The birth of a DeFi super app

TechFlow Selected TechFlow Selected

The birth of a DeFi super app

This article will describe how the unbundling and rebundling cycles in SaaS and fintech are unfolding in DeFi and crypto applications.

Author: Lorenzo Valente

As the crypto market matures, investors are looking to past tech booms for clues about the next big trend or inflection point.

Historically, digital assets have been difficult to compare directly with prior technology cycles, making it hard for users, developers, and investors to predict their long-term trajectory. This dynamic is changing.

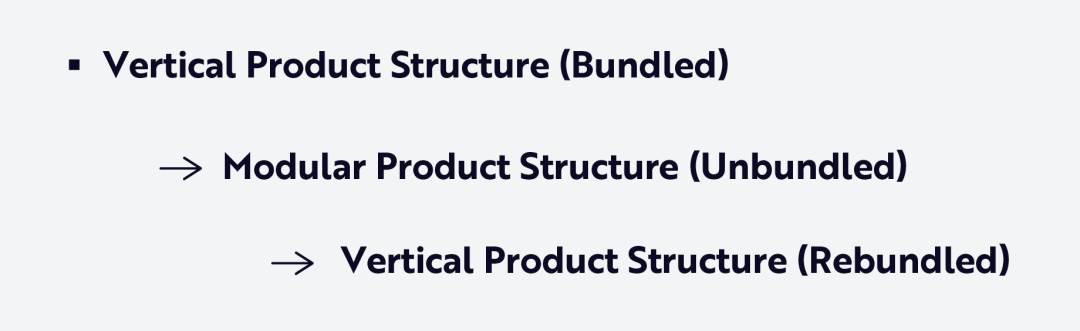

According to our research, the "application layer" in crypto is evolving much like the unbundling and rebundling cycles seen in SaaS (software-as-a-service) and fintech platforms.

In this article, I will describe how the unbundling and rebundling cycles in SaaS and fintech are playing out in DeFi (decentralized finance) and crypto applications. The pattern unfolds as follows:

The concept of "composability" is key to understanding the unbundling and rebundling cycle.

This is an analytical term used in fintech and crypto communities referring to the ability of financial or decentralized applications and services—especially at the application layer—to seamlessly interact, integrate, and build on one another like Lego bricks. Using this concept as a foundation, we describe shifts in product architecture in the two sections below.

From Verticalization to Modularity: The Great Unbundling

In 2010, Andrew Parker of Spark Capital published a blog post illustrating how dozens of startups seized opportunities from Craigslist’s unbundling. Craigslist was then a "horizontal" internet marketplace offering everything from apartments and odd jobs to goods sales, as shown in the image below.

Source: Parker 2010. For illustrative purposes only; not to be construed as investment advice or a recommendation to buy, sell, or hold any specific security.

Parker concluded that many successful companies—Airbnb, Uber, GitHub, Lyft—started by focusing on and vertically specializing in just a small slice of Craigslist’s broad functionality, significantly improving it.

This trend marked the first major phase of “market unbundling,” during which Craigslist’s fully bundled, multipurpose marketplace gave way to single-purpose applications. These newcomers did more than just improve Craigslist’s user experience (UX)—they redefined the experience. In other words, “unbundling” broke apart a broadly scoped platform into tightly focused, independent verticals, disrupting Craigslist by serving users in uniquely better ways.

What made this wave of unbundling possible? Fundamental shifts in technological infrastructure—including advances in APIs (application programming interfaces), cloud computing, mobile UX, and embedded payments—lowered the barrier to building specialized applications with world-class user experiences.

A similar unbundling has evolved in banking. For decades, banks offered a bundled suite of financial services under a single brand and app—from savings and loans to insurance. However, over the past decade, fintech startups have been precisely dismantling this bundle, each focusing on a specific vertical.

The traditional bank bundle includes:

-

Payments and remittances

-

Checking and savings accounts

-

Interest-bearing products

-

Budgeting and financial planning

-

Loans and credit

-

Investments and wealth management

-

Insurance

-

Credit and debit cards

Over the past decade, the bank bundle has been systematically broken down into a series of venture-backed fintech companies, many of which are now unicorns, decacorns, or even approaching hectocorns:

-

Payments and remittances: PayPal, Venmo, Revolut, Stripe

-

Bank accounts: Chime, N26, Monzo, SoFi

-

Savings and yield: Marcus, Ally Bank

-

Personal finance and budgeting: Mint, Truebill, Plum

-

Loans and credit: Klarna, Upstart, Cash App, Affirm

-

Investments and wealth management: Robinhood, eToro, Coinbase

-

Insurance: Lemonade, Root, Hippo

-

Cards and spending management: Brex, Ramp, Marqeta

Each company focused on a service it could refine and deliver better than incumbents, combining its expertise with new technological levers and distribution models to offer growth-oriented niche financial services in a modular fashion. In both SaaS and fintech, unbundling didn’t just disrupt incumbents—it created entirely new categories, ultimately expanding total addressable markets (TAMs).

From Modularity Back to Bundling: The Great Rebundling

Recently, Airbnb launched new "Services & Experiences" and redesigned its app. Users can now not only book accommodations but also explore and purchase add-on services such as museum visits, food tours, dining experiences, gallery walks, fitness classes, and beauty treatments.

Once a peer-to-peer lodging marketplace, Airbnb is now evolving into a vacation superapp—rebundling travel, lifestyle, and local services into a single, cohesive platform. Moreover, over the past two years, the company has expanded beyond home rentals, integrating payments, travel insurance, local guides, concierge tools, and curated experiences into its core booking service.

Robinhood is undergoing a similar transformation. Having disrupted the brokerage industry with commission-free stock trading, the company is now actively expanding into a full-stack financial platform, rebundling many of the verticals previously unbundled by fintech startups.

Over the past two years, Robinhood has taken the following steps:

-

Launched payment and cash management features (Robinhood Cash Card)

-

Added cryptocurrency trading

-

Introduced retirement accounts

-

Launched margin investing and a credit card

-

Acquired Pluto, an AI-driven research and wealth advisory platform

These moves indicate that, like Airbnb, Robinhood is bundling previously fragmented services to build a comprehensive financial superapp.

By controlling more of the financial stack—savings, investments, payments, lending, and advisory—Robinhood is reinventing itself from a broker into a full-service consumer finance platform.

Our research shows that this unbundling and rebundling dynamic is now impacting the crypto industry. In the remainder of this article, we present two case studies: Uniswap and Aave.

The Unbundling and Rebundling Cycle in DeFi: Two Case Studies

Case Study 1: Uniswap – From Monolithic AMM to Liquidity Lego, Back to Trading Superapp

In 2018, Uniswap launched on Ethereum as a simple yet revolutionary automated market maker (AMM). In its early days, Uniswap was a vertically integrated application: a small codebase of smart contracts hosted with an official frontend by the team. The core AMM functionality—swapping ERC-20 tokens in constant-product pools—resided in a single on-chain protocol. Users primarily accessed it through Uniswap's own web interface. This design proved highly successful, with Uniswap’s on-chain trading volume growing explosively to over $1.5 trillion cumulatively by mid-2023. With its tightly controlled tech stack, Uniswap delivered a smooth user experience for token swaps, helping bootstrap DeFi in its early days.

At the time, Uniswap v1/v2 implemented all trading logic on-chain, requiring no external price oracle or off-chain order book. The protocol internally determined prices within a closed system via its liquidity pool reserves (using the x*y=k formula). The Uniswap team developed the main user interface (app.uniswap.org), which interacted directly with Uniswap contracts. Most users initially accessed Uniswap through this proprietary frontend, akin to a dedicated exchange portal. Beyond Ethereum itself, Uniswap relied on no other infrastructure. Liquidity providers and traders interacted directly with Uniswap’s contracts, with no built-in external data feeds or plugin hooks. The system was simple but isolated.

As DeFi expanded, Uniswap evolved into composable liquidity "Lego," rather than remaining a standalone app. The protocol’s open, permissionless nature meant other projects could integrate Uniswap’s pools and add layers on top. Uniswap Labs gradually relinquished control over parts of the stack, allowing external infrastructure and community-built features to play larger roles:

-

DEX aggregators and wallet integrations: Much of Uniswap’s trading volume began flowing through external aggregators like 0x API and 1inch, rather than through Uniswap’s own interface. By the end of 2022, an estimated 85% of Uniswap swap volume was routed through aggregators like 1inch, as users sought optimal pricing across exchanges. Wallets like MetaMask also integrated Uniswap liquidity into their swap functions, enabling users to trade on Uniswap directly from their wallet apps. This external routing reduced reliance on Uniswap’s native frontend, turning the AMM into more of a plug-and-play module within the DeFi stack.

-

Oracles and data indexers: While Uniswap’s contracts never required price oracles for trading, the broader ecosystem built around Uniswap did. Other protocols use Uniswap pool prices as on-chain oracles, while Uniswap’s own interface relies on external indexing services. For example, Uniswap’s frontend uses subgraphs from The Graph to query pool data off-chain for a smoother UI experience. Instead of building its own indexing nodes, Uniswap leveraged community-driven data infrastructure—a modular approach that offloaded heavy data queries to specialized indexers.

-

Multi-chain deployment: During its modular phase, Uniswap expanded beyond Ethereum to numerous blockchains and rollups: Polygon, Arbitrum, BSC, Optimism, etc. Uniswap governance authorized its core protocol to deploy on these networks, effectively treating each blockchain as a base-layer plugin for Uniswap liquidity. This multi-chain strategy emphasized Uniswap’s composability—the protocol could exist on any Ethereum Virtual Machine (EVM)-compatible chain rather than being tied to a single vertically integrated environment.

More recently, Uniswap has been moving back toward vertical integration, aiming to capture more of the user journey and optimize its stack for its use cases. Key reintegration developments include:

-

Native mobile wallet: In 2023, Uniswap launched Uniswap Wallet—a self-custodial mobile app—followed by a browser extension where users can store tokens and interact directly with Uniswap products. Launching a wallet marks a crucial step toward controlling the user interface layer instead of ceding it to wallets like MetaMask. With its own wallet, Uniswap now vertically integrates user access, ensuring swaps, NFT browsing, and other activities occur within its controlled environment and likely route to Uniswap liquidity.

-

Integrated aggregation (Uniswap X): Uniswap introduced Uniswap X, an in-house aggregation and transaction execution layer, eliminating reliance on third-party aggregators for best-price discovery. Uniswap X uses an open network of off-chain "fillers" to source liquidity from various AMMs and private market makers before settling trades on-chain. As a result, Uniswap has transformed its interface into a one-stop trading gateway that aggregates liquidity sources for user benefit—similar to services provided by 1inch or Paraswap. By operating its own aggregator protocol, Uniswap Labs reclaims this function, keeping users internal while guaranteeing optimal pricing. Crucially, UniswapX is integrated directly into the Uniswap web app—and potentially into the wallet in the future—so users no longer need to leave Uniswap to access aggregator functionality.

-

App-specific chain (Unichain): In 2024, Uniswap announced its own Layer 2 blockchain—"Unichain"—as part of the Optimism Superchain. Taking vertical integration to the infrastructure level, Unichain is a custom rollup tailored for Uniswap and DeFi trading, aiming to reduce user fees by ~95% and latency to ~250ms. Uniswap will control the blockchain environment where its contracts run, rather than operate merely as an app on another chain. By running Unichain, Uniswap can optimize everything from gas costs to MEV (Maximal Extractable Value) mitigation for its exchange and introduce native protocol fee sharing with UNI holders. This full-circle transformation shifts Uniswap from a decentralized app (dApp) dependent on Ethereum to a vertically integrated platform with proprietary UI, execution layer, and dedicated blockchain.

Case Study 2: Aave – From P2P Lending Market to Multi-Chain Deployment, Back to Credit Superapp

Aave traces its roots to ETHLend in 2017, a self-contained lending app that evolved in 2018 into a decentralized peer-to-peer lending market renamed Aave. The team developed smart contracts for lending and provided an official web interface for user participation. At this stage, ETHLend/Aave matched lenders and borrowers via an order book model, handling everything from interest rate logic to loan matching.

As it evolved toward a pooled lending model similar to Compound, Aave underwent vertical integration. Aave v1 and v2 contracts on Ethereum included innovations like flash loans—a protocol-native feature allowing uncollateralized borrowing as long as repayment occurs within the same transaction—as well as interest rate algorithms. Users primarily accessed the protocol through Aave’s web dashboard. The protocol internally managed critical functions like interest accrual and liquidations, relying minimally on third-party services. In short, Aave’s early design was a monolithic money market: a dApp with its own UI handling deposits, loans, and liquidations in one place.

Aave has always been part of a broader DeFi symbiosis, integrating MakerDAO’s DAI stablecoin as a key collateral and lending asset from the start. Indeed, during its ETHLend incarnation, Aave launched alongside Maker and immediately supported DAI, reflecting tight coupling between early vertical pioneers and signaling early on that no protocol exists in isolation. Even in its "vertical" phase, Aave benefited from another protocol’s product—stablecoins—to function.

As DeFi matured, Aave unbundled and adopted a modular architecture, outsourcing parts of its infrastructure and encouraging others to build on its platform. Several shifts illustrate Aave’s move toward composability and external dependencies:

-

External oracle networks: Rather than exclusively running its own price feeds, Aave adopted Chainlink’s decentralized oracles to provide reliable asset pricing for collateral valuation. Price oracles are critical to any lending protocol, as they determine when loans become undercollateralized. Aave governance selected Chainlink Price Feeds as the primary oracle source for most assets on aave.com, outsourcing pricing infrastructure to a specialized third-party network. While this modular approach enhances security—for example, Chainlink aggregates multiple data sources—it also means Aave’s stability depends on external services.

-

Wallet and app integrations: Aave’s lending pools became building blocks integrated by many other dApps. Portfolio managers and dashboards like Zapper and Zerion, DeFi automation tools like DeFi Saver, and yield optimizers all access Aave’s contracts via its open SDK. Users can deposit or borrow via third-party frontends that interface with Aave, meaning the official Aave interface is just one of many access points. Even DEX aggregators indirectly leverage Aave’s flash loans for complex multi-step transactions executed by services like 1inch. By open-sourcing its design, Aave enables composability: other protocols can integrate Aave’s features—such as using Aave flash loans inside Uniswap arbitrage bots—all coordinated by external aggregators. As a liquidity module rather than a siloed app, Aave’s composability expands its influence across the DeFi ecosystem.

-

Multi-chain deployment and isolation modes: Like Uniswap, Aave deployed across multiple networks—Polygon, Avalanche, Arbitrum, Optimism—essentially achieving cross-chain modularity. Aave v3 introduced features like isolated markets for certain assets—an architectural modularity—creating separate risk parameters for each market, sometimes running independently from the main pool. It also launched permissioned variants like "Aave Arc" for KYC’d institutional use, which are conceptually independent "module instances" of Aave.

These examples demonstrate Aave’s flexibility across environments, not just within a single integrated setup. In this unbundled phase, Aave relies on a broader infrastructure stack: Chainlink oracles for data, The Graph for indexing, wallets and dashboards for user access, and other protocols’ tokens—like Maker’s DAI or Lido’s staked ETH—as collateral. The modular approach increases Aave’s composability and reduces the need to "reinvent the wheel." The trade-off is partial loss of control over those stack components and associated risks from depending on external services.

Recently, Aave has shown signs of returning to vertical integration by developing internal versions of key components it previously relied on externally. For example, in 2023, Aave launched its own stablecoin, GHO. Historically, Aave facilitated lending of various assets, especially MakerDAO’s DAI stablecoin, which scaled significantly on Aave. With GHO, Aave now has a native stablecoin on its platform, acting as a distribution channel for other protocol stablecoins. Like DAI, GHO is an overcollateralized, decentralized, dollar-pegged stablecoin. Users can mint GHO against their deposits on Aave V3, enabling Aave to reclaim a previously outsourced vertical in the lending stack—stablecoin issuance. Therefore:

-

Aave becomes an issuer of stable assets—not just a venue for borrowing existing stablecoins—and gains direct control over stablecoin parameters and revenue. GHO competes with DAI, so now Aave can recapture interest payments within its own ecosystem, benefiting AAVE token stakers instead of indirectly increasing fees for MakerDAO.

-

GHO’s introduction also requires dedicated infrastructure. Aave has "facilitators"—including major Aave pools—that can mint and burn GHO and set governance policies. By controlling this new functional layer, Aave builds an internal version of a MakerDAO product to serve its own community.

In another notable move, Aave is leveraging Chainlink’s Smart Value Routing (SVR) or similar mechanisms to recapture MEV (Maximal Extractable Value, analogous to payment for order flow in equities) for Aave users. Tighter coupling with the oracle layer to redirect arbitrage profits back to the protocol is blurring the boundary between the Aave platform and underlying blockchain mechanics. This suggests Aave is interested in customizing—or even owning—lower-level infrastructure like oracle behavior and MEV capture for its own benefit.

While Aave hasn’t launched its own wallet or chain like Uniswap and others, the founder’s other ventures suggest a vision of building a self-sustaining ecosystem. For instance, Lens Protocol, designed for social networking, could integrate with Aave for reputation-based finance. Architecturally, Aave is moving toward providing all key financial primitives—lending, stablecoin (GHO), and possibly decentralized social identity (Lens)—rather than relying on external protocols. In my view, this product strategy focuses on deepening the platform: by owning stablecoins, loans, and other services, Aave should see improved user retention and protocol revenue.

In summary, Aave has evolved from a closed-loop lending dApp into an open Lego-like system integrated with DeFi and dependent on others like Chainlink and Maker, and is now returning to a more expansive vertically integrated financial suite. The launch of GHO, in particular, highlights Aave’s intent to rebundle the stablecoin layer it once outsourced to MakerDAO.

Our research shows that the journeys of Uniswap, Aave, MakerDAO, Jito, and other protocols reflect a broader cyclical pattern in crypto. Early on, vertical integration—building a monolithic product with a very specific purpose—was necessary to pioneer new capabilities like automated trading, decentralized lending, stablecoins, or MEV capture. These self-contained designs allowed rapid iteration and quality control in emerging markets. As the field matured, modularity and composability became priorities: protocols unbundled parts of their stack to launch new features or deliver more value to external stakeholders, becoming "money Legos" by leveraging others’ strengths.

However, the success of modularity and composability brought new challenges. Relying on external modules introduced dependency risks and limited the ability to capture value generated elsewhere. Now, the largest players and protocols with strong product-market fit (PMF) and revenue streams are shifting strategies back toward vertical integration. While not abandoning decentralization or composability, these projects are strategically rebundling key components—launching their own chains, wallets, stablecoins, frontends, and other infrastructure. Their goals are to deliver a more seamless user experience, capture additional revenue streams, and reduce dependence on competitors. Uniswap is building wallets and chains, Aave is issuing GHO, MakerDAO is forking Solana to build NewChain, Jito is merging staking/restaking with MEV. We believe any sufficiently large DeFi application will eventually seek its own vertically integrated solution.

Conclusion

History doesn't repeat itself, but it often rhymes. Crypto is humming a familiar tune. Just like the SaaS and marketplace revolutions of the past decade, DeFi and application-layer protocols are progressing along a path of unbundling and rebundling, driven by new technical primitives, shifting user expectations, and the desire to capture more value.

In the 2010s, startups that specialized in narrow segments of the massive Craigslist marketplace effectively atomized it into distinct companies. This unbundling gave rise to giants—Airbnb, Uber, Robinhood, Coinbase—all of which later began their own rebundling journeys, integrating new verticals and services into cohesive, sticky platforms.

Crypto is following the same path—but at a revolutionary pace.

Protocols that started as narrowly scoped vertical experiments—Uniswap as an AMM, Aave as a money market, Maker as a stablecoin vault—modularized into permissionless Lego, opened up liquidity, outsourced key functions, and let composability flourish. Now that scale has been achieved and markets fragmented, the pendulum is swinging back.

Today, Uniswap is becoming a trading superapp with its own wallet, chain, cross-chain standards, and routing logic. Aave is issuing its own stablecoin and bundling lending, governance, and credit primitives. Maker is building an entirely new chain to improve governance of its monetary ecosystem. Jito unifies staking, MEV, and validator logic into a full-stack protocol. Hyperliquid merges exchange, L1 infrastructure, and EVM into a seamless on-chain financial OS.

In crypto, primitives are designed to be unbundled, but the best user experience—and the most defensible business—is increasingly rebundled. This isn’t a betrayal of composability, but its fulfillment: build the best Lego bricks, then use them to construct the best castle.

DeFi is compressing this entire cycle into just a few years. How? Because DeFi operates fundamentally differently:

-

Permissionless infrastructure reduces friction: Any developer can fork, copy, or extend existing protocols in hours, not months.

-

Capital formation is instant—tokens allow teams to fund new projects, ideas, or incentives faster than ever before.

-

Liquidity is highly mobile. Total Value Locked (TVL) moves at the speed of incentives, making it easier for new experiments to gain attention and successful ones to scale exponentially.

-

The potential market size is larger. Protocols access a global, permissionless pool of users and capital from day one, often scaling faster than Web2 peers constrained by geography, regulations, or distribution channels.

DeFi’s superapps are rapidly expanding in real time. We believe the winners won’t be the protocols with the most modular stacks, but those that know exactly which parts of the stack to own, which to share, and when to switch between the two.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News