Can stablecoins save Ripple as XRP payment functionality weakens?

TechFlow Selected TechFlow Selected

Can stablecoins save Ripple as XRP payment functionality weakens?

Ripple, a blockchain services company and creator of the XRP Ledger, announced it will launch a U.S. dollar-pegged stablecoin.

Compiled by: Jordan, PANews

Ripple, a blockchain services company and creator of the XRP Ledger, has announced plans to launch a U.S. dollar-pegged stablecoin, officially entering the stablecoin market valued at over $150 billion.

According to Ripple, its stablecoin is expected to launch later this year and will be fully backed 1:1 by U.S. dollar deposits, short-term U.S. Treasury securities, and other cash equivalents. Initially, it will be deployed on both Ripple’s XRP Ledger and the Ethereum blockchain, adhering to the ERC-20 token standard.

Better Late Than Never: Why Is Ripple Forcing Its Way Into the Stablecoin Race?

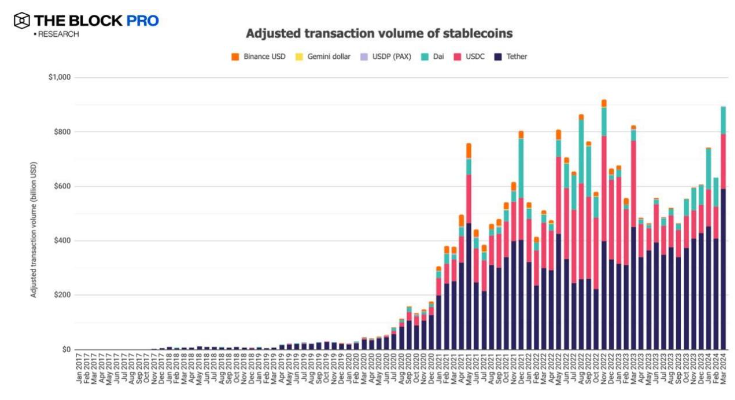

Today, the stablecoin market continues to expand rapidly. According to The Block Pro data, adjusted on-chain transaction volumes for stablecoins surged in March 2024, reaching $893.8 billion—an increase of 41.3%. The total supply of issued stablecoins also rose by 6.2% to $137.4 billion (surpassing $150 billion by early April). Tether and Circle have nearly monopolized the entire market: USDT holds a dominant 76.3% share, while USDC accounts for nearly 20%, giving the two together a combined market dominance exceeding 96%.

So why is Ripple venturing into this highly concentrated market? There are three main reasons:

-

First, demand for stablecoins continues to grow. In fact, stablecoins are among the most popular digital assets for cryptocurrency traders, as they are theoretically insulated from the price volatility seen in major cryptocurrencies like Bitcoin (BTC) and Ethereum (ETH). Based on Ripple's projections, the stablecoin market could exceed $2.8 trillion by 2028. There is clear demand within the crypto ecosystem for stablecoins that offer trust, stability, and utility—this is one of the key motivations behind their decision to enter the space.

-

Second, launching a stablecoin can help accelerate the development of Ripple’s ecosystem. As Ripple CTO David Schwartz explained, part of the motivation is opportunistic: “Stablecoins represent a growing market, and issuing one essentially allows you to operate like a bank that doesn’t pay interest—which seems like a pretty good business opportunity.” A successful stablecoin launch could bring more value and activity into the DeFi ecosystem of the XRP Ledger. Although the Ripple-supported blockchain already hosts services such as DEXs, it must be acknowledged that usage rates remain low compared to other blockchains.

-

Third, transparency will be a central focus for Ripple’s stablecoin issuance, with primary users being enterprises and banks. David Schwartz stated that Ripple will conduct monthly public audits performed by a top-tier accounting firm and take all necessary measures to ensure full transparency. In his words: “Ripple doesn’t want to squeeze out an extra few cents—we don’t need to. Ripple’s balance sheet is rock solid.” Moreover, Ripple’s target audience consists primarily of corporate clients and financial institutions—segments where regulatory compliance is paramount, as they must justify their stablecoin adoption decisions to shareholders and regulators alike. Therefore, Ripple intends to partner with U.S.-based banks to hold reserve assets, ensuring a “compliance-first” mindset across the entire stablecoin landscape.

Can a Stablecoin Save Ripple?

It should be noted that Ripple’s XRP-based business model has shown signs of stagnation. Austen Campbell, a professor at Columbia Business School and former Paxos stablecoin fund manager, bluntly stated: “No one uses XRP as a payment method, just as no one truly uses BTC.” Ripple’s partnerships centered around XRP-powered cross-border payments have largely failed to deliver results. Examples include:

-

Santander, one of Europe’s largest banks, decided to discontinue its collaboration with Ripple after realizing that XRP could not meet its customers’ needs;

-

The partnership between Ripple and MoneyGram ended abruptly due to rising costs associated with XRP-based cross-border transactions, as well as MoneyGram’s need to establish third-party relationships with geographically dispersed cryptocurrency exchanges;

-

Bank Dhofar, Oman’s second-largest bank, once announced plans to use RippleNet and offer Ripple-powered payment services to its customers. However, this mention appeared only on the bank’s website, and many of its other applications—including payment apps and remittance services—make no reference to Ripple whatsoever on their corporate websites.

Notably, whether XRP qualifies as a security remains unresolved and awaits final judgment following the appeal phase of Ripple’s four-year legal battle with the U.S. Securities and Exchange Commission (SEC). Facing potential SEC fines of up to $2 billion, Ripple urgently needs to identify new and reliable revenue streams. From this perspective, launching a stablecoin appears to be a logical strategic move.

Even a Late Entrant, Ripple Is Determined to Claim a Slice of the Stablecoin Pie

We all know that in the cryptocurrency space, stablecoins are considered one of the most important tools. Whether on centralized or decentralized trading platforms, and across both spot and derivatives markets, most transactions are priced in stablecoins. Despite their relatively small share of the overall crypto market capitalization, stablecoins generate substantial profits—this is precisely why companies like PayPal, First Digital Trust, and Ripple are rushing to enter the field. The pie is simply too big to ignore.

Andy Bromberg, CEO of Beam—a stablecoin wallet—pointed out that high yields on U.S. Treasuries have turned dollar-backed stablecoins into a “lucrative business.” According to U.S. government data, composite interest rates on Class I bonds (a type of U.S. Treasury bond whose rate adjusts every six months) reached 5.27% between November 2023 and April 2024. This means that if Ripple’s stablecoin reaches a scale of $1 billion, annual interest income alone would exceed $50 million.

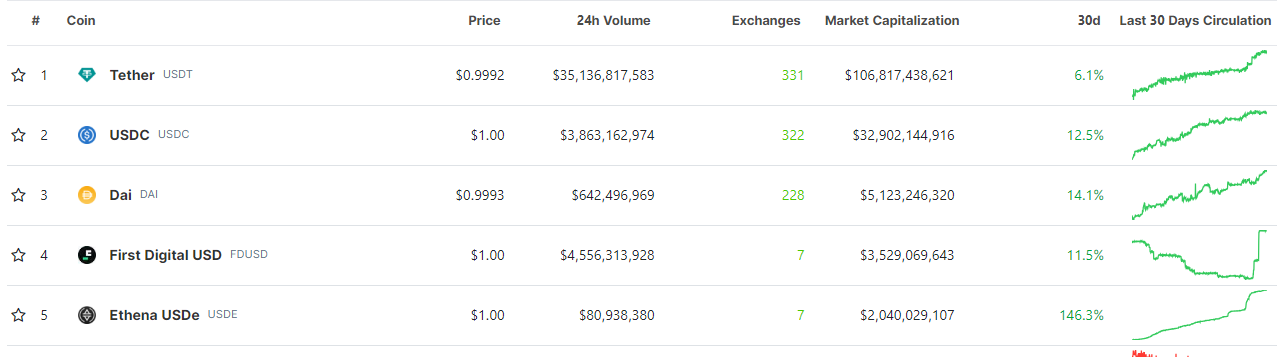

Achieving a $1 billion issuance scale in the stablecoin market does not seem far-fetched. Take USDe, the stablecoin launched by Ethena Labs, as an example—its market cap surpassed $2 billion within less than four months and quickly entered the top five largest stablecoins by market value.

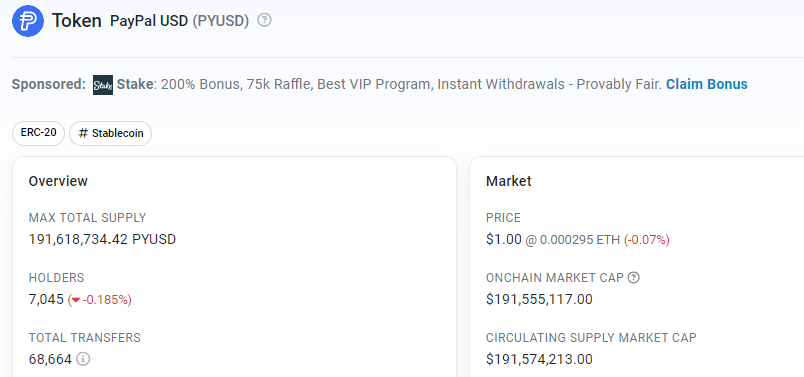

Of course, there are also industry examples worth learning from, such as PYUSD—the stablecoin issued by PayPal. Like Ripple’s planned stablecoin, PYUSD is fully backed by U.S. dollar deposits, short-term U.S. Treasuries, and similar cash equivalents, and is also built on the Ethereum blockchain using the ERC-20 standard. Yet since its launch, its circulation has reached only about $200 million, with fewer than 70,000 transactions recorded. One major reason for PYUSD’s slow adoption may lie in its limited real-world applications. Despite PayPal’s massive payment infrastructure, PYUSD has struggled to integrate effectively with DeFi protocols and DEXs in the crypto ecosystem.

Frankly speaking, the stablecoin market has yet to reach a “winner-takes-all” state, leaving room for new entrants. If the market grows twelvefold as Ripple predicts, the prize will become exceptionally attractive. Should Ripple eventually secure a top-three position, it would undoubtedly strengthen its standing in the broader cryptocurrency landscape.

However, whether Ripple ultimately achieves real success in the stablecoin market may depend more on its ability to attract end-users and retain them within its ecosystem. Only time will tell.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News