2024 H1 Web3 Funding Report: Over $7.5 Billion Raised, Number of Deals Up 58%

TechFlow Selected TechFlow Selected

2024 H1 Web3 Funding Report: Over $7.5 Billion Raised, Number of Deals Up 58%

Web3's pre-seed funding stage demonstrated strong resilience, reaching a new high in the first half of 2024 with $189 million raised.

Author: Cheeky Rolo

Translation: TechFlow

Summary

-

In the first half of 2024, Web3 fundraising activity increased significantly, with 1,240 projects raising $7.52 billion—representing a 24% increase in capital and a 58% rise in deal count compared to the second half of 2023. This outpaced the broader venture capital market, which saw capital grow by 16.1% but a 16.7% decline in deal volume.

-

Pre-seed funding in Web3 demonstrated strong resilience, reaching new highs in the first half of 2024 with $189 million raised across 80 deals. Series A funding also showed robust growth, raising $1.56 billion across 77 deals—nearly double the amount from the second half of 2023.

-

The global startup funding environment improved in Q2 2024, driven by an increase in large funding rounds and a surge in AI investment, which doubled to $24 billion. Despite market volatility, overall trends indicate gradual recovery, particularly in seed and Series A stages.

-

Growth in AI and Web3 investments reflects investor confidence in these high-growth sectors, contributing to stabilization and improvement in market conditions in 2024. This trend suggests potential upward momentum in the coming quarters, especially in early-stage deals.

Highlights: First Half of 2024

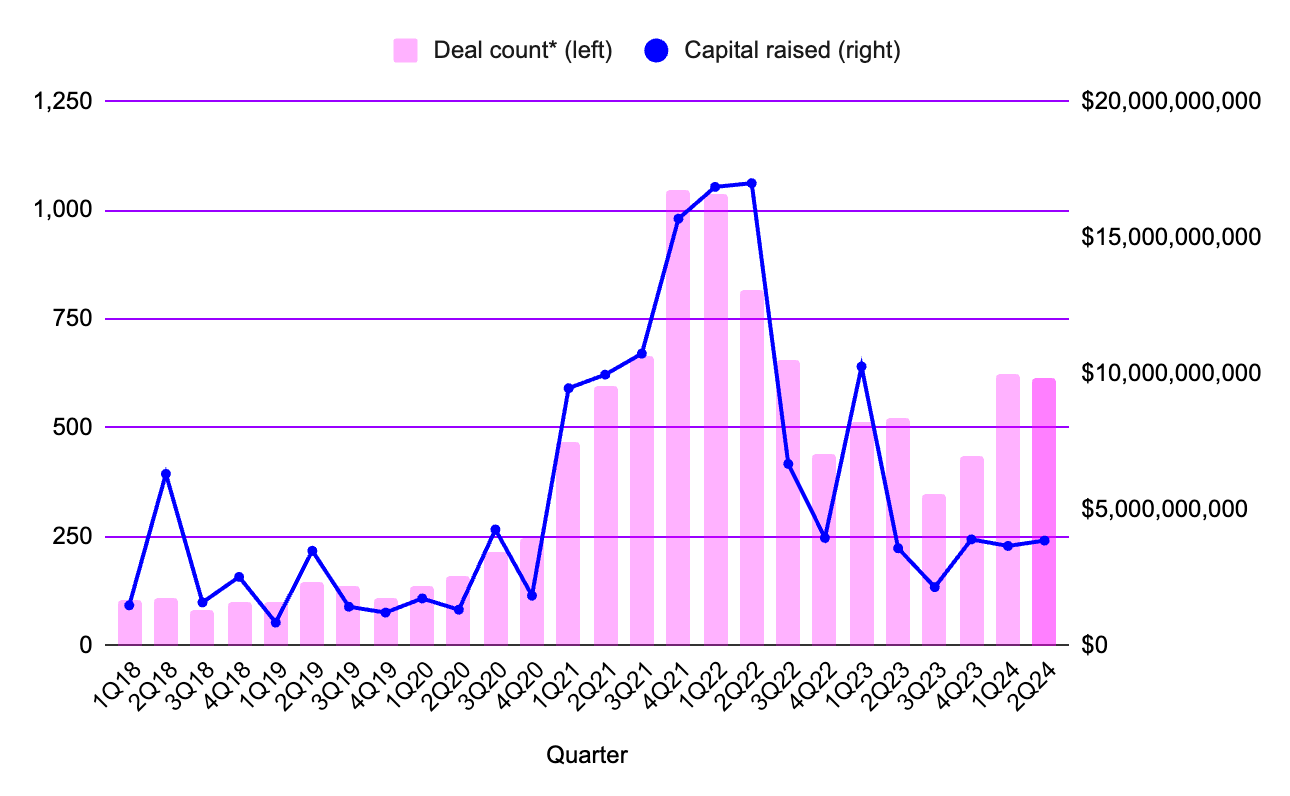

Source: Messari, Quarterly Deals Across Web3 Stages

*Note: Approximately 20% of projects did not disclose basic information such as amounts raised; "deal count" refers to projects that disclosed funding amounts.

-

In the first half of 2024, a total of $7.52 billion was raised across all stages by 1,240 projects—an increase of 24% in capital and 58% in deal count compared to the second half of 2023.

-

In Q1 2024, 624 projects raised $3.66 billion, representing a 6.2% decrease in capital from the previous quarter.

-

In Q2 2024, 616 projects raised $3.86 billion across all funding stages, a 5.5% increase from the prior quarter.

-

-

At first glance, performance in the first half of 2024 appears weaker than in the same period of 2023: 1,041 deals raised $13.9 billion then, meaning capital raised in H1 2024 was down 45.8% year-on-year.

-

However, this significant difference can be attributed to one standout case: Stripe raised $6.5 billion in March 2023. That single event accounted for 83% of funds raised that month, 63% of Q1 2023 totals, and 47% of the entire first half of 2023. If we exclude Stripe’s round as an outlier, H1 2024 fundraising actually exceeded H1 2023 by 2%—with $7.36 billion raised in H1 2023 after removing Stripe’s contribution.

-

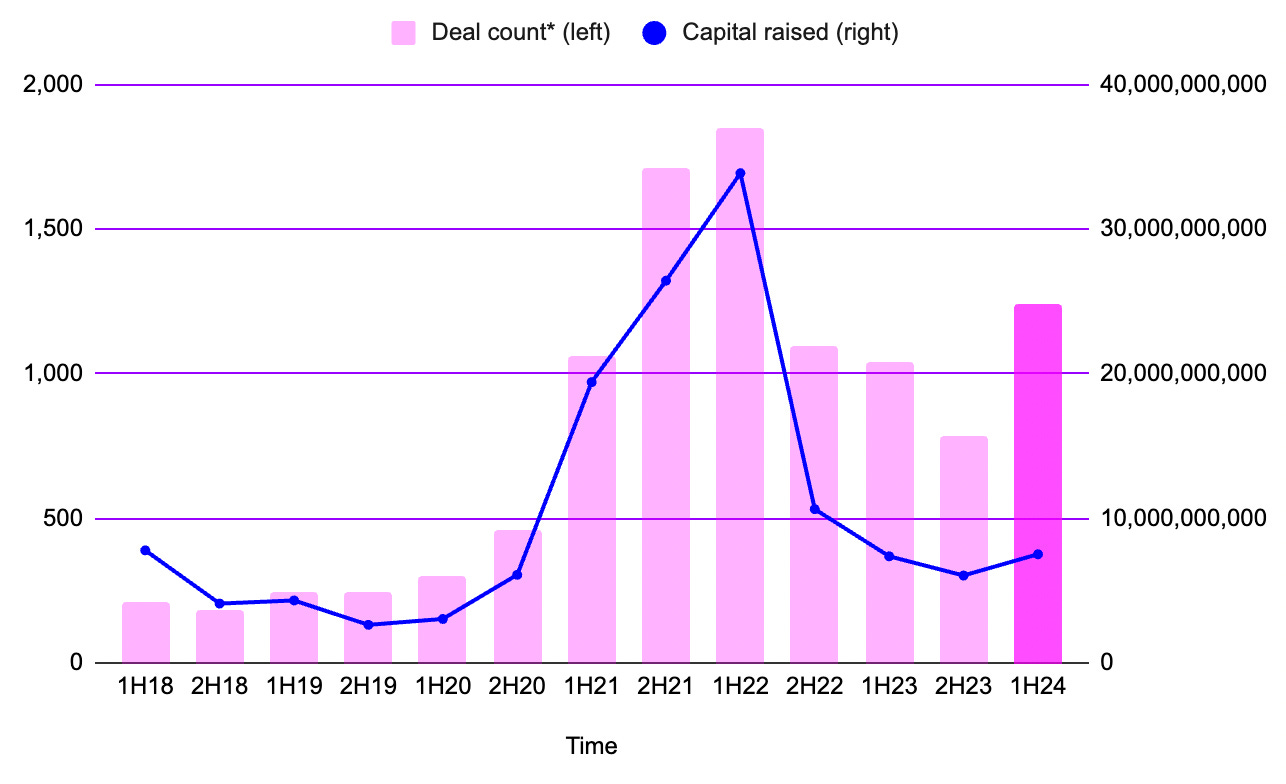

Source: Messari, Semi-Annual Deals Across Web3 Stages

Note: Stripe's $6.5 billion raise in March 2023 has been removed from the data in this chart

-

Looking at the broader venture capital market, $39.6 billion was raised through 2,525 deals in H1 2024, compared to $34.1 billion through 3,031 deals in H2 2023. This indicates a 16.1% increase in capital raised but a 16.7% drop in deal volume from H2 2023 to H1 2024.

-

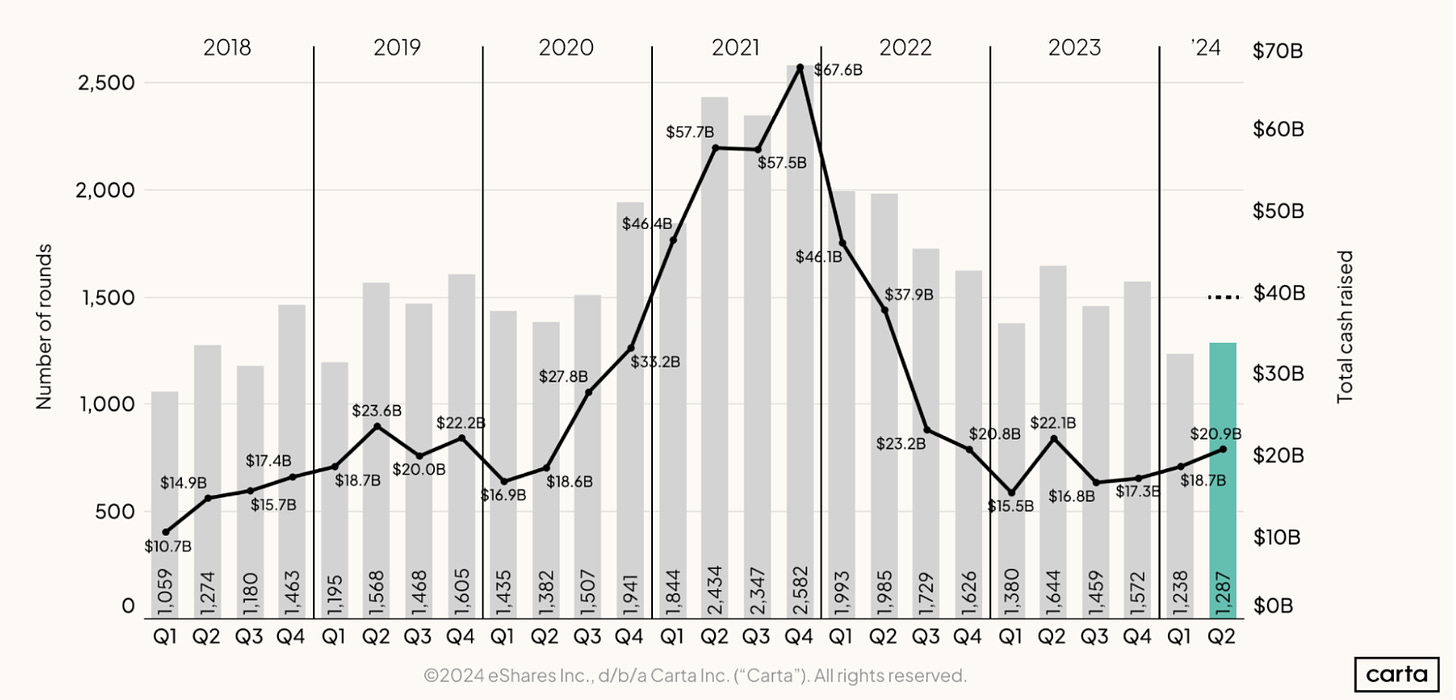

According to Carta, both deal count and total capital raised in Q2 2024 surged compared to Q1 2024, with 1,287 funding rounds completed totaling $20.9 billion—marking steady quarterly growth since Q3 2023. Q2 2024 recorded the highest level of VC investment over the past 12 months.

-

Source: Carta, Hamza Shad,“State of Private Markets Q2 2024”, August 2024

Source: Crunchbase, Gené Teare,“Global Funding and M&A Rebound in Q2 With AI Surge”, July 2024

-

Global startup funding rebounded in Q2, reaching $79 billion—up 16% from the previous quarter and 12% higher than $71 billion in Q2 2023. This growth was largely driven by mega-rounds exceeding $100 million. According to Crunchbase, we are currently in the eighth to ninth quarter of a broader funding downturn. Although this quarter ranks among the strongest since Q1 2023, it does not necessarily signal a full recovery in the venture capital market. Since 2023, funding levels have fluctuated significantly each quarter, primarily due to large pre-IPO and AI company financing rounds.

-

Overall, Web3 fundraising performance slightly improved relative to the broader venture capital market—not only due to greater capital growth (24% vs. 16%) but also because of a substantial increase in deal volume (58% increase in Web3 vs. a 17% decline in the broader market).

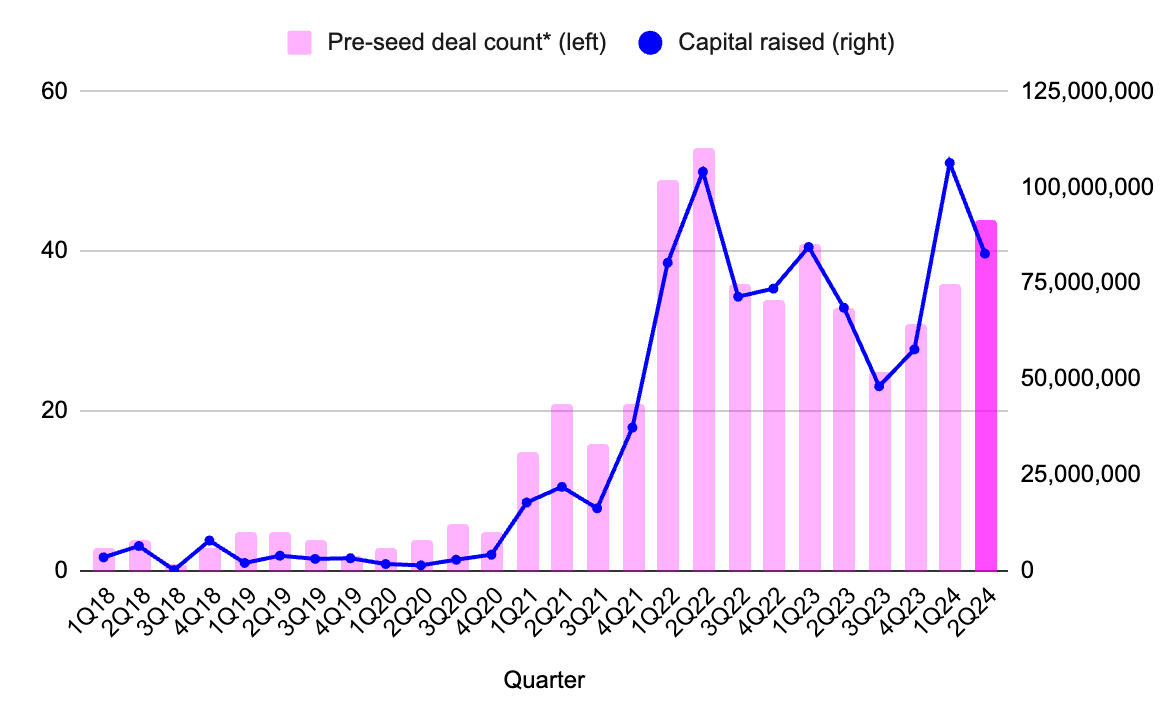

Web3 Pre-Seed Funding Landscape

Source: Messari, Web3 Pre-Seed Deals and Quarterly Fundraising

-

Since Q2 2023, pre-seed fundraising has shown the strongest resistance to bear market trends in both the Web3 sector and the broader venture capital landscape. Deal counts at the pre-seed stage have grown quarter-over-quarter since Q3 2023. In Q1 2024, Web3 venture capital achieved a record high in pre-seed fundraising: $106 million raised through 36 deals.

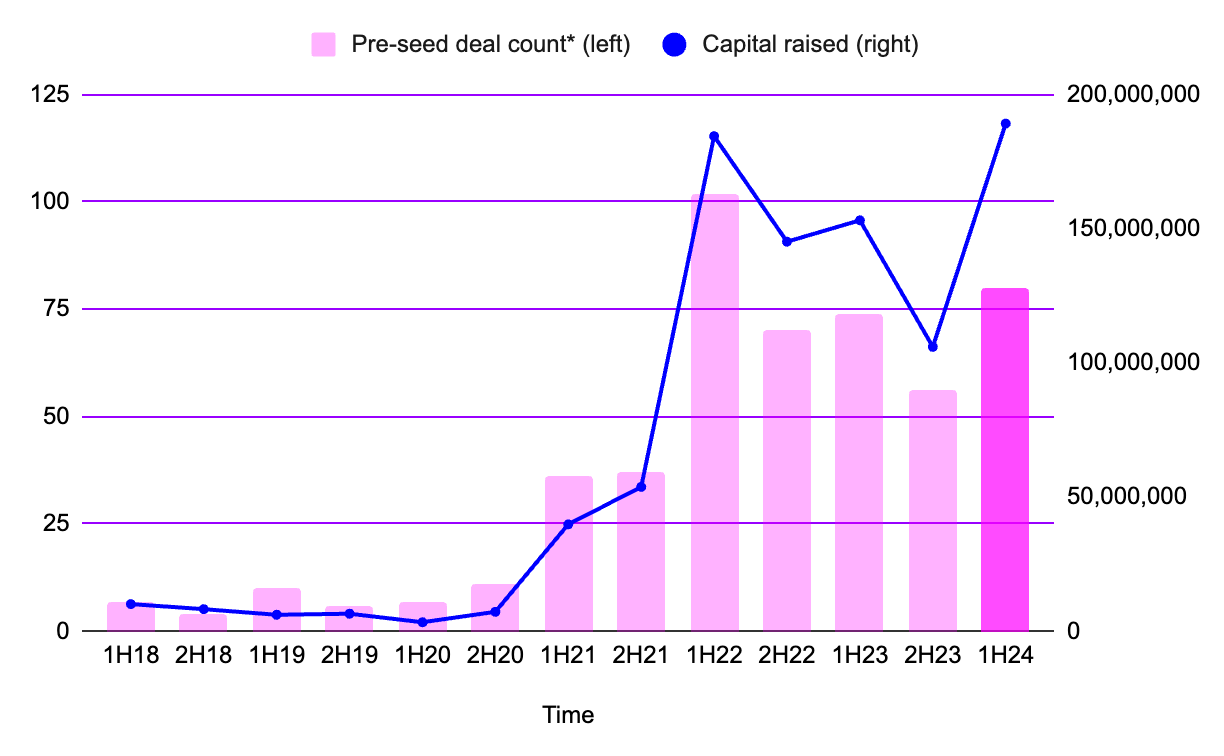

Source: Messari, Web3 Pre-Seed Deals and Semi-Annual Fundraising

-

This also set a new semi-annual record for Web3 pre-seed fundraising: $189 million raised through 80 deals in H1 2024, surpassing the previous high of $184 million raised through 102 deals in H1 2022.

Web3 Seed and Series A Funding Landscape

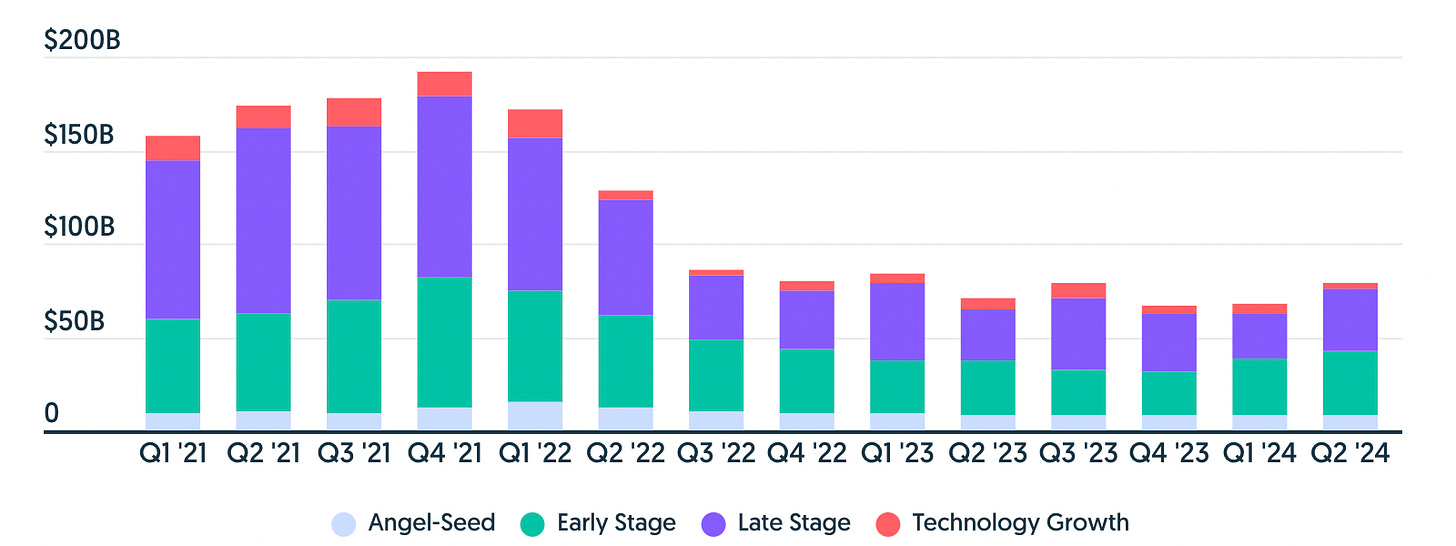

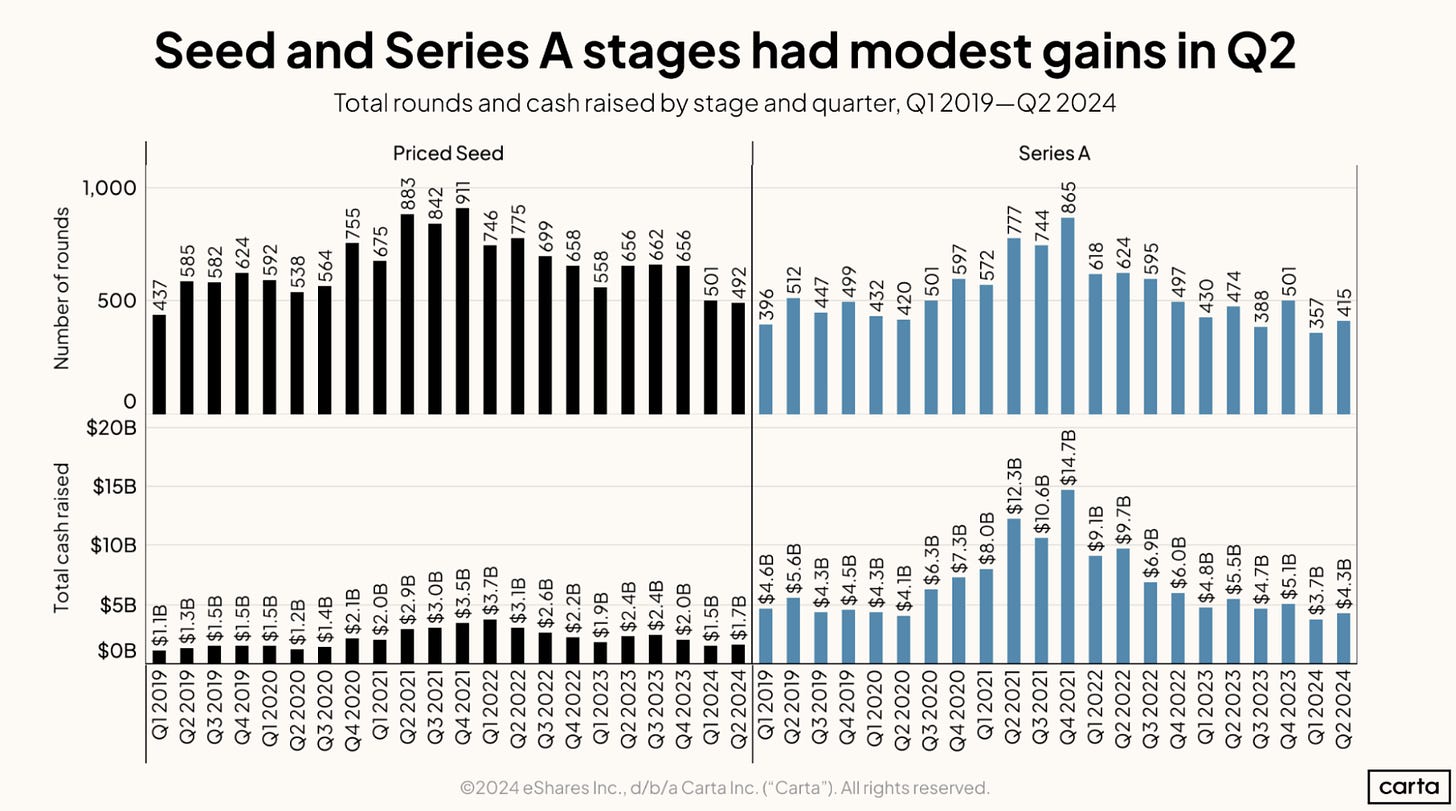

Source: Carta, Hamza Shad,“State of Private Markets: Q2 2024”, August 2024

-

Data from Carta illustrates the performance of seed and Series A deals in the broader venture capital market. In Q2 2024, seed deal volume remained nearly flat compared to Q1, while Series A deals outperformed the previous quarter—suggesting Q2 may mark a turning point after Q1, which had seen the lowest number of seed and Series A deals since early 2019. While total capital raised in both stages rose slightly in Q2, it is notable that Series A fundraising in Q1 hit a five-year low. Although the 16% growth in Q2 still places it among the lower-performing quarters for Series A, it could signal the beginning of an upward trend—albeit one that remains weak.

-

Against the broader funding market backdrop, the expected growth trend for seed and Series A deals becomes even clearer.

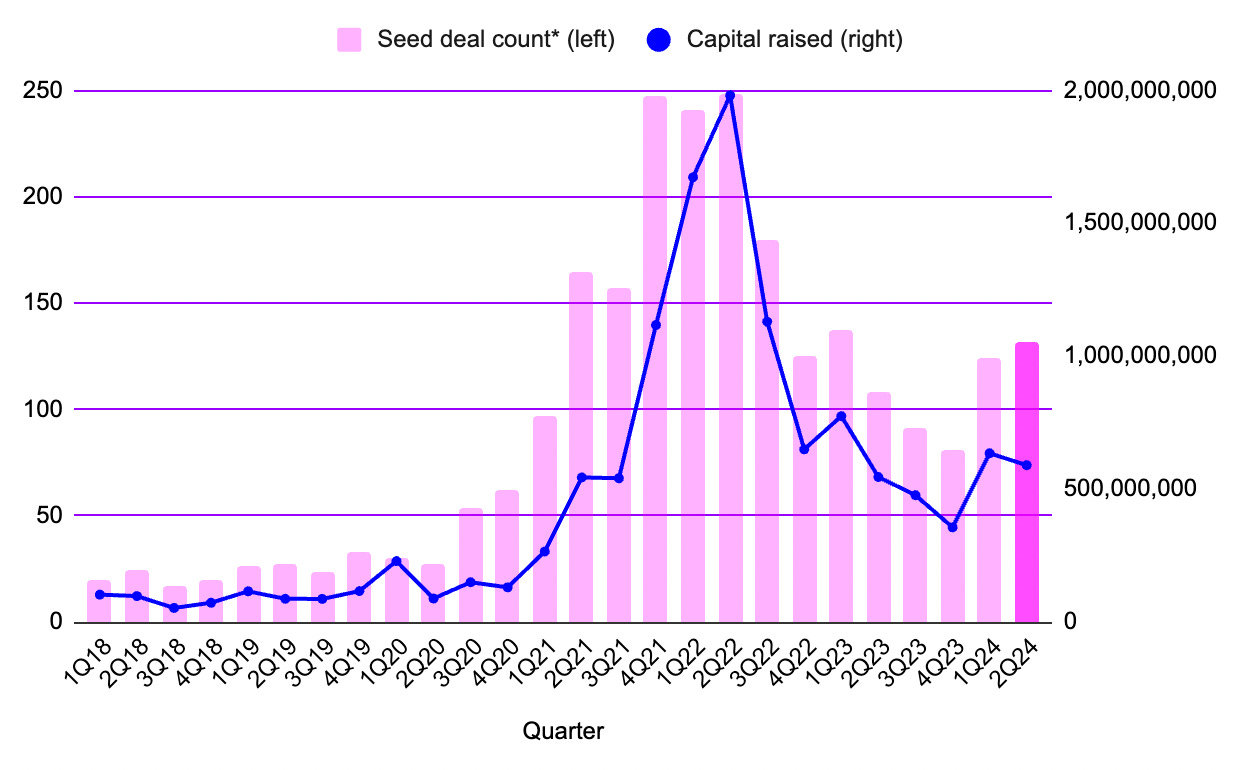

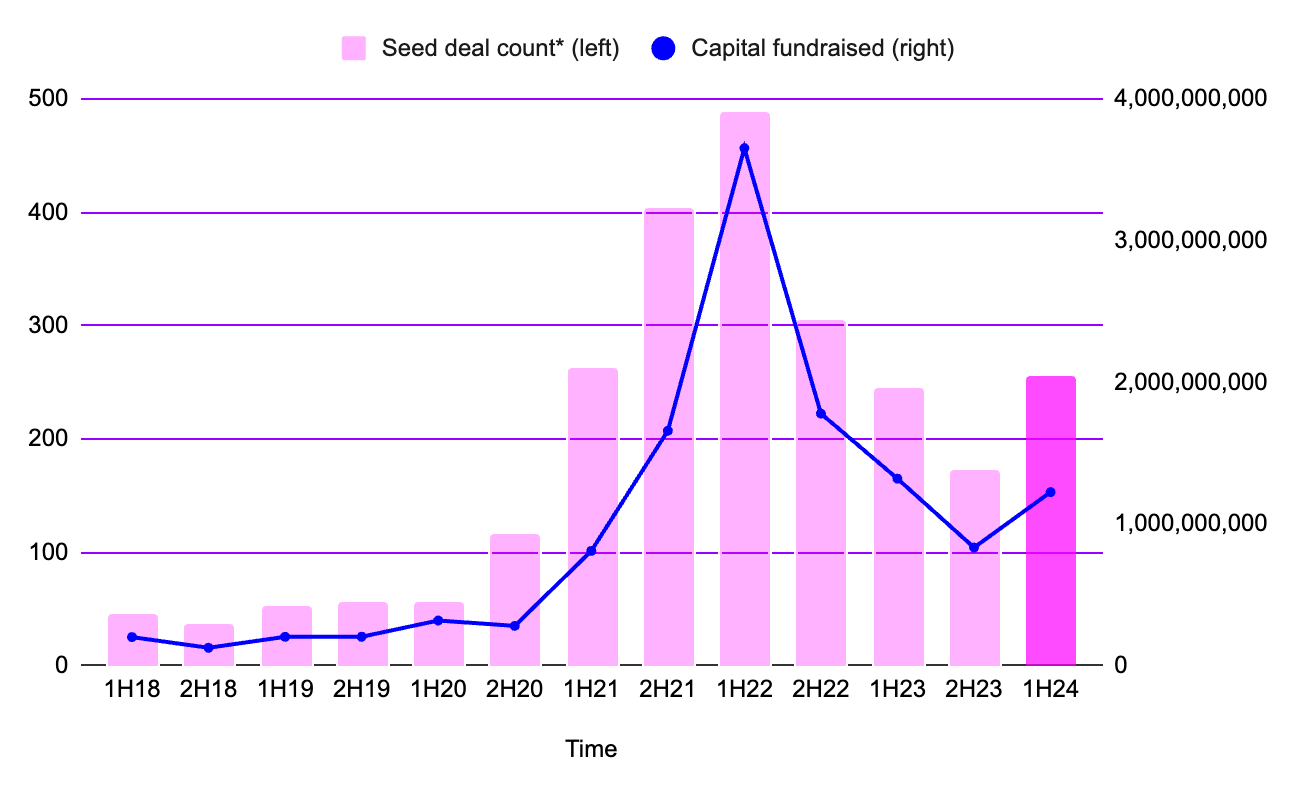

Source: Messari, Web3 Seed Deals and Quarterly Fundraising

Source: Messari, Web3 Seed Deals and Semi-Annual Fundraising

-

In the first half of 2024, the seed stage raised $1.23 billion across 256 deals—an increase of 47% in capital and 49% in deal count compared to the same period last year. Although seed-stage fundraising declined by 7% from Q1 to Q2 2024, transaction volumes have now grown for two consecutive quarters. Even so, Q2’s total funding still exceeded any single quarter between Q2 and Q4 2023.

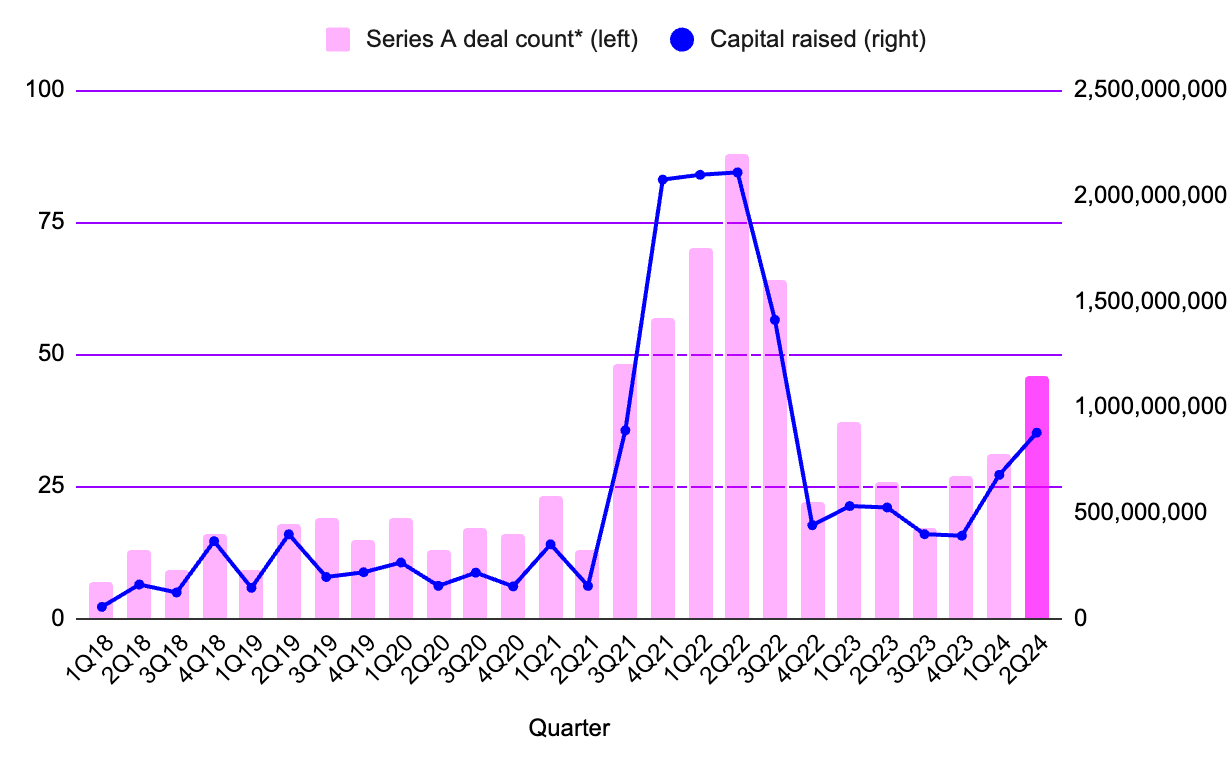

Source: Messari, Web3 Series A Deals and Quarterly Fundraising

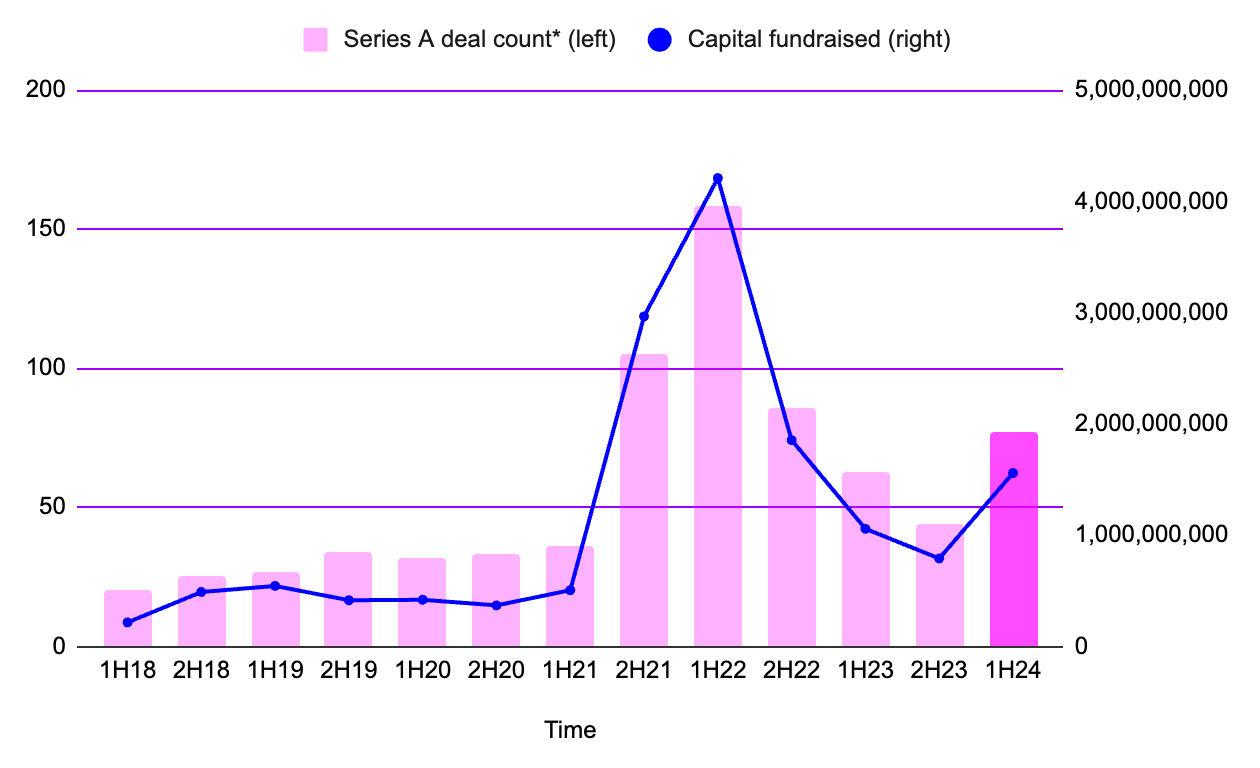

Source: Messari, Web3 Series A Deals and Semi-Annual Fundraising

-

The upward trend in Web3 Series A deals is even more pronounced, with both fundraising amounts and deal counts growing each quarter since the end of Q4 2023—contrasting with pre-seed or seed-stage trends during the same period. Overall, H1 2024 saw $1.56 billion raised through 77 Series A deals—nearly double the amount from H2 2023 (a 97% increase) and a 75% rise in deal volume.

-

Additionally, AI-focused fundraising surged, doubling quarter-over-quarter to $24 billion, accounting for a major share of total investment. Public token sales continue to dominate, while early-stage VC activity remains stable. This indicates sustained investor confidence in high-growth areas like AI and Web3, helping to stabilize and improve market conditions in 2024.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News