One Article to Understand Swell Network, Challenger in the Ethereum Staking Arena

TechFlow Selected TechFlow Selected

One Article to Understand Swell Network, Challenger in the Ethereum Staking Arena

In a highly competitive, network-effect-driven field, latecomers can actually gain greater advantages, and Swell Network is a perfect example.

Author: Ashu Pareek

Translation: TechFlow

Key Takeaways

- Swell Network is currently on its protected mainnet—a permissionless, non-custodial liquid staking protocol for Ethereum.

- Swell features the first integrated atomic deposits service: allowing users to directly deposit ETH into their chosen validator—creating a staking marketplace.

- To provide liquidity for staked assets, Swell mints and returns NFTs, known as swNFTs, to depositors.

- The swNFT acts as a container holding swETH along with information about stake, rewards, and the validator. swETH (non-rebasing) is returned at a 1:1 ratio to the deposited ETH (principal).

- Swell has become the first liquid staking service to adopt Distributed Validator Technology (DVT), enabling high capital efficiency and permissionless access to its validator set.

- It also plans to offer in-app DeFi vaults and white-label functionality, enabling node operators to build their own frontends atop the protocol.

Ethereum’s transition from Proof-of-Work (PoW) to Proof-of-Stake (PoS) has given ETH holders the opportunity to help secure Beacon Chain—the new central consensus layer of Ethereum.

In exchange for locking up ("staking") their holdings to propose new blocks, validators earn inflationary rewards.

Post-Merge, rewards will also include priority fees and Maximum Extractable Value (MEV), offering stakers attractive annual yields of 7–14%.

However, the high minimum capital requirement (32 ETH), technical complexity around the validation process, and extended lock-up periods (six months to a year post-Merge) have hindered both the ability and willingness of ETH holders to participate. To address these user experience challenges, an industry known as “Staking-as-a-Service” emerged.

So far, the most popular solution has been non-custodial liquid staking, led by Lido, with alternatives such as Rocket Pool.

While the current suite of non-custodial liquid staking protocols has been successful—accumulating over 34% of staked ETH—they leave many untested gaps in design and implementation.

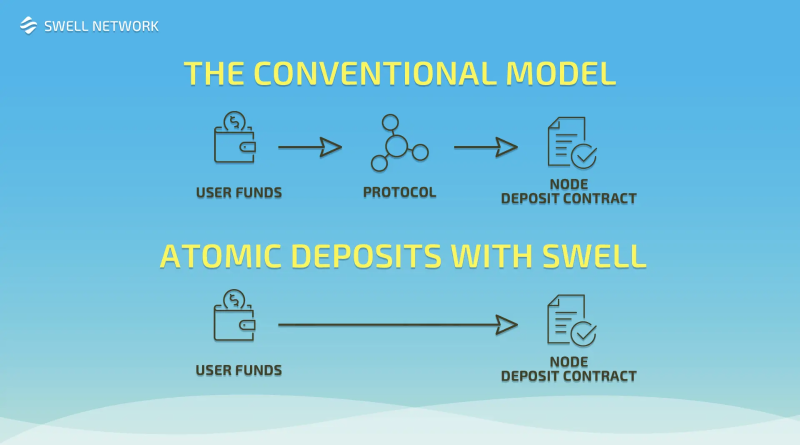

In a competitive, network-effect-driven space, latecomers can sometimes gain greater advantages. Swell Network is a prime example—it learns from prior non-custodial liquid staking pioneers and offers a novel way to stake and earn Ethereum yield. The key differentiator is its integration of atomic deposits: enabling users to directly deposit ETH into their chosen validator, thereby creating the first de facto staking marketplace.

Looking ahead, in addition to offering in-dApp DeFi vaults (similar to Yearn), Swell has taken concrete steps to become the first liquid staking service to implement Distributed Validator Technology (DVT). DVT will allow Swell to offer independent, permissionless node operators the same capital efficiency as commercial, whitelisted operators when joining its validator set.

Finally, Swell plans to build infrastructure enabling node operators to create their own frontends (“white-label”) atop the protocol.

If successfully executed, this could make Swell the preferred staking marketplace—fostering relationships, enabling customization, and increasing decentralization across the broader Ethereum network.

Background

Swell’s proof-of-concept (V1) launched in December 2020, shortly after the Beacon Chain went live.

In June 2022, Swell launched V2 private testnet on Kaleido and soon after opened public testing on Görli.

Around the same time, Swell completed a $3.75 million seed round led by Framework Ventures, with participation from IOSG Ventures, Maven Capital, Apollo Capital, Mark Cuban, Fernando Martinelli (Balancer), Ryan Sean Adams, and David Hoffman (Bankless).

By the end of August 2022, Swell V2 went live on Ethereum mainnet.

How Does Swell Work?

Swell operates very differently from other Ethereum liquid staking protocols.

In its final form, Swell V2 will involve:

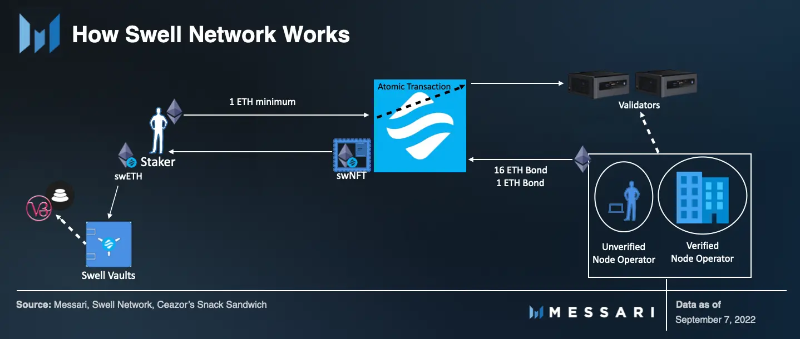

- Node operators responsible for managing staking. They can join permissionlessly (independent, requiring 16 ETH per validator) or via whitelist (verified, requiring 1 ETH per validator).

- Atomic deposits that allow users to stake directly with their chosen node operator, with a minimum of 1 ETH.

- swNFT/swETH, minted and returned to depositors (stakers). The swNFT is a container that holds swETH along with information about stake, rewards, and the validator. swETH (non-rebasing) is returned at a 1:1 ratio to deposited ETH (principal).

- swETH can be withdrawn and used in built-in DeFi vaults within the Swell dApp or anywhere ERC-20 tokens are accepted.

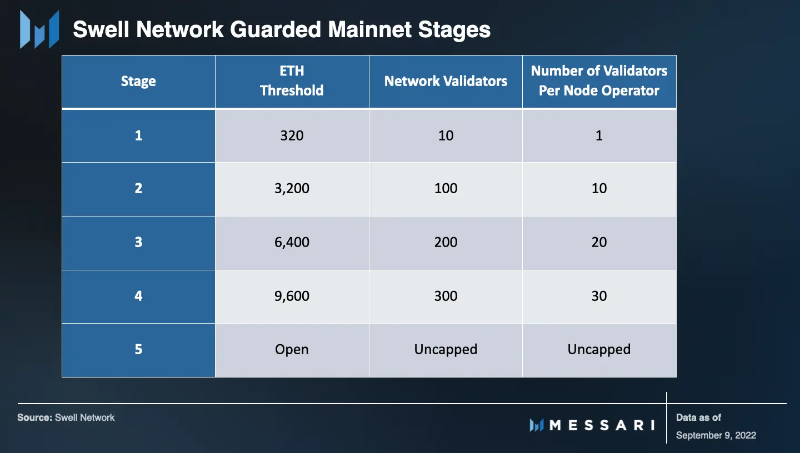

Swell’s secure launch is divided into five phases.

The protocol is currently in Phase One, with 242 ETH and 8 whitelisted node operators.

Completion of each phase depends on reaching its ETH threshold while maintaining normal operations.

Node Operations

Swell’s node operators are responsible for actual staking. Swell will host two types of node operators: verified (permissioned/whitelisted) and independent (permissionless).

During the protected launch phase, only verified node operators can accept deposits. These operators are typically experienced and apply through a vetting round. The first (and so far only) whitelist was curated by the Swell core team, onboarding eight commercial node operators: InfStones, RockX, Smart Node Capital, DSRV, Blockscape, HashQuark, Stakely, and Kiln.

Applications are evaluated based on experience, performance, infrastructure quality, diversity, security, potential contributions to the DAO, KYC checks, and contractual agreements.

Once Swell fully launches, independent node operators will be able to join the platform permissionlessly.

However, they must provide 16 ETH per validator as collateral to do so.

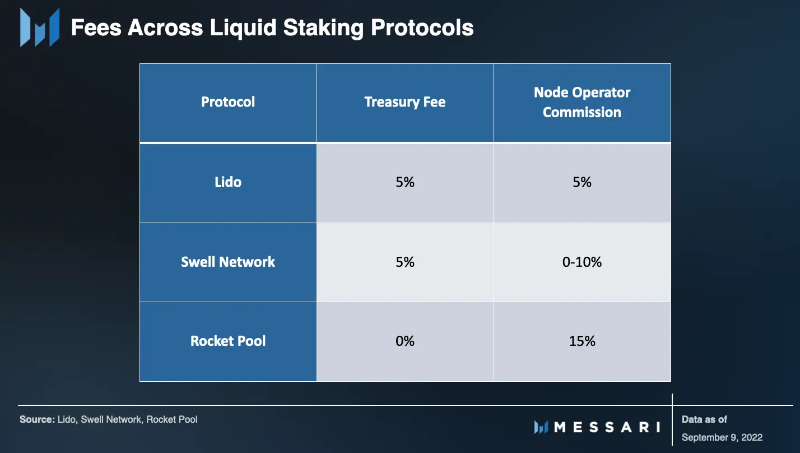

After joining, node operators set their own commission rate between 0–10%.

Currently, Swell also charges a 5% protocol fee on staking rewards, which goes directly into the DAO treasury and is subject to DAO governance.

Node operators also have flexibility in client selection. Post-Merge, they will have full control over how to redistribute priority fees and MEV rewards, as clients won’t configure fee recipient addresses. Swell also plans to eventually launch a smoothing pool similar to Rocket Pool’s.

While node operators can adjust their commission rates, the amount of additional yield sent to Swell’s designated fee pool, and how they display their performance (returns), they will compete in an open market. In theory, those who maximize transparency and returns while minimizing fees will attract the most staking.

swNFT and swETH

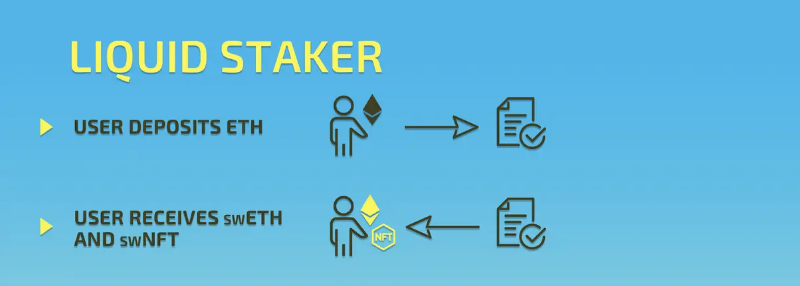

Because Swell uses atomic deposits, users stake (at least 1 ETH) directly into their chosen Beacon Chain deposit contract. In other words, users can select their node operator (based on profile, commission, and/or performance) and continue tracking their deposit.

In this model, staked ETH is not naturally fungible (i.e., liquid), as it is tied to a specific node operator rather than a general staking pool (composed of many operators). Swell has addressed this issue by using swETH derivatives and swNFTs to decouple deposited ETH from staking rewards.

In exchange for staking deposits, the contract mints and sends both swETH and swNFT to the user.

swETH is a non-rebasing ERC-20 liquid staking derivative token representing the principal stake, stored inside the swNFT.

During the protected launch phase, liquid staking remains disabled, meaning swETH cannot yet be withdrawn from the swNFT. Once withdrawals go live, stakers will be able to use swETH in DeFi. Meanwhile, node operators receive a soulbound (non-transferable) swNFT representing their collateral.

In addition to storing swETH, the swNFT holds staking rewards (yield) and specific, non-fungible details about the stake. This includes the delegated node operator, validator address, and deposit timestamp.

The swNFT itself does not accrue rewards. Instead, the swNFT containing staking information is linked to the yield generated by the original ETH deposited with the node operator.

In other words, the swNFT continues to accumulate rewards even without holding any swETH. To actually claim rewards (and principal), users must burn the swNFT using the original swETH amount deposited.

Withdrawals are expected to be enabled 6–12 months post-Merge. Until then, the primary source of swETH liquidity will be secondary markets.

This model creates interesting implications for swETH and swNFT holders.

First, under this model, the only way to earn staking rewards is to hold the swNFT—because swETH obtained without the swNFT does not accrue yield.

Eventually, swNFTs may also be used across DeFi in various ways: as collateral, with interest rate protocols (e.g., Element Finance and Yield Protocol), for node operators to build brand and relationships with stakers, and for access control to certain Swell features.

Roadmap

Improving Capital Efficiency

As mentioned earlier, once permissionless staking is enabled, independent node operators will need to provide 16 ETH of collateral per validator to join Swell’s network.

However, this poses a barrier to entry for independent operators and presents a challenge to Ethereum’s overall decentralization.

Swell V3 will reduce this requirement by leveraging secret shared validators (ssv.Network) technology, also known as Distributed Validator Technology (DVT).

Specifically, Swell will partner with ssv.Network (a DVT infrastructure protocol) to integrate SSV and reduce the collateral requirement for independent operators to just 1 ETH (matching that of verified operators).

Swell Vaults / DeFi Integration

Beyond delegation, liquid staking allows users to avoid the opportunity cost of locked funds. Instead, stakers can retain and use at least part of the staked value. With the introduction of Swell Vaults, Swell will take this further.

Initially, vaults within the dApp will be created by the Swell team, primarily to simplify and automate compounding, and to generate liquidity for swETH. Eventually, anyone will be able to build vaults and propose strategies (similar to Yearn).

The second component of DeFi integration will focus on creating liquidity for swETH. Once swETH becomes withdrawable, Swell will launch swETH/ETH liquidity pools on Uniswap V3 and Balancer. In addition to running liquidity mining programs, the team plans to incentivize vlAURA/veBAL holders to boost LP yields (and thus liquidity).

Swell Network Token

Swell has not yet launched its governance token SWELL. Beyond managing protocol parameters and cash flow usage, SWELL will be used to incentivize node operators and swETH/ETH liquidity providers.

Early users will receive airdrops, and seed round investors will have a three-year vesting schedule.

White-Labeled Liquid Staking

Swell will further enhance customization and staker-operator relationships by allowing node operators to build their own frontends using Swell’s backend.

Competitive Landscape

In the non-custodial liquid staking space, Swell’s biggest competitors are Lido and Rocket Pool.

In many ways, Lido and Rocket Pool sit on opposite ends of the spectrum in terms of product and approach.

Lido is the largest liquid staking provider, accounting for nearly 90% of all liquid-staked ETH.

Lido’s aggressive expansion on Ethereum has largely been driven by its deposit model. Lido relies solely on a small group of professional, whitelisted node operators and does not require them to post collateral. This model enables operators to easily absorb large volumes of ETH. Additionally, pooled staking allows users to start earning rewards immediately upon deposit (rather than waiting in the Ethereum validator queue), fueling rapid growth in Lido’s staked deposits.

On the demand side, Lido has deeply integrated stETH with nearly every major DeFi blue-chip protocol: Yearn, Curve, Aave, MakerDAO, Balancer, and others. Lido also spends millions monthly in LDO (its governance token) to incentivize liquidity (e.g., $2.5M LDO in August, ~$6M USD). This creates a powerful flywheel effect, driving more demand back into the staking service.

However, Lido has faced criticism from the Ethereum community, with many viewing it as a threat to Ethereum’s decentralization. Due to its relatively small, closed, institutional node operator set—effectively gatekept by an insider committee (LNOSG)—even though LDO holders have final say, insider ownership of LDO remains highly concentrated.

As a result, many prefer Rocket Pool, which takes an almost opposite approach. Nearly a year after Lido’s launch, Rocket Pool prioritized decentralization by enabling permissionless entry into its validator set.

The protocol secures validator slots through economic incentives rather than reputation or past performance. While Rocket Pool’s system enables broader participation in validation, it has created bottlenecks due to lower capital efficiency. Node operators currently need to deposit 16 ETH per validator plus bond RPL. This setup makes scaling validator counts and absorbing staked ETH challenging. As a result, Rocket Pool currently accounts for just over 5% of liquid-staked ETH and less than 2% of total staked ETH.

Swell leverages its late-mover advantage, learning from both protocols while introducing its own novel solutions to the “Staking-as-a-Service” landscape.

Swell’s first major strategic move is triangulating between Lido and Rocket Pool’s operator models. By supporting both permissionless and whitelisted node operators, Swell enables broader participation in validation (enhancing decentralization) while retaining strong capacity to absorb staking demand. Additionally, Swell will smoothly transition toward DVT by implementing permissionless validation from day one.

Swell also introduces several novel features—the most prominent being atomic deposits. The first open, transparent staking marketplace will bring benefits to both stakers and node operators. Stakers will be able to choose where to stake (based on performance, commission, infrastructure, jurisdiction, or other publicly listed traits) and track their stake on-chain.

Node operators can customize their offerings (e.g., priority fee/MEV distribution, commission, client choice), interface with clients (via swNFT), and eventually build their own frontends (‘white-label’) atop Swell. A trade-off of this model is that penalties and slashing are not shared across all users but are instead borne by the affected validator and its stakers.

Using NFTs is also a first among liquid staking protocols. This model eliminates the need for yield-bearing tokens (like Rocket Pool’s rETH or Lido’s stETH). While a necessary trade-off, the lack of fungibility may likely widen the swETH:ETH discount, especially in secondary markets.

Another Swell strategy is a 1 ETH minimum stake, as there is no staking pool. Depending on ETH price appreciation, a 1 ETH minimum could lock out many users in the future. Rocket Pool has a 0.01 ETH minimum, and Lido has no minimum requirement.

Two other competitive advantages for Swell are Swell Vaults and variable commission rates. Commission rates could become a major selling point, depending on where the internal market drives them.

The future staking ecosystem may accommodate these different models and their unique products. These models may begin to converge, especially regarding permissionless node operation and capital efficiency. Rocket Pool is currently considering a formal proposal to reduce required collateral to 8 ETH, and eventually even down to 4 ETH (alongside RPL bonding).

Lido’s roadmap is also becoming more competitive compared to Swell’s, as it too seeks to implement permissionless DVT. However, Swell appears further ahead on its roadmap, with imminent (mainnet) permissionless validation already underway and a public DVT strategy/partnership with ssv.network.

Risks

Swell’s biggest risk is its late market entry. While Ethereum staking is still in early stages, Lido—and to a lesser extent Rocket Pool—have already established strong footholds in DeFi and the broader ecosystem. They benefit from a powerful flywheel: integrations and liquidity drive demand, which in turn fuels more integrations and liquidity.

Swell has significant differentiation and is committed to incentivizing swETH liquidity and actively integrating with DeFi. However, the protocol will likely need flawless execution on its features to truly shift momentum. If successful, it could attract a meaningful inflow of ETH and spark its own competitive flywheel.

One potential narrative I see is becoming the first project to successfully implement DVT—reducing collateral requirements for independent operators to just 1 ETH. Unlocking this capital efficiency could enable a massive influx of independent validators while enhancing Ethereum’s decentralization. Beyond aligning with Ethereum’s core goals, DVT also enhances security by enabling trustless validation split across four operators.

Another narrative for Swell is building a highly attractive staker-operator marketplace. This market could benefit from external catalysts that increase the value of operator information—such as regulatory enforcement or crackdowns in certain jurisdictions. Another driver could be significantly lower commission rates than current industry standards, attracting stakeholders. This shift might also come from validator migration—commercial operators may be drawn to Swell’s flexibility, choosing to vertically integrate with clients using Swell’s swNFT and eventual white-label capabilities.

Customizability (for node operators) is a double-edged sword. Not only could commission rates converge above industry standards, but node operators might also collude to withhold priority fees/MEV from their fee pools. Even in a transparent, competitive market, the factors determining market equilibrium are multifaceted and impossible to predict in advance.

Although Swell uses swNFT/swETH to solve its fungibility issues, this feature introduces additional risk vectors. Like stETH, the swETH/ETH pair on secondary markets could deviate significantly from 1:1—even after withdrawals are enabled—because swETH is only valuable as a staking derivative to those with positions in Swell (limiting demand). This uncertainty may also hinder DeFi integration (as it would be seen as unstable collateral).

Conclusion

While Swell’s novelty brings uncertainty, it also brings differentiation.

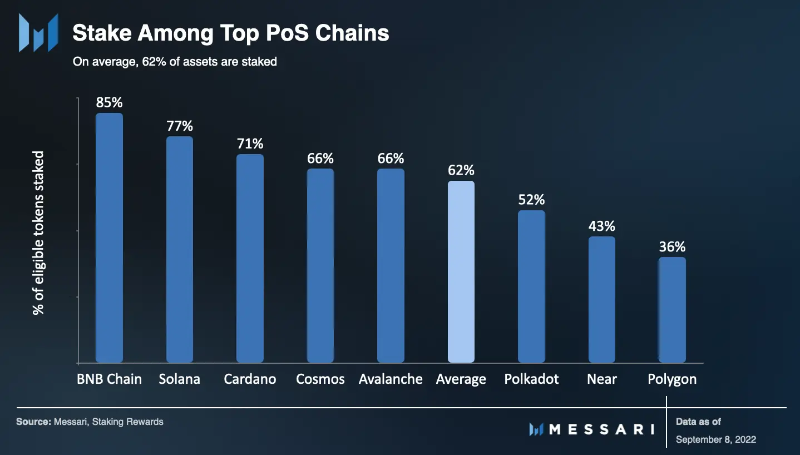

Currently, about 11% of circulating ETH is staked, and much of the growth is yet to come.

Swell is launching at the right time with a distinct, unique core product: an open, transparent staking marketplace. It’s hard to predict exactly how the liquid staking landscape will evolve, but Swell is undoubtedly an attractive offering for both stakers and node operators.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News