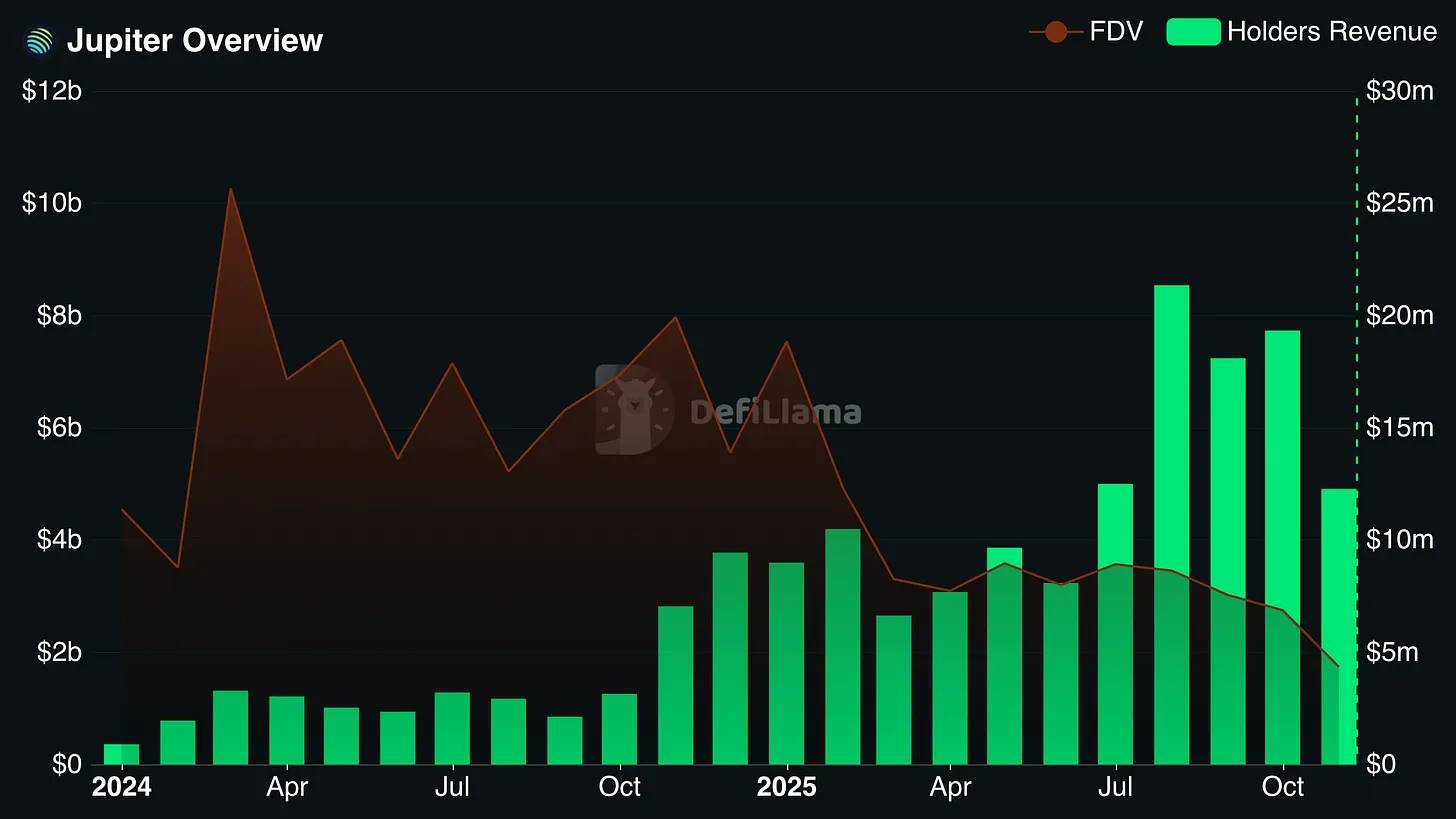

Jupiter

Jupiter has firmly established itself as one of the primary beneficiaries of Solana’s ecosystem growth. It is the most widely used DEX aggregator and perpetual contract decentralized exchange (perp DEX) on the Solana chain.

Additionally, Jupiter has made several strategic acquisitions, enabling it to leverage its distribution channels to expand into markets on other chains.

Notably, the annualized revenue distributed to Jupiter token holders is substantial, amounting to roughly 25% of its circulating market cap and exceeding 10% of its FDV (fully diluted valuation).

Other protocols meeting the criteria: Hyperliquid, Sky, Aerodrome, and Pendle

Positive Signals: Glimmers of Hope

The good news is that teams genuinely concerned about survival are rapidly recognizing this reality. I expect that in the coming years, pressure from the inability to endlessly sell tokens will drive more DeFi projects to develop real revenue streams and tie their tokens to those cash flows.

If you know where to look, the future is full of promise.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News