Cryptocurrency Three Hundred Years Ago: Re-examining Money's Second Empowerment Through John Law

TechFlow Selected TechFlow Selected

Cryptocurrency Three Hundred Years Ago: Re-examining Money's Second Empowerment Through John Law

If a token's value continues to depreciate and people lose trust in it, how can we rapidly increase its value—or even make it overvalued? Perhaps referencing John Law's approach from three hundred years ago, a feasible solution could be to re-empower the token through resource-backed exchange.

By: Tiny Hand

If a token's value continuously depreciates and people lose trust in it, how can it be rapidly revalued—or even overvalued?

Three hundred years ago, someone already offered a solution.

At a time when there was no modern banking or monetary system—when gold and silver coins were the norm—John Law issued paper money for the first time. He used government debt as a prerequisite to purchase shares in his company, turning deeply devalued bonds into sought-after assets and helping France escape a sovereign debt crisis. However, due to political constraints of the era, some of his envisioned mechanisms remained unrealized.

Today, three centuries later, the international monetary system has fully abandoned the gold standard, evolving into a credit-based framework similar to what John Law imagined. In the further frontier of cryptocurrency, variations of Law’s playbook replay daily—making once-unrealizable ideas now feasible.

In this article, we’ll uncover John Law’s method of creating “credit-backed paper money” and explore how to design a model for token empowerment.

Let’s examine what happened.

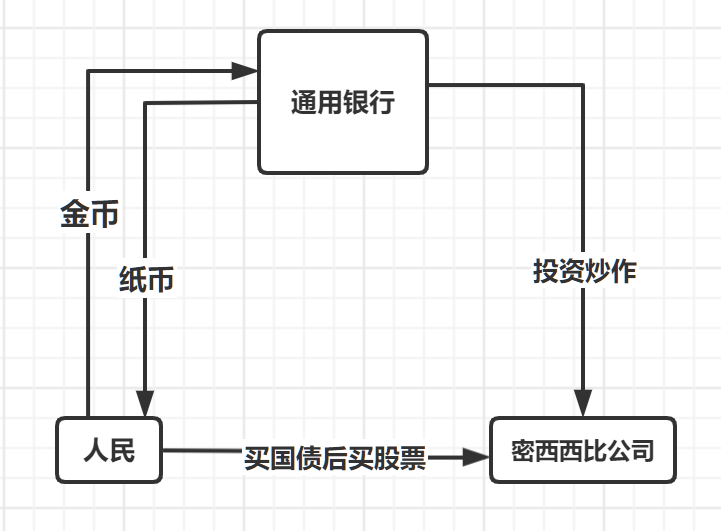

The context: France was in dire financial straits. With few options left, the government granted John Law special privileges to help resolve the debt crisis. This enabled the implementation of his vision: replacing a coin-based banking system with one based on credit.

■ 1. General Bank

John Law first established the General Bank, which issued paper notes redeemable at any time for gold coins. These notes could also be used in transactions. Thanks to their portability and backing by precious metals, along with the government’s promise not to interfere or devalue them [LS1], the notes quickly gained credibility. At first, Law even set a 1% premium for paper notes over gold, prompting widespread adoption.

■ 2. Mississippi Company

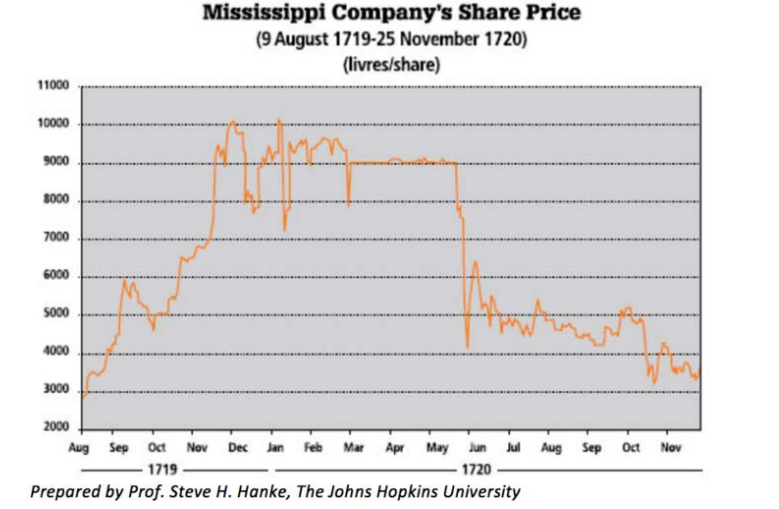

After securing exclusive rights from the French government to develop and trade in North America, Law founded the Mississippi Company. Promoting it with the narrative of “gold mining,” he funneled deposits collected by the General Bank into the company, driving its stock price upward. Amid rumors of instant wealth and soaring share prices, public FOMO (fear of missing out) surged, and people scrambled to buy shares.

Mississippi Company stock price chart

■ 3. Setting Entry Barriers

Law mandated that anyone wishing to buy company shares must first purchase government bonds—and use those bonds to acquire shares.

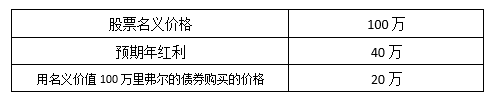

Let’s do the math: suppose you wanted to buy 1 million in shares:

The effective return on investment reached an astonishing 200%. People rushed to buy both bonds and shares. In open markets, share prices soared to ten times their initial offering price. Riding the wave of public FOMO, Law and the government issued an additional 1.5 billion livres in stock—12 times the volume of the previous two rounds combined.

This mechanism—using government debt to subscribe for new shares—temporarily restored the market value of previously worthless bonds back to par.

The government received money by selling bonds; the Mississippi Company acquired these bonds and then destroyed them, absolving the government of repayment obligations. In return, the government agreed to pay the company 4% annual interest for 25 years.

■ 4. Bank Restructuring and Debt Transfer

The French government restructured the private bank into the Royal Bank and began issuing large quantities of paper money. By late 1720, the total paper money supply reached 3 billion livres, while the Royal Bank held only 700 million in reserves. Through interest payments, the government effectively transferred its debt burden—eliminating massive liabilities.

■ 5. Aftermath

According to capital adequacy calculations, even using conservative estimates, the Royal Bank’s capital adequacy ratio reached 16%, double the level required under the modern Basel Accords. Yet, the first entity to initiate a bank run was none other than the monarchy itself. No bank—then or now—can withstand such pressure, including the Bank of England at the time. With insufficient gold reserves to meet redemption demands, nationwide gold conversion collapsed.

To prevent total economic collapse, John Law enacted deflationary measures: gradually reducing the official price of Mississippi Company shares from 9,000 livres per share down to 5,000 livres, while halving the circulating money supply. But public confidence in both paper money and stocks had already evaporated. Share prices continued to plummet—the “Mississippi Bubble” had burst.

■ Summary

Although the plan ultimately failed, we can still learn from John Law’s approach—and draw parallels to today’s crypto world.

The second step was crucial: Law created a compelling vision—“the Mississippi Company will discover gold in North America.” Then, when people wanted to invest, he imposed a condition: buying shares required prior purchase of government bonds.

Law employed two key tactics: first, investing gold deposits from the bank into the Mississippi Company to inflate stock prices; second, leveraging state endorsement to amplify publicity around the company’s colonial privileges. By shifting focus to grand narratives, he successfully induced mass bond purchases alongside stock subscriptions—alleviating France’s debt crisis.

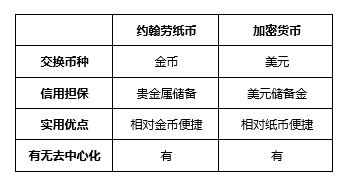

From a monetary perspective, why did people accept Law’s paper notes?

1. Redeemable for gold at any time

2. Protected from centralized government devaluation

3. Backed by precious metal reserves

4. More convenient than physical coins

5. Accepted by the government for tax payments

Today, cryptocurrencies exhibit similar traits: stablecoins like USDT are redeemable 1:1 for USD, operate on decentralized blockchains, and are backed by reserve assets. They serve as intermediaries to absorb market capital—different in origin but functionally comparable in building rapid consensus and boosting value.

Where Was the Reserve?

Historical records suggest that paper money wasn’t widely used in everyday transactions. Instead, institutions and companies adopted it for large-scale transfers and settlements due to its convenience. The lending relationships between banks and corporations created mutual dependency, discouraging mass sell-offs or redemptions. This institutional adoption served as implicit endorsement, reinforcing public trust.

Ordinary citizens didn’t question reserve adequacy—as long as powerful entities like the government continued holding and using the notes. But once those same authorities initiated massive redemptions, panic spread, triggering a liquidity crisis. Indeed, this is precisely how Law’s system ultimately collapsed.

Can We Solve These Historical Problems Today?

John Law had considered two solutions to secure adequate reserves: direct taxation to fund the treasury, or using paper money issuance as a form of indirect taxation. Both were blocked by the existing “tax farming” system.

Under France’s tax-farming regime, the monarchy outsourced tax collection to aristocrats who kept any surplus beyond fixed quotas. This undermined transparency and efficiency, preventing Law from establishing taxes as a reliable reserve mechanism.

In contrast, today’s crypto space has made a major leap forward: smart contracts. These enable automatic transaction-based taxation, eliminate third parties, increase transparency, and enhance system trustworthiness—making it structurally easier to build Law-like credit systems.

Regarding reserves, algorithmic stablecoins represent a breakthrough—they solve Law’s dilemma by removing reliance on fiat or crypto collateral. Instead, they manage token supply purely through algorithms and smart contracts. Functionally, their monetary policy mirrors central banking—and offers platforms greater operational flexibility.

Later depreciation of Law’s notes stemmed from capital flight (wealthy individuals converting paper to gold and smuggling it abroad) and declining circulation. Today, DeFi offers multiple liquidity solutions to stimulate usage. One could even imagine projects adopting Olympus-style bonding mechanisms to encourage staking and reduce outflows.

Back to 2022

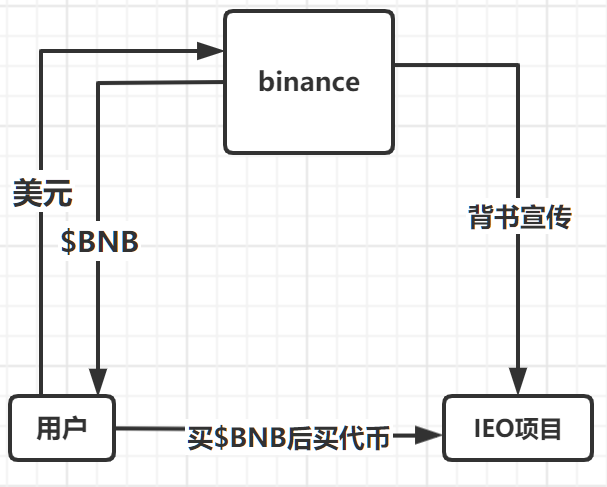

We’ve seen that after certain ICO projects skyrocketed, the market organically generated a narrative: “ICO investments yield massive returns.” Exchanges and project teams then collaborated on IEOs (Initial Exchange Offerings), curating and auditing high-potential projects.

Two parallels emerge with John Law’s paper money: rising asset value (stocks/tokens) and authoritative endorsement (government/exchange).

Take Binance’s IEO as an example: participation requires holding at least 50 $BNB. Every 50 $BNB earns one lottery ticket (up to 10 per account), making $BNB ownership an indirect entry requirement.

As demand rises, $BNB appreciates—gaining real utility as an IEO access pass. Similarly, purchasing Mississippi Company shares required first acquiring government bonds. In both cases, the underlying asset gains secondary utility as a “ticket” to opportunity.

The difference? Law’s primary goal was to revalue government debt, so he followed a “paper money → bonds → shares” path. He needed both currency issuance and bond reflation—adding complexity compared to today’s platform tokens. Still, his model offers valuable inspiration for modern token design.

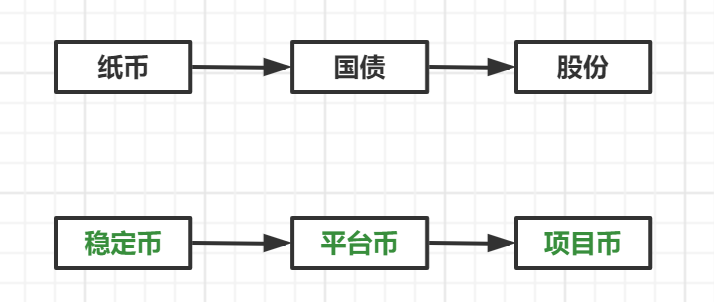

A New Token System Model

Looking back, Law’s merged institution functioned like a hybrid of the Federal Reserve and U.S. Treasury—handling money creation, taxation, and sovereign debt. By selling shares, he absorbed high-interest legacy debt, lowering financing costs.

Modern projects can adopt a similar blueprint for their own token ecosystems.

Here’s a proposed organizational token system:

Token structure:

1. Stablecoin

Purpose: Grant the organization “seigniorage rights”

Role: A reliable settlement medium

Initially, it could follow Law’s strategy—issuing at a premium to attract users. Unlike platform tokens, its value isn’t tied to team performance.

2. Platform Token

Equivalent to equity in the ecosystem. It connects various services, pays fees, and powers operations. Its value depends heavily on continuous team-driven innovation and revenue generation. Binance’s success shows how “security-like tokens” can evolve into “utility tokens,” opening new design possibilities.

3. Project Token

Issued by individual projects within the ecosystem. Value and functionality depend on each project team. Projects retain governance autonomy as long as they meet ecosystem standards.

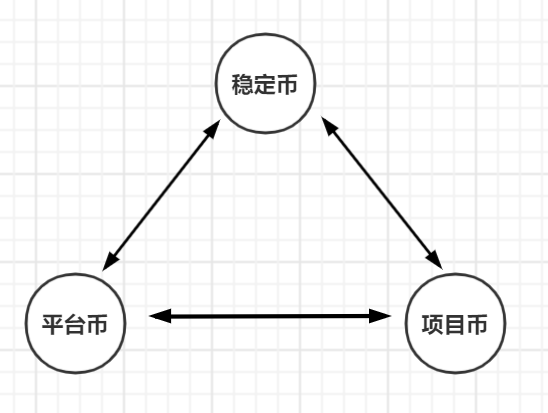

These three tokens interconnect and mutually empower one another.

For example: project tokens can be linked to platform tokens (via IEOs), and to stablecoins (for trading and settlement). Through strategic design, they create a self-sustaining loop supporting governance and profitability.

Three-token relationship diagram

This model has been validated—both by John Law’s short-term success and Binance’s long-term execution. However, most organizations lack the coordination power of France or Binance, making full implementation difficult. Many instead experiment with partial integration among the three token types.

How to Connect Them?

Whether a nation or a company, a model without resources cannot function. Initial resources act as the essential fuel. France’s starting advantage was colonial monopoly rights; Binance’s was exchange competitiveness. By leveraging these, France empowered the Mississippi Company, and Binance empowered its ecosystem partners—exchanging initial assets for real-world utility. This transformed tokens from hollow shells into functional instruments. Continuous resource swaps enabled systemic integration.

Therefore, for any organization, I recommend identifying your core resources and determining which of the three token roles best fits your position. Then, find pathways to interact with the other two. Use resource swaps to continuously reinvest in your token, expand its utility, and gradually bring the entire model to life.

Conclusion

Returning to our opening question: if a token keeps losing value and trust, how can we make it rise rapidly—or even exceed expectations? Perhaps, by following John Law’s 300-year-old playbook: use resource swaps to re-empower it. It’s worth a try.

History repeats—but thinking shouldn’t be bound by precedent. Crypto opens theoretical possibilities. Our task isn’t just to reflect on past failures, but to build systems of our own.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News