Layer1 to Layer2: Exploring the Business Behind "Ethereum Layer2"

TechFlow Selected TechFlow Selected

Layer1 to Layer2: Exploring the Business Behind "Ethereum Layer2"

The L2 business can yield quick results—let's hope it doesn't end up draining the pond.

Produced by: TechFlow Research

Author: David

Building Layer 2 (L2) solutions has recently become a growing trend.

From emerging projects to established blockchains, everyone is actively exploring and implementing L2 solutions.

On July 17, Mantle Network—an Optimistic Rollup-based modular L2 solution incubated by BitDAO—launched its mainnet;

On July 18, Linea, the L2 solution developed by Consensys (the parent company of MetaMask), opened access to its mainnet Alpha version;

Earlier, Coinbase also announced the testnet for its L2 solution, BASE.

Recently, even the established blockchain Celo released a proposal on its internal forum advocating a shift from being an independent Layer 1 (L1) chain to becoming an Ethereum-compatible L2 solution.

Two years ago during the new blockchain race, various chains emerged as “Ethereum killers,” attempting to dethrone Ethereum. Today’s rush into L2 development reflects more of an “Ethereum Builder” mindset—using technical improvements to alleviate Ethereum's performance bottlenecks.

These are two fundamentally different approaches: direct competition versus elegant parasitism.

Why is everyone now rushing into L2s instead of launching new standalone blockchains? Has the appeal of new L1s faded, or do L2s truly offer compelling new narratives and financial incentives?

L2: A Faster-Return Business

We won’t dwell on L2 solutions like Mantle and Linea that were designed as such from the start—their narrative centers around improving Ethereum’s scalability, reducing fees, and enhancing user and application experience.

However, when an existing L1 like Celo chooses to transition into an L2, the immediate impression might be one of “compromise” or “backtracking.” Competing L1s aim to solve Ethereum’s shortcomings through radical innovation—“I can do it better”—whereas shifting to become an Ethereum L2 feels like surrendering and joining forces.

Let’s first consider what Celo itself says about this decision:

The benefits of compatibility, security, and liquidity are undeniable. However, in my view, these arguments don’t touch upon the core interests: What determines whether a project chooses to build an independent L1 or leverage Ethereum via an L2 strategy to stake its claim?

The answer lies in cost and return.

An article from Lightning HSL titled "Rollups Are a Good Business" offers a valuable commercial perspective: Whether building an L1 or L2, the goal is to solve problems and create value. But from a business standpoint, L2s appear more profitable.

Business Model: L2 → Functionally equivalent to Ethereum mainnet → Lower gas fees, faster speeds → Attract dApps and users → Increase on-chain transaction volume;

L2 Revenue: Gas fees paid by users for transactions on the L2;

L2 Costs: Operators periodically batch-roll transactions and post them to Ethereum L1, paying gas fees;

The difference between revenue and cost represents the gross profit of operating an L2 rollup. Therefore, the more applications and TVL (Total Value Locked) on an L2, the greater the potential transaction volume—and thus higher income with relatively fixed costs, leading to increased profits.

In terms of cost, rollups don’t require developing complex consensus mechanisms. Theoretically, they don’t even need native tokens (though most current projects have them), and could run with just a single server. Core technical components can be built using open-source frameworks like Optimism or Arbitrum—essentially plug-and-play solutions, making them significantly easier than building an L1 from scratch.

In contrast, developing a new blockchain (L1) involves much higher costs and complexity:

-

First, you must develop a market-accepted consensus mechanism, requiring significant R&D resources, time, and expertise;

-

Second, you need to attract enough nodes to ensure network security and decentralization;

-

Finally, you must craft a differentiated narrative—such as emphasizing privacy or security.

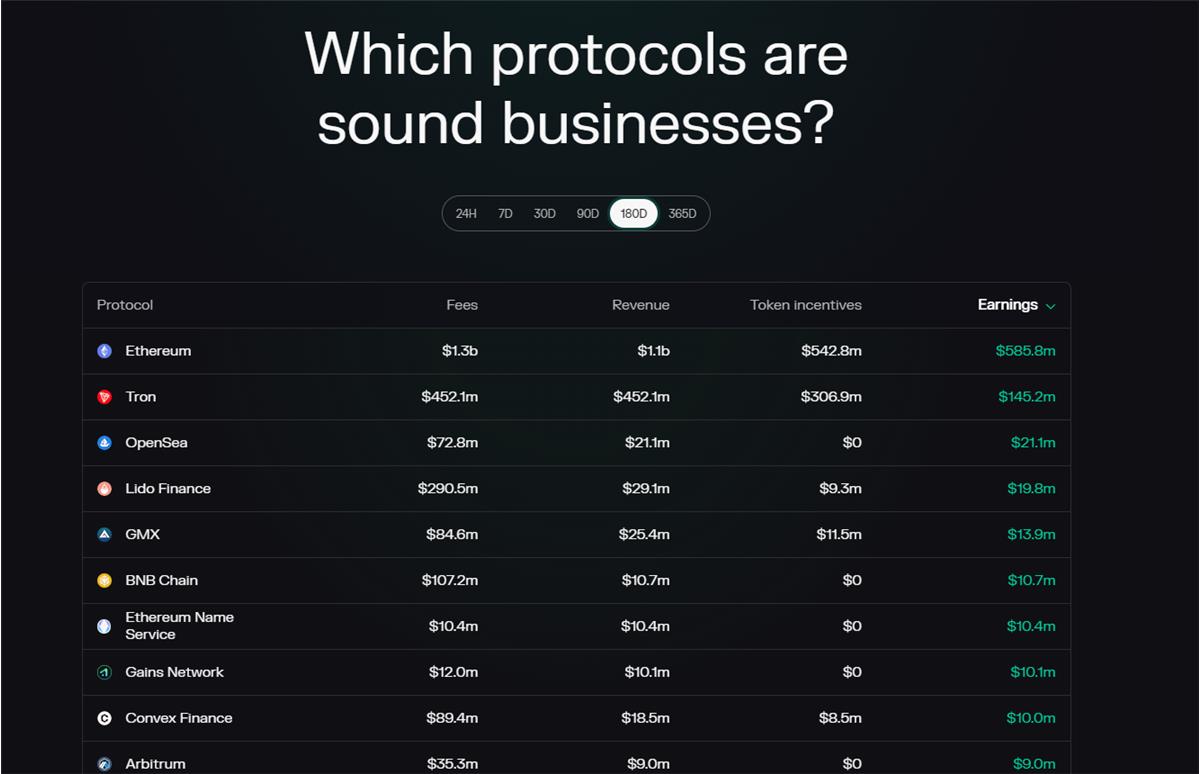

Moreover, data supports this cost-benefit analysis.

According to Token Terminal, among the top ten highest-revenue projects over the past six months, only Ethereum, Tron, and BNB Chain made the list at the L1 level—alongside Arbitrum, an L2. Considering the differences in development timelines, Arbitrum clearly outperforms in terms of revenue efficiency.

Additionally, in a bear market, it’s harder to raise funds from VCs and gain retail investor trust. Launching a new L1 inevitably faces hurdles from both primary and secondary markets. Monetizing tokens through capital markets becomes increasingly difficult—making L2 development a far more practical and lucrative alternative.

Rather than investing heavily and waiting long to build a unique chain from scratch, it’s more efficient to piggyback on Ethereum’s L2 ecosystem—with lower investment and faster returns.

More importantly, there’s the “traffic business”—where do users come from?

As mentioned earlier, TVL and transaction volume are key to L2 revenue, which ultimately depends on attracting users.

Companies like Coinbase, MetaMask, or Binance have a natural advantage—they can integrate their existing CEX or wallet user bases directly into their L2s, enjoying unparalleled user acquisition advantages compared to startups.

For L1s like Celo transitioning to L2s, they can migrate existing users—albeit requiring more incentives and guidance.

Regardless, most projects and capital entering the L2 space typically bootstrap from either their own product ecosystems or Ethereum’s existing user base, then expand into broader partnerships (e.g., Polygon’s moves in Web2).

Is L1 a Dead Sea, and L2 Approaching a Red Ocean?

The above discussion focuses on intrinsic differences between L1 and L2. But viewed from the external competitive landscape, the preference for L2 becomes even clearer.

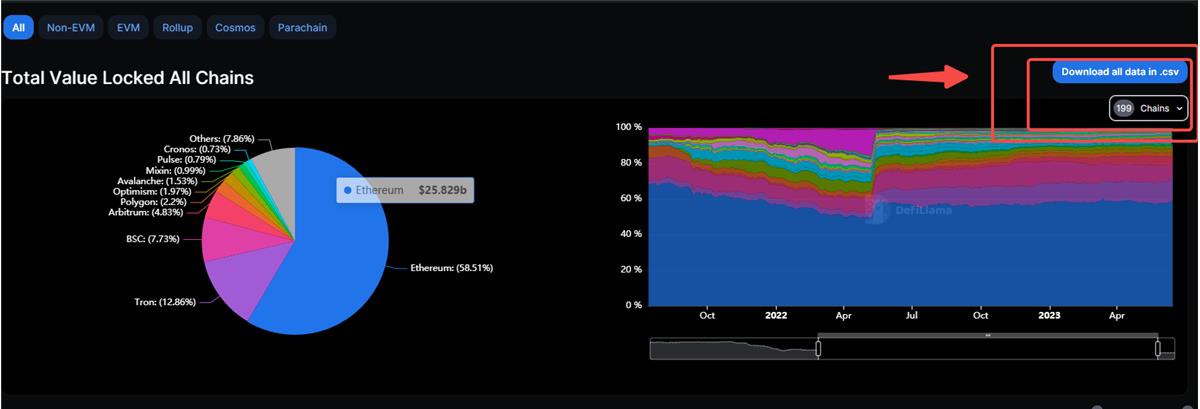

Data from DeFiLlama shows there are nearly 200 public blockchains currently in existence. Excluding dozens of L2s, this leaves approximately 190 L1s.

Thus, the L1 space resembles a dead sea: oversaturated and fiercely competitive.

Only a few chains dominate user mindshare. And given recent black swan events and capital outflows, many once-popular blockchains have vanished from key metrics dashboards—user activity, revenue, transaction volume, etc.

Most L1s still exist conceptually, but lack vitality. Jumping into this dead sea is hardly a sound business decision.

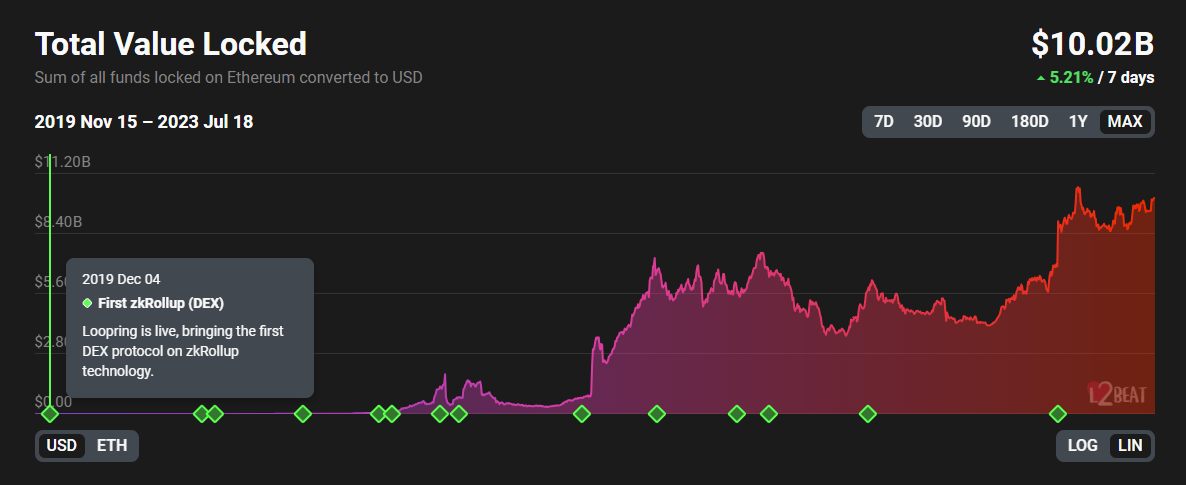

In contrast, the L2 pool looks slightly healthier.

Overall L2 TVL continues to grow over time;

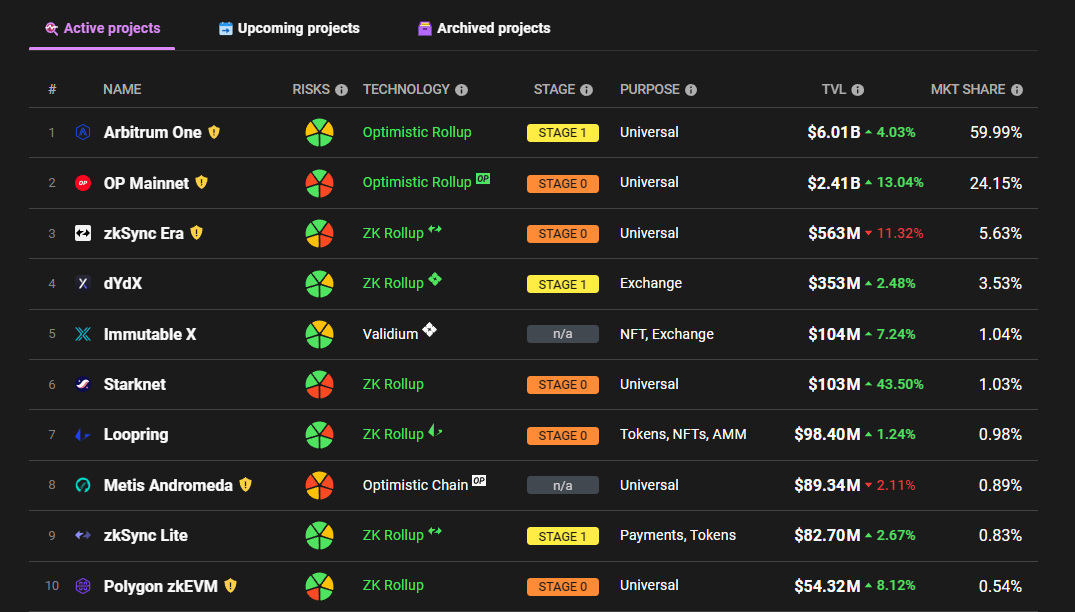

In terms of competition, L2Beat tracks 26 L2s—about one-seventh the pressure of the L1 space. While Arbitrum and Optimism lead in market share, other players have relatively scattered and balanced shares, leaving room for another major contender to emerge.

However, considering technical architecture, dominant representatives already exist across different stacks:

-

Optimistic Rollup: Optimism and Arbitrum;

-

ZK-Proof: Zksync and Starknet;

-

Built on OP Stack: Base;

-

EVM-compatible chain by Consensys: Linea;

-

Polygon’s ZK-EVM, etc.

It’s not a blue ocean, but compared to L1s, opportunities remain.

With Ethereum’s tech upgrades completed this year and future ones planned, performance-focused narratives will persist for some time—giving L2s a prolonged development window. Meanwhile, in a bear market where attention and funding are scarce, L2s enjoy sustained visibility and interest.

Therefore, from both competitive dynamics and external conditions, building L2s currently appears to be a profitable venture.

Who Is the L2 Business Serving?

Beyond the business angle, I sense a kind of redundancy within the ecosystem.

We frequently see projects migrating from one L1 to another, or expanding support across multiple L2s. Projects hop between chains, while the number of chains themselves keeps growing.

Switching ecosystems allows teams to re-stake territory, gather fresh resources, and capture new users. In a way, L1s and L2s resemble undeveloped colonies—ignoring technical nuances, the same business model can be redeployed elsewhere.

Do we really need so many “places”? Who are all these platforms serving?

Capital needs them, yield farmers need them, scams need them, narratives need them… but regular users probably don’t.

If every L2 pitches lower fees and faster speeds, what truly differentiates them?

After all, for end users, technical processes don’t matter—if outcomes are similar, increasingly commoditized L2s become interchangeable.

History shows that after each wave of new blockchain hype, Ethereum remains standing—and often emerges stronger.

Could the current L2 trend follow the same pattern? From blue ocean to red ocean to dead sea—a cycle of capital dumping, increasing project density, and eventually only one or two survivors floating atop a nearly empty pool.

The L2 business model offers fast returns—but let’s hope it doesn’t end in draining the pond dry.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News