TechFlow: Buying MSTR stock at a 75% premium instead of $100,000 in Bitcoin—has Wall Street gone crazy?

TechFlow Selected TechFlow Selected

TechFlow: Buying MSTR stock at a 75% premium instead of $100,000 in Bitcoin—has Wall Street gone crazy?

Investors buying MSTR stock are not only purchasing bitcoin, but also acquiring the "ability to continuously accumulate bitcoin in the future."

Author: Will Owens, Galaxy

Translation: AididiaoJP, Foresight News

Companies holding bitcoin on their balance sheets have become one of the most closely watched narratives in public markets in 2025. Although investors already have multiple direct ways to gain exposure to bitcoin (ETFs, spot bitcoin, wrapped bitcoin, futures contracts, etc.), many still choose to gain bitcoin exposure by purchasing shares of bitcoin-reserve companies trading at a significant premium to their net asset value (NAV) in bitcoin.

This premium refers to the difference between a company's stock price and the per-share value of its bitcoin holdings. For example, if a company holds $100 million worth of bitcoin and has 10 million shares outstanding, its per-share bitcoin NAV is $10. If the stock trades at $17.50, the premium stands at 75%. In this context, mNAV (multiple of NAV) indicates how many times the stock price exceeds the bitcoin NAV, while the premium rate is the percentage equivalent of mNAV minus 1.

Ordinary investors might wonder: why can these companies be valued so far above the intrinsic value of their bitcoin assets?

Leverage and Access to Capital

The most important reason for the premium of bitcoin-reserve companies over their underlying bitcoin assets may lie in their ability to leverage public capital markets. These companies can raise funds through bond and stock issuance to purchase more bitcoin. Essentially, they act as high-beta proxies for bitcoin, amplifying sensitivity to market volatility.

The most commonly used and effective tool in this strategy is the "at-the-market" (ATM) equity offering program. This mechanism allows companies to gradually issue new shares at prevailing market prices with minimal market impact. When the stock trades at a premium to bitcoin NAV, each dollar raised via an ATM offering can buy more bitcoin than the dilution caused by issuing new shares. This creates a “per-share bitcoin growth loop,” continuously expanding bitcoin exposure on a per-share basis.

Strategy (formerly MicroStrategy) is the prime example of this approach. Since 2020, the company has raised billions of dollars through convertible debt and secondary equity offerings. As of June 30, Strategy holds 597,325 bitcoins (approximately 2.84% of circulating supply).

Such financing tools are only available to public companies, enabling them to continuously accumulate bitcoin. This not only magnifies bitcoin exposure but also creates a compounding narrative effect—each successful fundraising and subsequent bitcoin purchase reinforces investor confidence in the model. Therefore, investors buying MSTR stock aren't just buying bitcoin; they're buying into the "ability to continuously accumulate more bitcoin in the future."

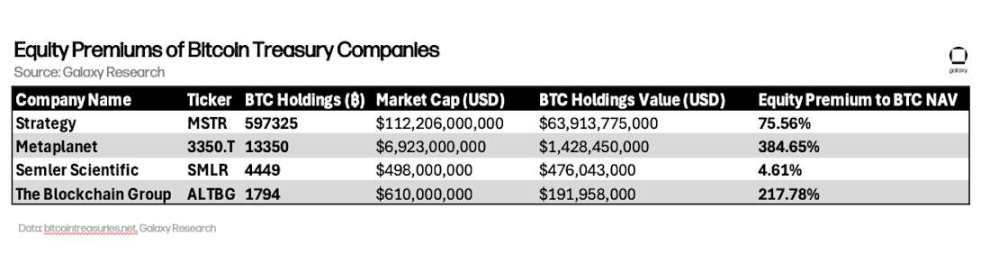

How Large Are the Premiums?

The table below compares the premium levels of select bitcoin-reserve companies. Strategy is the world’s largest publicly listed holder of bitcoin and the best-known player in this space. Metaplanet is the most aggressive accumulator of bitcoin (and will be discussed later for its transparency advantages). Semler Scientific was an early adopter, beginning bitcoin purchases last year. Meanwhile, France’s The Blockchain Group shows this trend is spreading globally beyond the U.S.

Premiums to NAV for selected bitcoin-reserve companies (as of June 30; assuming BTC price of $107,000):

While Strategy’s premium is relatively modest (~75%), smaller firms like The Blockchain Group (217%) and Metaplanet (384%) exhibit significantly higher premiums. These valuations suggest that market pricing reflects not only the growth potential of bitcoin itself, but also factors such as access to capital markets, speculative upside, and narrative value.

Bitcoin Yield: A Key Metric Behind the Premium

One core metric driving the stock premiums of these companies is “bitcoin yield.” This measures the growth in bitcoin holdings per share over a given period, reflecting how efficiently a company uses its fundraising capacity to accumulate bitcoin without excessive equity dilution. Metaplanet stands out for its transparency, offering a [real-time bitcoin dashboard] on its website that dynamically updates its bitcoin holdings, bitcoin per share, and bitcoin yield.

Source: Metaplanet Analytics (https://metaplanet.jp/en/analytics)

Metaplanet publishes proof-of-reserves, a practice not yet adopted by its peers. For instance, Strategy does not use any on-chain verification to prove its bitcoin holdings. At the "Bitcoin 2025" conference in Las Vegas, [Executive Chairman Michael Saylor explicitly opposed] public proof-of-reserves, calling it a “bad idea” due to security risks: “It weakens the security of issuers, custodians, exchanges, and investors.” This view is controversial—on-chain proof-of-reserves requires only sharing public keys or addresses, not private keys or signature data. Given Bitcoin’s security model is based on the principle that public keys can be safely shared, revealing wallet addresses does not compromise asset security (this is precisely a feature of the Bitcoin network). On-chain proof-of-reserves gives investors a direct way to verify the authenticity of a company’s bitcoin holdings.

What Happens If the Premium Disappears?

The high valuations of bitcoin-reserve companies have so far existed in a bull market environment characterized by rising bitcoin prices and strong retail enthusiasm. No bitcoin-reserve company has ever traded below its NAV for an extended period. The viability of this business model depends on the persistence of the premium. As [VanEck analyst Matthew Sigel noted]: “When the stock price falls to NAV, equity dilution ceases to be strategic and becomes value extraction.” This statement cuts to the core vulnerability of the model—the ATM equity issuance programs (the capital engine powering these companies) fundamentally rely on stock price premiums. When the share price exceeds per-share bitcoin value, equity fundraising increases per-share bitcoin exposure. But when the price falls toward NAV, equity issuance begins to erode rather than enhance shareholder bitcoin exposure.

The model depends on a self-reinforcing cycle:

-

Stock price premium supports fundraising capacity

-

Funds raised are used to buy more bitcoin

-

Bitcoin accumulation strengthens the company’s narrative

-

Narrative value sustains the stock price premium

If the premium disappears, the cycle breaks: funding costs rise, bitcoin accumulation slows, and narrative value weakens. Currently, bitcoin-reserve companies still enjoy access to capital markets and strong investor sentiment. However, their long-term success will depend on financial discipline, transparency, and the ability to grow bitcoin per share—not merely total bitcoin holdings. The “optionality value” that makes these stocks attractive in a bull market could quickly turn into a liability during a bear market.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News