Will moving toward mobile be the breakthrough opportunity for Web3?

TechFlow Selected TechFlow Selected

Will moving toward mobile be the breakthrough opportunity for Web3?

Whenever regulatory authorities attempt to create laws around technology, it indicates that the field has become a focal point, especially in emerging markets.

Written by: Joel John

Translated by: TechFlow

Bear markets are a good time to consider getting into cryptocurrency. Working in an industry that never sleeps comes with social, mental, and physical costs.

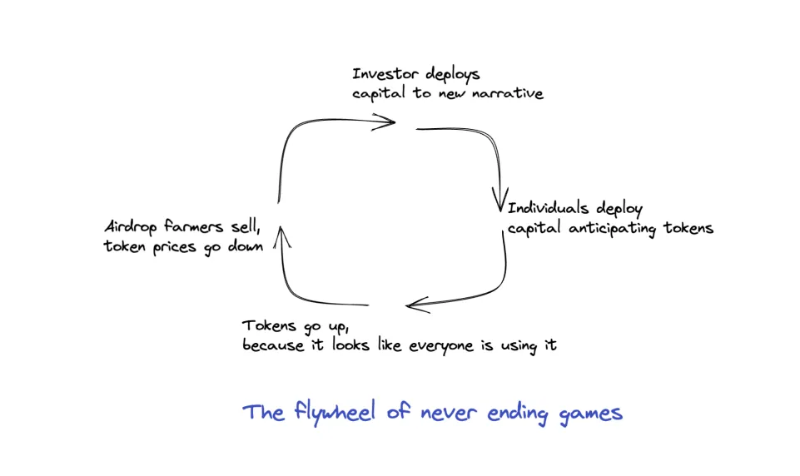

Due to how tokens work, the definition of a "successful" founder in the blockchain ecosystem differs slightly from that in the traditional world of the past.

You may frequently see founders without products, users, or business models earn incredible sums for themselves and their investors—entirely based on hype.

In crypto, you don’t need appeal, sticky users, or revenue to run a “billion-dollar protocol,” and many so-called meaningful “successes” make no meaningful difference to lives outside the industry.

Whenever regulators attempt to legislate around technology, it signals that the field has become a focal point, especially in emerging markets.

I would argue our industry is a case of Peter Pan syndrome: someone with an adult body but a child’s mind. It describes a dilemma: even though the games we play often feel technologically immature to founders, investors, and users alike, as long as capital can be made from these games, players will remain and the games will continue.

But reaching the scale of Coinbase, FTX, and Binance requires years of effort across different forms of capital.

Over the past five years, consumer-facing mobile apps have been the biggest driver of growth in the industry, explaining why Wyre and Moonpay are valued at $1.5 billion and $3.4 billion respectively—they serve as key infrastructure enabling apps to reach retail users via small transactions, primarily through mobile devices.

If cryptocurrency is to move beyond Peter Pan syndrome, it must reach ordinary people who don’t care about private keys and protocols. Our path to unlocking the next trillion dollars lies in understanding what people outside Twitter actually want.

This article is an initial exploration of motivations, macro trends, and opportunities—hopefully useful for founders looking to build in this space. With that context, let’s dive in.

Why PCs?

To understand why most Web3 applications today are PC-focused, recall that much of today’s crypto user base likely entered between 2017 and 2019. That era saw roughly $25 billion flow into over 8,000 ICOs—a golden age where anyone could trade and quickly profit. But like most trading, your edge depended on how fast you accessed information.

Back then, the average user experience revolved around ICOs, hoping they’d list at a high multiple. Once a token listed, you’d hunt for the next ICO to deploy funds. This was very different from pre-2017, when you could only transact (send/receive) or trade digital assets. That’s when wallets like MyEtherWallet and MetaMask began capturing market share.

As the DeFi ecosystem evolved into today’s behemoth, desktop-based applications became the standard interface for users to interact with the industry.

In my view, two reasons explain this:

- First, securely deploying large institutional capital into DeFi protocols to accumulate TVL required robust infrastructure. This was typically only possible via browser-based wallets like MetaMask, where interacting with smart contracts and adding new tokens was easier through desktop interfaces.

- Second, flywheel incentives pushed developers to build for the few users holding most of the capital. Products didn’t need to emphasize end-user experience because their primary goal was absorbing as much TVL as possible. Unfortunately, this also meant most users entering the ecosystem couldn’t access these new DeFi primitives throughout much of 2020.

Why shift to mobile?

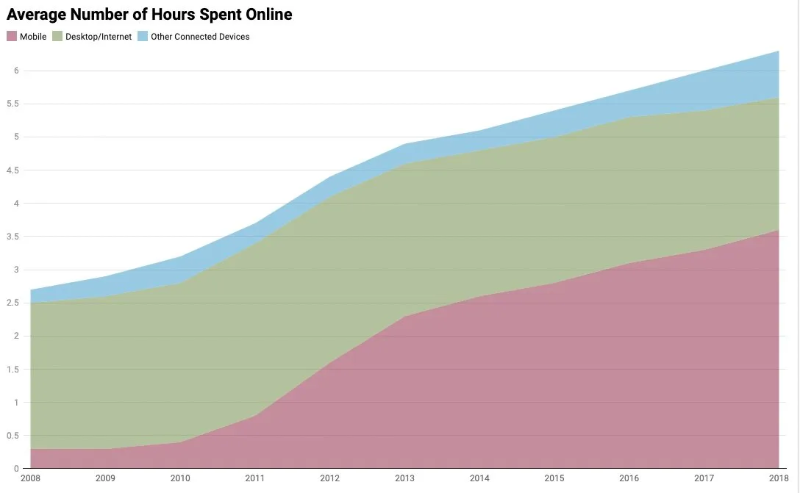

I view mobile devices as the distribution medium for Web3 applications because they command human attention better than any other device. Even when using attention-consuming devices like TVs, smartphones hold the upper hand. They’re the interface through which we learn, date, entertain ourselves, buy groceries, pay bills, and discover new ways of being. By 2013, internet usage via mobile had already surpassed that via laptops or desktops.

Building on mobile also allows those previously excluded—or barely able—to experience ownership. Mobile-first apps accelerate digitization, reduce costs, and make services more accessible.

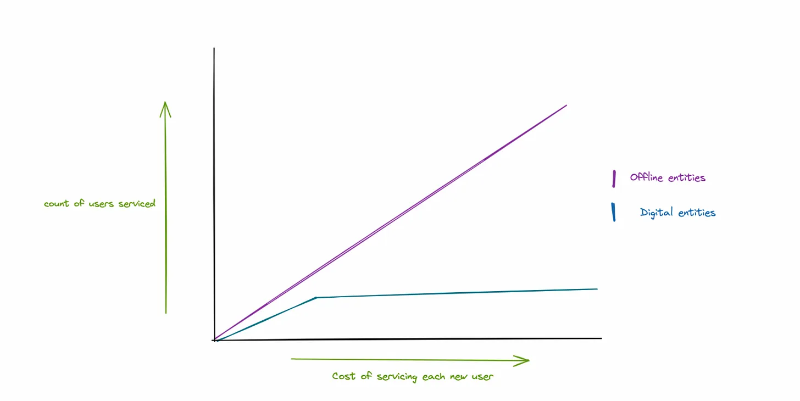

Historically, access to complex financial products and ownership tools involved high-cost, low-margin offerings. This explains why banking the unbanked was historically such a big challenge: employee hours scaled linearly while customer bases grew exponentially. Without digitization, serving growing user bases demanded enormous time investments, forcing banks to screen customers carefully.

Traditionally, a lender issuing loans to ten thousand users meant proportionally hiring credit evaluators. When digital banks emerged, AML/KYC and distribution scaled exponentially, drastically reducing time spent—allowing platforms to grow with smaller teams. As user bases expanded, the cost per additional user dropped significantly.

Take Compound and Aave as examples: because their smart contracts run on Ethereum, operational costs are far lower. DAOs don’t operate infrastructure themselves (that’s handled by the underlying blockchain), nor do they incur credit assessment or AML/KYC costs.

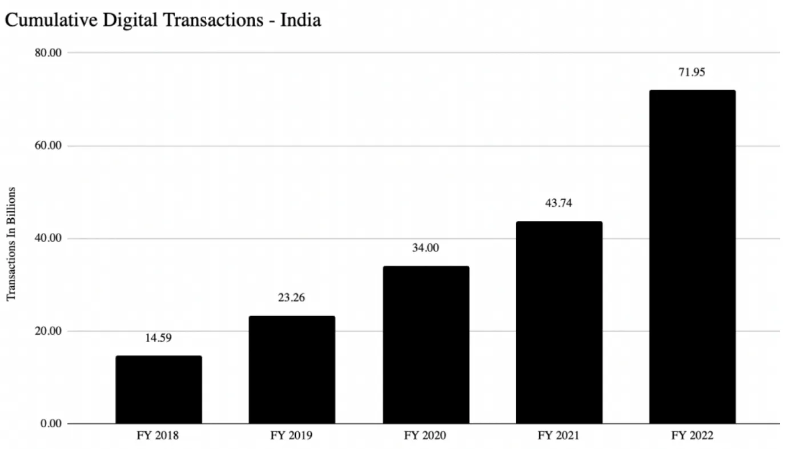

Digital banks disrupted the unit economics of inclusion. Suddenly, banks no longer needed physical branches in remote regions. Instead, they could reach users via mobile connectivity, conduct KYC remotely, and deliver banking services. Nowhere is this clearer than India, where a state-owned payment network called UPI grew from $4 billion in monthly transaction volume to over $120 billion within four years. Indians now conduct 72 billion digital transactions annually.

DeFi promises everyone access to investment-grade financial products. This echoes the ICO promise—that anyone could invest in early-stage projects. Broadly speaking, this is true—but it overlooks the fact that people generally prefer simplicity, “set-and-forget” solutions over ones requiring constant monitoring. I have a compelling example: JarHQ from India. The app consistently ranks among the top 20 in UPI transaction volume in the region. Why do users transact so much? To buy gold—starting at just $0.05.

Historically, buying gold in India was an elite activity—people spent large sums for relatively small quantities. Jar disrupted its unit economics by focusing on digital gold custody, dramatically lowering entry costs. Users flocked in, scaling at speeds most traditional, store-first competitors couldn’t match.

How does this translate to DeFi? In my view, most founders have shifted toward building products for institutions. Why? Because you can ignore user experience, focus on a handful of clients, and claim billions in TVL. Since your customer base consists almost entirely of experienced financial managers, little effort goes into user education.

This makes commercial sense—after all, the vast majority of volume still comes from desktop users. On the other hand, exchanges report nearly 90% of their user base accesses services via mobile apps. At its core, the battle between building for desktop versus mobile reflects a struggle between capital scale and mindshare.

Mapping User Motivations

I’m keen to understand user motivations and wallet user behavior patterns in emerging markets. Ravindra from Frontier Wallet kindly shared insights from his product. Frontier is one of the earliest smart contract-based wallets on the market, allowing users to easily track their portfolios across multiple blockchains without interacting with individual chain explorers.

Ravindra observed that Frontier users typically save between $1,000 and $10,000, are more crypto-literate than average exchange users, and maintain wallet balances averaging $150–$200. These users directly interact with multiple smart contracts and are particularly interested in earning USD-denominated yields. In inflation-prone regions like Turkey—one of Frontier’s larger markets—there’s strong interest in storing digital dollars and earning yield.

He’s seen distinct user segments treating Web3 as a consumption channel, often interacting with music- or gaming-related NFTs on-chain. In his view, the next wave of digital asset users won’t come for speculation—but for entertainment.

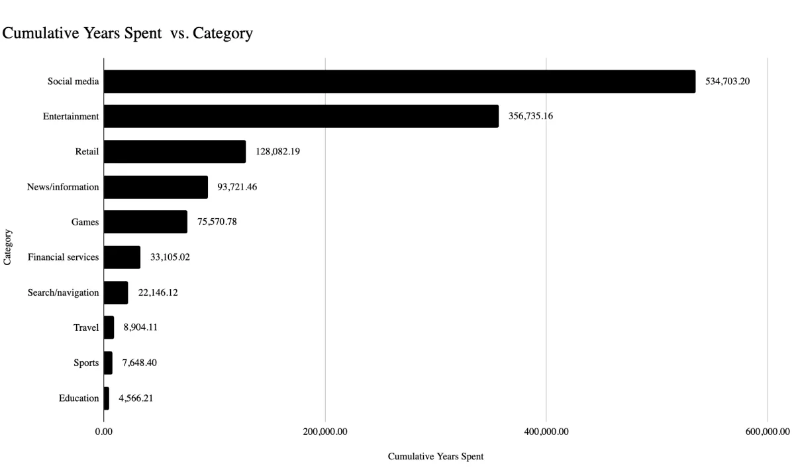

In my view, user growth in digital assets will follow a trajectory very similar to what we’ve witnessed in digital consumption in India. The data above shows how many minutes Indians spent consuming different app categories in a given year. Social media and entertainment—passive applications—gained the most traction.

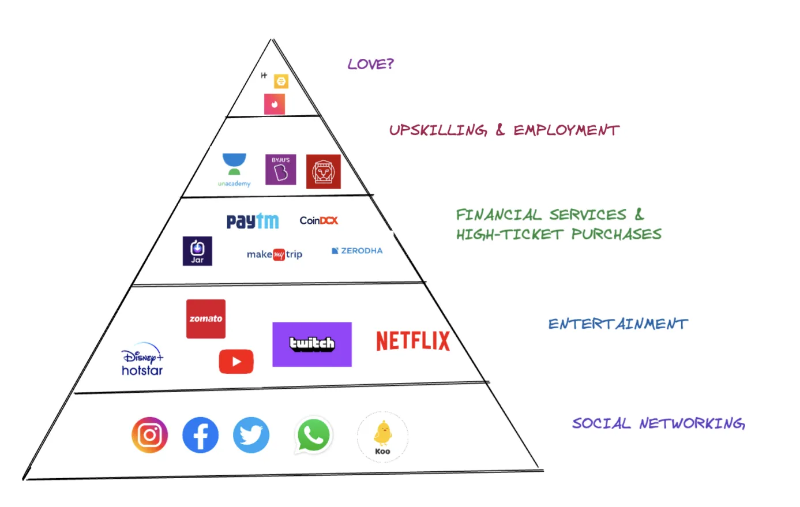

Consumption patterns loosely follow Maslow’s hierarchy of needs. Here, people start by fulfilling basic needs—a place to spend their attention. Then, moving up the curve, financial services for transactions and savings emerge, followed by a smaller segment focused on education or skill-building. I’ve attempted to map this into a Maslow-style hierarchy based on the data above.

In Web3—we invert this relationship. Most of us spend our time on Telegram, Discord, and Twitter. The market serves as entertainment, but at great economic cost.

Today’s Web3 apps focus on financial use cases or the speculative layer. For the industry to matter to the vast majority online, it must cater to what most people actually do online—use apps not for transactions, but for entertainment or connection.

This isn’t to say we aren’t moving in this direction. Axie Infinity’s surge in 2021 was partly due to the team spending two years building the largest mobile-first Web3 user base. More recently, Sweatcoin—a Web2 app with ~3–4 million DAU—launched an in-app token economy.

Apps like Mirror, Coinvise, and OpenSea enable creators to build stronger commercial relationships with their audiences. But in nearly all these cases, we assume user participation is active. Our focus should shift toward enabling passive participation—where users benefit without actively trading or posting. A class of applications may lead this shift.

That category is gaming. Games offer rich digital assets, attract the largest user bases across demographics, require minimal upfront investment, and—unlike most crypto apps today—deliver community and entertainment.

Given the overlap in user behavior between gamers and crypto participants, educating users about wallets, transactions, or NFT interactions becomes much easier through games.

What’s Next?

Today’s Web3 is a community of tech-brothers riding a speculative high, excitedly explaining how tracking tiny images to uncover wallet addresses is groundbreaking.

But if it’s to permeate society’s fabric, we must think clearly about how people interact with technology. We need tools that shift human perception of why they should care about this tech.

Some companies are already working toward this vision. Bluejay, for instance, is developing a stablecoin for emerging markets, while Goldfinch has issued over $100 million in loans to SMEs globally.

According to Crypto-art data, NFT hype is justified: in the past year alone, nearly 900 artists earned over $100,000, and more than 10,000 earned over $2,000.

Thus, in certain corners of the market, we’re making meaningful impact—but mobile can extend this to everyone.

Our focus should be guiding this transition—from a chaotic, confusing Web3 that sends users scattering in all directions—to a curated, guided, and genuinely useful Web3. All while preserving what made crypto compelling from the start: decentralization and inclusivity.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News