A Quick Overview of the New Landscape in Lending: What's Changed for New and Established Lending Projects?

TechFlow Selected TechFlow Selected

A Quick Overview of the New Landscape in Lending: What's Changed for New and Established Lending Projects?

Which project will lead lending in the next cycle?

Written by: Mikey 0x

Compiled by: TechFlow

Over the past few months, the DeFi lending landscape has undergone significant changes, and I believe it's important for people to catch up on some of the latest developments in this space. This article provides an overview of new protocols, key statistics, and which projects are likely to lead lending in the next cycle.

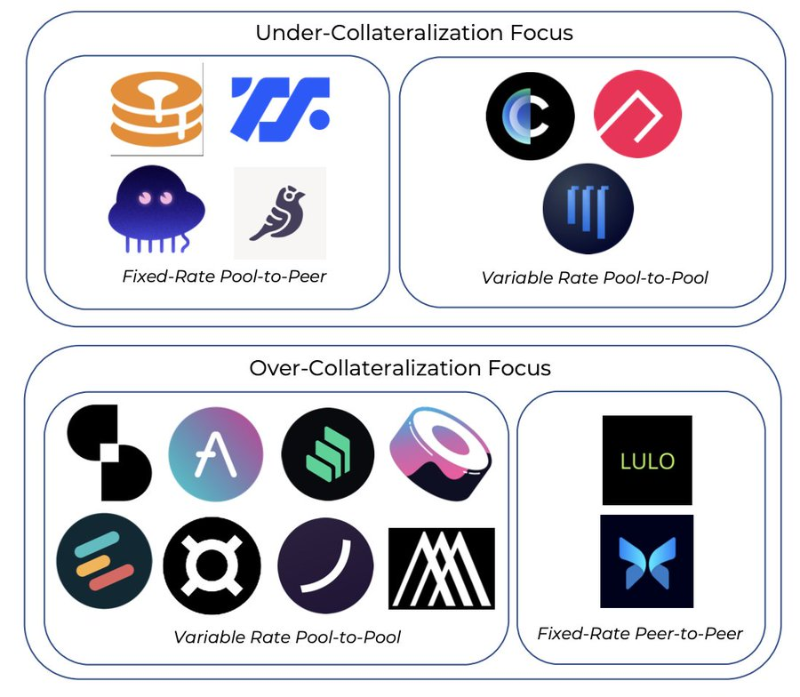

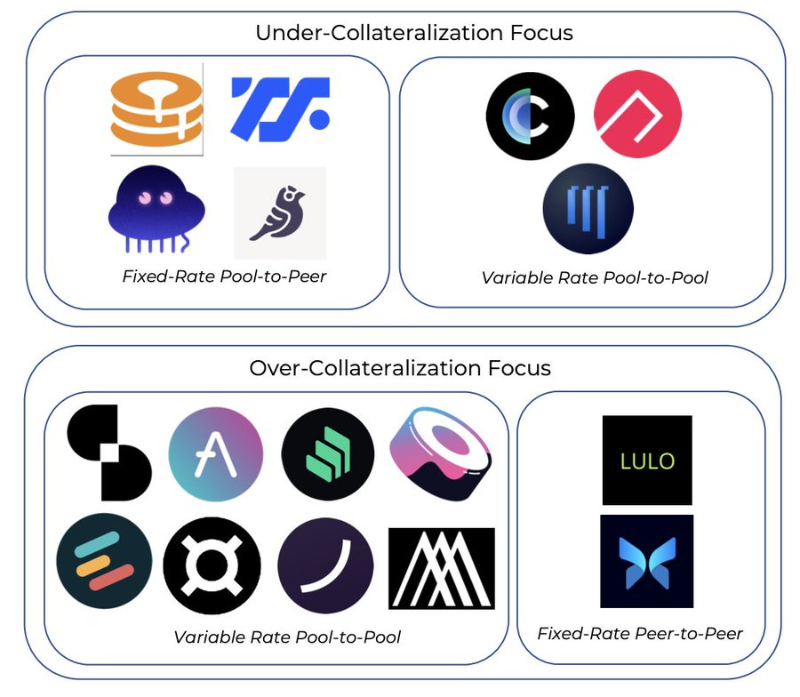

New Lending Protocols:

DammFinance and RibbonFinance are undercollateralized floating-rate lending protocols. They resemble Aave’s pool model in nature, offering frictionless deposits and loans.

dAMM currently supports 23 assets, with Ribbon set to launch soon.

Lulo is a P2P order book protocol on-chain, featuring fixed interest rates and term loans. Similar to Morpho, Lulo eliminates the traditional lender/borrower spread found in pool-based models by directly matching counterparties.

ArcadiaFinance is a lending protocol that allows borrowers to deposit multiple assets (ERC-20s and NFTs) as collateral into a single vault. These vaults are represented as NFTs, enabling composable second-layer products, while lenders can select risk profiles based on vault quality.

Arcxmoney is a lending protocol that evaluates borrowers based on their on-chain transaction history. The better the track record (i.e., no liquidations), the higher the maximum LTV—up to 100% LTV so far. Lenders provide liquidity based on the borrower’s credit risk.

dAMM and Ribbon compete directly with Maple and Atlendis in the institutional (undercollateralized) lending space.

Arcadia, ArcX, and Frax represent variations of existing models we’ve already seen in the sector.

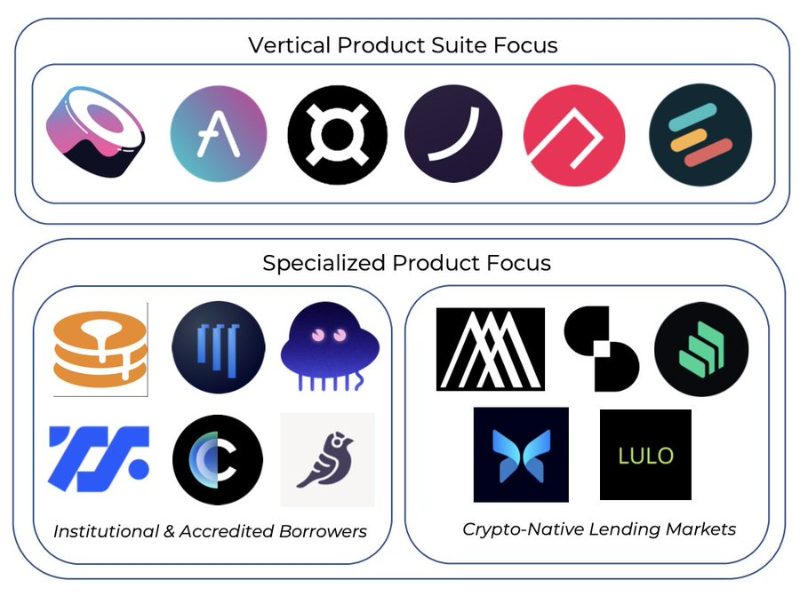

Many protocols continue to pursue verticalization in an effort to deepen moats and capture more value:

- Frax: Stablecoin, AMO, AMM, liquid staking

- AAVE: Stablecoin, undercollateralized loans, RWAs

- ArcX: Credit scoring

- Ribbon: Vaults + lending

Some lending protocols focus more on serving long-tail assets. In the institutional space, dAMM is currently the only one supporting many long-tail assets. Eulerfinance allows borrowing and lending of any asset, with some eligible for collateral.

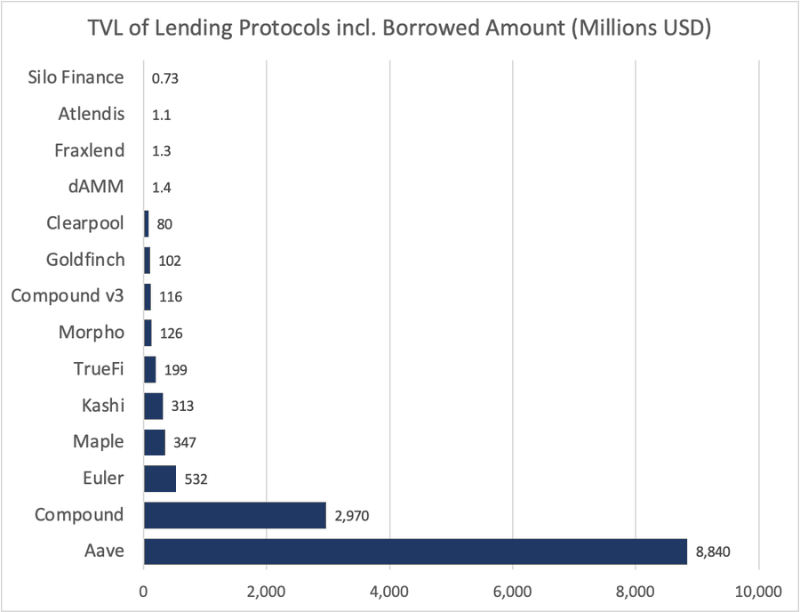

So far, AAVE is the clear winner, partly due to its aggressive multi-chain deployment—37% of its total TVL resides on L2s or EVM-compatible chains. COMP v3 has been slow to migrate funds from v2, which remains firmly in second place. Maple is the most popular undercollateralized lending protocol.

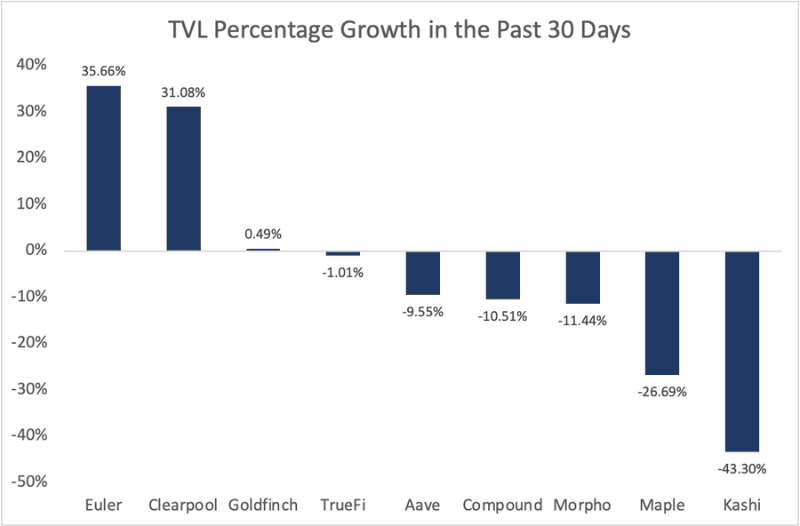

Over the past month, Euler and Clearpool were the only two semi-mature platforms to experience notable growth.

AAVE and Compound sit in the middle, while Kashi has shrunk the most.

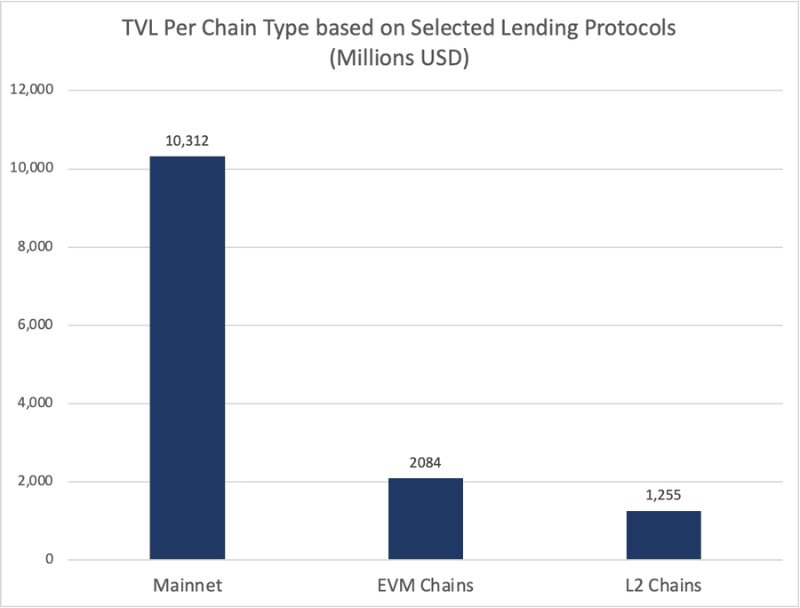

The majority of lending TVL remains on Ethereum mainnet, but EVM chains and L2s have been slowly gaining market share.

In the next cycle, increased L2 usage and a growing number of projects will accelerate demand for leverage, thereby boosting overall liquidity.

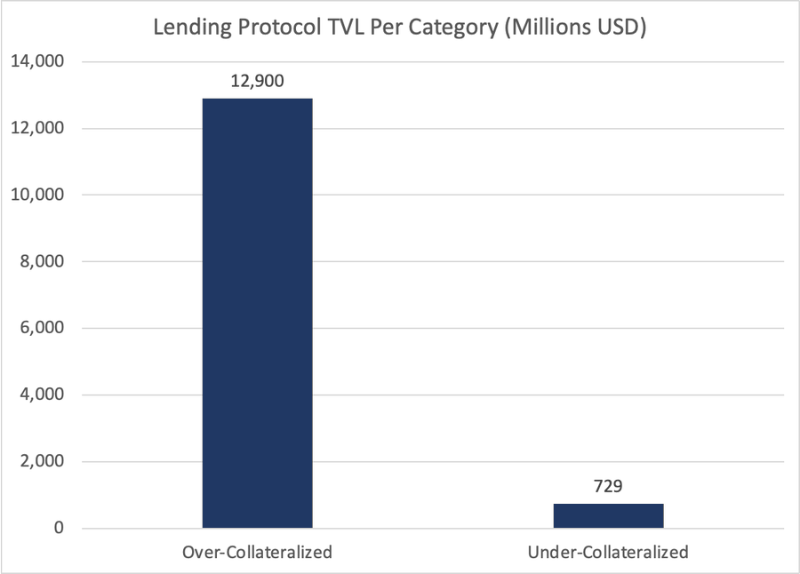

In terms of TVL per category, overcollateralized models have dominated so far.

This gap is expected to narrow significantly as KYC and ZK-based identity solutions unlock new use cases and more institutional capital enters on-chain markets.

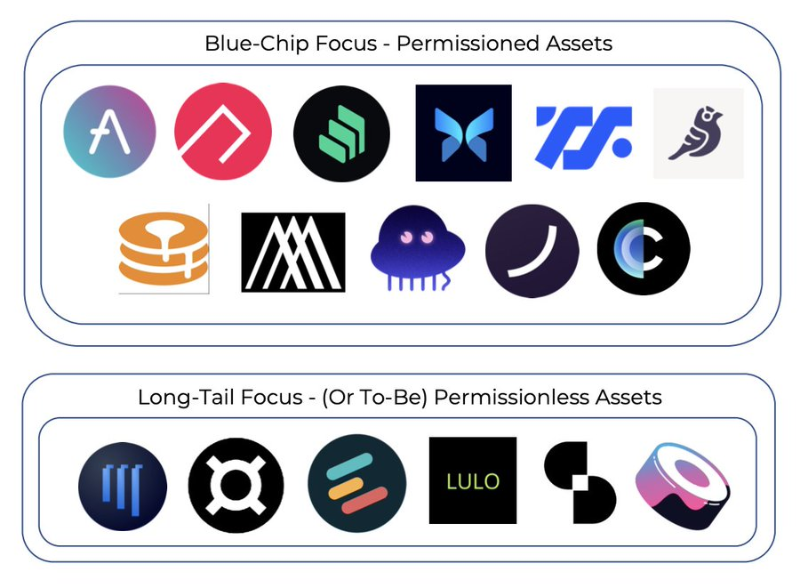

Regarding blue-chip versus long-tail asset lending, blue-chip assets currently represent nearly all of the available liquidity.

Euler is the most prominent protocol focused on long-tail assets, yet its long-tail asset TVL remains below 5%, primarily due to the opportunity cost of token collateralization.

Why deposit $GRT tokens into Euler when (non-liquid) staking can yield 10–30 times higher APR?

This will change over time as we see more liquid staking derivatives emerge in Web3 and DeFi, allowing tokens to simultaneously earn yield and be used as collateral.

Verticalization is an interesting trend observed across DeFi—not just in lending. Market share concentration is increasing, much like Lido, Uniswap, and MakerDAO, which dominate their respective categories.

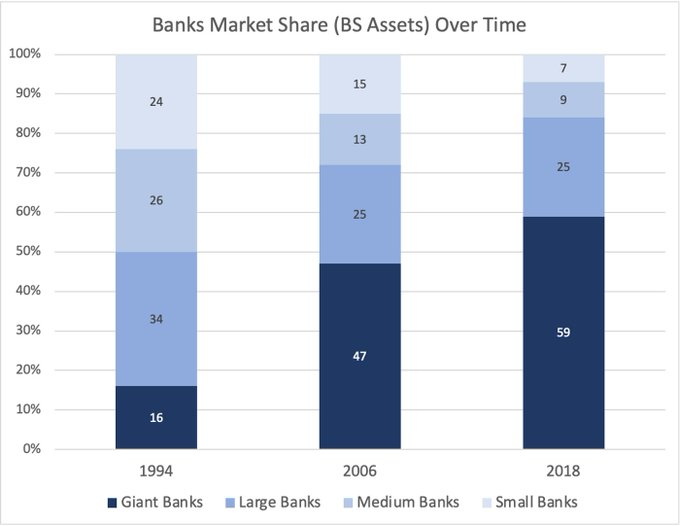

Over time, we may see DeFi (and lending) continue to consolidate—similar to how large banks have steadily grown over the past decades.

There are three key reasons:Strong network effects, verticalization (turning products into features), and brand moats.

New Lending Experiments:

1) Undercollateralized loans using zk proofs of off-chain collateral (linked with KYC)

2) Loans using socially contextual NFTs as collateral

3) DAO-focused lending

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News