Correctly understanding the logic of crypto token issuance to avoid being the greater fool

TechFlow Selected TechFlow Selected

Correctly understanding the logic of crypto token issuance to avoid being the greater fool

How are tokens typically issued? Why are they fundamentally different from stocks?

Written by: Jack Niewold

Compiled by: TechFlow

The crypto market is like a seesaw. When sellers and buyers are perfectly matched, prices remain stable. But when more tokens are being sold while the number of buyers decreases, prices fall.

Meanwhile, during bull markets, everyone wants new tokens. As suppliers decrease and more people join, prices rise, creating FOMO and sharp price increases. The market constantly swings between buyers and sellers. Momentum pushes from both sides, creating bullish or bearish conditions.

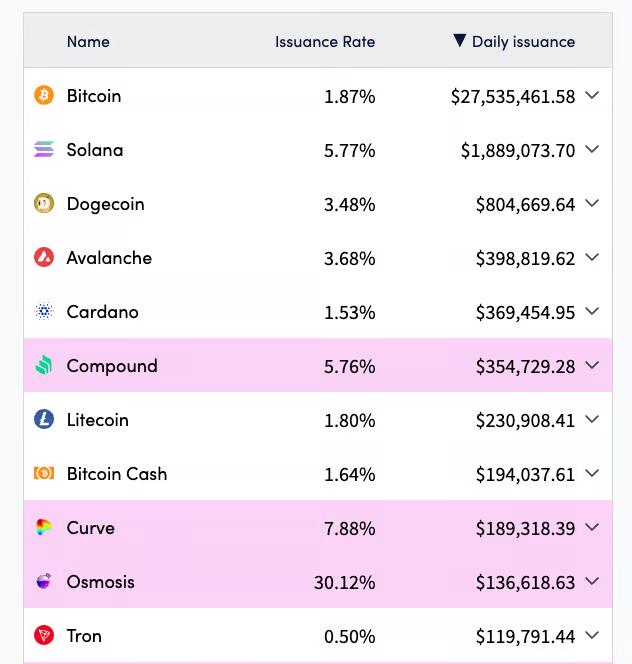

At least, that’s how it works in a simple market with fixed supply—but things are rarely this simple. Even Bitcoin has an annual inflation rate of about 1.87%. If we assume miners sell their entire supply while others simply hold their tokens, prices would still decline each year.

In short, unless a currency is net deflationary, new demand must drive price increases. This leads some to believe that crypto's steady state is slow leakage (bear market), with prices reflexively rising.

Meanwhile, traditional markets benefit from consistent capital inflows: monthly S&P 500 purchases, pension funds, stock buybacks. As a result, prices default upward; occasionally we experience reflexive downturns (crashes/recessions/bear markets).

But today, let’s discuss how tokens are typically issued, why they’re fundamentally different from stocks, how this usually harms investors, and what you can do about it.

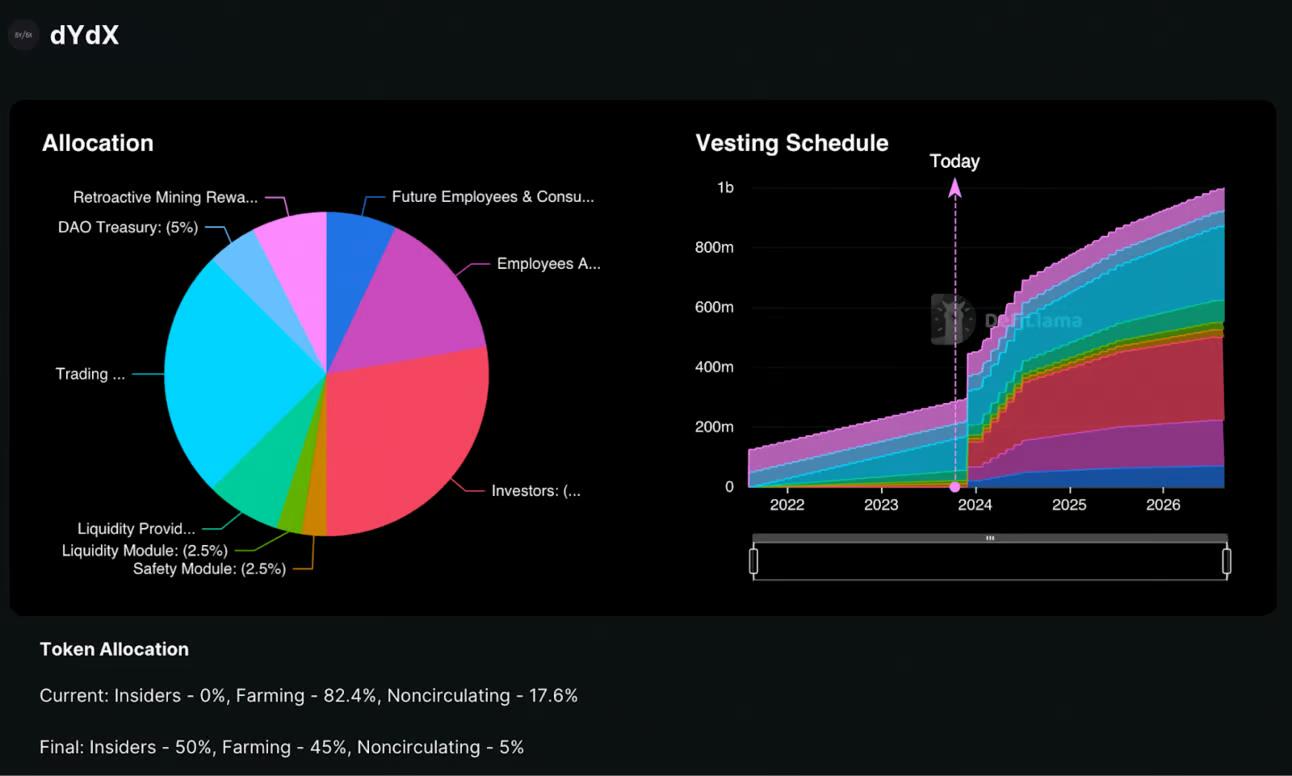

Let’s start with what many consider the worst offender: the perpetual futures exchange dYdX. Below is a chart showing its token inflation since late 2021.

Before 2024, we saw a gradual increase in token issuance, primarily due to liquidity incentives (necessary for exchanges to list tokens) and trading incentives. This makes sense, but it undoubtedly exerted downward pressure on price.

More severe was early 2024: investor unlocks, team tokens, employee rewards, and future advisor allocations all surged at an alarming rate. Not to mention trading rewards and liquidity incentives, which also increased (though less dramatically).

Let’s do a quick analysis: if we estimate today’s circulating supply at 300 million tokens, with a current market cap of around $300 million, and no new buyers enter, the price per token will drop significantly over the next four years. Assuming market cap remains flat, the price would decline by approximately 66%—a massive loss for anyone holding dYdX tokens.

On the other hand, founders often claim supply will decrease—or at least future releases will slow. Look at Binance’s CZ tweeting about burning Binance’s exchange token, BNB. While a small portion has been withdrawn from the market via buybacks, most of these “burns” involved tokens created in 2017 that were never actually released into circulation.

These actions have no real impact on supply and demand; those tokens were never owned by anyone, never traded back and forth, and never influenced the market price of BNB.

To be fair, I don’t think buyback-and-burn models are great either. Sure, they might temporarily boost prices, but I’d rather see that money spent on R&D, achieving product-market fit, and actual profitability (few crypto projects are profitable without token incentives). I believe profits should come from fundamentals, not artificial price manipulation.

Back to the original point: there are two reasons unlocks exist:

-

People want developers to be incentivized long-term;

-

People don’t want developers dumping tokens on them.

These are noble goals and worth pursuing. But getting this equation right is complicated. It involves market timing to some extent: I’d rather my tokens unlock during a massive bull run than during two years of decline. Game theory adds another layer: investors and founders often prefer having tokens now, regardless of long-term price.

Recently, I’ve seen an interesting mechanism for incentivizing founders: tokens are unlocked only upon reaching certain milestones—such as TVL, fee revenue, or user count. While these metrics can be gamed to some degree, it does mean founders must deliver real results before receiving their tokens. Sometimes investors are subject to the same terms: e.g., the protocol must achieve $100 million in TVL before tokens unlock.

As the industry matures, there’s growing disappointment over how retail investors have been treated over the past decade: if founders and investors want retail capital to return, they must prove their commitment to retail participants—which could ultimately benefit smaller investors.

On the flip side, we may see fewer VC-subsidized airdrops, reduced liquidity mining programs, and fewer unprofitable products. Either way, if the industry moves toward product-market fit, profitability, and operates more like traditional tech, it will be better for everyone.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News