IOSG: The era of application cycles has arrived, and Asian developers are entering their golden age

TechFlow Selected TechFlow Selected

IOSG: The era of application cycles has arrived, and Asian developers are entering their golden age

Trading, asset issuance, and financial applications still have the best PMF and are almost the only products capable of surviving both bull and bear markets.

Author: Jiawei, IOSG

In the mid-to-late 1990s, internet investment focused heavily on infrastructure. At that time, capital markets almost entirely bet on fiber-optic networks, ISPs, CDNs, and manufacturers of servers and routers. Cisco's stock price soared, surpassing a market cap of $500 billion by 2000, making it one of the most valuable companies globally; fiber equipment makers like Nortel Networks and Lucent also became hot favorites, attracting hundreds of billions in funding.

Amid this boom, the U.S. added millions of kilometers of new fiber-optic cables between 1996 and 2001—far exceeding actual demand at the time. The result was severe overcapacity around 2000: transcontinental bandwidth prices dropped more than 90% within just a few years, and the marginal cost of internet access nearly approached zero.

Although this infrastructure wave allowed later-born giants like Google and Facebook to grow on cheap, ubiquitous networks, it brought significant pain for investors at the time: infrastructure valuations collapsed rapidly, with star companies like Cisco losing over 70% of their market value within a few years.

Does this sound familiar to the past two years in Crypto?

1. Is the Infrastructure Era Temporarily Over?

Block Space Transitions from Scarcity to Abundance

Scaling block space and exploring blockchain’s “impossible trinity” have largely defined the early development themes of the crypto industry for several years, making it a fitting symbolic element to discuss.

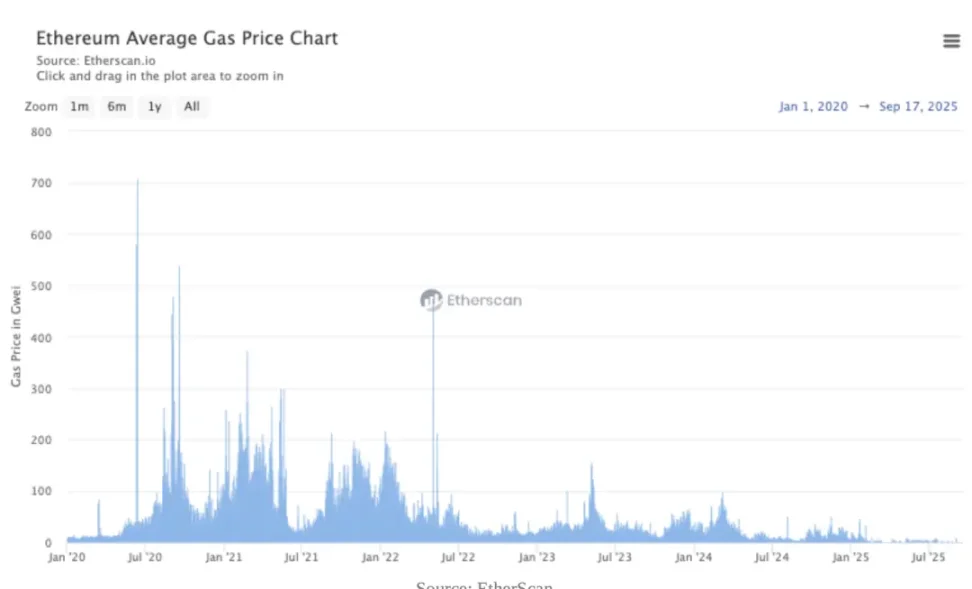

▲Source: EtherScan

In the early days, public chains had extremely limited throughput, making block space a scarce resource. Take Ethereum as an example: during the DeFi Summer, when various on-chain activities overlapped, transaction costs for DEX interactions often ranged between $20–50, reaching hundreds of dollars during peak congestion. During the NFT era, demand and calls for scaling reached their peak.

Ethereum’s composability is one of its major strengths, but overall it increased the complexity and gas consumption per call, causing high-value transactions to dominate the limited block capacity. As investors, we often discussed L1 fees and burn mechanisms, using them as anchors for L1 valuation. During this period, the market assigned high valuations to infrastructure, embracing the so-called "fat protocol, thin application" thesis—that infrastructure captures most of the value—sparking a construction boom, even a bubble, in scaling solutions.

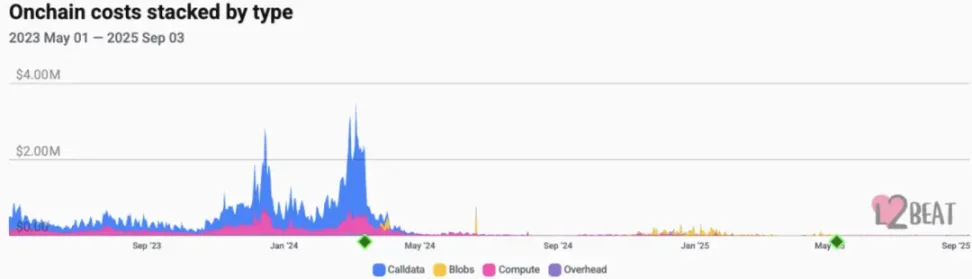

▲Source: L2Beats

In outcome, key Ethereum upgrades (e.g., EIP-4844) migrated L2 data availability from expensive calldata to lower-cost blobs, significantly reducing unit costs for L2s. Transaction fees on mainstream L2s generally dropped to the few-cents level. Modular architectures and Rollup-as-a-Service offerings further reduced the marginal cost of block space. Alt-L1s supporting various virtual machines also emerged. As a result, block space evolved from a single scarce asset into a highly interchangeable commodity.

The chart above shows the evolution of chain costs across various L2s over the past few years. We can see that from 2023 to early 2024, calldata dominated costs, with daily expenses even nearing $4 million. Then, in mid-2024, the introduction of EIP-4844 gradually replaced calldata with blobs as the main cost driver, significantly lowering overall on-chain costs. By 2025, total expenses stabilized at a low level.

With this shift, more applications can now directly place core logic on-chain, rather than relying on complex off-chain processing followed by on-chain verification.

From this point onward, value capture begins shifting from underlying infrastructure toward applications and distribution layers that directly handle traffic, improve conversion, and form closed-loop cash flows.

Revenue-Level Evolution

Building on the previous section, we can intuitively validate this view at the revenue level. In cycles dominated by infrastructure narratives, market valuations of L1/L2 protocols were primarily based on expectations of technical capability, ecosystem potential, and network effects—what we call the "protocol premium." Token value capture models were often indirect (e.g., through network staking, governance rights, or vague fee expectations).

Application-level value capture is far more direct: generating verifiable on-chain revenue through fees, subscriptions, or service charges. These revenues can be directly used for token buybacks, burns, dividends, or reinvestment into growth, forming a tight feedback loop. Application revenue sources become solid—increasingly derived from actual service fees rather than token incentives or market narratives.

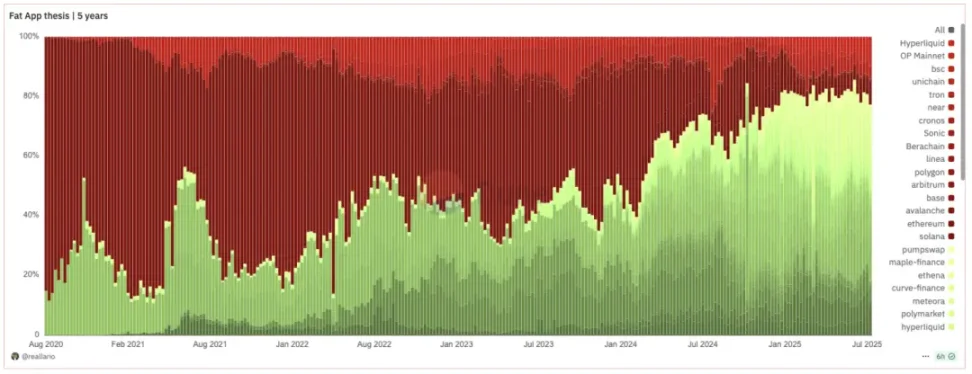

▲Source: Dune@reallario

The chart above roughly compares protocol (red) and application (green) revenues from 2020 to present. We can see application-captured value gradually rising, reaching about 80% this year. The table below lists the 30-day protocol revenue rankings from TokenTerminal, where L1/L2s account for only 20% among the top 20 projects. Notably dominant are applications such as stablecoins, DeFi, wallets, and trading tools.

▲Source: ASXN

Additionally, due to market reactions to buybacks, the correlation between application token prices and revenue data is gradually strengthening.

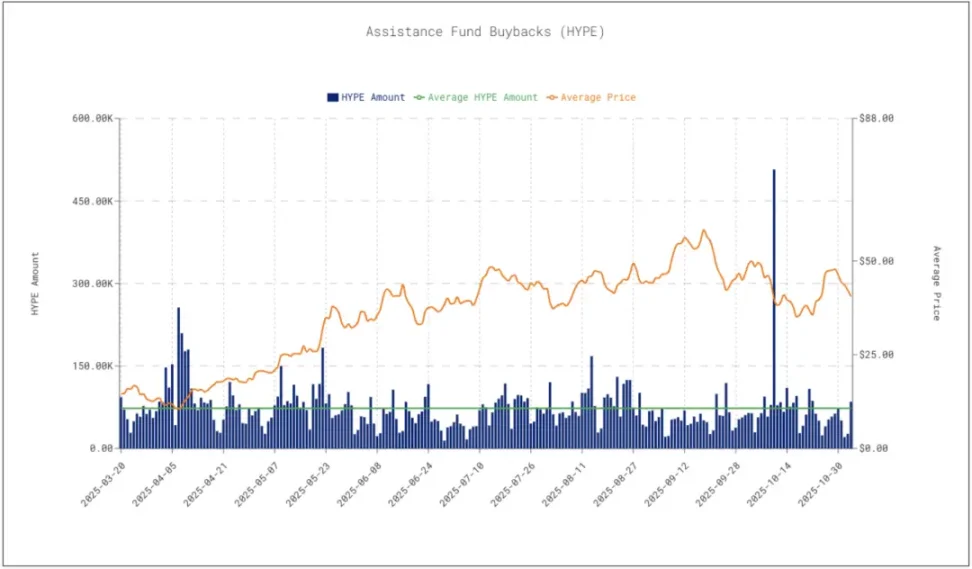

Hyperliquid repurchases around $4 million worth of tokens daily, providing clear price support. Buybacks are seen as one of the key drivers behind price rebounds, indicating that the market now directly links protocol revenue and buyback actions to token value—not just sentiment or narrative. The author expects this trend to intensify further.

2. Embracing the New Cycle Dominated by Applications

The Golden Age for Asian Developers

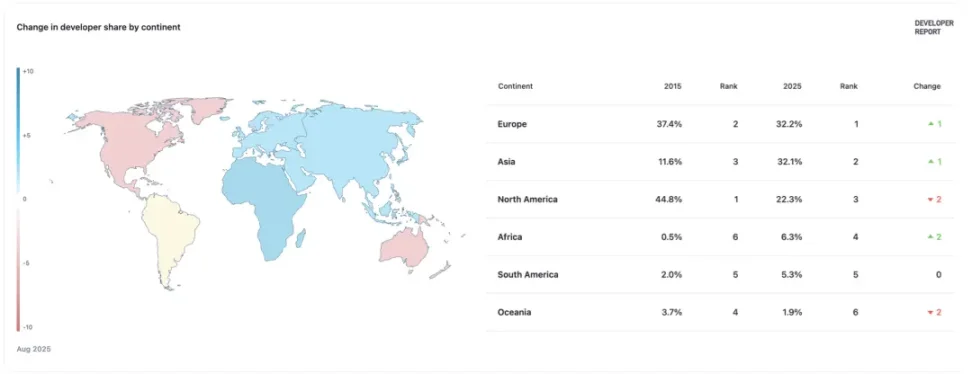

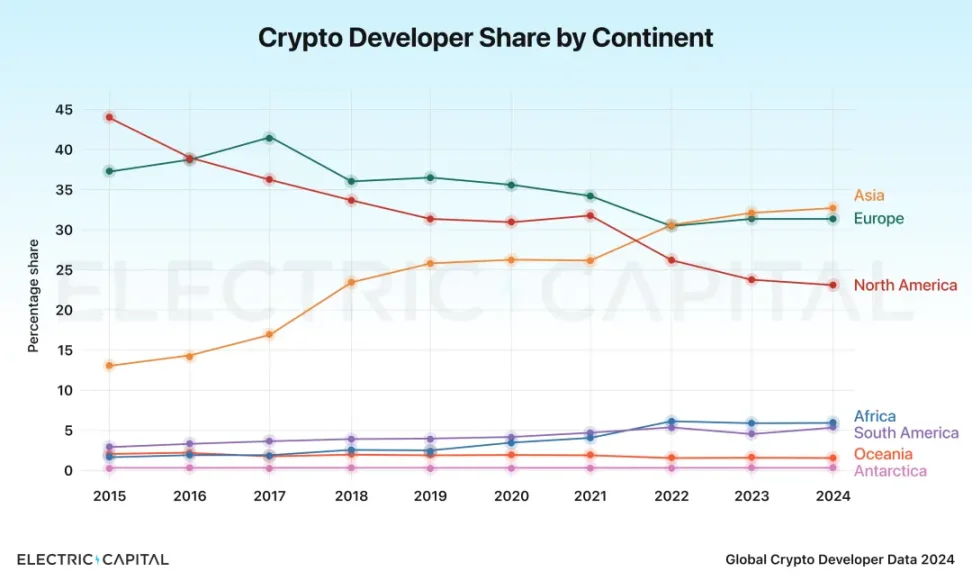

▲Source: Electric Capital

▲Source: Electric Capital

Electric Capital’s 2024 Developer Report shows that blockchain developers from Asia accounted for 32% of the global total—the first time surpassing North America and becoming the world’s largest developer hub.

Over the past decade, global products like TikTok, Temu, and DeepSeek have demonstrated Chinese teams’ exceptional capabilities in engineering, product design, growth, and operations. Asian teams, especially Chinese ones, possess an extremely fast iteration pace, rapid demand validation, and strong execution through localization and growth strategies for international expansion. These traits align perfectly with crypto: requiring swift adaptation to market shifts, serving global users, cross-language communities, and multi-jurisdictional regulations simultaneously.

Therefore, Asian developers—particularly Chinese teams—enjoy structural advantages in the crypto application cycle: strong engineering skills combined with sensitivity to market speculation cycles and exceptional execution speed.

Given this context, Asian developers have natural advantages in delivering globally competitive crypto applications faster. Projects like Rabby Wallet, gmgn.ai, and Pendle exemplify Asian teams’ growing presence on the global stage.

We expect a swift shift in market dynamics: from previously U.S.-led narratives to a new path where Asian teams lead with product deployment, then expand outward into Western markets. Under the application cycle, Asian teams and markets will gain greater influence.

Early-Stage Investing in the Application Cycle

Here are some perspectives on early-stage investing:

Trading, asset issuance, and financialized applications still achieve the best product-market fit and are almost the only types capable of surviving both bull and bear markets. Examples include perpetual platforms like Hyperliquid, launchpads like Pump.fun, and products like Ethena, which packages funding rate arbitrage into something broader user bases can understand and use.

If uncertainty is high within a niche sector, consider investing in the sector’s beta—identifying which projects benefit from its overall growth. A classic example is prediction markets: there are about 97 public prediction market projects, with Polymarket and Kalshi emerging as clear winners. The odds of a long-tail project overtaking them are slim. Instead, investing in tooling projects—such as aggregators or position analytics tools—for these markets offers higher certainty, allowing investors to ride the sector’s growth wave. This turns a difficult multiple-choice question into a much simpler single-choice one.

Once a product exists, the next challenge is driving mass adoption. Beyond common entry points like Social Login provided by Privy, the author believes aggregated trading frontends and mobile apps are equally important. In an application-driven cycle, whether for perpetuals or prediction markets, mobile becomes the most natural user touchpoint—whether for a user’s first deposit or daily high-frequency actions, the mobile experience is smoother.

The value of aggregated frontends lies in traffic distribution. Distribution channels directly determine user conversion efficiency and project cash flow.

Wallets are also a crucial part of this logic.

The author believes wallets are no longer just asset management tools—they increasingly resemble Web2 browsers. Wallets directly capture order flow, routing it to block builders and searchers to monetize traffic. At the same time, they act as distribution channels, integrating cross-chain bridges, built-in DEXs, staking access, and other third-party services, becoming direct gateways for users to reach other applications. In this sense, wallets control order flow and traffic distribution, serving as the primary entry point for user relationships.

For infrastructure in this cycle, the author believes purpose-built standalone blockchains have lost relevance, while infrastructure built to support applications can still capture value. Specific examples include:

-

Infrastructure enabling customized multi-chain deployment and app-specific chain creation, such as VOID;

-

Companies offering user onboarding (covering login, wallet, deposits/withdrawals, fiat on/off ramps), such as Privy, Fun.xyz; this also includes wallet and payment layers (fiat-on/off ramps, SDKs, MPC custody, etc.);

-

Cross-chain bridges: as the multi-chain reality sets in, secure and compliant bridges will be urgently needed to accommodate application traffic.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News