Deep Dive into L2 Economic Models: With the Cancun Upgrade Approaching, How to Make Investment Choices Between L2 and L1?

TechFlow Selected TechFlow Selected

Deep Dive into L2 Economic Models: With the Cancun Upgrade Approaching, How to Make Investment Choices Between L2 and L1?

This report explores the complexities of evaluating Ethereum Layer 2 solutions, providing insights into the economic factors underpinning their value propositions.

Author: Revelo Intel

Translation: TechFlow

Introduction: Understanding the Economics of Rollups

Ethereum's scalability roadmap is increasingly focused on rollup solutions, and with growing adoption and the anticipated EIP-4844, Ethereum Layer 2 (L2) solutions are gaining lasting significance.

However, evaluating L2 solutions is far from straightforward. Unlike L1 networks such as Ethereum, which have clear revenue streams from transaction fees and explicit costs from token issuance, L2 solutions present unique valuation challenges.

This report explores the complexities of assessing Ethereum Layer 2 solutions, offering insights into the economic factors underpinning their value proposition.

Overview

In recent years, significant technological advancements in rollup solutions cannot be overlooked. Since the emergence of rollup technology in 2018, substantial talent and research investment have led to remarkable technical progress, including EVM-equivalent rollup implementations, bridge technologies based on fraud and validity proofs, breakthroughs in batch data compression, and the introduction of rollup software development kits (SDKs). Notably, various rollup solutions such as Optimism, Arbitrum, Base, zkSync, and StarkNet have entered the market, fostering a thriving ecosystem and placing other Layer 1 solutions at a vulnerable and exposed position in the battle for market share.

Although current adoption rates meet expectations and demonstrate feasibility in attracting the next generation of users, the growth trajectory of Layer 2 solutions (L2) will accelerate in the coming months. With the upcoming EIP-4844 and the launch of new chains like Scroll, Linea, and Base, L2s are now in the spotlight.

EIP-4844: Cutting the Cost Tree

The upcoming Dencun upgrade brings a major feature—EIP-4844, also known as Proto-Danksharding—which marks a significant reduction in operational costs associated with rollups. While Danksharding specifications continue to evolve, EIP-4844 paves the way for a seamless transition within the Ethereum protocol architecture to accommodate future Danksharding implementations.

Current rollup implementations face two major challenges. First, there is a data storage bottleneck due to L2s processing millions of transactions daily, aggregating them, and submitting transaction proofs to Ethereum. Second, transferring transaction data from L2s to Ethereum incurs transaction costs.

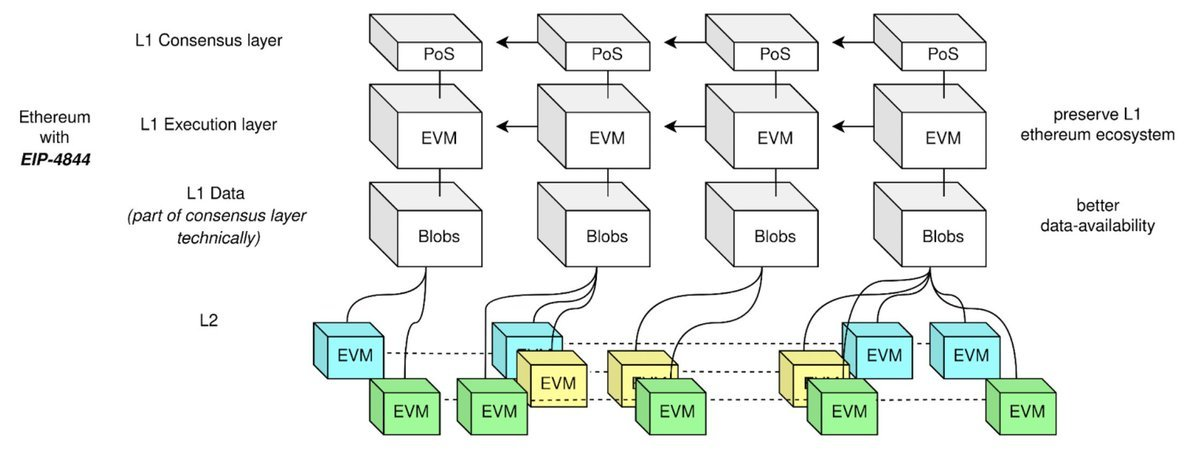

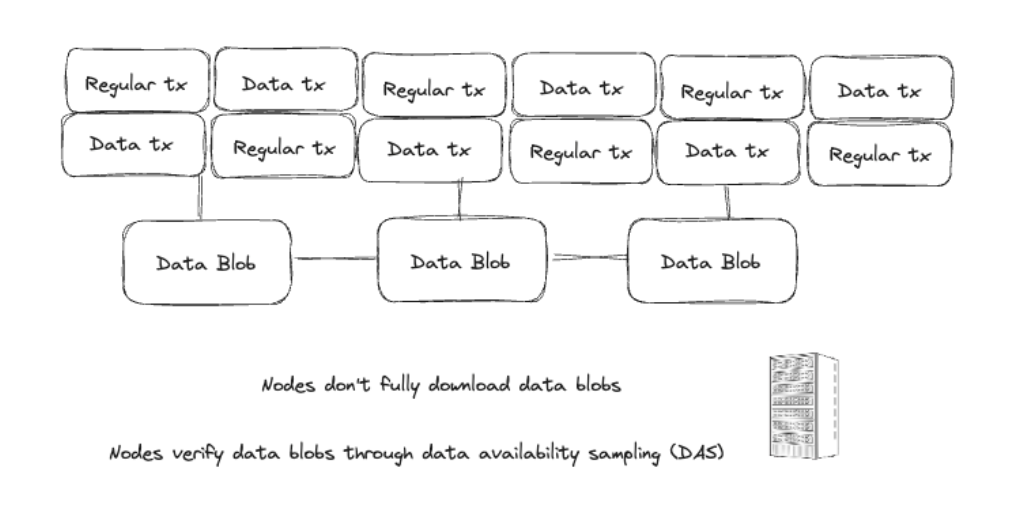

At the core of EIP-4844 is the concept of "blobs" (binary large objects). Essentially, blobs are data chunks associated with transactions, distinct from regular transactions. These blob data chunks are stored specifically on the Beacon Chain and incur minimal gas fees. They allow Ethereum blocks to include more data without increasing block size. Simply put, using blobs can increase data capacity by nearly tenfold compared to average block sizes.

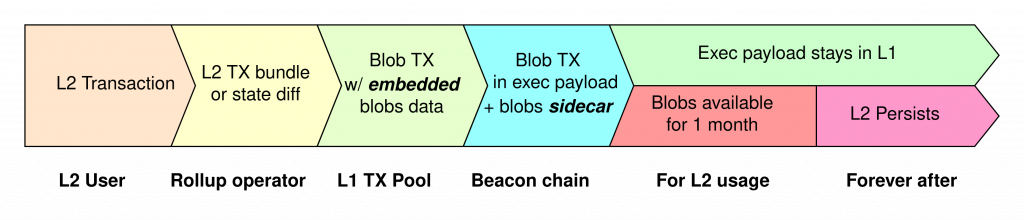

The primary purpose of blobs is to significantly reduce data availability (DA) costs, especially for L1 rollup data publication. Unlike traditional methods where all rollup data is stored in Ethereum’s calldata space, blobs provide an efficient and cost-effective alternative. Since the consensus layer manages blob storage, blob transactions do not impose additional requirements on validators. Additionally, blob data is automatically deleted after a proposed period of 30 to 60 days, aligning with Ethereum’s goal of scalability rather than indefinite data storage.

Before EIP-4844 implementation, L1 publishing costs accounted for over 90% of total rollup expenses. Looking ahead, EIP-4844 introduces the concept of "data gas," a new fee category for blob transactions. This separates the cost of publishing L2 data to Ethereum from standard gas prices. With dynamic pricing based on blob supply and demand, L2s can achieve significant cost reductions when submitting data to Ethereum, potentially reducing costs by up to 16 times or 90% of current gas fees.

Blobs are like data chunks that make Ethereum run more efficiently. They are stored separately, do not interfere with validators, and disappear when no longer needed. This means lower costs and more data space, making Ethereum faster and cheaper.

The Economics of Rollups

To understand the importance of EIP-4844, it is essential to grasp the business model of rollups. This upgrade leads to significant cost reductions, while revenue expectations may remain stable or increase with growing on-chain activity.

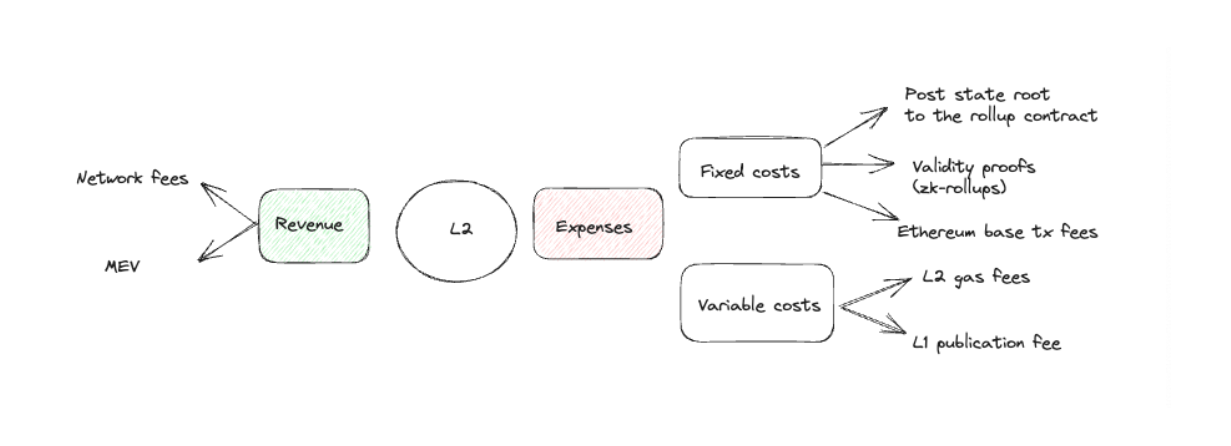

For a comprehensive understanding of EIP-4844’s impact on rollup economic models, it is necessary to analyze their revenue sources in detail. Rollups generate income from network fees and Miner Extractable Value (MEV), with MEV capital currently controlled by centralized sequencers who hold a monopoly on MEV.

On the cost side, rollups face fixed and variable expenses. Fixed costs arise from operations such as posting state roots to rollup smart contracts, ZK rollup validity proofs, and base Ethereum transaction fees. Variable costs include L2 gas fees and L1 publishing fees required for storing batch data on Ethereum.

EIP-4844 introduces a dynamic blob fee system, where fees are determined independently of block space demand based solely on blob supply and demand, differing from traditional fee models. As a result, post-EIP-4844 Ethereum fee markets include two dimensions:

-

Standard transaction fee market based on EIP-1559: This dimension retains the existing EIP-1559 fee market for regular transactions, with unique dynamics including base fees and priority fees aligned with EIP-1559 principles.

-

Blob fee market: The second dimension introduces a blob fee market where fees are entirely determined by current blob supply and demand. This creates an independent ecosystem separate from the standard transaction fee market, ensuring blob fees are unaffected by fluctuations in block space demand.

Analysis of the EIP-4844 fee market reveals several notable outcomes:

-

As the number of application-specific chains and general-purpose L2s increases, blob demand is expected to gradually rise. When demand exceeds blob targets, EIP-4844’s price discovery mechanism could lead to rising data gas prices.

-

During demand surges, data gas costs are expected to grow exponentially. If blob demand exceeds target levels, data gas costs will rapidly and exponentially increase, potentially multiplying tenfold or more within hours. Once blob demand reaches the target, data gas prices will grow exponentially every 12 seconds.

EIP-4844 changes how rollups earn and spend money. With dynamic blob fees, part of the fee market follows conventional rules, while another part adjusts according to blob supply and demand. As blob demand grows, so do gas costs.

Rollups as a Service

With the increasing number of application-specific chains, the Rollups as a Service (RaaS) business model is becoming increasingly important. For example, compared to application-specific chains on platforms like Cosmos, Ethereum Layer 2 offers clear advantages, primarily due to the emergence of RaaS solutions.

A key reason for this advantage is reduced infrastructure overhead. In the context of Ethereum Layer 2, this process is significantly simplified thanks to RaaS solutions. These services streamline the deployment, maintenance, and management of customized rollups, effectively addressing the technical complexities developers often face when developing on mainnets. As a result, RaaS enables developers to focus on application-layer development, enhancing their overall productivity.

RaaS also offers significant customization. Developers can not only choose their preferred execution environment, settlement layer, and data availability layer protocols but also gain flexibility in critical areas such as sequencer structure, network fees, token economics, and overall network design. This adaptability ensures RaaS can be tailored to the specific needs and goals of a wide range of projects, enhancing the versatility of Ethereum Layer 2 solutions.

We can distinguish two main service types:

-

SDKs (Software Development Kits): These serve as development frameworks for rollup deployment, including well-known options such as OP Stack, Arbitrum Orbit for L3s, Celestia Rollkit, and Dymension RollApp Development Kit (RDK).

-

No-code rollup deployment services: To simplify design, these services enable rollup deployment without deep coding knowledge. Solutions such as Eclipse, Cartesi, Constellation, Alt Layer, Saga, and Conduit fall into this category. They lower the barrier for developers and organizations to leverage rollup technology.

We can also include a third category: shared sequencer sets serving multiple rollups simultaneously, such as Flashbots’ Suave or Espresso.

Although current market conditions show limited demand for custom rollup creation, it is generally expected that RaaS could spark the emergence of hundreds to thousands of rollups as macroeconomic conditions improve and product-market fit becomes clearer.

RaaS makes developers' work simpler, faster, and more flexible. This allows them to prioritize and focus more on the core logic and business models of their applications.

Questioning the Utility of L2 Tokens

The success of rollup solutions such as Optimism, Arbitrum, Mantle, and zkSync is undeniable. However, from an investment perspective regarding rollup governance tokens like $OP or $ARB, the situation becomes more complex.

Bear Market: Limited Upside Potential

In traditional financial markets, shareholders enjoy a range of rights, including dividends, voting rights, and asset claims, giving stocks intrinsic value and making them attractive investments. In contrast, tokens representing only governance rights lack these guarantees, being limited to voting on governance proposals. Since sequencer revenue generated from transaction fees does not flow to token holders, network growth does not necessarily translate into increased token value. This raises legitimate questions about the value proposition of rollup tokens.

Although governance rights have inherent value, particularly in Layer 2 solutions where token holders wield significant influence—as shown by Optimism’s RPGF and Arbitrum’s STIP—the absence of dividends or other income sources makes them a different form of investment.

In today’s high-interest-rate environment, assets that do not provide tangible returns may be less attractive to conservative investors. Rising interest rates increase the cost of capital, making the opportunity cost of holding non-yielding assets more significant. In this context, ETH with stable staking returns might be a better choice for risk-averse investors, despite the growth potential of rollup tokens.

Bull Market: Growth Narrative

In financial markets, a company’s value is not solely tied to profits or dividends. For instance, growth stocks are valued based on their long-term growth potential and reinvestment strategies. Investing in rollup governance tokens can be similar to investing in non-dividend growth stocks. Historically, companies like Amazon chose not to distribute dividends but instead reinvested profits into expansion and innovation. Investors in such companies do not necessarily seek immediate returns through dividends; instead, they expect long-term growth and value appreciation. Taking Optimism and the $OP token as an example, there is a clear commitment to reinvesting profits into ecosystem growth, promoting increased demand for native dApps, sequencer revenue, and a virtuous cycle around RPGF. Moreover, with initiatives like Superchain on the horizon and continuous bandwidth expansion of the OP Stack, a powerful moat created by network effects will eventually become difficult to ignore.

Industry Outlook

L2s are evolving into a highly competitive arena, and implied expectations from airdrops can significantly influence user behavior within any given L2. However, it is crucial to recognize that the valuation of a specific L2 is inherently linked to the value of the L1, with network effects serving as the differentiating factor.

This connection becomes evident when examining the current operations of rollups. They collect gas fees in ETH and must pay data availability fees to Ethereum in ETH. Essentially, these rollups cannot execute their own monetary policies; Ethereum dictates how much they must pay to the underlying chain.

Therefore, L2s do not possess a unique monetary premium. Nevertheless, L2 tokens are not always traded in line with this reality. However, as long as they can build strong ecosystems and foster network effects, these L2s have the potential to become sovereign entities in the future, and the market may seek to anticipate and front-run this opportunity.

Airdrops can indeed influence user behavior. But the issue is: the value of L2s is closely tied to Ethereum (L1). L2s charge and pay in $ETH, so they don't have their own monetary rules. In this context, the current operational model of L2s is clear: they charge end users and retain a portion of these fees to cover Ethereum settlement and data availability costs. Holding the associated governance token essentially equates to owning a share of the profit margin generated by the L2.

Things become more interesting when multiple instances can be created, as in the case of Optimism. In such scenarios, the profit margins generated by these instances can flow back to token holders. For example, Base allocates 10% of its fees to Optimism.

This model unlocks greater scalability potential for L2 assets, setting a precedent for sharing a portion of fees with other chains as an implicit licensing agreement. This dynamic not only adds depth to the L2 ecosystem but also strengthens the value proposition of L2 tokens as they continuously evolve and adapt within the competitive landscape.

Current State

Currently, Ethereum trades at approximately $301.4 billion, and its value is expected to rise as rollups built on it grow. Additionally, the introduction of Rollup-as-a-Service (RaaS) is expected to bring a wave of general-purpose and application-specific rollups into the market.

But even though we can expect increased value for the base layer, L2s typically exhibit higher beta relative to $ETH. Furthermore, investors may view their tokens as bets on the entire ecosystem. We recommend caution with this approach, as individual projects commonly shift to the latest and most popular L2 at any given time.

Moreover, L2s are positioned to attract more users, thereby increasing value flowing back to Ethereum. This dynamic may follow a power-law distribution, although less pronounced than observed in liquid staking. Therefore, conversely, ETH may be the underlying asset investors prefer to hold. As more L2s enter the market, dApps ultimately spread across multiple L2s, making it increasingly complex to pick the winning chain. However, regardless of which L2 ultimately wins, ETH holders and Ethereum validators will benefit from increased rollup activity.

In summary:

-

Ethereum's value rises with the growth of rollup technology, and Rollup-as-a-Service (RaaS) will bring a wave of rollups into the market

-

L2 volatility differs from ETH, and projects can quickly switch between L2s

-

L2s will attract more users, benefiting $ETH holders and validators, but picking winners among L2s becomes complex

-

Ultimately, holding ETH may be the safest bet.

Do We Still Need Alternative L1 Solutions?

The era of rotating trades among L1s seems to be over. As L2 solutions effectively address Ethereum's scalability challenges, questioning the value propositions of other L1 blockchains such as Near, Avalanche, Solana, and Fantom becomes crucial.

A key distinction lies in the ease of launching total value locked (TVL). L2s have an advantage here because users and developers are already familiar with tools on Ethereum. They simply need to bridge assets to an L2 chain to take advantage of lower transaction costs. Essentially, TVL initially on Ethereum is merely seeking a more cost-effective transaction environment.

However, it is important to recognize that other L1 solutions still serve specific purposes and offer unique characteristics that may appeal to certain use cases.

-

Diversified Ecosystems: Other L1s cultivate their own ecosystems, often with distinct communities, projects, and innovations. These ecosystems may meet the needs of specific markets or industries.

-

Specialized Features: Some L1s prioritize features such as high throughput, low latency, or specific consensus mechanisms. These attributes may make them better suited for certain applications, such as high-frequency trading or gaming.

-

Diversification: From an investment standpoint, diversifying across different L1s can reduce risk. Although Ethereum remains dominant, other L1s may offer diversification opportunities. For example, investing in Solana can serve as a hedge against EVM (Ethereum Virtual Machine) dominance (imagine a zero-day vulnerability discovered in the EVM).

L1s that bring unique value to the ecosystem (such as Solana, Monad, etc.) will survive. Merely offering an EVM-compatible chain with lower gas fees is no longer sufficient. This may seem obvious now, but in the past, many instances existed where EVM-compatible chains with lower gas costs reached excessively high valuations. Take Moonriver, for example—an EVM-compatible chain on Kusama (Polkadot’s canary chain)—which reached an all-time high of $494 in Q4 2021 and now trades at $4.

In summary:

-

L2s reduce the need for L1 rotation trading. Although other L1 blockchains still serve unique purposes, L2s have an advantage in terms of total value locked (TVL) by offering familiar tools and lower transaction costs.

-

However, diversified ecosystems, specialized features, and diversification make other L1s still attractive for specific use cases and risk mitigation.

-

Surviving L1s will bring unique value beyond EVM compatibility and lower gas fees

Key Takeaways

-

Traditional valuation methods are better suited for L1s, with transaction fees as revenue and token issuance as cost. L2s present unique valuation challenges.

-

Although cryptocurrencies and stocks differ structurally, fundamental investment logic still applies—investing in assets with long-term growth potential can be an attractive strategy.

-

L2s operate by capturing spreads, and this model is strengthened when forming implicit revenue-sharing agreements with other chains, such as Base allocating 10% of fees to the Optimism treasury.

-

ETH can be seen as an "index" asset, while L2s function like individual "stock picks." Regardless of which L2s are most active, ETH holders and Ethereum validators will benefit from increased rollup activity.

Conclusion

One way to view this issue is that EIP-4844 will significantly reduce L2 costs, while their revenues are expected to grow over time. The difference between the two represents the profit margin of these L2s. As this gap widens, the likelihood increases that they will begin sharing these profits with token holders. If you are willing to wait for these pieces to fall into place, considering this logic in advance is a reasonable approach.

As we chart a path forward for rollup governance tokens like $OP or $ARB, it is clear that the field is poised for transformation. EIP-4844, the rise of ERC-4337, and the emergence of RaaS (including SDKs and no-code deployment services) signal an impending wave of rollup adoption.

This wave of adoption may see the rise of thousands, perhaps even tens of thousands, of rollups. However, investor perceptions of the value of these governance tokens are divided. On one hand, challenges such as the lack of traditional value capture mechanisms and the impact of high-interest-rate environments may limit the upside potential of rollup tokens. On the other hand, some investors may compare these tokens to non-dividend growth stocks like Google, Amazon, and Tesla, recognizing their potential for higher valuations due to long-term growth prospects.

As we enter a more competitive landscape, remaining adaptive is crucial, taking into account the evolving dynamics and unique characteristics of rollup governance tokens.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News