From Retail Paradise to Financial Disruptor: A Deep Dive into Robinhood's Business Landscape and Future Strategy

TechFlow Selected TechFlow Selected

From Retail Paradise to Financial Disruptor: A Deep Dive into Robinhood's Business Landscape and Future Strategy

Analyze the evolution of Robinhood's business model, the logic behind its core strategy, and project its future impact on the industry market.

By: Aiying Compliance

On June 30, 2025, Robinhood's stock surged more than 12% during trading, hitting an all-time high. The market frenzy was not solely due to a strong earnings report, but rather driven by a series of major announcements made in Cannes, France: launching a stock tokenization product, building its own Layer 2 blockchain based on Arbitrum, and offering perpetual contracts to EU users... These moves mark a fundamental shift in how the market perceives Robinhood—no longer just a "retail trading app" for young investors, but a potential "disruptor of financial infrastructure."

Aiying (Aiying) is a compliance consulting team with hands-on experience in both corporate and client-side legal and operational roles, deeply understanding the balance between regulatory compliance and real-world business models. This article primarily explores how Robinhood’s business model has evolved. What is its current strategic core—especially its deep commitment to RWA (Real World Assets) and cryptocurrency technology—and how will this reshape its own value while bringing profound impacts to traditional finance and the crypto industry? We will analyze Robinhood from three dimensions—"yesterday, today, tomorrow"—to dissect the evolution of its business model, the logic behind its core strategy, and project its future influence on the market landscape.

I. Yesterday: From "Zero Commissions" to "Diversification"—Rampant Growth and Transition Pains

This section provides a quick review of Robinhood’s rise and initial business model construction, setting the stage for understanding its current strategic transformation.

1. Founding Vision and User Positioning

Robinhood's story began with two Stanford University graduates from physics and mathematics backgrounds—Baiju Bhatt and Vladimir Tenev. Their experience developing low-latency trading systems for hedge funds led them to realize that institutional-grade technology could also serve retail investors. True to its namesake "Robin Hood," their founding mission was "financial democratization"—providing ordinary people with the same investment opportunities as institutions. This vision resonated strongly with millennials’ distrust toward big banks in the aftermath of the 2008 financial crisis.

Riding the mobile internet wave, they launched a mobile-first app in 2014. Its two disruptive innovations were:

-

Zero-commission trading: completely breaking the traditional brokerage fee model and dramatically lowering the barrier to entry.

-

Exceptional user experience: a clean, even "addictive" interface design—such as confetti animations after trades—that gamified complex financial transactions, attracting many inexperienced young investors.

Thanks to this precise positioning, Robinhood had already accumulated 800,000 users on its waitlist before officially launching in 2015, achieving viral growth and ushering in a new era for young investors.

2. Building the Core Business Model and Controversies

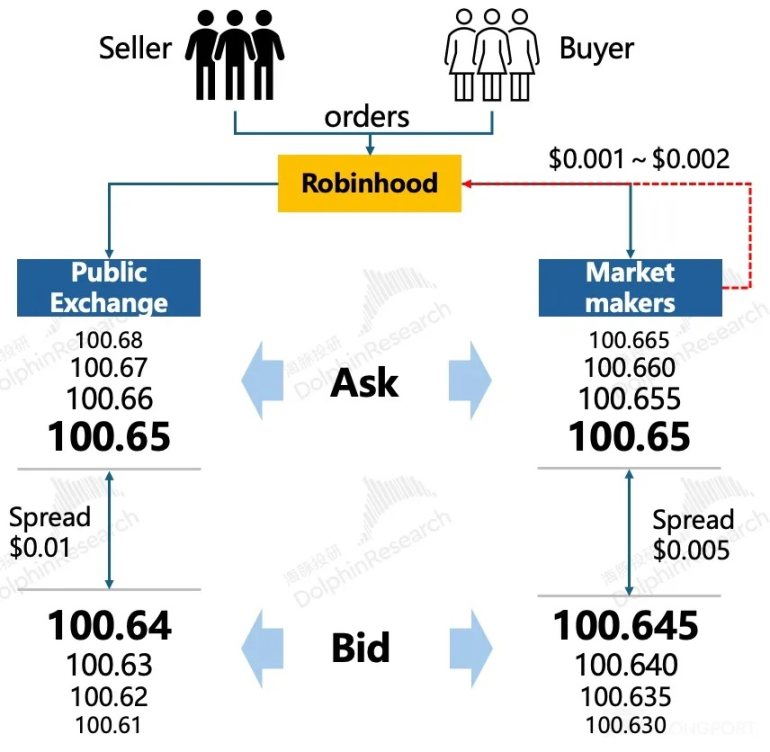

"Zero commissions" wasn't free. Behind it lay Robinhood’s carefully constructed diversified revenue model, most notably—and controversially—PFOF.

PFOF (Payment for Order Flow)

PFOF is the cornerstone enabling Robinhood’s "zero commissions." In short, instead of routing user orders directly to exchanges, Robinhood bundles and sells them to high-frequency market makers like Citadel Securities. These market makers profit from tiny spreads and pay Robinhood a portion in return. According to research data, in Q2 2024, Robinhood held about 20% of the stock PFOF market and a dominant 35% share in options PFOF. While highly profitable, this model has sparked long-standing regulatory scrutiny over whether Robinhood sacrifices best execution prices for users' benefit.

Diversification Efforts

Beyond PFOF, Robinhood expanded into multiple business lines, forming three main revenue pillars:

-

Trading business: expanding rapidly from stocks to options (2017) and cryptocurrencies (2018). Data shows that options and crypto—both high-volatility assets—generate significantly higher trading revenue than stocks, reflecting users’ appetite for high-risk, high-return investments.

-

Interest income: through margin lending and cash management services, Robinhood converts users’ idle funds and leverage demand into stable interest income, now its second-largest revenue source, especially valuable in high-interest-rate environments.

-

Subscription services: Robinhood Gold, launched in 2016, offers premium features such as instant deposits and pre-market/post-market trading. By Q1 2025, Gold subscribers surpassed 3.2 million, marking Robinhood’s early transition from a pure trading platform to a “financial SaaS” model focused on enhancing user stickiness and revenue stability.

3. Growing Pains: Crises and Reflections

Rapid growth inevitably brought growing pains. Robinhood faced numerous crises throughout its journey:

-

Technical and risk control failures: In March 2020, during a historic surge in U.S. equities, Robinhood’s platform crashed all day, triggering mass lawsuits. Later that year, a 20-year-old user died by suicide after misunderstanding his options account balance, exposing serious deficiencies in user education and risk warnings beneath the “gamified” interface.

-

GME incident and trust crisis: The GameStop event in early 2021 marked a turning point in its reputation. At the height of retail investors battling Wall Street, Robinhood abruptly restricted purchases of GME and other popular stocks, accused of “pulling the plug” and betraying retail traders. Though officially explained as meeting clearinghouse margin requirements, the label of “stealing from the poor to enrich the rich” stuck, undermining its foundational principle of “financial democratization.”

-

Ongoing regulatory pressure: From FINRA fines related to PFOF to SEC investigations into its crypto operations, regulation remains a Damocles sword hanging over Robinhood.

These crises collectively revealed Robinhood’s vulnerabilities: unstable technology platforms, flawed risk controls, and inherent conflicts between its business model and user interests. It was precisely these painful lessons that forced Robinhood to seek a new growth narrative and strategic direction—to move beyond the label of “meme stock playground” and rebuild market trust.

II. Today: All in Crypto—Robinhood’s Strategic Ambition and Business Logic

This section forms the core of the article, providing an in-depth analysis of Robinhood’s current strategic focus on RWA and cryptocurrency technology, unpacking the underlying business logic and competitive advantages.

1. Core of the Strategic Shift: Why RWA and Stock Tokenization?

Robinhood’s bet on RWA and crypto technology is no passing trend, but stems from deep financial drivers and strategic considerations.

“We have the opportunity to show the world what we’ve always believed—that cryptocurrency is far more than just a speculative asset. It has the potential to become a cornerstone of global finance.” — Vladimir Tenev, Robinhood CEO

Financial Driver: The Profit Engine

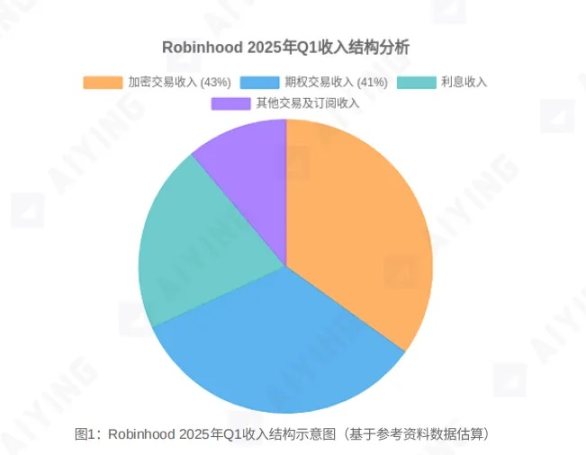

Financial reports show that crypto has become Robinhood’s most profitable segment. In Q1 2025, crypto trading generated $252 million in revenue, accounting for 43% of total trading revenue—surpassing options for the first time as the top contributor. More importantly, its margins are staggering: according to analysis, the rebate rate from crypto order flow is 45 times that of stocks and 4.5 times that of options. Fueled by both growth and profitability, going “all in crypto” became inevitable.

Narrative Upgrade: From Broker to “Bridge”

This move elevates Robinhood from a controversial “retail broker” to a “bridge connecting traditional finance (TradFi) and the on-chain world.” Not only does it help escape the regulatory shadow of PFOF and the cyclical stigma of “meme stocks,” but it also positions the company to enter a multi-trillion-dollar market—the digitization and tokenization of vast real-world assets.

Core Goal: Disrupting Traditional Financial Infrastructure

In correspondence submitted to the U.S. Securities and Exchange Commission (SEC), Robinhood clearly articulated its vision for RWA tokenization. They argue that blockchain technology can enable the following—aimed at fundamentally overturning the inefficiency, high cost, and access barriers of the current securities trading system:

-

24/7 trading: breaking down time barriers imposed by traditional exchanges.

-

Near-instant settlement: moving from T+2 to T+0, significantly reducing counterparty risk and operational costs.

-

Unlimited divisibility of ownership: allowing high-value assets (e.g., real estate, art) to be fractionalized, lowering investment thresholds.

-

Enhanced liquidity: creating broader markets for traditionally illiquid assets (e.g., private equity).

-

Automated compliance: embedding regulatory rules via smart contracts to reduce compliance overhead.

2. A Triad Strategy: How Will Goals Be Achieved?

To achieve this grand vision, Robinhood has deployed a “three-pronged” strategic approach, moving from application layer down to infrastructure layer.

Stock Tokenization (Stock Token)

This serves as the “entry point” for its RWA strategy. By launching tokenized U.S. stocks in the EU market—with 24/5 trading and dividend support—Robinhood is conducting large-scale market education and technical validation. This aims to bridge traditional assets with the on-chain world, enabling conventional investors to seamlessly enter the crypto ecosystem.

Building a Custom L2 Chain (Robinhood Chain)

This is Robinhood’s most ambitious strategic move. By building its own Layer 2 chain optimized for RWA using the Arbitrum Orbit tech stack, Robinhood is evolving from an “application” into an “infrastructure provider.” Owning its own public chain means controlling rule-making power and ecosystem dominance. In the future, issuance, trading, and settlement of all tokenized assets will occur within this closed-loop ecosystem, establishing formidable technological and commercial moats.

Platformization (Broker-as-a-Platform)

Through acquisitions (e.g., Bitstamp, WonderFi) and new product launches (e.g., perpetual contracts, staking services, AI advisor Cortex, credit card crypto cashback), Robinhood is building an “all-in-one investment platform powered by crypto.” Integrating trading, payments, asset management, and infrastructure, it covers the full lifecycle from funding to asset appreciation, aiming to maximize individual user lifetime value (LTV).

3. Comparative Analysis: Robinhood vs. Coinbase & Traditional Brokers

Robinhood’s strategic positioning places it uniquely within the competitive landscape.

vs. Coinbase

-

Divergent paths: Coinbase is an “on-chain exchange,” focusing on native crypto assets and earning institutional trust through compliance. Robinhood, by contrast, is a “securitized broker,” aiming to bring massive traditional assets onto the blockchain.

-

Advantage comparison: Coinbase excels in deep roots in the crypto industry, regulatory expertise, and institutional clientele. Robinhood’s strengths lie in its massive retail user base, superior product experience, and a more aggressive, focused RWA strategy.

vs. Traditional Brokers (Schwab, IBKR)

-

Model differences: Traditional brokers like Charles Schwab and Interactive Brokers primarily serve high-net-worth individuals and institutions, relying more on interest and advisory fees. Robinhood targets younger, active retail traders whose revenue depends heavily on trading fees—especially in crypto.

-

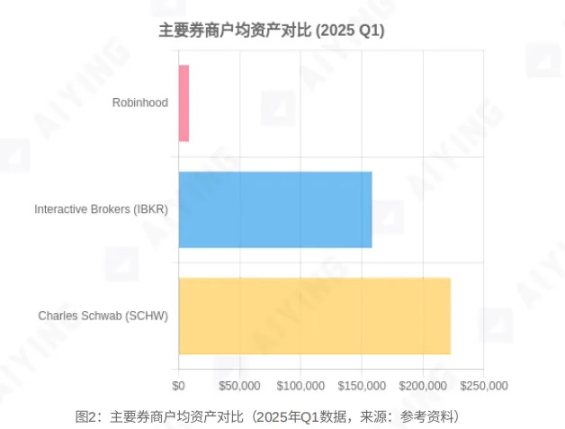

Data comparison: Third-party data indicates Robinhood now exceeds two-thirds of Schwab’s account count, yet its average user capital (AUC) is only about 2% of Schwab’s. This represents both a weakness and a growth opportunity. Recent products like IRA retirement accounts and credit cards aim to increase user asset size and loyalty, encroaching on traditional brokers’ turf. In terms of trading revenue growth—particularly in crypto—Robinhood has far outpaced legacy firms.

III. Tomorrow: The "First Gateway" to Reshaping Financial Order? Opportunities and Risks Coexist

Based on the above analysis, Aiying evaluates the potential market impact and internal challenges facing Robinhood’s future trajectory.

1. Potential Impact on Financial Market Structure

-

Squeezing liquidity from altcoins: when investors can trade compliant, convenient blue-chip stock tokens (e.g., OpenAI, SpaceX) backed by real value, demand for high-risk, fundamentals-lacking altcoins and meme coins may drastically decline. The crypto market could further split into “mainstream coins via ETFs” and “infrastructure coins linking to TradFi,” leaving many altcoins marginalized.

-

Reshaping stock trading rules: 24/7 trading will dismantle traditional pre- and post-market boundaries, profoundly affecting global liquidity distribution, price discovery mechanisms, and market maker strategies. The question “Will you watch Nasdaq or Robinhood for pre-market action?” may evolve from a joke into a serious consideration.

-

Accelerating TradFi giants’ entry: Robinhood’s bold moves act as a “catfish,” stirring up the entire traditional finance sector. Its experimentation will force JPMorgan, Goldman Sachs, and others to accelerate their own tokenization initiatives, sparking a new fintech arms race.

2. Robinhood’s Own Opportunities and Valuation Reconfiguration

If successful, Robinhood stands to gain immense opportunities.

Becoming the RWA “First Gateway”: With its massive user base and leading product experience, Robinhood has the potential to become the central hub connecting trillions of dollars in real-world assets with the crypto ecosystem. It would capture dual generational tailwinds: “intergenerational wealth transfer” (an estimated $84 trillion shifting from baby boomers to millennials) and “crypto adoption.”

Shift in valuation anchor: its valuation logic is undergoing a qualitative change. No longer seen merely as a cyclical brokerage subject to trading volume and interest rates, Robinhood is transforming into a hybrid entity combining SaaS (Gold subscriptions), fintech (platform effects), and infrastructure (public chain value). This multidimensional business model vastly expands its growth ceiling, requiring entirely new valuation frameworks from the market.

3. Persistent Risks and Challenges

Robinhood’s grand vision faces significant hurdles:

-

Regulatory uncertainty: the biggest bottleneck. In its letter to the SEC, Robinhood explicitly highlighted existing regulatory obstacles: How should RWA tokens be legally classified? How can brokers meet digital asset custody rules (e.g., Rule 15c3-3)? How to calculate capital requirements for digital assets (Rule 15c3-1)? Despite a seemingly friendlier political climate toward crypto in the U.S., any regulatory shift could deliver a fatal blow.

-

Execution and competition risks: building an L2 chain, integrating Bitstamp, and executing global expansion each demand exceptional project management and execution capabilities. Meanwhile, competition from native crypto players like Coinbase and Kraken, and awakened TradFi titans like Goldman Sachs and JPMorgan, will be fierce. As the saying goes, “execution determines survival.” Robinhood must prove it can deliver, not just dream.

-

Inherent business model fragility: despite increasing diversification, its revenue remains heavily reliant in the short term on volatile trading activities, particularly crypto. This means its performance will still be subject to market cycles. Balancing disruptive innovation with the development of more stable, predictable revenue streams is key to long-term health.

Conclusion: A Blueprint for the Evolution of Old and New Finance

Looking back at Robinhood’s journey, it is no longer just a “retail toy” grabbing attention with “zero commissions” and “gamification.” Through a bold bet centered on RWA and crypto technology, it is attempting to move from the periphery to the center of the financial system—becoming a “institutional designer” and “infrastructure provider” at the intersection of old and new financial orders.

Its ambitions extend far beyond surface-level features like 24-hour trading or instant settlement. It seeks a fundamental restructuring of the entire system for asset issuance, trading, and settlement—transforming the closed, expensive, inefficient rules of traditional finance into an open, programmable, composable new financial logic.

The success or failure of this transformation will not only determine Robinhood’s fate but also significantly shape the evolution path of global financial markets over the next decade. For investors and observers alike, Robinhood is no longer just a stock ticker—it is a dynamic “blueprint” revealing the infinite possibilities of future finance. Volatility will persist, but the space for institutional arbitrage has only just begun to open.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News