A Comprehensive Guide to NFT Lending Projects: Who's Leading and Who's Falling Behind?

TechFlow Selected TechFlow Selected

A Comprehensive Guide to NFT Lending Projects: Who's Leading and Who's Falling Behind?

NFT lending has definitely been the hottest area over the past few weeks.

Author: William M. Peaster

Translation: TechFlow intern

As the NFT ecosystem sentiment heats up and a wave of high-quality projects emerges, more and more people are seeking ways to leverage their NFTs without selling them. Among these, NFT lending has undoubtedly become one of the hottest areas in recent weeks.

Main Types of NFT Lending

Currently, there are two main types of NFT lending: NFT leasing and NFT-backed loans.

The first type allows users to rent out their NFTs to others. For example, if a borrower wants to temporarily access an NFT-gated community, they can rent an NFT for that purpose. reNFT is one team operating in this space.

The second type—NFT-backed lending—allows users to collateralize their NFTs to borrow other cryptocurrencies. I will focus on this form of NFT lending below, as it is currently more widespread and in higher demand than leasing platforms.

Why Borrow Against NFTs?

In many jurisdictions, selling an NFT (like selling regular cryptocurrency) triggers a taxable event. However, borrowing against your assets (such as crypto or NFTs) generates non-taxable income under U.S. tax rules.

Therefore, by choosing to use an NFT as collateral, individuals can gain immediate liquidity without actually selling the NFT and triggering tax consequences.

Additionally, some users leverage their NFTs through borrowing to acquire additional funds for purchasing more NFTs—essentially using leverage.

Explosion of Lending Platforms

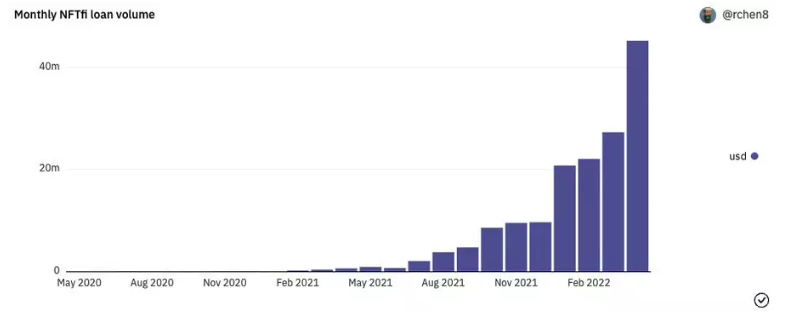

The earliest and most popular NFT lending protocol is NFTfi, a peer-to-peer (P2P) NFT lending platform where users lend directly to each other.

On NFTfi, lenders can earn interest by providing DAI or WETH loans, while borrowers can gain liquidity by listing eligible NFTs as collateral. Loan terms (duration, interest rate, etc.) are negotiated between parties, and in case of default, the associated NFT is transferred to the lender. To date, NFTfi has facilitated over $170.5 million in loans.

Other Newer P2P NFT Lending Platforms

-

AbraNFT — An NFT lending project built by Abracadabra Money

-

Arcade — An NFT lending project built on top of Pawn Protocol, an NFT infrastructure system

Alternative Approaches to NFT Lending

P2P lending is not the only way to facilitate NFT loans.

For instance, JPEG—a new NFT lending protocol—has pioneered a novel approach called NFDP (NFT-Backed Debt Position). The mechanism works similarly to Maker Vaults, but instead of depositing ETH to borrow DAI, NFDP allows users to deposit NFTs like CryptoPunks to borrow JPEG’s PUSD stablecoin.

Notably, the project uses Chainlink oracles to obtain and maintain on-chain pricing data for its NFT collateral.

Recently, another model—pool-based lending—has also been gaining momentum.

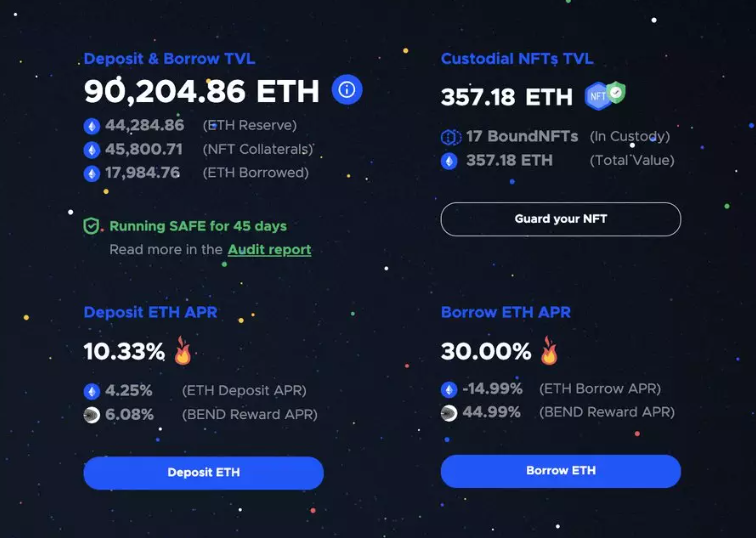

These platforms require lenders to act as liquidity providers (LPs), depositing ETH into a pool from which borrowers can take loans after first locking up an NFT as collateral. For example, BendDAO is a pool-based lending project that accepts blue-chip NFTs such as Azukis, Bored Apes, CryptoPunks, CloneX, Doodles, and Mutant Apes as initial collateral types.

Other Notable Pool-Based Projects

-

DropsDAO – "Instant lending for JPEG, NFTs, and metaverse assets"

-

Fluid – "Fair, instant, protected, NFT-backed lending"

-

Pine – "Permissionless NFT-backed lending and NFT financing"

P2P vs. NFDP vs. Pool-Based Models

Each of these three models comes with its own advantages and disadvantages for NFT lending:

Advantages of P2P

-

Well-suited for rare NFTs; traders can customize loan terms based on specific NFT traits.

-

Liquidation, or default, occurs only when the borrower fails to repay (not due to floor price drops).

-

Smart contract logic is simple and straightforward.

Disadvantages

-

Longer loan origination times; requires time to find willing lenders

-

Lending yields are not consistent

Advantages of NFDP

-

Mature Collateralized Debt Position (CDP) structural design

Disadvantages

-

Rapid floor price declines may lead to under-collateralization and liquidation

-

Custom oracles have not yet been thoroughly battle-tested

-

Currently limited range of accepted collateral

Advantages of Pool-Based Models

-

Borrowers can receive loans instantly

-

Lenders can immediately earn yield on their ETH deposits

Disadvantages

-

More complex token economics

-

More complex smart contracts

-

Limited collateral options

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News