Understanding the Three Models of NFT Collateralized Lending: Peer-to-Peer, Pooled, and Centralized

TechFlow Selected TechFlow Selected

Understanding the Three Models of NFT Collateralized Lending: Peer-to-Peer, Pooled, and Centralized

Back to collateralized lending: for NFTs, collateralization clearly entails certain liquidity costs—when the token price rises, you can't sell to realize profits; when the price falls, you can only hold passively.

Original Title: A Brief Reflection on NFT Collateralized Lending

Original Author: Jiawei

Introduction

(It’s been over ten months since the DeFi summer of 2020. Aave, once a blue-chip in DeFi lending, has quietly dropped to 61st in market capitalization ranking, while Compound has fallen even further beyond the top 100—an unexpected turn.)

Regarding collateralized lending, for NFTs there is clearly a liquidity cost involved: when token prices rise, holders cannot sell to realize profits; when prices fall, they can only hold passively.

For institutions or core players holding top-tier NFT projects (such as CryptoPunks and BAYC), selling may not be their intention at all. Therefore, when asset liquidation is needed, collateralized lending becomes a viable option—especially given that high-end NFT prices tend to be relatively stable.

Furthermore, retail investors often trade NFTs speculatively with frequent buying and selling. Given that their total NFT holdings are generally low in value, such assets are less suitable for use as collateral.

Thus, in the short term, NFT lending will likely remain a niche sector, primarily serving holders of top-tier or blue-chip NFTs.

Three Types of Projects

Peer-to-Peer Model

In DeFi lending, Aave's predecessor Ethlend adopted a peer-to-peer model.

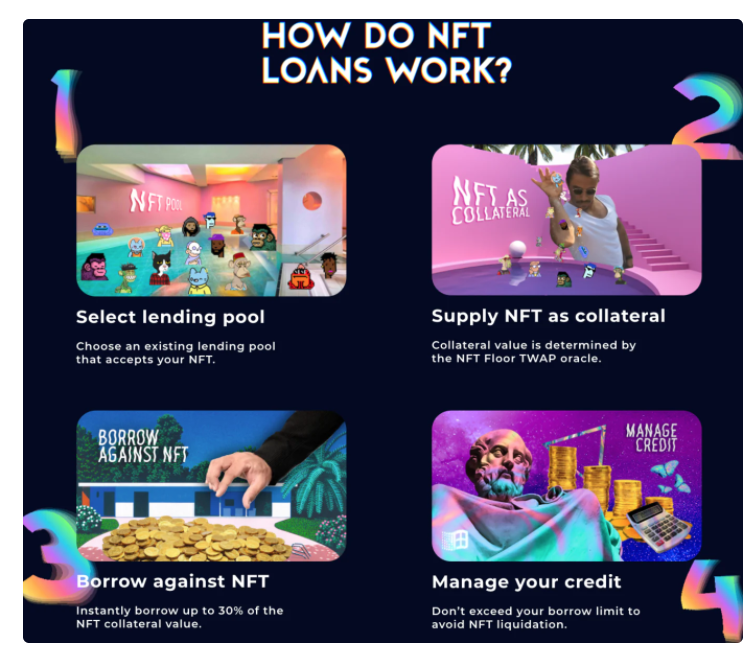

Arcade operates similarly. Its AssetWrapper contract supports bundling ERC721, ERC1155, and ERC20 assets into wrapped NFTs (wNFTs). Borrowers set loan amount, repayment terms, currency, and duration, then pledge the wNFT as collateral, waiting for lenders to match the request. Future versions of Arcade plan to add installment repayment options.

Notably, Arcade does not feature automatic liquidation. In case of default, borrowers retain the ability to repay the loan before the lender claims the collateral.

For peer-to-peer platforms, timely fulfillment of lending demands directly impacts user experience. Currently, Arcade does not publish average matching wait times. However, according to team members, loan requests using floor-priced BAYC and CryptoPunks are typically fulfilled instantly.

An important distinction between NFTs and fungible tokens (FTs) is that each NFT within a collection varies. Lenders may struggle to assess rarer pieces, and disagreements over valuation between parties increase uncertainty in lending.

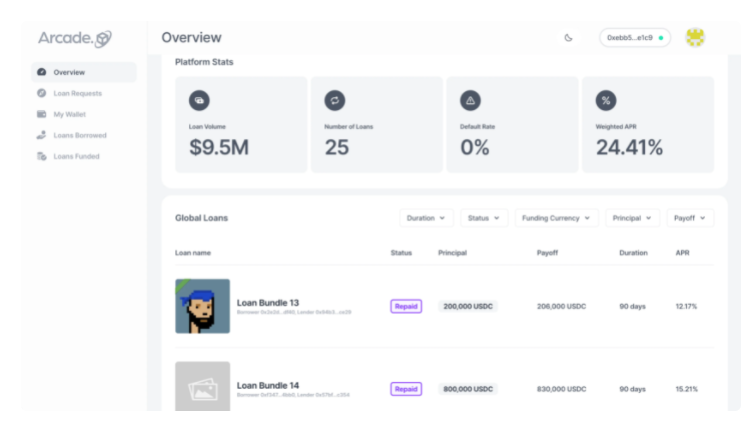

As of now, Arcade has facilitated over $9.5 million in total loans across 49 NFT collections. In December last year, it raised a $15 million Series A round led by Pantera Capital.

Pool-Based Model

The second type follows a pool-based model similar to Aave and Compound—for example, Drops DAO.

Under this model, loans have no maturity date, and interest rates are determined dynamically based on asset utilization. Real-time NFT pricing relies on oracle feeds.

Dyo Hu provides a more detailed comparison of peer-to-peer versus pool-based models in this article.

For highly rare NFTs, their value gets diluted within a shared pool, resulting in lower loan-to-value ratios and making borrowing less favorable.

Overall, the pool-based model is more complex, carrying risks of price manipulation and cascading liquidations. Given the generally low liquidity in the NFT market, this model poses higher systemic risk. In the early stages of decentralized NFT lending, the peer-to-peer model appears comparatively more stable and reliable.

Centralized Model

At the end of last year, digital asset financial services firm Nexo partnered with Three Arrows Capital to launch a centralized NFT lending service. Exchange Kraken also plans to introduce a similar offering.

Nexo essentially offers an OTC-style service requiring basic KYC information. Currently, only BAYC and CryptoPunks are accepted as collateral, with a minimum NFT value of $500,000. The annualized interest rate is around 15%, and the loan-to-value ratio ranges from 10% to 20%. For instance, a $500,000 NFT could secure a loan between $50,000 and $100,000.

The centralized NFT lending model suits institutional users but may feel less native to crypto OGs.

Closing Thoughts

By analogy with the real-world art market, global art transactions declined 22% year-on-year in 2020 due to the pandemic, yet still exceeded $50 billion—numerically suggesting strong potential for art-backed lending.

However, authenticating physical artworks (including antiques) remains subjective and lacks authoritative verification, making valuation difficult. Due to illiquidity, even after liquidation, there's no guarantee the collateral can be resold. To offset these risks, traditional pawnshops heavily discount items, offering very low loan-to-value ratios.

In contrast, verifying NFT authenticity requires only checking the contract address; valuations can reference floor prices of comparable NFTs; and online trading makes resale significantly easier. From both technical and operational standpoints, NFT lending faces fewer obstacles than traditional art financing.

Recently, Azuki quickly rose to rank 8th in OpenSea trading volume. More such blue-chip projects are likely to emerge. Headline NFTs like CryptoPunks and BAYC, rising blue-chips like Doodles and Azuki, along with land parcels in Sandbox and Decentraland, are poised to become primary collateral assets in future NFT lending markets.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News