Hong Kong ouvre la voie aux ETF sur actifs virtuels : une prévision de 500 millions de dollars est-elle prudente ou optimiste ?

TechFlow SélectionTechFlow Sélection

Hong Kong ouvre la voie aux ETF sur actifs virtuels : une prévision de 500 millions de dollars est-elle prudente ou optimiste ?

Pourquoi les institutions accordent-elles une telle importance aux flux sud (« southbound funds ») lorsqu'elles évaluent l'échelle des capitaux entrants ?

Production | OKG Research

Author | Hedy Bi

The approval of spot Bitcoin ETFs is no longer news. According to Reuters yesterday, at least three offshore Chinese asset management firms will soon launch Hong Kong-based spot virtual asset ETFs (spot Bitcoin and spot Ethereum ETFs). The Hong Kong government's strong support for Web3 and its continuous favorable policies have become an industry-wide expectation. OKLink Research has observed that the recent approval of Hong Kong’s spot Bitcoin and Ethereum ETFs did not generate as much market excitement as the U.S. spot Bitcoin ETF approvals. However, in responding to media inquiries, we found that the key questions revolve around how much capital inflow this could bring and its deeper implications. This article explores these issues from the perspective of a "Hong Kong stock trader":

1. Why do institutions place such importance on southbound funds when estimating capital inflows?

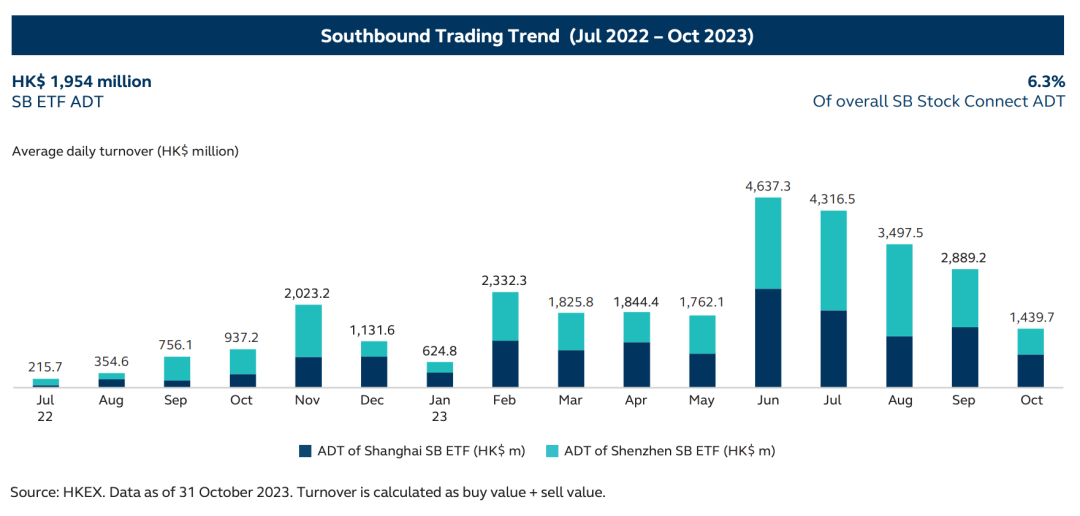

Since July 2022, ETFs have been included in the "Stock Connect" program for the first time. This initiative allows mainland Chinese and Hong Kong investors to trade and settle stocks listed on each other's exchanges through their local securities and clearing systems, creating two categories: southbound funds (from mainland China to Hong Kong) and northbound funds (from Hong Kong to mainland China).

If southbound funds gain access, the virtual asset market represented by Bitcoin would become a new financial market bridging China and the United States. According to public data from the China Securities Regulatory Commission (CSRC), as of December 31, 2023, although only eight southbound-eligible ETFs were available to mainland investors, they achieved a daily trading volume of 108.3 billion RMB (approximately 15 billion USD). In other words, just 5% of eligible ETFs accessible via southbound funds attracted 16% of total capital inflows into HKEX (via the RMB channel).

However, we also note that the number of qualified ETFs accessible via the Shanghai-Hong Kong or Shenzhen-Hong Kong Stock Connect channels remains very limited. Furthermore, in its 2024 outlook, the Hong Kong Securities and Futures Commission (SFC) proposed strengthening Hong Kong’s position as a leading global offshore RMB center through initiatives like the "Swap Connect," "HKD-RMB dual-counter model," and designated market makers for dual counters. Considering the mainland’s current stance on virtual asset trading, and after discussions with financial market professionals and Web3 experts in Shanghai and Hong Kong, OKLink Research concludes that in the short term, it is highly unlikely that Hong Kong’s spot Bitcoin and Ethereum ETFs will be opened to mainland investors. Based on input from regulators and industry insiders, mainland residents are currently unable to invest in spot Bitcoin and Ethereum ETFs via the Shanghai-Hong Kong or Shenzhen-Hong Kong Stock Connect programs.

Moreover, funds withdrawn via Shanghai/Shenzhen-Hong Kong Connect must return along the original path through the local settlement system—meaning RMB flows in and out via the Connect programs without leaving other assets behind in the Hong Kong market. This implies that offshore RMB is excluded from the Shanghai/Shenzhen-Hong Kong Connect channels.

2. U.S. Bitcoin ETF vs. Hong Kong ETF: Does Hong Kong remain attractive?

We note that Bloomberg’s senior ETF analyst Eric Balchunas believes $500 million would be an optimistic figure. Nevertheless, we firmly believe that the potential of Hong Kong’s virtual asset ETF market far exceeds this number. This article analyzes the topic from three angles: investor risk appetite in Hong Kong, the state of Hong Kong’s virtual asset market prior to the announcement, and differences between ETF structures in both regions:

While Eric Balchunas uses overall ETF market size for comparison—and indeed, Hong Kong’s ETF market is much smaller than the U.S.—we observe an interesting phenomenon. Among Hong Kong’s top ten ETFs by AUM, the largest holds 54% of total AUM, compared to just 20% in the U.S. This indicates a highly concentrated distribution among Hong Kong ETF investors, with over half of investments focused on the top players.

Additionally, the largest ETF in Hong Kong by AUM is SPDR GOLD TRUST, which tracks gold—an asset often compared to Bitcoin—and has an AUM of approximately $69.8 billion. In contrast, the largest U.S. ETP is the S&P 500-tracking fund with an AUM of about $518.7 billion, making SPDR GOLD TRUST roughly 13.5% the size of the top U.S. ETF. This further supports the conclusion that the concentration effect is significantly stronger in Hong Kong’s ETF market, and while U.S. investors show greater interest in equities (e.g., S&P 500), Hong Kong investors exhibit stronger interest in gold. This reflects differing risk appetites and understandings of economic cycles between the two markets. Hong Kong investors are likely to show greater acceptance of Bitcoin as “digital gold.”

Data source: HKEX, ETFdatabase

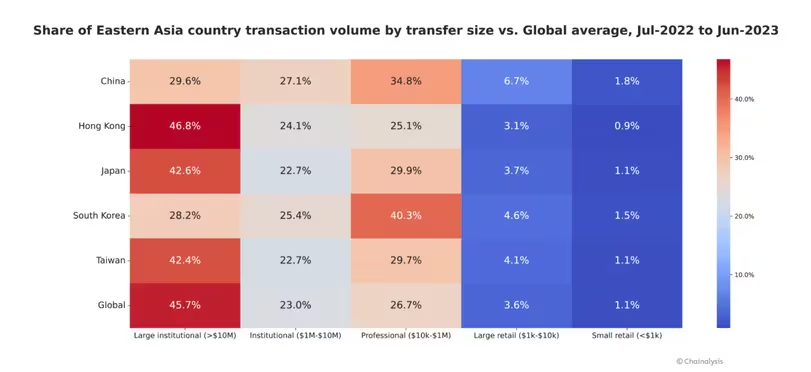

Public enthusiasm for Bitcoin also appears higher in Hong Kong. At the end of last year, OKLink Research conducted field research in Hong Kong’s OTC virtual asset market and found that, as of January this year, there were at least 200 physical crypto OTC exchange shops. We estimate that annual average transaction volume through these shops alone exceeds $10 billion. Even before ETFs existed, Chainalysis estimated that despite Hong Kong’s population being much smaller than the U.S., its active OTC crypto market drove $64 billion in trading volume during the bear market period from June 2022 to June 2023. Compared to other Asian regions, Hong Kong dominates large institutional cryptocurrency transactions. In Hong Kong’s annual virtual asset trading volume, 46.8% consists of institutional trades exceeding $10 million, above the global average for similar transactions.

Data source: Chainalysis

Furthermore, regarding redemption mechanisms, due to Hong Kong’s comprehensive regulatory framework for virtual assets, in-kind redemption offers advantages for "Crypto-native" investors. The four options—crypto-in cash-out, crypto-in crypto-out, cash-in crypto-out, and cash-in cash-out—are more flexible than the U.S.-only cash redemption model (the last option), creating arbitrage opportunities. Moreover, for Hong Kong investors already holding BTC and ETH, this reduces the risk of being flagged for illicit funds when converting crypto to fiat, thus better protecting investor assets.

Regarding spot Ethereum ETFs, although Ethereum’s current market cap stands at $371.7 billion—significantly smaller than Bitcoin’s $1.25 trillion—issuers may have stronger incentives to promote Ethereum ETFs. Besides price appreciation, Ethereum ETFs offer additional yield through staking rewards. As early as February 7, 2024 (local time), Ark Invest filed an updated S-1 amendment stating: “The sponsor may from time to time stake a portion of the trust’s assets with one or more trusted third-party staking platforms.”

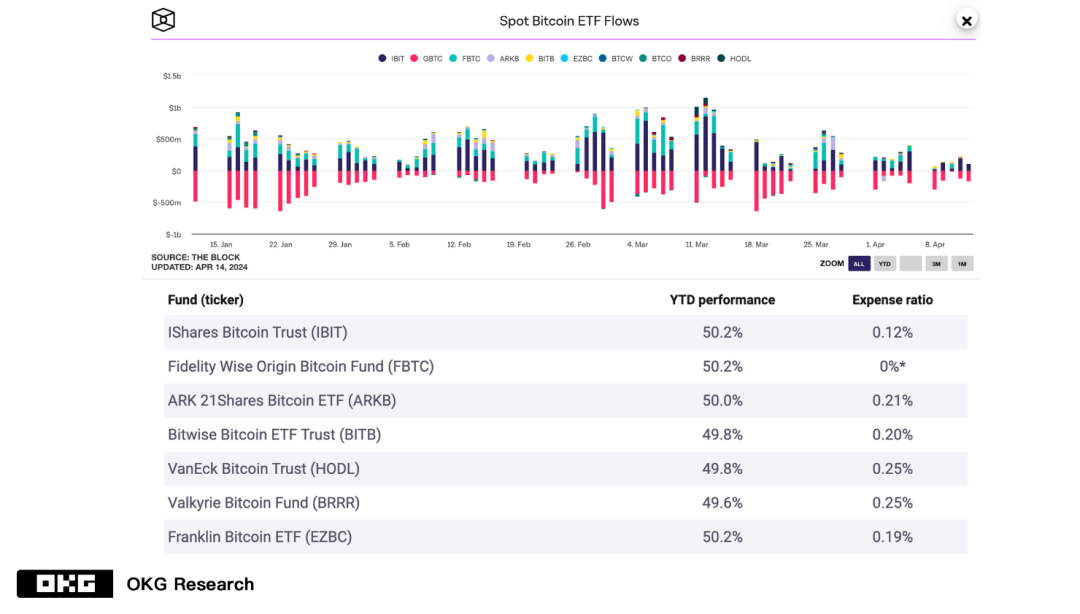

For Hong Kong qualified investors, especially high-volume traders, management fees for Hong Kong ETFs are currently not particularly competitive. However, other factors affect capital inflows. For instance, FBTC, which charges a 0% fee, did not rank first in capital inflows—a result possibly linked to its use of self-custody rather than third-party custodians like Coinbase or Gemini.

Data source: The Block, Public Info

Hong Kong’s strategic push into Web3 and opening well-known investment vehicles like ETFs carries deeper significance. This is not only a positive move for financial institutions seeking balance sheet adjustments amid general asset contraction but also a strategic effort to stay at the table—or even lead the creation of a new financial ecosystem. With fundamental tailwinds such as the upcoming Bitcoin halving, the future potential of Hong Kong’s spot virtual asset ETFs is worth watching closely!

Bienvenue dans la communauté officielle TechFlow

Groupe Telegram :https://t.me/TechFlowDaily

Compte Twitter officiel :https://x.com/TechFlowPost

Compte Twitter anglais :https://x.com/BlockFlow_News