A Guide to the 6 Key Risks to Watch in the Early Stages of Fed Rate Cuts

TechFlow Selected TechFlow Selected

A Guide to the 6 Key Risks to Watch in the Early Stages of Fed Rate Cuts

At the beginning of an interest rate cut cycle, it doesn't immediately mean a sharp surge is coming; there are still some risks worth watching out for.

By Web3Mario

Summary: On August 23, 2024, Federal Reserve Chair Powell officially announced at the Jackson Hole Global Central Bank Symposium: “Now is the time for policy adjustment. The direction ahead is clear—interest rate cuts are coming. The timing and pace will depend on incoming data, evolving economic outlooks, and the balance of risks.” This marks a turning point in the Fed’s nearly three-year tightening cycle. Assuming no major macroeconomic surprises, the first rate cut is likely to occur at the September 19 meeting. However, entering the early phase of a rate-cutting cycle does not immediately translate into market rallies. Several risks remain that investors should watch closely. Below, I summarize the six most critical issues to monitor during this initial easing phase: U.S. recession risk, pace of rate cuts, the Fed’s QT (Quantitative Tightening) program, re-ignition of inflation, global central bank coordination efficiency, and U.S. political risk.

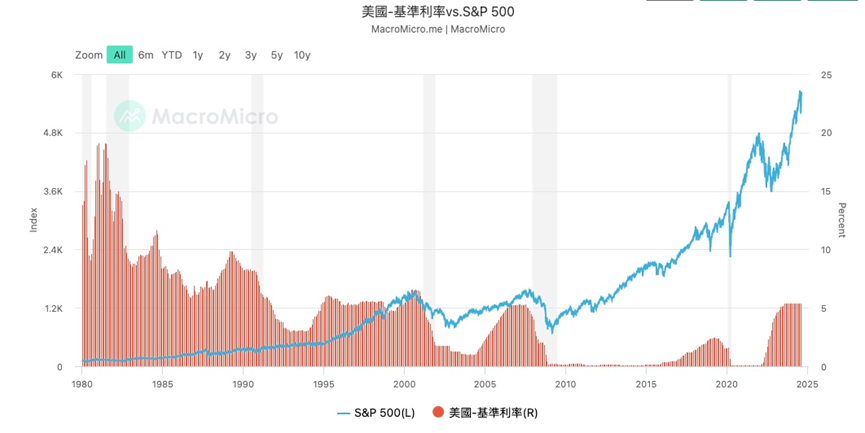

Rate cuts do not necessarily lead to immediate risk market rallies—in fact, markets often decline initially

Monetary policy shifts by the Federal Reserve have profound impacts on global financial markets. Especially during the early stages of rate cuts, although lower rates are typically seen as stimulative for growth, they also bring a series of potential risks. This means that rate cuts do not guarantee an immediate upswing in risk assets—in fact, markets often fall. The reasons behind this phenomenon can generally be categorized as follows:

- Increased financial market volatility

While rate cuts are often interpreted as supportive signals for the economy and markets, during their initial phase, uncertainty and market volatility may rise. Investors may interpret the Fed’s actions differently—some may view rate cuts as a sign of concern over slowing growth. This uncertainty can trigger significant swings in both equity and bond markets. For example, during the 2001 downturn and the 2007–2008 financial crisis, despite the Fed initiating rate cuts, stock markets continued to fall sharply. This was because investors feared that economic deterioration would outweigh any positive effects from monetary easing.

- Inflation risks

Lower interest rates reduce borrowing costs, encouraging consumption and investment. However, if rate cuts are too aggressive or prolonged, they may fuel inflationary pressures. When abundant liquidity chases limited goods and services, prices can surge rapidly—especially when supply chains are constrained or the economy nears full employment. Historically, in the late 1970s, Fed rate cuts contributed to soaring inflation, forcing later aggressive rate hikes that triggered recessions.

- Capital outflows and currency depreciation

Fed rate cuts typically erode the yield advantage of the U.S. dollar, prompting capital to flow from U.S. markets into higher-yielding assets abroad. Such outflows put downward pressure on the dollar, leading to depreciation. While a weaker dollar can boost exports, it also raises risks of imported inflation—particularly when commodity and energy prices are high. Moreover, capital flight could destabilize emerging markets, especially those reliant on dollar-denominated financing.

- Financial system instability

Rate cuts are often used to ease economic stress and support financial stability, but they may also encourage excessive risk-taking. With cheap credit, financial institutions and investors may chase higher returns through riskier investments, inflating asset bubbles. For instance, after the 2001 tech bubble burst, the Fed slashed rates to stimulate recovery—but these policies inadvertently fueled the housing bubble, ultimately contributing to the 2008 financial crisis.

- Limited effectiveness of policy tools

In the early phase of rate cuts, if the economy is already near zero rates or in a low-rate environment, the Fed's conventional tools become constrained. Overreliance on rate cuts may fail to stimulate growth effectively—especially when rates approach zero. This necessitates unconventional measures such as Quantitative Easing (QE). In both 2008 and 2020, the Fed had to deploy additional tools after cutting rates to near zero, highlighting the limited efficacy of rate cuts alone under extreme conditions.

Looking at historical data since the 1990s, following the end of the Cold War and the onset of U.S.-led globalization, the Fed’s monetary policy has often exhibited a lagging nature. Today, amid escalating U.S.-China tensions and the breakdown of old global orders, policy uncertainty has intensified further.

Key Current Market Risk Factors

Next, let’s examine the main current market risks: U.S. recession risk, pace of rate cuts, the Fed’s QT (Quantitative Tightening) program, re-emergence of inflation, and global central bank coordination efficiency.

Risk One: U.S. Recession Risk

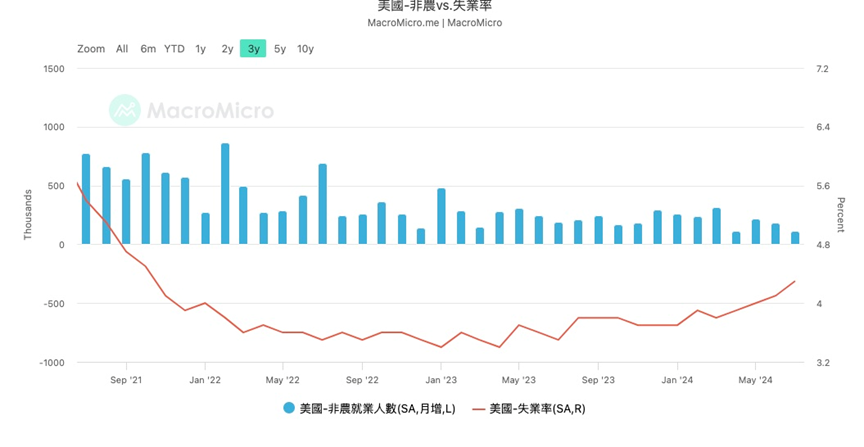

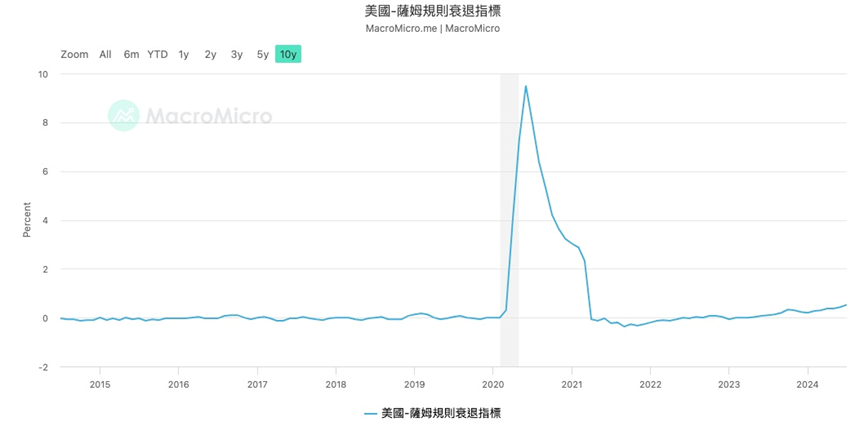

Many refer to the potential September rate cut as a “preventive” or “preemptive” move—a decision made not because the economy has clearly deteriorated, but to mitigate rising recession risks. As analyzed in my previous article, the U.S. unemployment rate has officially triggered the "Sahm Rule" recession warning threshold. Therefore, it is crucial to observe whether the September rate cut can curb the rising unemployment trend and help stabilize the economy against a deeper downturn.

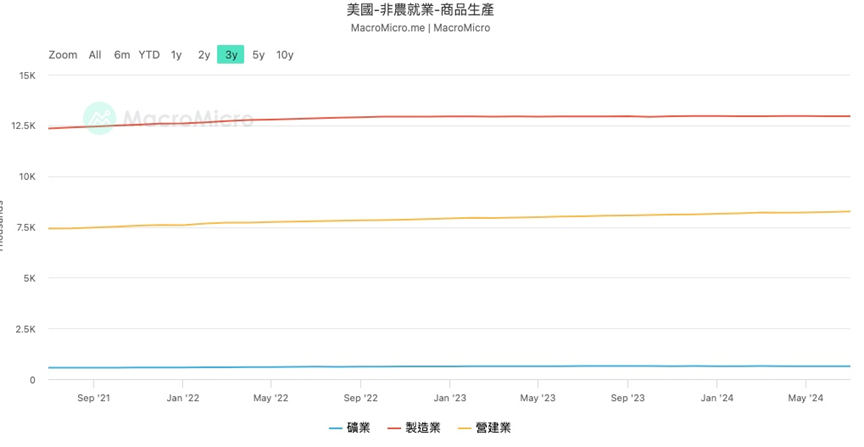

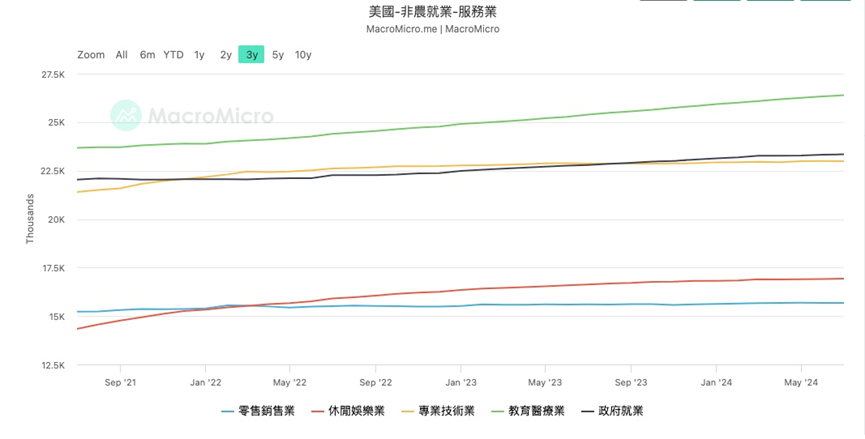

Examining subcomponents of non-farm payroll data, we see prolonged low-volatility fluctuations in goods-producing sectors, with construction contributing more than manufacturing. For the U.S. economy, high-end manufacturing, along with its supporting technology and financial services, are key drivers. When high-income professionals in these sectors earn more, wealth effects boost consumer spending, benefiting mid-to-low-tier service industries. Thus, employment trends among this group serve as a leading indicator for overall labor health. Weakness in manufacturing employment may signal early warning signs. Additionally, the U.S. ISM Manufacturing Index (PMI) shows a rapid decline, further confirming softness in the manufacturing sector.

Turning to services, professional & technical services and retail show similar stagnation. Positive contributions mainly come from education, healthcare, leisure, and hospitality. I believe two factors explain this: First, recent resurgences of COVID-19 cases and hurricane-related disruptions have created shortages in medical personnel. Second, July is peak vacation season in the U.S., boosting tourism and leisure spending. Once holidays end, these sectors are likely to face setbacks.

Overall, U.S. recession risks remain present. Investors should continue monitoring key macro indicators including non-farm payrolls, initial jobless claims, PMI, Consumer Confidence Index (CCI), and home price indices.

Risk Two: Pace of Rate Cuts

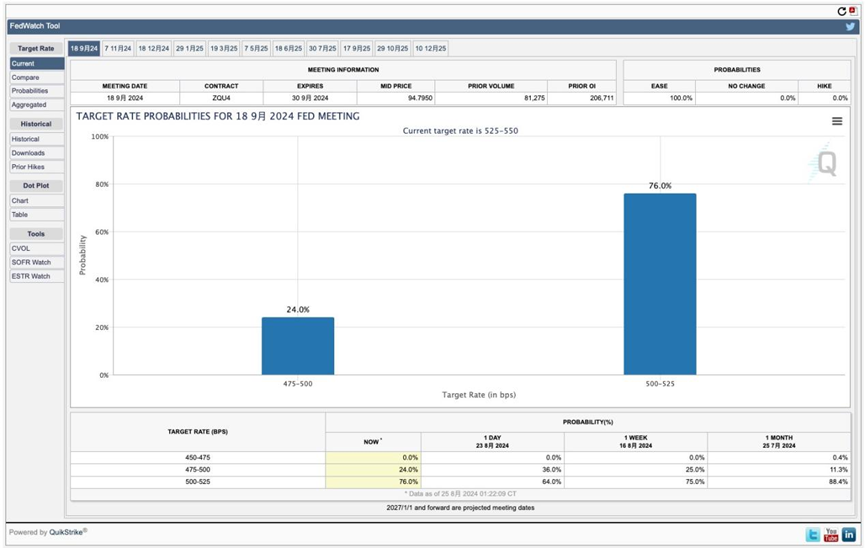

The second key factor is the pace of rate cuts. Even though a shift toward easing is confirmed, the speed of cuts will significantly impact risk asset performance. Emergency rate cuts by the Fed are historically rare. Between scheduled FOMC meetings, markets must interpret economic fluctuations independently, which influences pricing. If data suggest the Fed is cutting too slowly, markets may react prematurely. Hence, establishing an appropriate cutting rhythm—and guiding expectations via forward guidance—is essential for aligning market behavior with Fed objectives.

Current market pricing implies about a 75% chance of a 25–50 bps cut in September and a 25% chance of a 50–75 bps reduction. Monitoring these probabilities offers clear insight into prevailing market sentiment.

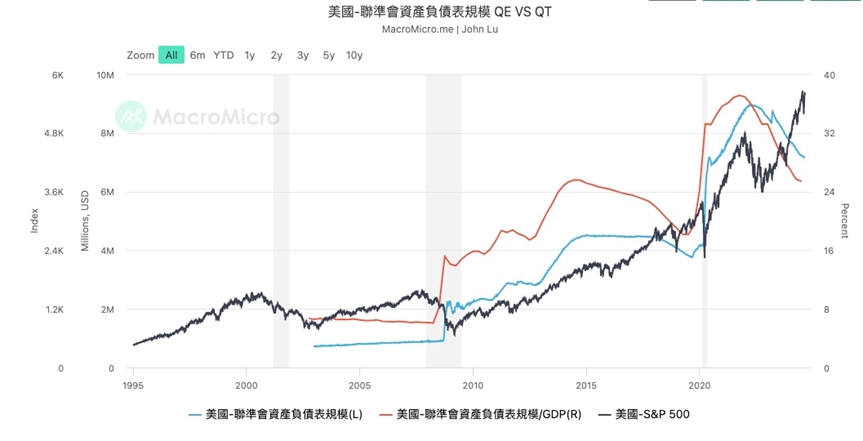

Risk Three: QT Program

After the 2008 financial crisis, the Fed quickly brought interest rates to zero, yet the economy failed to recover—signaling a breakdown in traditional monetary policy transmission. With no room left to cut rates, the Fed introduced Quantitative Easing (QE), expanding its balance sheet to inject liquidity and increase bank reserves. This effectively transferred market risk onto the central bank’s balance sheet. To reduce systemic risk, the Fed must eventually reverse this process through Quantitative Tightening (QT), shrinking its balance sheet and preventing excessive buildup of its own vulnerabilities.

Powell’s speech did not address the current QT plan or future adjustments. Therefore, ongoing attention to the QT trajectory and its impact on bank reserve levels remains necessary.

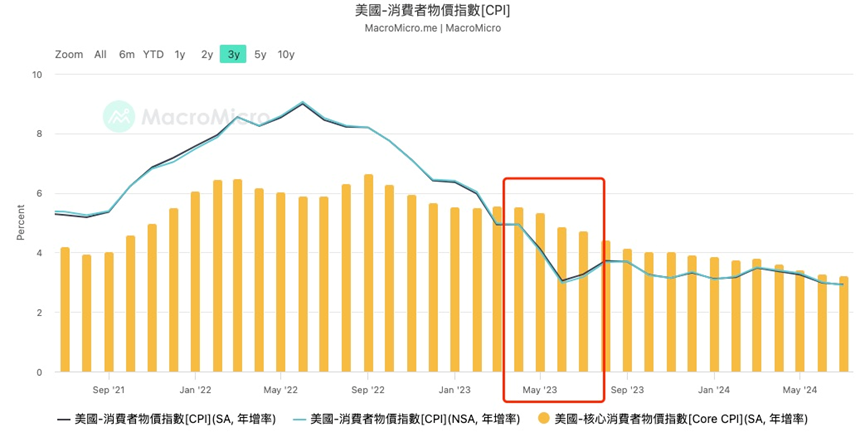

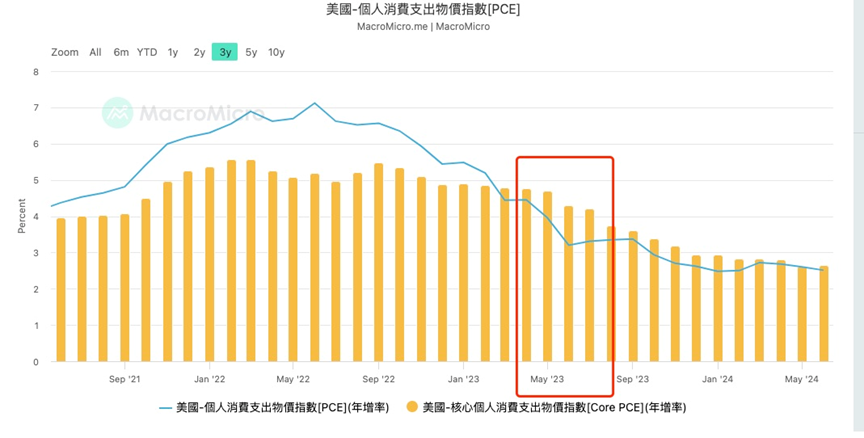

Risk Four: Re-ignition of Inflation

Powell expressed optimism about inflation control during Friday’s meeting, noting that while the 2% target hasn’t been reached, confidence in managing inflation is growing. Indeed, recent data support this view. Some economists have even begun questioning whether the 2% inflation target remains appropriate post-pandemic.

However, several risks remain:

-

First, from a macro perspective, U.S. reindustrialization efforts have faced numerous obstacles. Amid U.S.-China strategic competition and broader deglobalization trends, supply-side constraints remain fundamentally unresolved. Any geopolitical shock could reignite inflation.

-

Second, unlike previous cycles, the U.S. economy avoided a deep recession during this hiking cycle. As rate cuts begin, risk assets are likely to rebound. Renewed wealth effects could drive demand-side expansion, pushing up service-sector inflation once again.

-

Finally, there’s a statistical consideration: To filter out seasonal noise, CPI and PCE data are reported year-over-year. Starting in May 2024, the high base effect from 2023 will drop out of the comparison window. From that point onward, inflation readings may appear artificially elevated due to easier year-on-year comparisons.

Risk Five: Global Central Bank Coordination Efficiency

Most readers likely still recall the risks tied to the Japan-U.S. interest rate differential earlier in August. Although the Bank of Japan swiftly intervened to calm markets, recent testimony by Governor Kazuo Ueda before Congress revealed a hawkish tilt. During his remarks, the yen strengthened noticeably, only stabilizing after officials reiterated calming statements. In reality, Japan’s domestic macro data do justify rate hikes—as I detailed in a prior article. Yet, given Japan’s long-standing role as a primary source of global carry-trade funding, any tightening by the BOJ introduces significant uncertainty into risk markets. Close monitoring of its policy stance is therefore essential.

Risk Six: U.S. Election Risk

Lastly, the U.S. election poses a major risk. In prior analyses, I’ve examined the economic policies of Trump and Harris in detail. As the election draws closer, increasing political polarization and unpredictable events will heighten market uncertainty. Staying informed about election-related developments is thus imperative.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News