Crypto Market Macro Report: Signs of an Altcoin Season Emerge, Institutional Adoption Fuels Selective Bull Run

TechFlow Selected TechFlow Selected

Crypto Market Macro Report: Signs of an Altcoin Season Emerge, Institutional Adoption Fuels Selective Bull Run

The next wave of wealth transfer is already underway.

1. Macro Turning Point Reached: Regulatory Warming and Policy Support Align

At the beginning of Q3 2025, a quiet transformation has taken place in the macro landscape. The policy environment that once pushed digital assets to the margins is now becoming an institutional driving force. Against the backdrop of the Federal Reserve ending its two-year rate-hiking cycle, fiscal policy returning to stimulus mode, and global crypto regulation accelerating toward an "inclusive framework," the crypto market stands on the brink of structural revaluation.

First, from a monetary policy perspective, U.S. macro liquidity is entering a critical turning window. While the Fed officially emphasizes "data dependency," markets have already priced in rate cuts during 2025. The growing divergence between the lagging dot plot and forward-looking futures expectations highlights this shift. Ongoing political pressure from the Trump administration on the Fed is further politicizing monetary tools, signaling that real interest rates will gradually decline from their highs in the second half of 2025 through 2026. This expectation gap opens an upward valuation channel for risk assets—especially digital assets. More importantly, as Powell becomes marginalized in political maneuvering and a more "compliant Fed chair" looms, monetary easing may not just remain an expectation but become policy reality.

Meanwhile, fiscal expansion is unfolding in parallel. Fiscal stimulus like the "One Great America Act" is unleashing unprecedented capital flows. The Trump administration’s massive spending on manufacturing reshoring, AI infrastructure, and energy independence is creating a cross-sector “capital flood channel” spanning traditional industries and emerging tech. This not only reshapes the internal circulation structure of the dollar but also indirectly boosts marginal demand for digital asset classes—particularly as capital seeks high-risk premiums. Concurrently, the U.S. Treasury has adopted a more aggressive strategy in bond issuance, signaling tolerance for debt expansion and reviving Wall Street's consensus around "printing money for growth."

The fundamental shift in policy signals is most evident in regulatory restructuring. In 2025, the SEC’s stance toward the crypto market underwent a qualitative change. The official approval of ETH staking ETFs marks the first time U.S. regulators have recognized yield-bearing digital assets as eligible for integration into traditional finance. Meanwhile, progress on Solana ETFs has given even previously labeled “high-Beta speculative chains” like Solana a historic opportunity for institutional adoption. Crucially, the SEC is now developing unified standards to streamline token ETF approvals, aiming to create a replicable, scalable compliance pipeline. This represents a fundamental shift in regulatory logic—from a “firewall” to a “pipeline project”—with crypto assets now being incorporated into financial infrastructure planning for the first time.

This regulatory mindset shift isn't unique to the U.S. Compliance races are heating up across Asia, particularly in financial hubs such as Hong Kong, Singapore, and the UAE, all competing for regulatory advantages in stablecoins, payment licenses, and Web3 innovation projects. Circle applying for U.S. licensing, Tether launching a Hong Kong-dollar-pegged stablecoin, and Chinese giants like JD.com and Ant Group pursuing stablecoin-related qualifications indicate that the convergence of sovereign capital and internet behemoths has begun. Stablecoins will no longer be mere trading tools but integral components of payment networks, corporate settlements, and even national financial strategies—driving systemic demand for on-chain liquidity, security, and infrastructure assets.

Moreover, risk appetite in traditional markets shows signs of recovery. The S&P 500 hit new highs in June, with tech stocks and emerging assets rebounding in tandem. IPO activity is warming up, and user engagement on platforms like Robinhood is rising—all signaling that risk capital is flowing back. This round of capital return isn’t solely focused on AI and biotech but is starting to revalue blockchain, crypto finance, and on-chain structured yield assets. This behavioral shift in capital allocation is more honest than narratives and more forward-looking than policy changes.

When monetary policy enters a loosening phase, fiscal policy fully unleashes liquidity, regulation shifts toward “inclusion equals support,” and overall risk appetite recovers, the environment for crypto assets has clearly moved beyond the困境 of late 2022. Under this dual engine of policy and market momentum, one conclusion emerges clearly: the brewing of a new bull market isn't driven by sentiment—it’s a process of institutional-driven value revaluation. It’s not merely about Bitcoin taking off; it’s about global capital markets restarting their practice of “paying premiums for certainty.” The spring of crypto is returning—not explosively, but steadily and powerfully.

2. Structural Rotation: Enterprises and Institutions Are Leading the Next Bull Run

The most significant structural change in today’s crypto market isn’t price volatility, but the deep-seated shift of holdings—from retail investors and short-term capital to long-term holders, corporate treasuries, and financial institutions. After two years of cleansing and restructuring, the participant base of the crypto market is undergoing a historic reshuffle: speculation-driven users are being marginalized, while institutions and enterprises investing for strategic allocation are becoming the decisive forces behind the next bull run.

Bitcoin’s performance tells the whole story. Despite unremarkable price movements, its circulating supply is rapidly moving into “locked-up” status. According to data tracking by firms including QCP Capital, listed companies have cumulatively purchased more Bitcoin over the past three quarters than ETFs have net bought in the same period. Firms like MicroStrategy, NVIDIA supply chain partners, and even some traditional energy and software companies now view Bitcoin as a “strategic cash alternative,” not just a short-term portfolio tool. This behavior reflects a deep understanding of global currency devaluation trends and a proactive response based on insights into incentive structures like ETFs. Compared to ETFs, direct spot purchases give enterprises greater flexibility, voting rights, and stronger holding resilience, making them less susceptible to market sentiment swings.

At the same time, financial infrastructure is removing barriers for institutional inflows. The approval of Ethereum staking ETFs does more than expand the boundary of compliant products—it signifies that institutions are beginning to include “on-chain yield assets” in traditional portfolios. Anticipated approval of Solana spot ETFs further broadens the horizon. Once staking yield mechanisms are packaged into ETFs, they will fundamentally alter traditional asset managers’ perception of crypto as “non-yielding, purely volatile,” prompting a shift from hedging to yield-based allocation. Additionally, Grayscale’s major crypto funds applying to convert into ETFs mark the breaking down of barriers between traditional fund management and blockchain-based asset management.

More importantly, corporations are directly engaging in on-chain financial markets, dismantling the previous isolation between “off-exchange investment” and the on-chain world. Bitmine increased its ETH holdings by $20 million via private placement, while DeFi Development went further, deploying $100 million to acquire Solana ecosystem projects and repurchase platform equity—demonstrating active participation in building the next-generation crypto financial ecosystem. This goes beyond traditional VC investments in startups; it’s capital injection with characteristics of “industrial consolidation” and “strategic positioning,” aimed at securing core rights and profit-sharing privileges within new financial infrastructure. The resulting market impact is long-tailed: stabilizing market sentiment and enhancing valuation anchoring capabilities at the protocol layer.

In derivatives and on-chain liquidity, traditional finance is actively expanding its footprint. CME’s open interest in Solana futures reached 1.75 million contracts—a record high—while monthly trading volume for XRP futures surpassed $500 million for the first time, indicating that traditional trading institutions have integrated crypto assets into their strategy models. The driving forces behind this are hedge funds, structured product providers, and multi-strategy CTA funds. These players don’t chase quick profits but operate based on volatility arbitrage, capital structure games, and quantitative factor models—bringing fundamental improvements in “liquidity density” and “market depth.”

From a structural rotation standpoint, the notable decline in retail and short-term trader activity reinforces these trends. On-chain data shows a continuous drop in the proportion of short-term holders, declining activity among early whale wallets, and stabilization in search and wallet interaction metrics—indicating the market is in a “consolidation and settlement phase.” Although prices appear flat during this stage, historical patterns show that such quiet periods often precede the biggest rallies. In other words, the chips are no longer in retail hands— institutions are quietly building foundational positions.

Equally important, financial institutions' “productization capability” is rapidly materializing. From JPMorgan Chase, Fidelity, and BlackRock to emerging retail platforms like Robinhood, PayPal, and Revolut, all are expanding crypto trading, staking, lending, and payment functionalities. This not only makes crypto assets truly usable within fiat systems but also enhances their financial attributes. In the future, BTC and ETH may no longer be seen simply as “volatile digital assets,” but as “configurable asset classes”—complete with derivatives markets, payment use cases, yield structures, and credit ratings forming a full-fledged financial ecosystem.

At its core, this structural rotation isn’t just a simple shift in holdings—it’s a deepening of crypto asset “financial commodification” and a complete transformation of value discovery logic. The dominant players are no longer emotion- and hype-driven “fast-money crowds,” but institutions and enterprises with clear mid-to-long-term strategic plans, rational allocation frameworks, and stable capital structures. A truly institutionalized, structurally grounded bull market is quietly forming—not loud or emotional, but solid, enduring, and transformative.

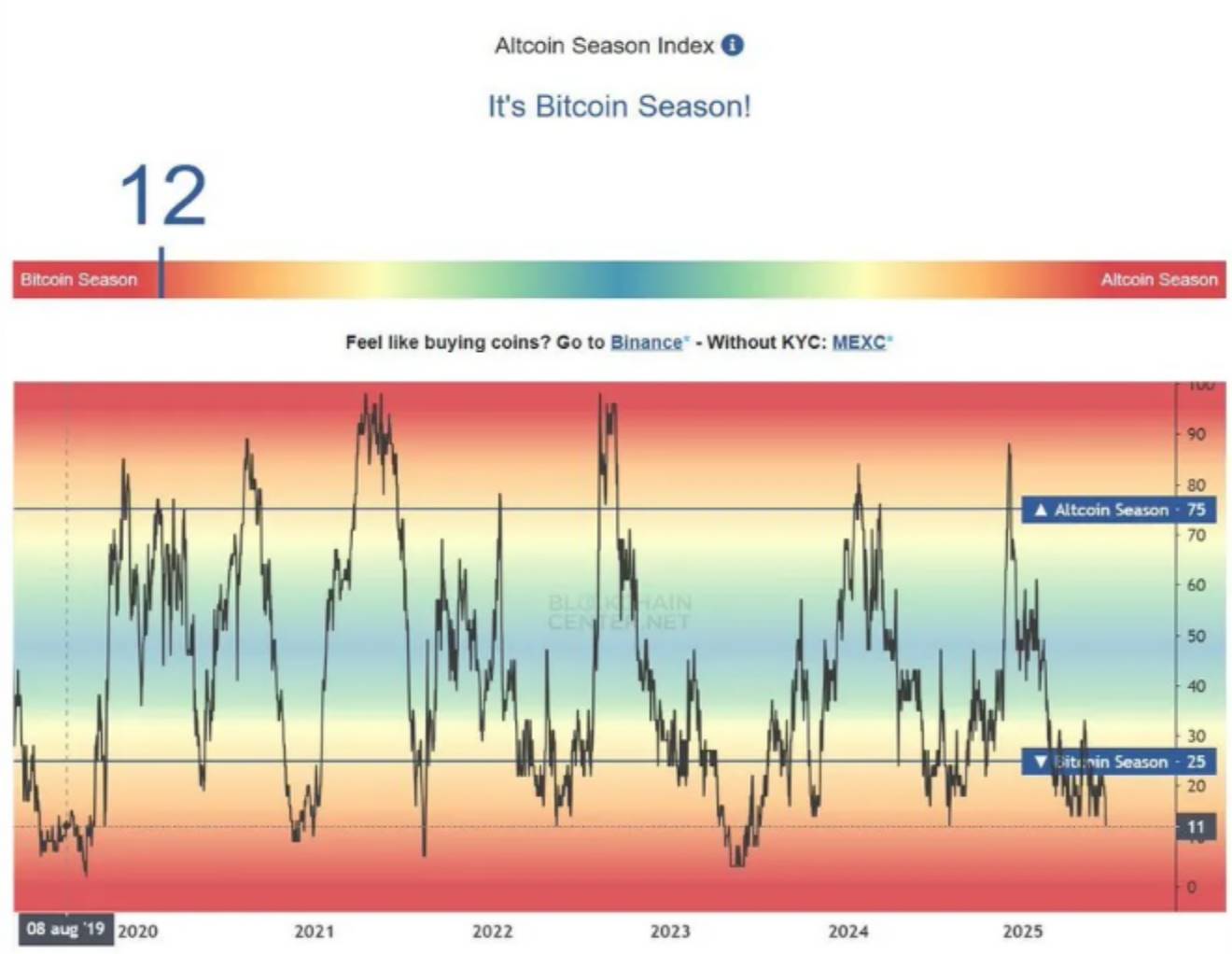

3. Altseason Reimagined: From Broad Rallies to Selective Bull Markets

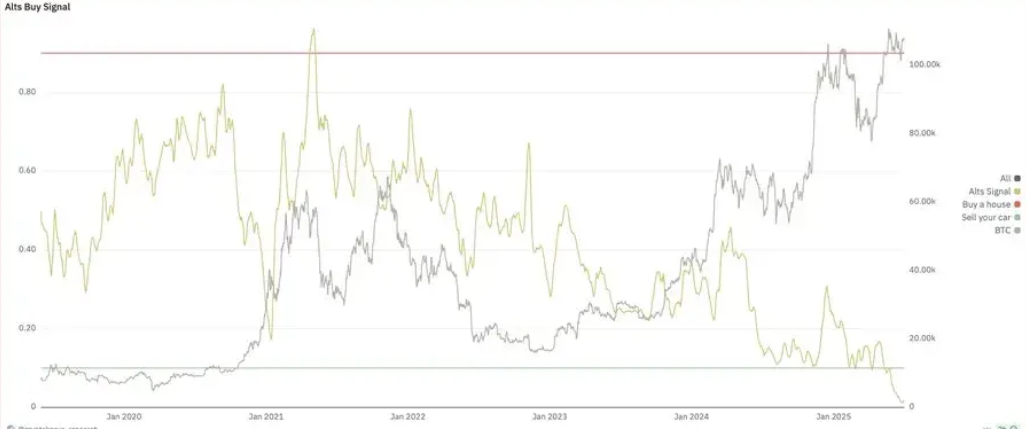

When people think of “altseason,” they often recall the widespread euphoria and universal rallies of 2021. But in 2025, the market’s evolution has quietly changed course—the idea that “altcoin gains = everything rises together” no longer holds. Today’s altseason is entering a new phase: broad rallies are gone, replaced by a “selective bull market” driven by narratives such as ETFs, real yields, and institutional adoption. This reflects the maturation of the crypto market and the inevitable outcome of capital screening mechanisms returning to rationality.

Structurally, leading altcoins have completed a new round of consolidation. After weeks of declines, the ETH/BTC ratio has seen its first strong rebound, with whale addresses accumulating over a million ETH in a short time and large on-chain transactions becoming frequent—indicating that institutional capital has started repricing top-tier assets like Ethereum. At the same time, retail sentiment remains low, with search indices and wallet creation volumes yet to recover significantly. Yet this creates an ideal “low-noise” environment: without overheated emotions or explosive retail participation, the market becomes easier for institutions to steer. Historically, it is precisely during these ambiguous phases—neither clearly rising nor fully stable—that the largest trend opportunities emerge.

But unlike previous cycles, this alt rally won’t be “rising together”—it’ll be “each flying their own path.” ETF applications have become the new anchor for thematic structure. Solana’s spot ETF, in particular, is now viewed as the next “market consensus event.” From the launch of Ethereum staking ETFs to debates over whether Solana’s staking rewards will be included in ETF dividends, investors are already positioning around yield-generating assets. Governance tokens like JTO and MNDE are beginning to follow independent price trajectories. In this new narrative cycle, asset performance will hinge on questions like: “Does it have ETF potential? Can it generate real yield distributions? Will it attract institutional allocations?” No longer will a single wave lift all boats—instead, we’ll see a divergent evolution where strength begets strength and weak projects get culled.

DeFi is another key arena in this “selective bull market,” though its logic has fundamentally shifted. Users are transitioning from “points-and-airdrop farming” to “cash-flow-oriented DeFi,” with protocol revenue, stablecoin yield strategies, and restaking mechanisms becoming central valuation metrics. Liquidity providers no longer blindly chase high APY lures but prioritize transparency, yield sustainability, and underlying risk profiles. This shift has fueled the rise of projects like Renzo, Size Credit, and Yield Nest—entities that grow not through marketing hype but through innovative structured yield products and fixed-rate vaults attracting sustained capital inflows.

Capital itself is becoming increasingly “realist” in its choices. On one hand, stablecoin strategies backed by real-world assets (RWA) are gaining institutional favor, with protocols like Euler Prime aiming to build on-chain equivalents of “government bonds.” On the other, cross-chain liquidity integration and seamless user experience are becoming decisive factors in capital allocation. Middle-layer projects like Enso, Wormhole, and T1 Protocol are emerging as new liquidity hubs thanks to frictionless bridging and embedded DeFi capabilities. In short, in this era of selective bull markets, Layer 1 blockchains no longer dominate trends—rather, the infrastructure and composable protocols built atop them become the new centers of valuation.

Even speculative segments are shifting direction. Meme coins retain popularity, but the era of “everyone pumping together” is over. Instead, “platform rotation trading” strategies are rising—such as Binance-listed meme contracts that rely on rapidly turning negative funding rates followed by sharp sell-offs. These carry extremely high risk and lack sustainability. This indicates that even as speculative themes persist, mainstream capital interest has clearly shifted. Investors now prefer projects offering sustainable yields, genuine user bases, and strong narratives—even if it means sacrificing explosive returns—for more predictable growth paths.

In summary, the defining feature of this altseason isn’t “which L1 will take off,” but “which assets can integrate into traditional financial logic.” From ETF structural changes and restaking yield models to simplified cross-chain UX and the fusion of RWA with institutional credit infrastructure, the crypto market is entering a deep cycle of value revaluation. Selective bull markets aren’t weaker bull runs—they’re upgraded ones. The future no longer belongs to greater fool games, but to those who understand narrative logic, grasp financial architecture, and are willing to quietly accumulate positions in “quiet markets.”

4. Q3 Investment Framework: From Core Allocation to Event-Driven Tactics

The market setup for Q3 2025 is no longer about simply betting on “recovery in market sentiment” or “Bitcoin leading alone.” It’s a full-dimensional restructuring of asset composition. As the high-interest-rate era draws to a close and ETF inflows continue to rise, investors must strike a balance between “core stability” and “event-driven localized explosions.” From long-term Bitcoin allocation to thematic trades on Solana ETFs, and rotational strategies in DeFi yield protocols and RWA vaults, a layered, adaptive asset framework has become essential to navigating Q3 volatility.

First, Bitcoin remains the top choice for core holdings. With ETF inflows showing no sign of reversal, corporate treasuries continuing to accumulate, and dovish signals emerging from Fed policy, BTC demonstrates strong downside resilience and capital-attracting power. Standard Chartered’s latest report raised its year-end BTC price target to $200,000—an optimistic forecast, yet one underpinned by compelling logic: corporate buying is becoming the market’s biggest variable, and the “structural accumulation” nature of ETFs has already altered the traditional post-halving price trajectory. Even if Bitcoin hasn’t reached new highs yet, its ownership structure and capital characteristics make it the most stable foundational asset in this cycle.

Within the rotation of major assets, Solana stands out as the most thematically explosive candidate for Q3. Top-tier institutions like VanEck, 21Shares, and Bitwise have filed applications for SOL spot ETFs, with approval windows expected to close around September. With staking mechanisms potentially integrated into ETF structures, SOL’s “quasi-dividend asset” profile is attracting significant pre-positioning capital. This narrative could boost not only SOL itself but also governance tokens within its staking ecosystem, such as JTO and MNDE. From its current level near $150, SOL offers exceptional value and beta elasticity. For capital that missed the early BTC rally, the Solana sector could become a strategic option for both “catch-up” and “leadership” gains.

At the sector level, DeFi portfolios still warrant active rebalancing. Unlike earlier stages focused solely on APY chasing, current focus should center on protocols with stable cash flows, real yield distribution capabilities, and mature governance. Projects such as SYRUP, LQTY, EUL, and FLUID can serve as configurable options, using equal-weight allocation to capture relative outperformance and reinvest profits cyclically. Importantly, these protocols often exhibit “slow capital return” and “delayed breakout” characteristics, so they should be approached with a medium-term mindset, avoiding knee-jerk reactions to short-term price swings. Especially when Bitcoin dominance remains high and mainstream sentiment hasn’t fully rotated to alts, DeFi assets are better suited as structural reinforcements rather than tactical speculations.

For speculative allocations, meme assets should have strictly controlled exposure. It is recommended to limit them to less than 5% of total net assets, managed with an options-like mindset. Given that current meme contracts are largely manipulated by high-frequency traders—offering high risk alongside rare high-return opportunities—clear stop-loss rules, take-profit thresholds, and position caps should be established. Contracts on major exchanges like Binance (e.g., $BANANAS31, $TUT, $SIREN), which often spike briefly amid highly negative funding rates and sharp pullbacks, require a “quick in, quick out” strategy. For event-driven traders, these can act as sentiment hedges—but never mistaken as core trend drivers.

Beyond allocation, another key to Q3 lies in timing event-driven plays. The market is transitioning from an “information vacuum” to a period of “dense event releases.” Trump’s renewed support for crypto mining and criticism of Fed Chair Powell have accelerated expectations of policy shifts. The passage of the One Great America Act, Robinhood’s L2 launch on Arbitrum Orbit, and Circle’s U.S. license application collectively signal rapid changes in the U.S. regulatory landscape. With the Solana ETF review timeline approaching, the market is likely to enter a phase of “policy-capital resonance” from mid-August to early September. Positioning for such events shouldn’t wait until the “good news is confirmed”; instead, investors should anticipate and gradually build positions to avoid FOMO traps.

In addition, structural alternative themes deserve attention for breakout potential. For instance, Robinhood’s L2 development and push into tokenized stock trading could ignite a new narrative around “exchange chains” and RWA integration. Projects like $H (Humanity Protocol) and $SAHARA (AI + DePIN convergence), supported by verifiable roadmaps and active communities, might become breakout stars in niche sectors. For investors capable of deep roadmap analysis, early opportunities in such projects can form part of high-volatility strategies—but always with strict position control and risk management.

Overall, Q3 2025 investment strategy must abandon the “flood-the-field” approach in favor of a hybrid model: “core as anchor, events as wings.” Bitcoin is the anchor, SOL the flagbearer, DeFi the structure, memes the supplement, and events the accelerant—each component requiring distinct allocation weights and trading rhythms. In this new environment of ever-expanding ETF capital foundations, the market is quietly reshaping a new valuation system based on “mainstream assets + thematic narratives + real yields.” Success will no longer depend on luck, but on whether investors can decode the capital logic behind this transformation.

5. Conclusion: The Next Wealth Migration Is Already Underway

Every bull-bear cycle is essentially a periodic reshuffling through value revaluation—and true wealth migration rarely occurs during the market’s loudest moments, but quietly takes place amid confusion. At this pivotal juncture, although the market hasn’t yet returned to mass euphoria, a selective bull market—led by institutions, driven by compliance, and backed by real yields—is brewing. In short, the prologue has already been written; only those few who understand it need to step in.

Bitcoin’s role has fundamentally changed. It is no longer just a symbol of youth speculation but is evolving into a new reserve component on global corporate balance sheets and a national-level inflation hedge. Over the past year, from Tesla and MicroStrategy to Bitmine and Square, more and more companies have added it to their core holdings. Meanwhile, ETF inflows in the U.S. have transformed the old “miner-exchange-retail” ownership structure, forming a foundational capital reservoir. The biggest influence on Bitcoin’s future price won’t come from viral posts on X, but from institutional purchase records in quarterly earnings reports, allocation decisions by pension funds and sovereign wealth funds, and macro policy shifts that reprice risk asset valuations.

At the same time, next-generation financial infrastructure and assets are slowly but surely evolving from “narrative bubbles” to “systemic adoption.” Solana, EigenLayer, L2 rollups, RWA vaults, restaking bonds—they represent a broader trend: crypto assets are transforming from “anarchic capital experiments” into “predictable institutional assets.” These structural opportunities will guide the next tide of capital. Make no mistake: this isn’t the continuation of a get-rich-quick game, but a pricing revolution crossing asset boundaries. The past belonged to PC internet and U.S. equities; the future belongs to on-chain collaboration and digital property rights.

Altseason hasn’t returned—it has evolved. The 2021-style meme-driven, play-to-earn-linked “universal rally” won’t repeat. The next cycle will be deeply anchored in three pillars: real yield, user growth, and institutional integration. Protocols that offer institutions stable yield expectations, assets that attract steady capital via ETF channels, and DeFi projects with genuine RWA mapping capabilities that connect to real-world scale will become the “blue chips” of the new era. This is the elitization of alts—a selective bull market that eliminates 99% of fake assets.

For ordinary investors, challenges and opportunities coexist. The surface appearance of the market remains stagnant—low heat, fragmented sectors, weak sentiment, poor momentum—but this is precisely the golden period when large capital quietly builds positions. When the market starts asking “where’s the next breakout point?”, you should instead ask: “am I positioned on the right structure?” It’s not random gambles, but portfolio restructuring, that determines whether you’ll capture the profits of the main uptrend.

Whether it’s institutional absorption of Bitcoin, the Solana ETF narrative, rebuilding DeFi’s cash flow valuation system, or the global wave of stablecoins and the establishment of a new L2 order, Q3 2025 will serve as the prelude to this wealth migration. You may not have noticed it yet—but it has already begun. You may still be waiting—but opportunity never waits.

The next bull market won’t ring bells for anyone. It will only reward those who started thinking ahead of the crowd. Now is the time to seriously plan your portfolio structure, information sources, and trading rhythm. Wealth isn’t distributed at the climax—it shifts quietly before dawn.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News