80 Billion in Losses Take Down FTX, Wallet Security Solutions Are What Safeguard the Bottom Line of Web3

TechFlow Selected TechFlow Selected

80 Billion in Losses Take Down FTX, Wallet Security Solutions Are What Safeguard the Bottom Line of Web3

Regulation cannot solve all problems, especially at the upcoming turning point of Web3.

The collapse of cryptocurrency exchange FTX.com has triggered a Lehman-style crisis in the crypto industry, causing sharp declines in Bitcoin, Ethereum, and other digital assets. The crypto market has suffered severe damage, sparking widespread panic, extending the bear market, and making it difficult to determine when the bottom will be reached.

After hardship comes prosperity. R3PO firmly believes that the bull market lies ahead. During this long winter, where and how strength is accumulated will be key to whether vitality can flourish in spring. Visionary capital is increasing investments in infrastructure-related sectors.

R3PO believes it is time to rethink how we manage our assets more securely. Web3 wallets should also seize opportunities from this crisis. While the weak are fearful, the strong have already taken action. Cobo has planned to use MPC (Multi-Party Computation) for safer asset management. Only through advanced cryptographic technologies can our assets remain secure—this marks the coming-of-age ceremony for decentralization.

R3PO has conducted an in-depth analysis of the current Web3 wallet landscape, examining the wallet market from both an industry researcher’s macro perspective and a user-centric viewpoint focused on actual usability. The following keywords and insights reflect patterns observed during our research, offered for readers’ reference. For more detailed data and analysis, please refer to the full report.

1. Trend: Evolution toward smart contract-based, multi-chain, multi-signature wallets, with wallets becoming primary hubs for traffic and applications

2. Intelligence: Smart contract solutions will split into two technical paths: AA (Account Abstraction) and EOA + Contract

3. Security: Secure Multi-Party Computation (MPC) will become the foundational technology for multi-sig, co-management, and social recovery mechanisms

4. Usability: Combining Web2-like seamless, passwordless, recoverable experiences with Web3 principles of data ownership and privacy protection

5. Integration: Wallet + Cross-chain + DApp integration can build a fully decentralized DeFi ecosystem independent of CEXs

6. Richness: DApp Stores, services, B/C-end features, and Swap functions will become major revenue sources across various wallet types

Full Report

You own your assets only when you control your private keys.

This statement has become especially precious after the FTX collapse. In the journey toward decentralization, security has never been emphasized so highly. After Binance burst the bubble, it captured 70% of the spot market share—but is this really the future we envisioned for cryptocurrencies?

R3PO believes it is time to reconsider how we manage our assets. Web3 wallets should identify their opportunities amid crises. While the weak fear, the strong act. Cobo has already planned to adopt MPC for more secure asset management. Only through greater adoption of encryption technologies can our assets remain safe—this is the rite of passage back to true decentralization.

The development history of wallets has been extensively documented by many institutions and perspectives. However, during the recent Binance vs. FTX saga, we realized that wallets and on-chain data were the only means to uncover who the real "Pinocchios" are—not by listening to what they say, but by checking how many coins are actually in their wallets.

Deconstructing wallet evolution and technological routes from the product perspective allows deep understanding of core wallet concepts. But this represents only half the picture—the user experience forms the other half. R3PO finds that users care little about complex classifications or diverse technical approaches; instead, they focus on direct experience, which we summarize as security, usability, and functionality.

1. Security should meet bank-level asset protection standards;

2. Usability should match seamless experiences like Alipay or credit cards;

3. Functionality must fulfill users’ practical Web3 needs such as asset holding, DeFi participation, and NFT display.

This report eliminates outdated information (e.g., what paper wallets are) and removes “redundant” content such as non-leading projects. We aim to minimize noise and focus exclusively on the current landscape and future trends of wallets. Ultimately, whether technological or product-driven, everything must serve the user.

The report is divided into four parts: origin and classification of wallets, current wallet functionalities and extensions, future development directions, and overall market size of existing wallets.

Origin and Classification of Wallets

The 1.0 era of wallets can be categorized as “address-as-wallet” or “hard drive-as-wallet.” At Bitcoin’s inception, there were no dedicated tools for asset management. For example, Satoshi Nakamoto suggested using different wallet addresses for each transaction to preserve anonymity.

Before ASIC miners emerged, individuals could mine Bitcoin using personal computers, storing coins directly on hard drives—making hard drives the earliest form of hardware wallets.

The 2.0 era emerged alongside industrialized Bitcoin mining, as miners needed to store Bitcoin for profit-sharing with mining pools or awaiting favorable sale prices. This timing gap created real demand for wallets.

From 2009–2013, wallets offered only basic single-chain storage and withdrawal functions. Representative products included Bitcoin Core (Bitcoin-qt), a full-node, high-security wallet developed in 2011 that used private keys for management.

However, fundamentally, these were less like modern wallets and more akin to Bitcoin node synchronization software. Their heavy design prevented mainstream adoption.

The 3.0 era arrived with the rise of the Ethereum ecosystem.

Starting in 2014, with Ethereum’s emergence, multi-chain and smart contract wallets became dominant. Early examples include domestic wallets like Bitpie and imToken, while Gnosis Safe pioneered smart contracts and institutional asset management tools.

From 2018 onward, DeFi, NFTs, and richer DApps became mainstream trends. Beyond asset management, the primary function of wallets shifted to interacting with DApps—exemplified by MetaMask and meta-wallets like WalletConnect.

The 4.0 era is defined by smart contracts, multi-chain support, and multi-signature capabilities. With progress in Ethereum account abstraction, eliminating EOA accounts and retaining only smart contract accounts has become feasible. Multi-chain interoperability is gradually achieved via EVM compatibility and cross-chain bridges. Meanwhile, the growing popularity of MPC enables practical implementation of multi-signature functionality, significantly enhancing security and enabling social recovery. Key representative products include Zengo, Bitizen, and M-Safe.

We are currently transitioning from Wallet 3.0 to Wallet 4.0, with consumer-focused MetaMask and institution-oriented G-Safe serving as the main benchmarks to surpass.

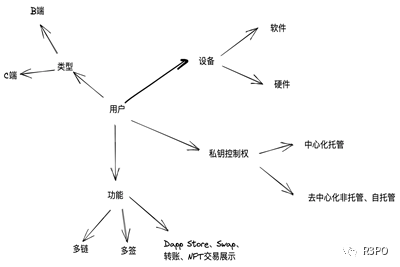

From a user perspective, wallet differences lie only in product and functionality. For instance, MPC provides security and multi-sig technology; G-Safe serves DAOs and institutions as a professional tool; everyday users mostly interact with leading consumer-facing software wallets like imToken—essentially C-end, software-based, decentralized, multi-chain wallets.

Image Caption: Abstract Classification of Wallets Source: R3PO

From the wallet’s own structural standpoint, classification dimensions are more varied—such as hot/cold storage or physical medium—but most wallets can be broadly divided into device-based and custodial types.

Current Wallet Functions and Extensions

From a macro perspective, wallet functions can be abstracted into three categories:

1. Traffic/Funds Gateway

In the crypto world, exchanges are the largest hubs for traffic and token trading. Following the NFT boom, NFT marketplaces may emerge as a second type of centralized exchange (CEX).

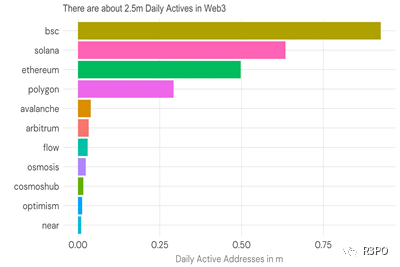

Data shows that 2.5 million wallets are active daily on top public blockchains, with BNB Chain, Solana, Polygon, and Ethereum accounting for over 80%.

Yet, comparing total CEX account numbers, exchanges currently hold 90 million active addresses—36 times more than on-chain active wallets. When expanding further to the Web2 world, platforms like Visa, MasterCard, and Apple Pay have account bases in the hundreds of millions to billions.

Put politely, on-chain wallets are still in early development; put bluntly, true decentralization remains far off.

Image Caption: Web3 Monthly Active Users Source: Dune

2. DApp Store / Connect / Swap

Currently, the main purpose of wallets is not “asset management”—at least, asset management only holds practical significance for institutions and DAOs. Individual users primarily use wallets to “interact” with DApps.

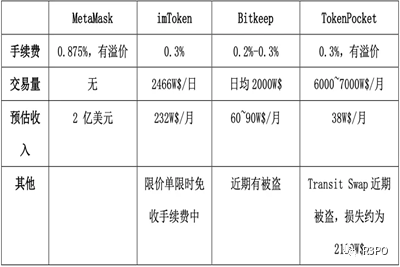

This can be further subdivided into connection models and ranking-based promotion models. MetaMask exemplifies the connection model, whose workflow consists of activation, interaction, and signing. It supports user-defined DApps and chains, making it inherently a multi-chain wallet—for example, supporting user-added chains like BNB Chain.

The DApp Store model, best represented by BitKeep, features in-app DApp displays, rankings, promotions, and direct listing of tokens/NFTs—a heavily operated approach aiming to monetize “user behavior.” This is a workaround in Web3 where data cannot be monetized directly. The traffic business never sleeps—it just changes its path.

Swap functionality is currently the most direct way for wallets to monetize traffic—more direct than DApp promotion and closer to end-users. For example, MetaMask’s sole direct revenue source is its built-in MetaMask Swap feature. However, this relies on its 30 million active users, making it hard for others to replicate.

3. Wallet Functional Expansion

Building upon these core functions, since 2021, wallets have increasingly integrated additional features—particularly those tied to individual identity, such as DID (Decentralized Identifiers), SBTs (Soulbound Tokens), and NFT displays.

Essentially, wallets serve as “containers” for accounts. Decentralized systems struggle with front-end KYC/AML procedures, and non-custodial C-end wallets technically cannot control user types. Thus, on-chain behavioral data becomes the primary tool for profiling users.

While still cutting-edge and challenging to implement at scale today, wallets represent a promising entry point for on-chain identity verification—especially as privacy protection grows in importance.

Future Development Directions of Wallets

We place wallet development directions ahead of market analysis because shifts in user experience will reshape the current market landscape. The wallet sector stands at another inflection point—an opportune moment for new entrants.

First, let us dispel technological mysticism. Whenever a new narrative emerges, technical hype follows a predictable pattern—Move language advantages, MPC’s role in wallet security, ZK’s universal applicability, etc. But this isn’t the whole story. Technology is merely a building block; it’s functionality that reshapes markets.

Earlier, we mentioned smart contract-based, multi-chain, multi-signature wallets. This concept can be broken down into the following equations:

Smart Contract Multi-Chain Multi-Sig Wallet = Usability + Security (1)

Usability + Security = AA + MPC + EVM Multi-Chain (2)

AA refers to Account Abstraction, primarily explored on Ethereum. Thanks to EVM-compatible chains and cross-chain bridges, this can be seen as a future trend.

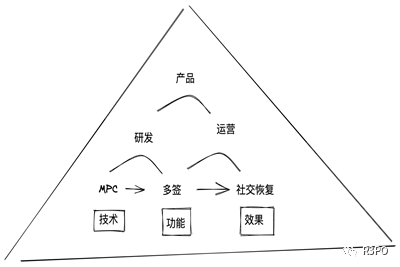

From a more complex functional standpoint, the future form of wallets involves a multivariate evolutionary process. Achieving a smart contract-based, multi-chain, multi-signature wallet through accumulation in MPC and other technologies, usability, and security is extremely challenging.

Image Caption: Relationship Between Wallet Technology and Products Source: R3PO

Discussing MPC alone isn’t difficult, but moving from technical principles to market competition requires a long product iteration cycle. Just as we know Layer 2 on Ethereum will likely emerge from ZK-based solutions, identifying the ultimate winning product isn’t something we can declare today.

Secure Multi-Party Computation (SMPC or MPC) primarily addresses how to securely compute a predefined function without a trusted third party. In MPC-based multi-signature schemes, a single private key never exists in full. Instead, multiple private key shards are distributed among participants, who jointly compute the final signature via MPC protocols. This signature can then be verified against the corresponding single public key.

Key players include Fireblocks (B2B), ZenGo (B2C), and Safeheron (middleware providing security services to MetaMask).

Fireblocks

Fireblocks provides a digital asset custody platform to 1,300 large institutions, offering MPC wallets, token issuance/management, and DeFi access. Clients include banks, exchanges, lending platforms, hedge funds, market makers, and other financial institutions. It supports private key export, enabling exit mechanisms.

One client, Revolut (valued at $5.5 billion, one of the largest fintech firms), uses Fireblocks’ MPC technology to introduce crypto services to its 13 million global retail customers. This infrastructure provides a secure payment rail for digital asset transfers. Through MPC wallets, Revolut can expand its crypto product lines and retail-facing features.

ZenGo

Zengo is a relatively mature, MPC-based, keyless EOA wallet. It recently raised $20 million in funding from Insight Partners, Samsung, and others. Samsung’s investment gives Zengo significant distribution advantages through Samsung devices. Upon account creation, Zengo generates two key shares—one stored on the user’s device, the other on Zengo’s server. For exit mechanisms, Zengo designed a private key recovery procedure entrusted to a trusted third party. If Zengo ceases operations, the third party verifies and releases the recovery protocol, allowing users to regenerate and export their private keys locally.

Safeheron

Already partnered with MetaMask to provide comprehensive MPC solutions. Its current product suite includes:

1. MPC Wallet App: Enables internal teams to collaboratively manage digital assets;

2. MPC Wallet API: Allows clients to automate transaction signing without risking private key exposure;

3. MPC Web3 Browser Extension: Enables multi-party approval workflows for accessing Web3 protocols.

From this perspective, sketching out the technology is just the beginning. Rapid product iteration and responsiveness to market demands are ultimately what solve problems—an ongoing process where operations outweigh pure technology.

This does not mean technology is unimportant. Rather, it emphasizes that technology is only the first step—market adoption remains the ultimate judge of its practicality.

Viewing wallet evolution through smart contract accounts, the clearest trend is the unification of Ethereum account types—merging EOA (Externally Owned Accounts) and smart contract accounts into a single “account abstraction.” Note: here, account abstraction refers to smart contract accounts that retain all EOA functionalities.

Key characteristics of smart contract wallets include:

Seedless

Contract wallets do not possess private keys and require no seed phrase backup. Ownership is established via on-chain code binding user-specific information (e.g., device ID, email). This eliminates the risk of losing encrypted assets due to lost mnemonic phrases, achieving truly keyless storage.

Multi-Signature Support

CA accounts support programmability, enabling easier implementation of multi-sig mechanisms. For example, M-Safe creates multi-sig wallets based on different addresses, allowing organizations to jointly manage assets with transfer controls, transaction approvals, and audit trails.

Gasless

CA accounts allow gas fee sponsorship, preventing failed transactions due to insufficient fees and improving user experience. However, under extreme network congestion, fees may spike dramatically—especially since smart wallets involve more complex logic than EOA wallets, making wallet creation and every operation more expensive. Sustainable product design is essential. For instance, Argent once paid over 50 ETH in gas fees during volatile conditions. To address this, Unipass adopts a sponsor-pays-gas model for new users and plans to introduce fee-offset mechanisms to enhance user experience while ensuring long-term operational viability.

Once fully realized, CA accounts will accelerate the move toward keyless wallets and enable gasless interactions with complex DeFi products.

However, currently, no fully functional AA-compliant wallet has launched. The closest are G-Safe and M-Safe. G-Safe is an EVM-layer smart contract wallet, while M-Safe is natively built on Move language—technically closer to the base layer but still in early promotion stages with questionable EVM compatibility.

In summary, MPC enhances security in keyless environments, while AA enables sophisticated smart interactions.

Overall Market Size of Existing Wallets

According to a new report by Grand View Research, the global cryptocurrency wallet market is expected to reach $48.27 billion by 2030, growing at a CAGR of 24.4% during the forecast period.

A report by Triple-A estimates that as of 2022, there are over 320 million cryptocurrency users globally. As of August 2022, the number of cryptocurrency wallet users reached 84.02 million, up from 76.32 million in August 2021.

Within the crypto space, user conversion remains possible. Current wallets have not yet gained full trust, and most people still rely primarily on exchanges to manage assets.

Key drivers include El Salvador’s Bitcoin legalization, the rise of DeFi and NFTs. Since September 2021, 2.7 million Salvadorans have adopted the Chivo wallet, enabling direct Lightning Network payments.

Beyond blockchain, broader factors—including mainstream adoption of DeFi, breakout success of NFTs, and national recognition of Web3 and metaverse concepts as new economic engines—are collectively driving wallet user growth.

Breaking it down, key trends include:

1. Growing merchant support: For example, Lightning Network payment provider Strike continues acquiring users in Latin America. According to BitPay, 40.0% of merchants accepting crypto are new, and their average purchase amount is twice that of credit card transactions.

2. C-end users drive volume, B-end users drive profits: Individual users accounted for over 62.0% of revenue in 2021, with North America dominating the wallet market, contributing over 30.0% of revenue.

3. Victory of usability: Hot wallets accounted for over 55.0% of revenue in 2021; Android-based wallets captured 45.0% of revenue, underscoring the importance of accessibility and ease of use—especially among lower-income groups—and highlighting critical data supporting UX-centric design.

4. Swap remains a key revenue stream: Swap generated over 40.0% of revenue in 2021.

Image Caption: Wallet Classification Source: R3PO

Conclusion

As the cryptocurrency market reaches another decisive moment, the harm caused by opaque practices at CEXs continues. User funds can only be truly owned when they circulate on-chain; otherwise, repeated misappropriation will persist—no one adheres to principles when facing profit.

Regulation cannot solve everything—especially at this pivotal juncture for Web3. The industry must have the courage to deliver better solutions. Wallets represent the ideal solution for personal and institutional asset management. It is time they take up this historical responsibility. What fortune offers, if not taken, brings consequences.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News