Web3 Music Sector: Market Background, Commercial Value, Growth Trajectory, and Investment Opportunities

TechFlow Selected TechFlow Selected

Web3 Music Sector: Market Background, Commercial Value, Growth Trajectory, and Investment Opportunities

From a Web3 business perspective, the music sector features a massive two-sided market: creators and consumers.

Researcher: Xu Xiaopeng, Mint Ventures

Key Takeaways

1. Music is a $20 billion annual global market, and industry power is gradually shifting from copyright-holding record labels to online music platforms.

2. In the short to medium term, Web3 and music NFTs cannot resolve the overall issue of low musician income. Their significance lies in offering an innovative framework for value distribution in the music industry, preparing the groundwork—technologically, commercially, and ideologically—for future upgrades.

3. The Web3 music sector currently lacks breakout conditions comparable to DeFi and still requires maturation in user base and community mindset, though its technological foundation is relatively mature.

4. Music NFTs are unlikely to replicate the popularity of profile picture (PFP) NFTs. Instead, Web3 music projects should look to DeFi’s business flywheel model as a blueprint for growth.

Main Content

This edition of our sector deep dive focuses on the Web3 music space.

Following the 2020 explosion of the DeFi sector, crypto-based businesses welcomed their first major non-investor user group: financial customers. Then, with the rise of NFTs in 2021, the Web3 application wave spilled beyond finance, giving rise to NFT collectibles and the "Summer of Play-to-Earn" gaming boom. With DeFi having demonstrated viable commercialization and NFTs/gaming expanding the crypto user base, the "creator economy" quietly emerged at the end of 2021 as the next major Web3 narrative.

Web3 music is a sub-sector within this broader creator economy. Additionally, as music represents a significant category among NFT collectibles, it can also be seen as part of the larger NFT movement.

From a Web3 business perspective, the music sector presents a vast two-sided market: creators and consumers. Technologically, tools like NFTs, Layer-1 blockchains, and decentralized storage (e.g., Arweave, Filecoin) are increasingly mature. Narratively, the music sector benefits from dual tailwinds: NFT collectibles and the creator economy.

If 2021 was the inaugural year for Web3 music, will 2022 become its year of opportunity?

In this article, we explore and attempt to answer the following questions:

● What is the broader market context for the Web3 music sector?

● How do we define Web3 music projects? What problems in the existing music industry do they—and music NFTs—solve?

● What prerequisites are needed for Web3 music projects to achieve breakout success?

● In what form might the Web3 music sector experience explosive growth?

● How can investors identify opportunities in this space?

Section 1: Current State and Business Model of the Music Industry

1.1 Participants and Evolution of the Music Industry

Music is a massive industry, rivaling social media and gaming in terms of intellectual property (IP) and user scale. It has a clear supply-demand structure: on the supply side are musicians or record labels and entertainment groups that sign artists; on the demand side are music consumers, ranging from casual listeners to passionate fans.

The music industry has a long commercial history. Its mediums have evolved from live band performances to phonographs, then radio, television, vinyl records, tapes, CDs, MP3s, and now streaming platforms. Each shift in distribution medium has triggered structural changes across the industry.

Historically, record companies held dominant influence, controlling artist discovery, branding, production, promotion, physical distribution, and concert operations. They captured the majority of royalty revenue and retained ownership of vast music copyrights. However, the emergence of the internet eroded their control over production and promotion, as marketing channels shifted from centralized media to social platforms. Digital technologies lowered creation costs, enabling more individuals to produce and release music rapidly and directly.

Online music platforms have emerged as new intermediaries between artists and listeners. They handle promotion, distribution, recommendation, and revenue settlement, while increasingly moving upstream by nurturing new talent and original content. The number of artists signed directly to these platforms continues to grow. This surge in original content satisfies Gen Z’s evolving tastes and appetite for novelty, while also giving platforms leverage against traditional labels in copyright negotiations.

Having outlined the current landscape, it's crucial to reflect on a foundational question before diving deeper: In today’s world, what kind of product is music? All commercial logic and industrial structures stem from how we answer this.

Zhong Wen, a writer at the WeChat public account "Pingwan," offered a classic description:

"...Regardless of context or format, music’s core attribute remains unchanged—it is a way for us to empathize with the world, a language transcending time, space, and culture.

Perhaps this is precisely what makes the music industry so 'sexy.' In every era and civilization, we need music, and we are moved by similar rhythms."

Pingwan: “Over 71 million paying users on streaming platforms, TME spins the music industry flywheel”

As a spiritual good that fosters empathy, music exhibits stronger repeat consumption than books, films, or TV series. Even the most novelty-seeking listeners often have songs they’ve played hundreds of times. Once someone discovers a beloved track, the resulting loyalty can be tens of times greater than with other content formats.

To summarize the music industry:

● Key players include musicians (songwriters, performers), record labels, music platforms, and consumers.

● Online music platforms have replaced traditional record labels as the dominant force, controlling promotion, distribution, and revenue settlement, while expanding upstream to cultivate artists and produce original music.

● At its core, music provides a means of empathizing with the world. It is the most frequently consumed and sticky form of digital content.

1.2 Market Size of the Music Industry

Next, we examine the size of the current music market through three lenses: revenue, consumers, and musicians.

1.2.1 Revenue Scale

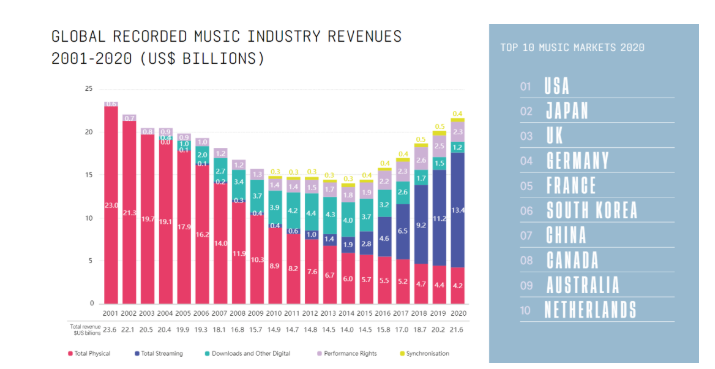

According to the International Federation of the Phonographic Industry (IFPI)'s 2021 report, the global recorded music market generated $21.6 billion in revenue in 2020. After hitting a low of $14 billion in 2014, it has seen six consecutive years of growth but has yet to surpass its 2001 peak.

Source: Global Music Report 2021 https://gmr2021.ifpi.org/report

The U.S., Japan, the UK, Germany, and France rank as the top five music-consuming nations, with China in seventh place, just behind South Korea. Despite China’s massive internet population, its music subscription penetration lags far behind Western countries. According to Tencent Music Entertainment Group (TME)—China’s largest music platform by users and revenue—its Q3 2021 report showed 71.2 million paying subscribers, representing an 11.2% paid user ratio. Average monthly revenue per user (ARPU) was RMB 8.9 (~$1.30) during the first three quarters of 2021.

Source: TME Q2 2021 Financial Report

By comparison, Spotify—the leading international streaming giant—reported 365 million monthly active users and 165 million paying subscribers in Q2 2021, a 45.2% conversion rate, roughly four times that of TME. Its ARPU stood at $5.02.

In terms of revenue sources, streaming accounted for 62% of total global music income in 2020, growing 19.9% year-on-year. Other sources—including physical sales (records, CDs), downloads, performance rights, and synchronization licenses—all declined compared to the previous year (partly due to pandemic impacts).

These figures confirm that music is a $20 billion+ global market. Platforms like Spotify and Tencent Music (operating QQ Music, KuGou, Kuwo) have driven the recovery of a once-stagnant industry since 2001. The dominant business model today is “streaming platforms paying artists based on play counts,” commonly known as the “streaming platform model.”

1.2.2 Subscriber Scale

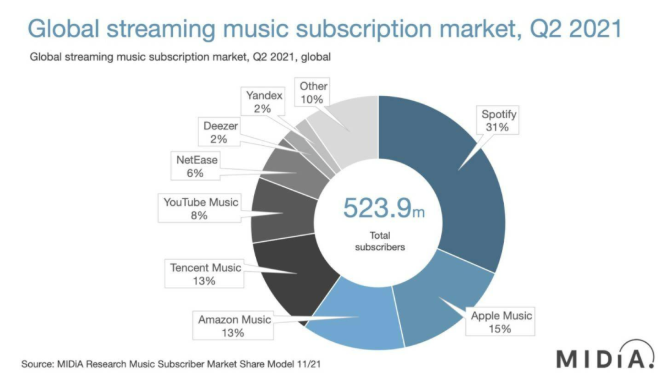

According to research firm MIDiA Research, global streaming subscriptions reached 523.9 million in Q2 2021, up 26.4% year-on-year. Spotify remained the leader in subscriber count.

Source: MIDiA Research

Of course, music consumers extend beyond paying subscribers to include physical media buyers, concertgoers, merchandise purchasers, and licensing clients (e.g., advertisers). However, these groups largely overlap with streaming users.

1.2.3 Number of Musicians

At Spotify’s “Stream On” investor event, CEO Daniel Ek revealed that by the end of 2020, 8 million artists were registered on Spotify, projecting this number to reach 50 million by 2025. In China, both Tencent Music and NetEase Cloud Music recently disclosed artist data, each hosting over 300,000 independent musicians. Conservatively estimating, the global number of musicians likely exceeds 10 million.

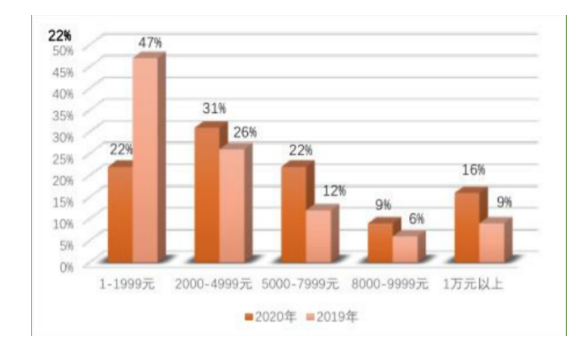

Despite rising numbers, musician incomes remain poor. Only a small fraction earn a living solely from music. According to Loud & Clear’s report, only 184,500 creators earned over $1,000 from Spotify by 2020. In China, a 2021 report by the Communication University of China found that 51% of musicians earned less than RMB 4,999 per month, and only 9% earned over RMB 10,000. This marked improvement from 2019, when 49% earned between RMB 1,000–1,999—insufficient for basic living expenses.

Chinese Musician Income Comparison: 2019 vs. 2020

Source: China Musician Report 2021, Communication University of China

1.3 Business Logic of the Music Market

Copyright is the core of the music industry’s business model. A song’s full rights typically break down into four components: composition/lyrics copyright, sound recording copyright, and performer’s rights. These four parties share royalties (copyright fees) from distribution. Other contributors—producers, arrangers, session musicians—usually receive one-time payments.

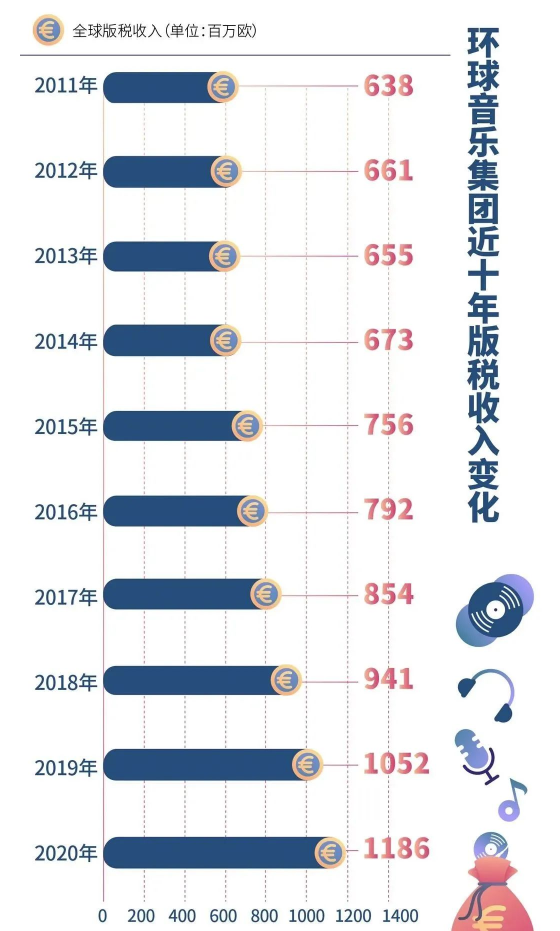

Historically, major record labels were central to music production, discovering artists, songwriters, and professional teams. They wielded significant power, owning performer rights and master recordings, while their affiliated publishing arms managed composition rights. As smaller labels were acquired, copyright became concentrated among a few giants. For example, Universal Music’s parent company Vivendi reported €1.186 billion in publishing revenue in 2020, which continues to grow.

However, with the rise of online platforms, independent artists and top-tier IP holders launching their own studios are gradually breaking free from label control.

For both independent artists and labels, online platforms are now a primary source of copyright revenue.

Streaming platforms typically pay rights holders based on play counts. Spotify, for instance:

Spotify generates revenue mainly through paid subscriptions and ads on its free tier. Roughly two-thirds of this revenue goes to rights holders. Spotify allocates funds from a royalty pool based on each rights holder’s “market share” of total streams, rather than paying a fixed fee per stream.

This is because subscribers pay a flat monthly fee regardless of usage.

Each month, Spotify sums all streams by rights holders in a region and divides by total regional streams to calculate each party’s share of that market’s royalty pool.

For example, if total streams in Mexico amount to 1,000 and a given artist accounts for 1 stream, they receive 1/1,000 of Mexico’s entire royalty pool. The size of each regional pool depends on local subscription and ad revenues.

Thus, an artist’s income from streaming platforms depends on three key factors: total platform revenue, their own play count, and the aggregate play count of all other artists.

Besides streaming, musicians may earn from live shows (online/offline), direct digital album sales/downloads, sync licensing (for films, ads, variety shows), and merchandise. However, these sources either contribute minimally or are shrinking in relative importance.

1.4 Summary

To summarize this section:

● Music’s essence lies in enabling emotional connection with the world. It is the most replayed and stickiest form of digital content.

● The music market exceeds $20 billion annually, with online platforms capturing the largest and fastest-growing share.

● Online music platforms are replacing traditional record labels as central players, extending influence across the entire value chain.

● The core business model revolves around copyright. Low average musician earnings result from intensifying competition and platform-dominated industry structures.

These dynamics constitute the backdrop against which the Web3 music sector operates—shaping its potential value and logic.

Section 2: The Value of Web3 Music Projects

2.1 Defining the Web3 Music Sector

The Web3 music sector refers to a blockchain-native music ecosystem characterized by:

● Core protocols built and operated on blockchain infrastructure

● Digital music assets issued and transferred via blockchain and decentralized storage

● Decentralized, transparent value distribution

● Listeners evolving into community members with expanded rights, co-creation opportunities, and even shared ownership of IP value

Given these features, what problems can Web3 music projects and music NFTs solve, and what new opportunities might they unlock?

2.2 Problems Web3 Music Projects Aim to Address

2.2.1 Web3 Cannot Solve Low Musician Incomes in the Short Term

A common claim about Web3 music or music NFTs is that artists can use NFTs as vehicles to sell directly to fans, bypassing exploitative layers of record labels and streaming platforms, thereby increasing income.

However, I argue that the Web3 music wave won’t significantly raise average musician earnings in the near term. Instead, it offers more transparent, diverse channels and value distribution tools.

Like any product, music follows supply and demand. While digital music has near-zero marginal cost, consumer attention is finite. The total global “content consumption time” is capped, and music competes with video games, social media, and online videos for this limited resource.

On the supply side, digital tools have drastically lowered music creation barriers, leading to an explosion in new content. On the demand side, total attention spans face hard limits and intense cross-category competition.

Under these conditions, the oversupply of music against scarce attention means most tracks become obscure “zombie works”—an inevitable outcome of fierce competition. Web3 and NFTs won’t change this reality, just as DeFi enables fairer, more open finance without making everyone wealthy.

2.2.2 The Value of Web3 Music and NFTs: Restructuring Value Distribution and Laying Infrastructure for Future Services

So what positive changes do Web3 and NFTs bring to the music industry?

I believe there are two main contributions:

● Blockchain and smart contracts enable more transparent, automated, and efficient value distribution among artists, users, and stakeholders

● Unlike traditional digital music, which offers only “listening value,” NFT-based music gains programmability, provenance, composability, and tradability—enabling unimaginable new service models and experiences

In short: redefining value distribution, adding value beyond mere listening, and laying technological, commercial, and ideological groundwork for the next phase of music industry evolution.

2.2.2.1 Restructuring Value Distribution

“Restructuring value distribution” primarily means:

● Increasing transparency and efficiency in revenue sharing, improving information symmetry

● Offering artists shorter, less-intermediated distribution paths and transaction-based royalty models

● Enabling listeners to participate in value distribution

Specifically:

a. Improving transparency and efficiency in revenue distribution

In the current music industry, streaming revenue is split among multiple parties. As Wu Xiangfei, a lyricist quoted in a 2021 Southern Weekly report titled “Ten Years of Copyright Wars: Prices Up Nearly 1000x, Is Music Better Now?”, explained:

“On streaming platforms, 42% of a song’s revenue goes to record labels, ~30% to operating systems (like Android/iOS), ~20% to the platform itself, and only ~8% to composers and lyricists combined. Singers are usually paid separately by labels.”

Platforms provide detailed playback data to rights agencies, which then report individual statistics and royalty statements to creators. But verifying these reports is difficult. As Wu noted: “High维权 costs and weak bargaining power leave creators with no choice but to accept them silently.”

He added:

“Different publishers offer different rates—the pricing power lies entirely with companies… Two organizations quoted royalties differing by 195x for the same song in the same year.”

Against powerful, centralized labels, platforms, and agencies, individual creators struggle to audit their actual earnings. A blockchain-based music industry could dramatically improve transparency throughout the value chain. Smart contracts would automate royalty settlements—making them faster, fairer, and fully auditable. Greater transparency reduces rent-seeking by intermediaries, benefiting artists and users alike in the long run.

b. Providing leaner distribution channels and novel royalty mechanisms

Platforms like Catalog, Sound.xyz, and Nina offer new distribution avenues where artists mint their music as NFTs and sell them directly—via auction or fixed price—to collectors. Artists can also set resale royalties, earning a percentage each time their NFT is resold.

Catalog music NFT detail page showing current owner, sale price, and resale royalty rate

c. Including users in the value distribution network

Traditional digital music files grant only usage rights (playback), whereas NFTs represent ownership—even linking directly to copyright and enabling buyers to share in royalty income. Web3 music platform Royal operates on this principle: when users buy an artist’s NFT, they gain a portion of the song’s streaming revenue.

Taken together, Web3 music represents a shift in “production relations,” with NFTs serving as the technical vehicle.

2.2.2.2 Unlocking New Music Services and Use Cases

Beyond reshaping value distribution, the longer-term impact of Web3 music and NFTs may lie in leveraging their programmability, traceability, composability, and tradability to create entirely new services and scenarios—sparking broad innovation and increasing overall industry output.

For example, Live Nation recently launched Live Stubs—a project giving concertgoers a free NFT ticket stub upon purchasing a ticket. CEO Michael Rapino explained: “Our Live Stubs product taps into fans’ nostalgia for collecting physical stubs, while giving artists a new tool to deepen fan relationships. We can’t wait to see what this community creates.”

Though Live Nation hasn’t detailed the functionality of these “stub NFTs,” we can imagine several possibilities:

● Exclusive access pass to official fan clubs or DAOs

● Backstage footage access for that concert

● Fan credential for receiving token airdrops from the artist

● Blind box functionality to unlock perks like front-row seats or backstage passes for future shows

● Identity badge displayed in a user’s on-chain profile

● …and more

Additionally, thanks to programmability, artists can grant remixing rights via NFTs. Other musicians could purchase original stems, create derivative works, and mint new NFTs—services already offered by platforms like async.art.

We must admit our imagination here is still limited. Truly transformative innovations often lie beyond current understanding. Just as concertgoers a century ago couldn’t envision paying to attend a virtual Justin Bieber concert in the metaverse via VR, we cannot yet predict the full scope of Web3 music innovation.

On November 18 last year, Justin Bieber hosted a “metaverse concert” using motion capture technology in collaboration with virtual concert company Wave VR

But we can confidently say:

● Web3 music services will be richer, more diverse, and more engaging than today’s Web2 offerings

● In a blockchain-based metaverse, NFTs may become the default music format

Then, NFT-based music won’t just be for playback—it could serve as a “collectible,” “identity marker,” “remix素材,” “ticket,” or “financial asset”—a key unlocking a wide range of music experiences.

In summary, in the short term, Web3 music projects offer new value distribution models—making the system more transparent and equitable while transforming passive listeners into active stakeholders. Long term, the Web3 paradigm unlocks entirely new service categories, with NFTs potentially becoming the dominant music format.

However, for Web3 music applications to go mainstream, several prerequisites remain unmet.

Section 3: Prerequisites for the Rise of Web3 Music

3.1 User Scale: The Challenge Facing Web3 Music, Social, and Gaming Apps

While the long-term outlook for Web3 music is promising, we must recognize a key difference between it—and Web3 social/gaming apps—and DeFi: we cannot simply replicate DeFi’s success in these domains.

Bitcoin and blockchain were conceived as financial tools. Satoshi designed Bitcoin as a decentralized payment system. From day one, every public address represented a financially motivated user—whether driven by belief in decentralization or pure speculation.

That’s why DeFi applications built on Ethereum’s smart contracts spread so rapidly—they directly served users’ financial needs.

We can observe the same pattern in gaming. Between 2018–2019, there was a brief wave of blockchain games centered on the idea of “games on blockchain.” The movement fizzled quickly, remembered mostly for gambling apps and speculative schemes like FOMO3D—perfectly aligned with users’ speculative instincts.

In 2021, blockchain gaming returned with far greater scale, participation, and longevity. Contributing factors included a larger crypto population, established DeFi/NFT habits, and a bull market—but the core reason for its success was deep integration of financial mechanics. In truth, many “blockchain games” were not games at all, but Ponzi-like financial schemes wrapped in gameplay.

In short, in a crypto world dominated by financial users, only applications with strong financial appeal succeed easily. Pure music, social, or gaming apps face much steeper challenges.

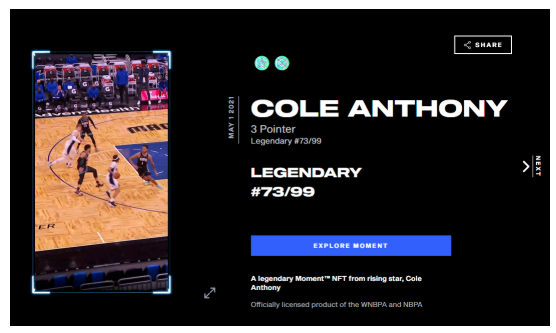

Yet music holds a unique advantage: artists possess exceptional fan mobilization power. When musical IP integrates effectively with crypto projects, non-crypto user growth can break through. A prime example is NBA Top Shot—Flow’s NFT project combining a traditional sports IP with blockchain.

NBA Top Shot homepage displaying digital collectible cards. Source: https://nbatopshot.com/

NBA Top Shot began testing in 2020 but exploded in 2021. According to DappRadar, it has seen over 14 million transactions totaling more than $860 million, with over 520,000 unique traders. Notably, trading volume correlates strongly with star power—its December 2021 volume surged 72% month-over-month following a collaboration with Kevin Durant.

Similarly, Web3 music projects need strong IP backing. Many music celebrities have already joined: rappers like Snoop Dogg, pop legends like Whitney Houston, and Chinese singer Hu Yanbin, who released an NFT album called “Monk” with Tencent Music.

Even traditional labels are experimenting. In November 2021, Universal Music announced Kingship—a Bored Ape-themed band.

User scale remains the biggest hurdle for Web3 music products. Beyond waiting for broader crypto adoption, active involvement from music stars and institutions may be the fastest path to scaling.

3.2 Technical Readiness: Layer-1 Blockchains and Decentralized Storage

Compared to user adoption, the technology stack for Web3 music is relatively mature. A typical song is 5–6MB—well within the capacity of current Layer-1 blockchains paired with decentralized storage solutions like Arweave or IPFS/Filecoin. Playback and listening UX are comparable to Web2, except most purchases require crypto payments. However, as crypto-to-fiat gateways expand, buying NFT songs with fiat will soon be seamless.

3.3 Community Mindset: DAO Experiments Among Fan Communities and Value Redistribution

As entrepreneur and investor Peter Thiel wrote in *Zero to One*, a new product must offer an experience “10x better” to overcome user habits and trust barriers. While musicians have strong incentives to experiment with Web3, most users won’t switch unless Web3 music offers unique, hard-to-replicate features.

Currently, Web2 platforms excel in library breadth, audio quality, and streaming speed—areas where Web3 struggles to compete.

Do users care enough about owning music—shifting from streaming access to NFT ownership? Probably not—at least not yet.

Per IFPI’s 2020 report, streaming subscription revenue grew 19.9% YoY, while download revenue fell 15.7%—a sharper decline than even pandemic-hit live performances. The trend is clear: users are moving from device-based “ownership” to platform-driven “access.” Unless music NFTs offer compelling added value, this shift won’t reverse.

Consider Kings of Leon, the first band to release an NFT album (*When You See Yourself*) on March 5, 2021. One NFT variant, the “Golden Ticket,” grants lifetime VIP access: four front-row seats to every future concert, plus perks like private drivers, meet-and-greets, and exclusive lounges. But such personalized services carry real costs—unlike zero-marginal-cost streaming—and can’t scale to mass audiences.

Limited-edition “Golden Ticket” NFT issued by Kings of Leon

In my view, the true upgrade in value for music NFTs may begin with “DAO membership privileges” and reimagined value distribution.

DAOs—decentralized, collaborative, shared governance models—are naturally suited to fan communities. Many fan groups already operate like proto-DAOs, emphasizing contribution and passion. Yet they suffer from opaque fund management, unclear responsibilities, and disbandment when key members leave. Integrating NFTs, smart contracts, and DAO tools can resolve these issues.

More importantly, owning a specific music NFT could become a gateway to joining an artist’s DAO. Accumulating, combining, and using music NFTs within DAOs opens countless use cases.

For Gen Z—who embrace novelty and crave belonging and self-expression—joining, participating in, and co-building a DAO around a favorite artist will deliver far deeper satisfaction than merely “owning a song” or attending a concert. For the DAO itself, NFTs streamline verification and management. With proper onboarding and engagement rules, increased participation can spark unforeseen vitality—potentially birthing entirely new music services.

Moreover, if music NFTs link royalty distributions directly to fans—and introduce referral or curation incentives—this could deepen social marketing and user engagement, creating richer value.

Therefore, over the next 1–2 years, key indicators to watch include: the emergence of Web3-native artist fan organizations, and whether new NFT-based value distribution models can mobilize massive user bases. These developments may signal the arrival of Web3 music’s breakthrough moment.

In sum, for the Web3 music sector to experience a “DeFi Summer”-style breakout, it must satisfy several prerequisites: sufficient user scale, technical readiness, and widespread adoption of DAO principles in music. These will be critical areas to monitor.

Section 4: The Growth Trajectory of the Web3 Music Sector

Looking back at successful, user-scale crypto sectors with lasting impact—first DeFi (rising in 2020), then PFP NFTs (exploding in 2021)—which path might Web3 music

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News