Who controls stablecoin custody, controls the future of banking

TechFlow Selected TechFlow Selected

Who controls stablecoin custody, controls the future of banking

From deposits to stablecoins, banking is undergoing its biggest transformation in 200 years.

Author: Decentralised.Co

Translation: TechFlow

Whoever controls the foundation of stablecoins controls the future of banking. For the past 200 years, banks achieved scale by absorbing deposits; fintech companies expanded by renting deposits. Today, stablecoins have made deposits mobile—a shift that is reshaping the global banking landscape.

Every banking revolution begins with a transformation in how money is stored.

In the 19th century, banks issued private notes backed by gold, but trust was local and fragile.

In the 20th century, centralized trust through the Federal Reserve and the Federal Deposit Insurance Corporation (FDIC) gave rise to banking giants like JPMorgan Chase and Citibank.

In the 2010s, fintech companies built new types of banks using digital tools—examples include Revolut and Nubank.

Today, stablecoins are fully extracting deposits from banks, making them programmable, borderless, and highly liquid at internet scale.

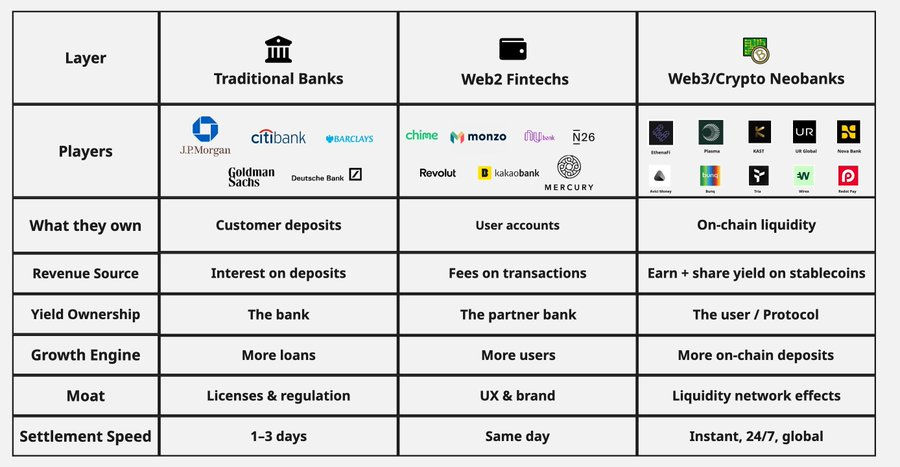

Web2 fintech companies redesigned the interface of banking, but left the underlying infrastructure unchanged.

For example, Revolut holds customer deposits at Lloyds Bank; Nubank’s reserves ultimately sit at the Central Bank of Brazil; Wise still settles via SWIFT. These companies changed how people interact with money—but not where money is actually held.

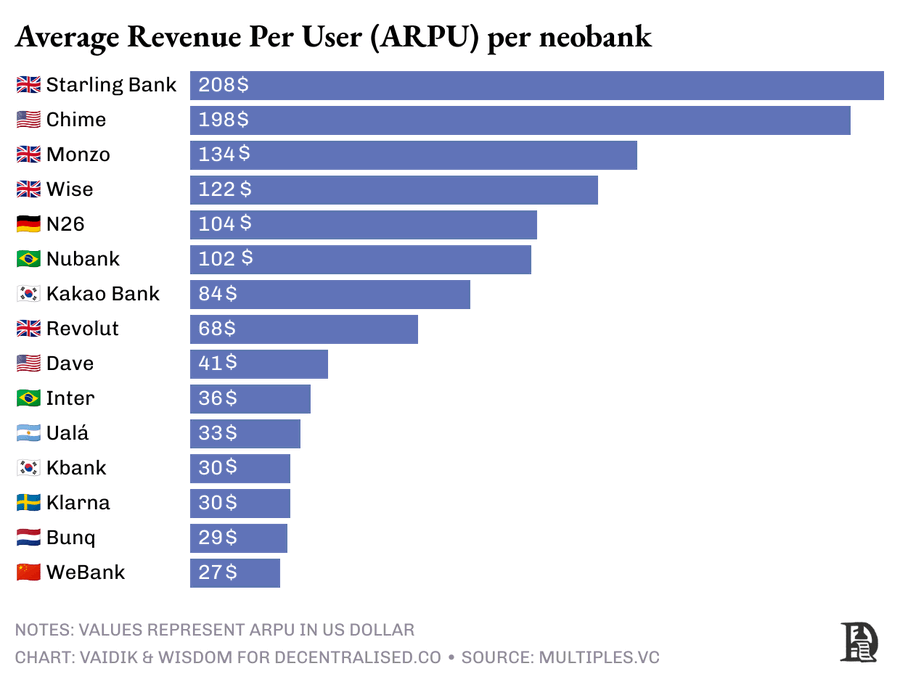

As a result, among the world's 15 largest neobanks, nine generate less than $100 in annual revenue per user.

Web2 fintech built better bank apps, while crypto neobanks are building better banks.

These banks operate by holding stablecoin deposits directly on-chain and using those balances as their funding base. Like traditional banks, they deploy deposits—but instead of opaque balance sheets and lending, they direct liquidity into transparent on-chain markets such as tokenized U.S. Treasuries or decentralized finance (DeFi) lending pools.

Users can see where funds are going and, in some cases, even share in the returns.

Because programmable finance doesn’t require physical branches, it can expand fastest in places where traditional banks cannot serve.

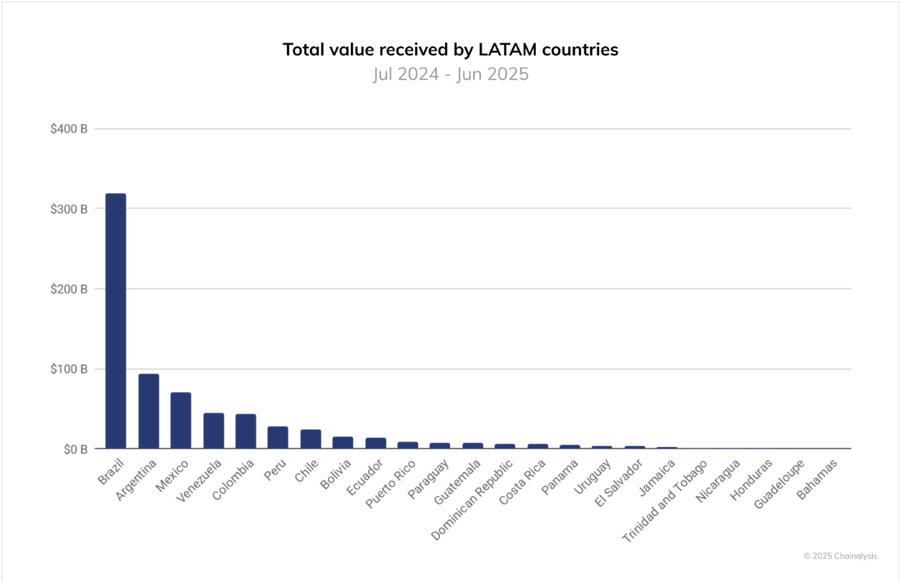

In regions where banks fail to preserve asset value, stablecoin-powered neobanks have become the default method for storing, paying, and transferring money.

According to Chainalysis, last year saw over $1.5 trillion in cryptocurrency inflows across Latin America—$319 billion in Brazil alone—with nearly 90% coming from stablecoins used for savings, payroll, and remittances.

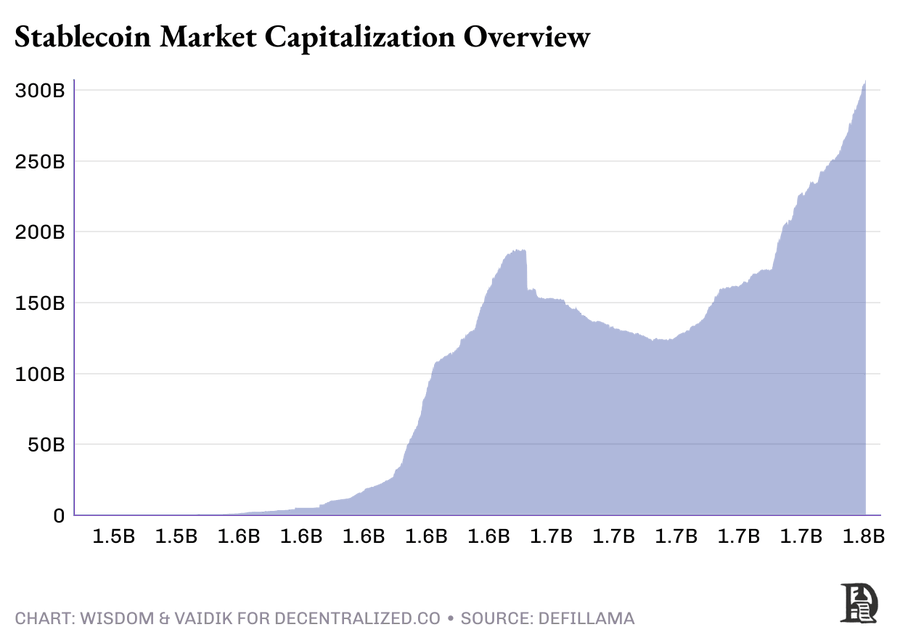

As stablecoins enter the mainstream, deposits are increasingly pooling outside the traditional banking system.

Today, more than $300 billion in digital dollars flows between wallets and tokenized treasuries. Though these flows remain uncoordinated, their scale is already massive.

A similar situation occurred in the 19th century: hundreds of “free banks” issued their own notes, each backed by different reserves. This led to frequent bank runs and collapses in trust—until institutions like JPMorgan Chase began consolidating deposits to restore stability and unify the system.

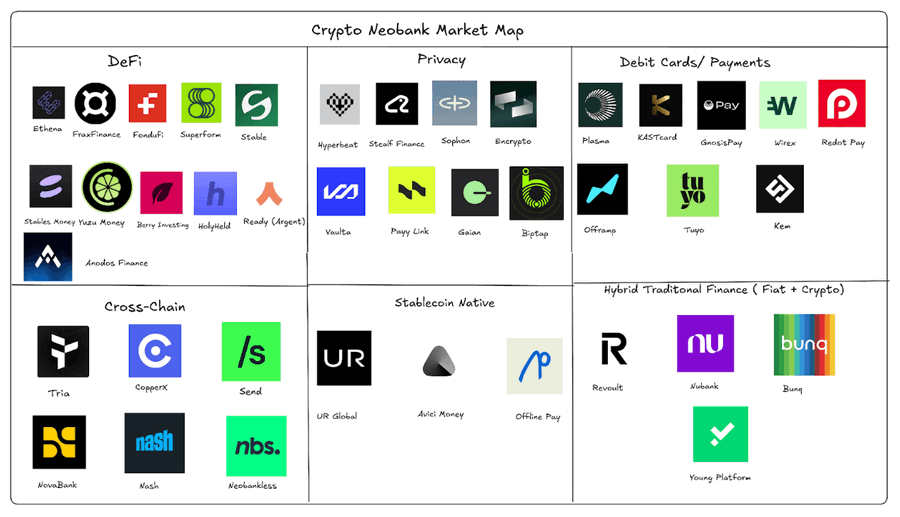

Crypto neobanks are solving the same problem today by organizing fragmented digital dollar deposits into a coherent system.

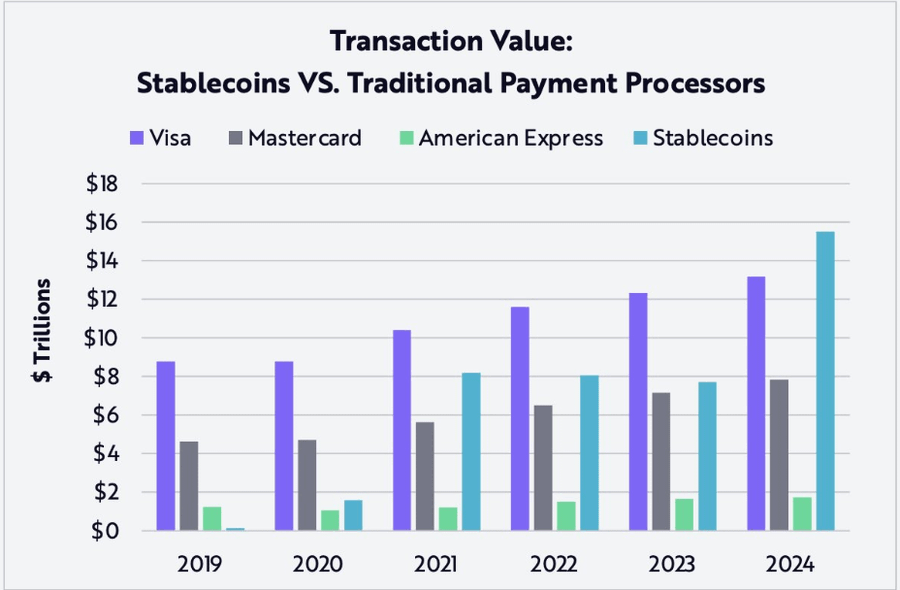

According to ARK Invest’s BIG IDEAS 2025 report, stablecoins settled over $15.6 trillion in transactions in 2024—more than the combined total of Mastercard and American Express.

The platforms managing these flows—wallets, exchanges, and crypto neobanks—are quietly becoming the new settlement layer of global finance.

Protocols like KAST, Tria, and Plasma are becoming the default hubs for stablecoin liquidity—just as JPMorgan once centralized dollar clearing, or Stripe did for online payments.

KAST is a payments neobank; Tria builds self-custodial accounts for users; Plasma provides the on-chain infrastructure that powers money movement.

That’s why giants like BNY Mellon and Visa are racing to integrate stablecoin payment networks, while Stripe is building its own Layer 1 blockchain. They’re all chasing the same goal: controlling where digital dollars are stored—because everything else in finance is built on top of this foundation.

Traditional banks earn a few percentage points by investing deposits in loans and securities, but pass almost none of the returns back to users.

With tokenized dollars, these yields are no longer hidden within bank balance sheets. Users can see exactly where returns come from and where they go—and in many cases, directly participate in them.

Total global commercial deposits amount to approximately $87 trillion.

As more capital moves on-chain, this capital will no longer need intermediaries to transfer or earn yield—it will demand efficiency. And whoever builds these on-chain payment networks will dominate the next era of banking.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News