Did the Fed's quantitative easing render bear markets meaningless?

TechFlow Selected TechFlow Selected

Did the Fed's quantitative easing render bear markets meaningless?

Market optimism is high, with retail investor confidence nearing historic highs. If the Federal Reserve continues intervening in the market through quantitative easing policies, investors should pay attention to the importance of holding assets over the long term.

Written by: Anthony Pompliano

Translation: Baicai Blockchain

Market optimism is spreading, and capital flows are shifting accordingly. As Adam Kobeissi pointed out:

"Individual investor confidence in the market is near historic highs: 46% of U.S. retail investors believe there is less than a 10% chance of a market crash within the next six months. This proportion has reached its highest level since June 2006 and has doubled over the past two years. (Source: Yale School of Management survey). In other words, investor concern about the stock market has dropped to its lowest level in 14 years. Meanwhile, the S&P 500 has rebounded approximately 50% from its October 2022 lows. On the flip side, investors now perceive current market valuations as the most overvalued since April 2000, just before the dot-com bubble burst. Market sentiment has become extremely euphoric."

The craziest part of this optimism is this: in the long run, optimists tend to be right. I believe this phenomenon has become increasingly evident in financial markets because the Federal Reserve broke the system around 16 years ago. Since then, we've never truly recovered—and I don't think we ever will.

This weekend, I read a book titled *The Lords of Easy Money* by Christopher Leonard. It provides a detailed account of the evolution of Federal Reserve policy over recent decades, particularly the rise of quantitative easing (QE) and its profound impact on markets and financial assets.

One key takeaway from the book: for the past fifteen years, economists, investors, and market commentators have made a critical mistake—they’ve focused too much on price inflation caused by QE, while largely ignoring asset inflation, which stems from the same root cause.

1. Two Perspectives on Asset Inflation

Asset inflation can be viewed in two ways:

1) The first perspective argues that asset prices cannot rise indefinitely. If QE drives this trend, then asset bubbles will eventually burst.

2) The second view contradicts the first, asserting that if central banks remain willing to lower interest rates and print more money whenever asset prices fall, then asset bubbles won’t burst.

I lean toward the second view. There’s strong reasoning to suggest that as long as the U.S. dollar remains fiat currency, the American economy will not experience another bear market lasting longer than 18 months. That may sound bold—let me explain why.

2. The New Normal of Economic Policy

Central banks have now fully mastered the mechanics of quantitative easing. They can slash interest rates and create money at astonishing speed. For example, during the 2020 pandemic outbreak, the Fed cut interest rates to 0% and created trillions of dollars in a matter of weeks. Although asset prices briefly "collapsed," they quickly rebounded and went on to reach new highs.

This is now the “new normal”—asset prices seem to perpetually rise, fueling the widespread optimism in the market.

3. A New Economic Reality

For those who came of age in the pre-QE economic environment, this new reality might feel disorienting. But nearly two decades of data show we’ve entered an entirely new economic regime.

As Christopher Leonard points out in the book, modern money is no longer real physical currency—it's digitally created out of thin air through electronic entries and ultimately funneled to a select group of primary dealers.

This shift has fundamentally altered our traditional understanding of markets, inflation, and investing.

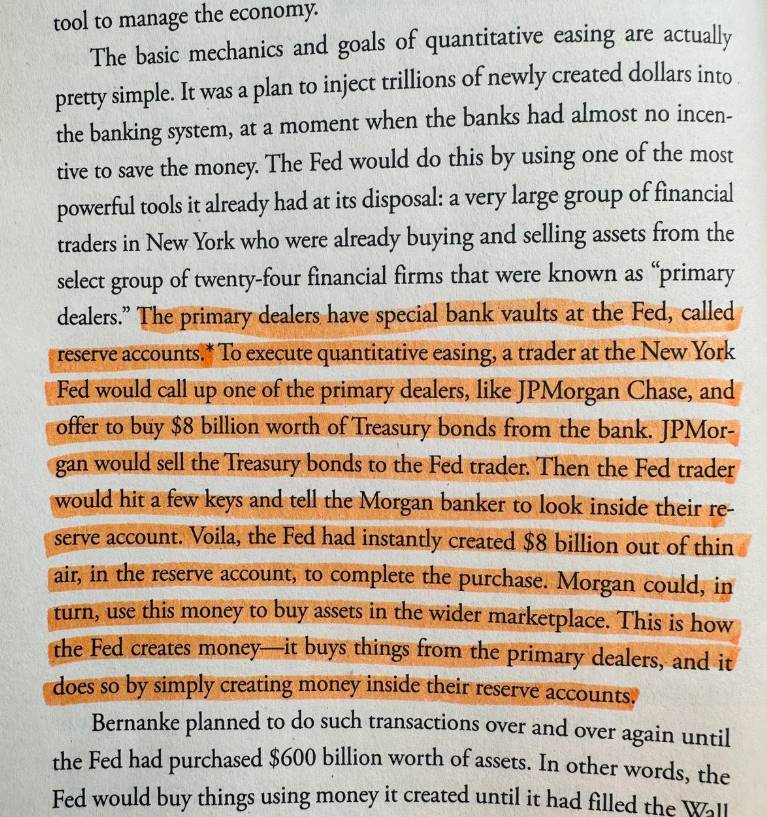

Translation: Quantitative easing is actually quite simple. At its core, it involves creating large amounts of new money and injecting it into the banking system. The goal is to stimulate economic growth when banks lack incentive to lend. The Fed uses a powerful mechanism to achieve this: coordinating with a network of major financial traders in New York—affiliated with 24 firms known as “Primary Dealers,” responsible for buying and selling assets.

These primary dealers hold special bank vaults at the Fed called reserve accounts. When the Fed wants to implement QE, traders at the New York Fed contact these dealers—say, JPMorgan Chase—and propose purchasing $8 billion worth of Treasury bonds. JPMorgan sells those bonds to the Fed trader. Then, with just a few keystrokes, the Fed trader notifies JPMorgan’s bankers to check their reserve account.

In an instant, the Fed creates $8 billion in the reserve account to complete the purchase. JPMorgan can then use this newly created money to buy other assets in the market. This is how the Fed creates money: by purchasing assets from primary dealers and crediting their reserve accounts.

In short, this is how the Fed uses “money creation” to influence markets and stabilize the economy.

If you give someone a printing press, they’ll start printing.

And when the Fed starts printing, asset prices keep rising. You might ask: “What happens if the Fed stops printing?” The analysis shifts—but the crucial point is: America can no longer afford to stop. We’ve become dependent on cheap and abundant money.

This is why I believe sustained bear markets lasting more than 18 months are almost impossible. If the Fed sees asset prices drop significantly, they will intervene swiftly and aggressively.

The market doesn’t operate independently of the Fed; rather, the Fed acts in response to market movements.

In *The Lords of Easy Money*, author Christopher Leonard gives a perfect example of this: under Ben Bernanke, the Fed initially planned to roll out QE on a smaller scale and slower pace, but fearing a disconnect between market expectations and actual action—which could trigger falling asset prices—Bernanke ultimately had to meet market expectations.

Why does this matter? Because the optimism I mentioned at the beginning is critical: the market effectively forces the Fed to intervene and push asset prices higher. Market participants expect it—so the Fed must act.

Now, the market is truly in the driver’s seat.

This development means investors face a choice. You can believe the market has gone mad and that a multi-year bear market is imminent. Or you can recognize that the Fed has permanently broken financial market stability, and they will continue to intervene with economic stimulus whenever problems arise—until excessive money printing leads to high inflation in the U.S. dollar (and that process will take far longer than most people imagine!)

I’m an optimist, and a student of history. Just look back at the Global Financial Crisis (2008), and you’ll see that the rules of the game changed long ago. The key to investing isn’t timing the market—it’s time spent holding assets.

Bearish voices sound smart, but bullish investors are the ones who ultimately win.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News