How far is the world where everyone can buy U.S. stocks without financial access barriers?

TechFlow Selected TechFlow Selected

How far is the world where everyone can buy U.S. stocks without financial access barriers?

If the vision of crypto is to put everything on the chain, stocks will undoubtedly be a crucial piece of the puzzle, making this experiment one to watch.

Author: Fishmarketacad

Translation: AididiaoJP, Foresight News

Stock tokenization is not a new term, but due to Robinhood's announcement of launching tokenized U.S. stock services for European customers—and even developing its own L2—stock tokenization has once again become a market focus.

Most people still have only a vague understanding of stock tokenization. This article attempts to provide a comprehensive overview of the fundamentals of stock tokenization, covering:

-

Definition and operational mechanisms of tokenized stocks

-

Why do we need tokenized stocks?

-

Comparison between spot and perpetual contract-based tokenized stocks

-

The future of tokenized stocks

1. What Are Tokenized Stocks? How Do They Operate Legally?

Before discussing the differences between spot and perpetual contract-based tokenized stocks, let’s first understand why tokenized stocks are regaining attention.

Regulatory and Legal Uncertainty

Although there are technical challenges with tokenized stocks, the legal aspects are more complex. For years, major jurisdictions like the United States lacked clear regulations, forcing crypto companies to offer related services in crypto-friendly regions. The Crypto Act provides a clear legal framework for issuing tokenized securities, introducing the legal concept of a book-entry system (Wertrecht), allowing digital records to replace physical stock certificates. The Crypto Act makes it legally feasible to tokenize real-world assets.

Backedfi's Practice

Backedfi issued "bTokens" in Liechtenstein—ERC-20 tokens representing fully collateralized tracking stocks. Each bCOIN token corresponds to actual Coinbase shares held by a custodian. This structure separates regulated issuance processes from permissionless secondary market trading.

Users must complete full KYC/AML procedures to directly mint or redeem bTokens. These tokens can be freely transferred and traded on DEXs or a few regulated exchanges. When qualified investors redeem bTokens, they receive cash value rather than the underlying stock, as Backed’s broker publicly sells the underlying shares and transfers the proceeds, minus a small redemption fee, into fiat or stablecoins like USDC. Redeemed bTokens are immediately destroyed, ensuring a 1:1 redemption ratio.

bTokens do not confer stock ownership or voting rights; they represent contractual claims to the economic value of the underlying stock. If Backedfi goes bankrupt, the underlying stocks are held by an independent third-party custodian, segregated from company assets. bToken holders may recover value as creditors through liquidation, though the process is complicated.

Who Can Trade These Tokenized Stocks?

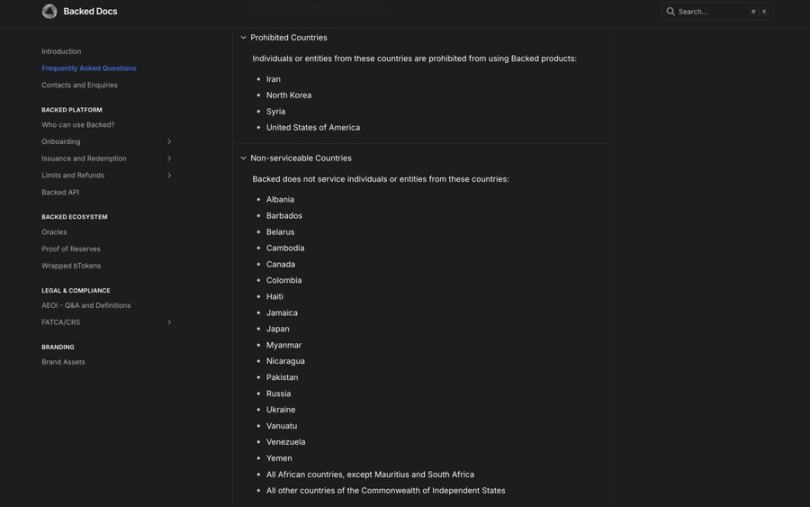

bTokens are regulated under European law (specifically in Liechtenstein and Jersey) and are not registered with the U.S. Securities and Exchange Commission.

Once minted, these tokens can be traded permissionlessly on DEXs, which should block access for U.S. users. The core challenge lies here: issuers have clear compliance obligations, but controlling secondary market access comprehensively is extremely difficult. For U.S. users, bypassing restrictions to trade these tokens remains a high-risk, non-compliant activity.

Robinhood's Model

Robinhood takes a fundamentally different approach, embedding blockchain-related technology within its own trading platform while maintaining a centralized, user-friendly interface. Robinhood’s stock tokens are not direct claims on stocks but derivatives constructed under MiFID II regulations. When users “purchase” stock tokens, they are actually entering into contracts with Robinhood Europe that track U.S. stock prices.

The underlying assets are held by U.S.-licensed institutions, and the tokens are essentially recorded on a blockchain (initially Arbitrum, with plans to migrate to a proprietary L2). This structure allows Robinhood to deliver a seamless user experience while retaining full control over the assets. Key features include:

-

Closed ecosystem: Users can buy, sell, and hold tokenized stocks within the Robinhood app but cannot withdraw them to external wallets or other platforms, limiting their composability within the DeFi ecosystem.

-

24/5 trading: Bridges the time gap between European and U.S. markets, enabling users to respond to market movements outside traditional trading hours.

-

Seamless operations: Automatically handles corporate actions such as stock splits and mergers, with cash dividends paid in euros without currency conversion fees, simplifying the user experience.

Effectively, Robinhood uses blockchain as an efficient internal ledger to provide exposure to U.S. stock derivatives. This approach prioritizes usability and compliance within its platform over the open ecology of DeFi. While the closed system offers retail users a secure experience, it sacrifices DeFi’s composability.

By preventing users from withdrawing their tokenized stocks, these assets cannot serve as collateral or liquidity in broader on-chain economies. This creates an opportunity for other platforms to leapfrog ahead—not only competing for users but also building truly permissionless and interoperable tokenized assets that form the foundation of an open DeFi ecosystem.

Regulatory Summary

Global regulation has given rise to two dominant models for tokenizing stocks:

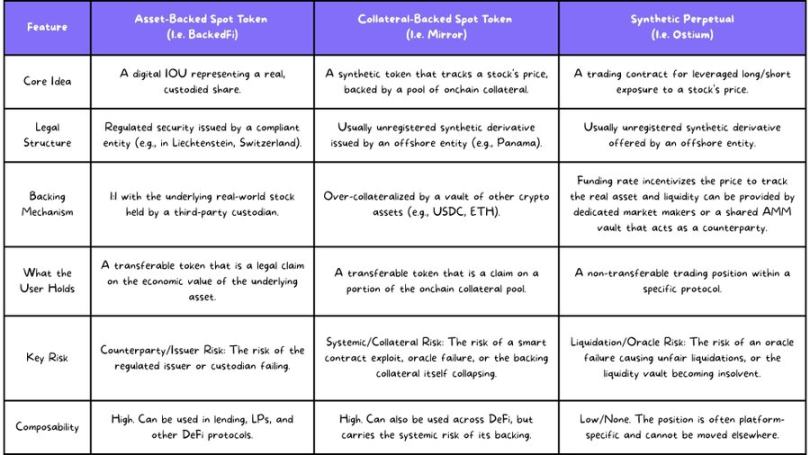

1. Spot Tokenized Stocks

Both Robinhood and Backed.fi adopt this model, where each on-chain token corresponds to real stocks held by a custodian. Differences lie in:

-

Crypto-native firms like Backed.fi purchase stocks (e.g., TSLA), which are held by custodians, and then mint corresponding tokens (e.g., bTSLA) on public blockchains. Tokens can be freely transferred and composed, but only qualified investors can directly mint/redeem.

-

Robinhood’s stock tokens for European clients are derivatives under MiFID II, with underlying assets held by U.S.-licensed institutions. The tokens are on-chain IOUs currently non-withdrawable to external wallets.

2. Perpetual Futures

This model does not involve direct ownership of underlying assets and exists in a legal gray area.

Operation: Decentralized perpetual exchanges face significant legal risks when listing perpetual contracts on stocks. U.S. and European regulators view security-based derivatives as regulated products requiring specific licenses. To mitigate risk, decentralized perpetual exchanges often register in crypto-friendly jurisdictions and restrict access from certain countries (e.g., the U.S.).

These two models have distinct advantages and disadvantages, catering to different user needs and risk preferences.

2. Why Do We Need Tokenized Stocks?

Why do we need tokenized stocks? The answer depends on the user’s identity and location.

Bull Case: A More Open Global Market

The strongest argument for tokenized stocks lies in their potential to democratize financial access globally.

-

Global financial inclusion: Participation in U.S. and European stock markets is high, but only 5–15% of users in other regions can invest in U.S. stocks. Tokenized stocks allow users in Southeast Asia or Latin America to gain exposure to U.S. stocks using just a smartphone and internet connection, without meeting traditional banking requirements.

-

24/7 market access: U.S. trading hours are inconvenient for Asian users. Tokenized stocks break this barrier, allowing global users to trade according to their own strategies.

-

Permissionless innovation: Tokenized stocks are open financial primitives. Developers worldwide can build new applications on top of them, such as self-custody brokerage apps, complex structured products, or automated yield vaults—innovations impossible with traditional brokers.

Bear Case: Niche Products for Developed Markets

For average investors in developed countries, there is no urgent need for tokenized stocks:

-

Solving real problems?: Users in the U.S. and Europe can already use low-cost, easy-to-use platforms like Robinhood. While self-custody in DeFi is powerful, wallet setup, gas fee management, and hacking risks remain significant barriers for mainstream adoption.

-

Liquidity fragmentation: On-chain trading experiences are poor, with high slippage for large orders. Unless on-chain liquidity approaches traditional market levels, users face impermanent loss risks.

Currently, the most urgent demand for stock tokenization comes from groups excluded by the traditional financial system. For developed nations, its true value will gradually emerge as the DeFi ecosystem matures and composability advantages become evident.

3. Spot vs. Perpetual Contract-Based Stock Tokenization: Utility and Challenges

After understanding the legal scope and technical structures of on-chain stocks, we can now examine how users weigh the trade-offs between the two in practice. Two main models dominate the market:

-

Asset-backed stock tokens: Confer stock ownership

-

Synthetic perpetual contracts: Designed for capital-efficient trading

While a third theoretical model exists (e.g., collateralized spot tokens like Mirror Protocol), its systemic risks have been too high for market acceptance. Therefore, this article focuses on the first two models.

Spot Stock Tokenization: Utility and Challenges

Utility

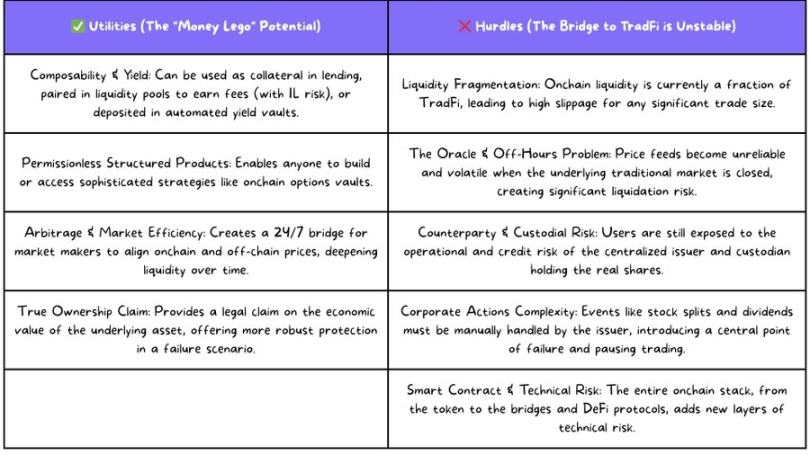

On traditional brokerage platforms, users can only use stock portfolios as collateral for margin loans, with limited utility. The core advantage of tokenization is composability—transforming static assets into dynamic "money legos" that enable use cases unreachable in traditional finance:

Autonomous yield generation: Users can deposit tokenized stocks into yield vaults. The vaults pledge them to lending protocols to borrow stablecoins and automatically compound returns back into the stock position, turning passive holdings into actively revenue-generating assets.

Permissionless structured products: On-chain protocols can execute complex trading strategies. As tokenized stocks mature, options protocols will emerge, allowing users to run options strategies by depositing tokenized stocks and gaining return opportunities independent of crypto markets.

Liquidity provision: Users can pair tokenized stocks with other assets to provide liquidity and earn trading fee shares (though subject to impermanent loss risk).

Promoting arbitrage and market efficiency: Tokenized stocks create a 24/7 bridge between on-chain and traditional markets. When market makers detect significant price deviations—say, between an Apple token on-chain and Nasdaq—they can lock in risk-free profits by buying the undervalued asset and selling the overvalued one, driving prices back into alignment and enhancing market liquidity.

Challenges

Significant obstacles remain on the development path:

Liquidity fragmentation: This is the most pressing issue. Current liquidity in tokenized stocks is far from sufficient to support large trades. Traditional markets easily handle million-dollar orders, whereas on-chain transactions of $100,000 can cause over 1% slippage.

Oracle and market closure issues: DeFi relies on oracles for asset pricing, but what is the “true price” when traditional markets are closed? For example, during geopolitical turmoil, Pax Gold (PAXG) surged 20% due to low volume. If oracles treat such temporary spikes as “true prices,” it could trigger cascading liquidations across lending markets and perpetual DEXs, creating systemic risk.

Smart contract and technical risks: Every layer—from token contracts to cross-chain bridges to DeFi protocols—introduces new potential failure points. Even historically secure protocols like GMX v1 can be exploited years later.

Counterparty and custody risk: Even fully collateralized spot tokens require trust in issuers (e.g., Backedfi or Robinhood) and their custodians. Though regulated, these institutions are not risk-free. In case of failure, users must go through lengthy legal processes to reclaim asset value.

Corporate action handling: Events like stock splits, dividend payments, and mergers cannot be autonomously executed on-chain and require intervention by centralized operators.

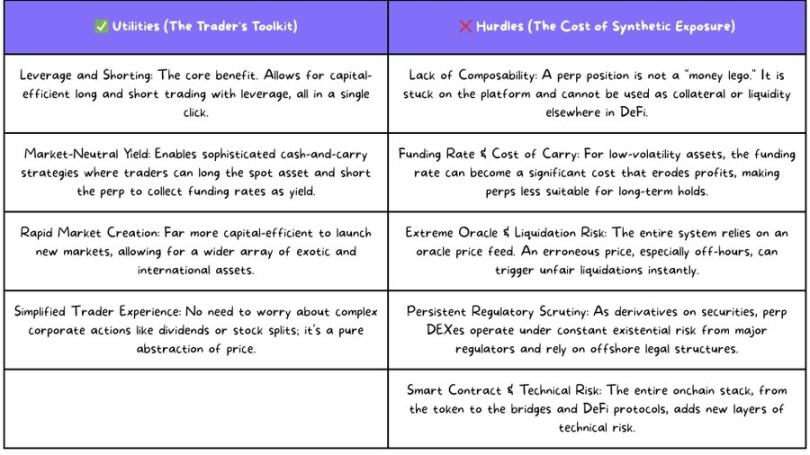

Perpetual Contract-Based Stock Tokenization: Utility and Challenges

Perpetual contracts do not aim to confer asset ownership but focus on providing pure, capital-efficient price exposure—the preferred tool for active traders.

Utility

The core advantages of perpetual DEXs center around trading:

Advanced trading features (leverage and shorting): One-click long/short functionality facilitates high-frequency trading.

Capital efficiency and rapid market creation: Unlike spot tokens requiring millions in custodied underlying stocks, a perpetual DEX can launch a market with just a well-capitalized AMM pool, enabling flexible listing of diverse assets.

Simplified trading experience: No underlying assets mean no need to handle dividends, stock splits, or other corporate actions—traders can focus solely on price movements.

Delta-neutral yield strategies: When spot tokens and perpetual contracts coexist, market-neutral yield strategies become possible. For instance, when funding rates are positive, buying spot and shorting perpetuals enables capital-efficient “cash and carry” arbitrage (similar to Ethena’s strategy).

Challenges

The unique risks of perpetual contracts cannot be ignored:

Lack of ownership and composability: Perpetual positions usually cannot be withdrawn, lent, or used as collateral in other DeFi protocols—composability is sacrificed for trading efficiency.

Funding rate complexity and “holding cost”: When market sentiment strongly favors one side, longs must continuously pay shorts. For low-volatility stocks, funding rates may exceed daily price movements, eroding profits. Thus, perpetuals are better suited for short-to-medium-term trading or delta-neutral strategies.

Extreme oracle and liquidation risks: The system is entirely dependent on oracle prices. During traditional market closures, if oracles pull abnormal prices from illiquid sources, instantaneous cascading liquidations may occur.

Ongoing regulatory pressure: As security derivatives, perpetual DEXs typically register in offshore jurisdictions and use geo-blocking to avoid U.S. and European regulation, yet they constantly face existential risks from policy crackdowns.

4. The Future of Stock Tokenization

Robinhood’s entry has shifted this space from niche experimentation to a mainstream race. Over the next year, we will see:

Liquidity battles: Platforms will compete for market makers and trading volume through incentives like yield farming and point airdrops, addressing the classic “chicken-and-egg” problem.

Exploration of regulatory paths: More issuers will follow Liechtenstein’s model, and frameworks from places like Hong Kong may also become templates. Tentative collaborations between traditional financial institutions and compliant crypto firms will emerge.

Composability in practice: Mainstream lending protocols may begin accepting “blue-chip” tokenized stocks as collateral. Automated yield vaults and basis trading strategies will rise in popularity.

Maturity of perpetual markets: Listed assets will expand beyond U.S. tech stocks to include Hong Kong stocks and commodities. Upgrades to oracles and risk management systems will become key technical priorities.

If the vision of crypto is to put everything on-chain, stocks are undoubtedly a crucial piece of the puzzle. This experiment is worth watching closely.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News