JPMD is not just a technological upgrade; it also introduces a new class of digital assets in the form of tokenized bank deposits.

Authors: Zhou Hao, Sun Yingchao

(Zhou Hao is Chief Economist at Guotai Junan International and a member of the China Chief Economists Forum)

JPMorgan Chase has quietly filed a trademark application for "JPMD," sparking interest in both the financial and crypto industries. Unlike speculative token launches or experimental pilots, this move signals that the world's largest bank is rapidly advancing into digital finance. However, JPMD is not a stablecoin.

Investors tend to view this as a strategic bet on blockchain infrastructure. Backed by regulated deposits and piloted on public blockchains, JPMD could serve as a blueprint for how traditional institutions can embrace decentralized rails without sacrificing compliance, stability, or control.

JPMD is a blockchain-based form of customer deposits that operates seamlessly within existing banking infrastructure. Essentially, JPMD tokens are issued to represent institutional clients’ U.S. dollar deposits held at JPMorgan. These tokens can be transferred, traded, or used for payments across supported blockchain networks.

JPMorgan chose Base—a Layer-2 blockchain developed by Coinbase—for its pilot, involving the transfer of a fixed amount of JPMD to Coinbase to test institutional transfers. Upon successful completion, selected institutional clients will gain access to real-time transactions. Industry insiders interpret this move as JPMorgan’s strategic shift from permissioned chains to public blockchains, suggesting that permissioned blockchains and permissioned distributed ledger technologies (DLTs) may have reached a dead end in certain areas of innovation and product development.

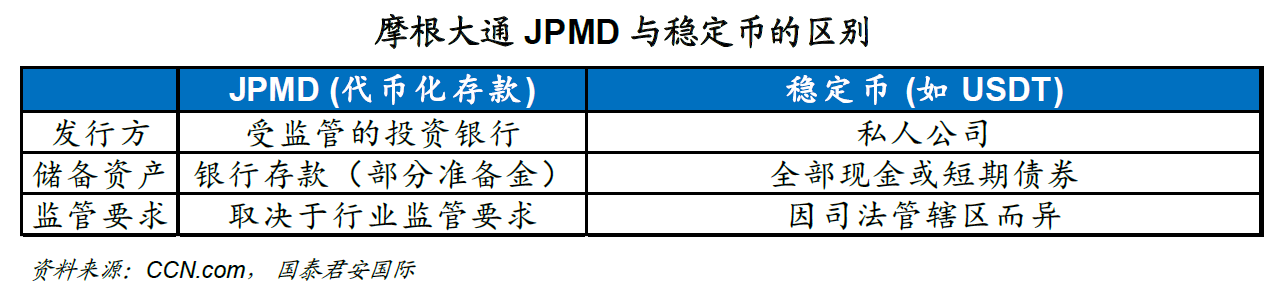

It is crucial to understand the difference between deposit tokens and stablecoins. Stablecoins like USDT are typically backed 1:1 by cash or equivalents and issued by private companies. They aim to maintain stable value and are widely used in crypto trading and DeFi. Deposit tokens, on the other hand, are directly issued by regulated banks, backed by fractional reserves (like traditional bank deposits), and designed for integration with the banking system. Institutional experts highlight regulatory advantages as key. A potential advantage of JPMD over Circle is that JPMorgan is a bank—and a major one—with decades of operational and regulatory experience, understanding core banking services such as balance management. Thus, from a technical perspective, what makes JPMD truly interesting is the innovation it brings in risk management, operations, and product development from the world’s largest bank.

From a broader trend standpoint, JPMD is more than just a technological upgrade—it introduces a new class of digital assets in the form of tokenized bank deposits. Positioned as a trusted and compliant gateway to blockchain-based finance, it offers institutions a way to participate in digital assets while maintaining regulatory standards. Ultimately, it could become a model for how traditional finance can adopt blockchain innovation without compromising security or oversight. If JPMorgan successfully scales JPMD beyond the pilot phase, it may lead a transformation—meaning banks, payments, and capital markets begin to exist securely and legally on-chain.

In the longer term, the convergence between institutional finance and decentralized infrastructure is already underway. As more digital financial tools integrate with digital technologies—such as an increasing number of tokenized assets being built on the Solana ecosystem—staking services like Marinade will become part of TradFi’s validation and infrastructure layer. This also implies that future on-chain financial transactions will become richer and more derivative in nature, while compliance will deepen its integration with traditional finance.

JPMorgan Chase has quietly filed a trademark application for "JPMD," sparking interest in both the financial and crypto industries. Unlike speculative token launches or experimental pilots, this move signals that the world's largest bank is rapidly advancing into digital finance. However, JPMD is not a stablecoin.

Investors tend to view this as a strategic bet on blockchain infrastructure. Backed by regulated deposits and piloted on public blockchains, JPMD could serve as a blueprint for how traditional institutions can embrace decentralized rails without sacrificing compliance, stability, or control.

JPMD is a blockchain-based form of customer deposits that operates seamlessly within existing banking infrastructure. Essentially, JPMD tokens are issued to represent institutional clients’ U.S. dollar deposits held at JPMorgan. These tokens can be transferred, traded, or used for payments across supported blockchain networks.

Unlike stablecoins such as USDC or USDT, JPMD is:

-

Fully integrated into the traditional banking system

-

Backed by real bank deposits held under regulatory supervision

-

Designed specifically for institutional use

Currently, JPMD is available only to institutional users. However, if the pilot proves successful and regulations evolve to support broader adoption, future iterations could enable cross-border commercial payments, treasury management solutions, and programmable settlement for corporate finance. Given current banking regulations, it is unlikely that retail customers will have access to JPMD in the near term.

JPMorgan’s trademark filing outlines a broad range of services associated with JPMD, including:

While not a stablecoin, JPMD encompasses many characteristics associated with fiat-backed digital tokens. This suggests JPMorgan may position JPMD not merely as a payment tool, but potentially as foundational infrastructure for tokenized finance.

From JPM Coin to JPMD

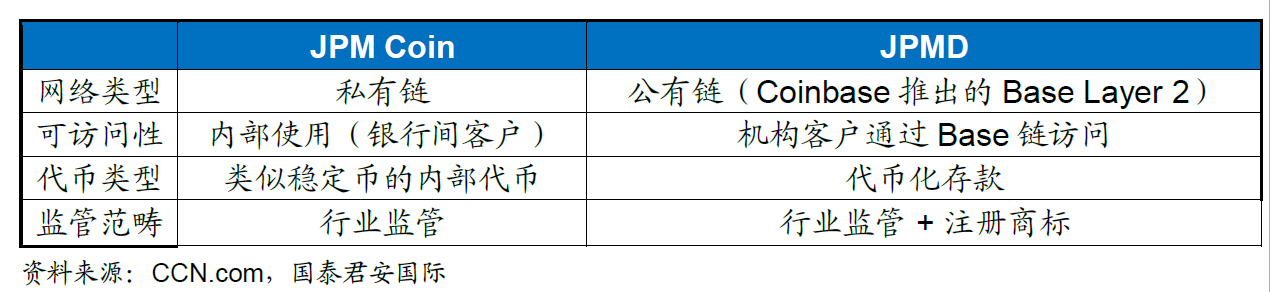

JPMorgan is no stranger to digital tokens. Its JPM Coin, launched in 2019, has already processed over $1.5 trillion in institutional payments on a private blockchain. The key difference with JPMD is its use of public blockchains, enabling broader interoperability.

JPMD extends the concept of JPM Coin by enabling on-chain transfers that interact with a wider blockchain ecosystem, including Ethereum-based applications and institutions operating on Base.

Launching on Base: Why Choose a Layer-2?

JPMorgan’s choice of Base—the Ethereum Layer-2 blockchain developed by Coinbase—reflects a strategic openness. While JPMD is currently confined to JPMorgan’s ecosystem, issuing it on Coinbase’s Base network signals the bank’s intent to expand into broader consumer and commercial payment scenarios in the future. Base is known for:

-

High throughput and low transaction fees

-

Compatibility with Ethereum-based infrastructure

-

Increasing adoption among institutional DeFi projects

By choosing Base, JPMorgan will:

-

Leverage a scalable and secure public blockchain

-

Benefit from Coinbase’s regulatory reputation and user base

-

Explore practical blockchain applications beyond proof-of-concept stages

The pilot involves transferring a fixed amount of JPMD to Coinbase to test institutional transfers. Once completed successfully, select institutional clients will gain access to real-time transactions. Industry observers see this as JPMorgan’s strategic shift from permissioned to public blockchains, indicating that permissioned blockchains and permissioned DLTs may have hit a dead end in certain aspects of innovation and product development.

Permissioned blockchains require identity verification for node participation (e.g., consortium or private chains) and primarily serve enterprise use cases (such as supply chain finance). Permissioned DLT emphasizes “access control,” contrasting with the “decentralized, permissionless” nature of public blockchains like Bitcoin and Ethereum. Fundamentally, blockchain was conceived to solve trust issues through decentralization, whereas permissioned chains retain “centralized oversight” (e.g., administrator privileges), compromising data transparency and censorship resistance—potentially limiting their ability to foster disruptive innovations (such as Web3 or metaverse applications that rely on public chains).

That said, some industry experts argue that permissioned blockchains are not entirely a “dead end.” In specific contexts—such as government services or large-scale enterprise supply chains where compliance and efficiency must be balanced—the controllability of permissioned chains remains advantageous. Their innovation path is shifting toward “efficiency optimization” (e.g., improving TPS) rather than “decentralized disruption.” Meanwhile, there is a growing trend of hybrid models combining permissioned and public blockchains—using permissioned chains for handling private data and public chains for ecosystem connectivity—potentially opening new avenues for product development.

JPMD vs. Stablecoins

Understanding the distinction between deposit tokens and stablecoins is critical. Stablecoins like USDT are typically backed 1:1 by cash or equivalents and issued by private firms. They aim to maintain stable value and are widely used in crypto trading and DeFi. While USDT still dominates in market cap and usage, Circle’s IPO in June 2025 marks its transition from a privately held company to a public one, giving USDC a regulatory and transparency edge—especially in institutional markets.

Deposit tokens, by contrast, are directly issued by regulated banks and backed by fractional reserves (akin to traditional bank deposits), aiming for seamless integration with the banking system. Institutional experts consider this regulatory advantage pivotal. A key advantage of JPMD over Circle is that JPMorgan *is* a bank—a major one—with decades of operational and regulatory experience in managing fundamental banking functions like balance sheets. Therefore, from a technical standpoint, the most compelling aspect of JPMD lies in the innovation it brings to risk management, operations, and product design from the world’s largest financial institution.

Naveen Mallela, head of Kinexys—the blockchain division at JPMorgan—described deposit tokens as “a superior alternative to stablecoins from an institutional perspective.” This is because they offer compliance, scalability, and the potential for interest payments—features largely absent in most current stablecoins.

JPMD’s launch comes shortly after the U.S. Senate approved the GENIUS Act, marking a significant step toward stablecoin regulation. If passed, the bill would introduce clearer rules for digital dollar tokens, including reserve requirements and audit standards.

JPMD and the Future of Digital Finance

The emergence of JPMD is part of a broader trend:

Tokenized assets are gaining momentum: Real-world assets (RWA) such as U.S. Treasuries and bonds are increasingly being tokenized, with firms like BlackRock and Franklin Templeton exploring blockchain for issuance and settlement.

Banks are reversing marginalization: JPMorgan, Citigroup, and others are actively testing digital versions of their services—from tokenized deposits to programmable payments.

Compliance is becoming a competitive advantage: Unlike early crypto projects, institutions now seek regulatory clarity. JPMD sits precisely at the intersection of innovation and regulation.

From these perspectives, JPMD is more than just a technical upgrade—it introduces a new class of digital assets through tokenized bank deposits. It is positioned as a trusted and compliant entry point into blockchain-based finance, offering institutions a pathway to engage with digital assets while upholding regulatory standards. Ultimately, it could become a template for how traditional finance adopts blockchain innovation without sacrificing security or oversight. If JPMorgan successfully expands JPMD beyond the pilot stage, it may spearhead a transformation—ushering in an era where banks, payments, and capital markets securely and legally operate on-chain.

In the longer term, the integration between institutional finance and decentralized infrastructure is already underway. As more digital financial tools converge with digital technologies—such as growing numbers of tokenized assets being built on the Solana ecosystem—services like Marinade will become part of TradFi’s validation and infrastructure layer. Marinade Finance (Marinade) is the leading liquid staking protocol on Solana. Users stake SOL—the native token essential to the Solana blockchain—to receive mSOL. mSOL represents staked SOL plus accrued rewards and can be freely used in DeFi to earn additional yield. It automatically distributes SOL across numerous validator nodes, offering ease of use, strong returns (base staking yield + DeFi opportunities), and support for network decentralization. This implies that future on-chain financial transactions will become richer and more derivative in nature, while compliance will further deepen integration with traditional finance.