Economic Reality: AI Alone Propels Growth, Cryptocurrency Becomes Political Asset

TechFlow Selected TechFlow Selected

Economic Reality: AI Alone Propels Growth, Cryptocurrency Becomes Political Asset

A wave of liquidity will arrive in 2026, and the market consensus hasn't even started pricing it in yet.

Author: arndxt

Translation: Chopper, Foreisght News

If you've read my previous articles on macro dynamics, you might already sense what's coming. In this piece, I'll break down the true state of the current economy: artificial intelligence (AI) is the only engine driving GDP growth; every other area—labor markets, household finances, affordability, asset accessibility—is deteriorating; and everyone is waiting for a "cycle turning point," but there is no real "cycle" to speak of anymore.

The truth is:

-

Markets are no longer driven by fundamentals

-

AI capital expenditure is the sole pillar preventing a technical recession

-

A wave of liquidity will arrive in 2026, and market consensus hasn't even begun pricing it in

-

Wealth inequality has become a macro-level constraint forcing policy adjustments

-

The bottleneck for AI isn't GPUs—it's energy

-

Cryptocurrencies are becoming the only asset class with genuine upside potential for younger generations, giving them political significance

Do not misjudge this transition risk and miss the opportunity.

Market Dynamics Are Decoupled from Fundamentals

Last month’s price swings had no support from new economic data, yet were violently shaken by shifts in the Fed's stance.

Merely due to comments from individual Fed officials, rate cut probabilities swung repeatedly from 80% → 30% → 80%. This phenomenon confirms the core feature of today’s market: systemic capital flows have far more impact than active macro views.

Here is micro-structural evidence:

1) Volatility-targeting funds mechanically reduce leverage when volatility spikes and increase leverage when volatility declines.

These funds do not care about the “economy,” as they adjust exposure based solely on one variable: market volatility.

When market volatility rises, they de-risk → sell; when volatility falls, they re-risk → buy. This causes automatic selling during weak markets and automatic buying during strong ones, amplifying two-way volatility.

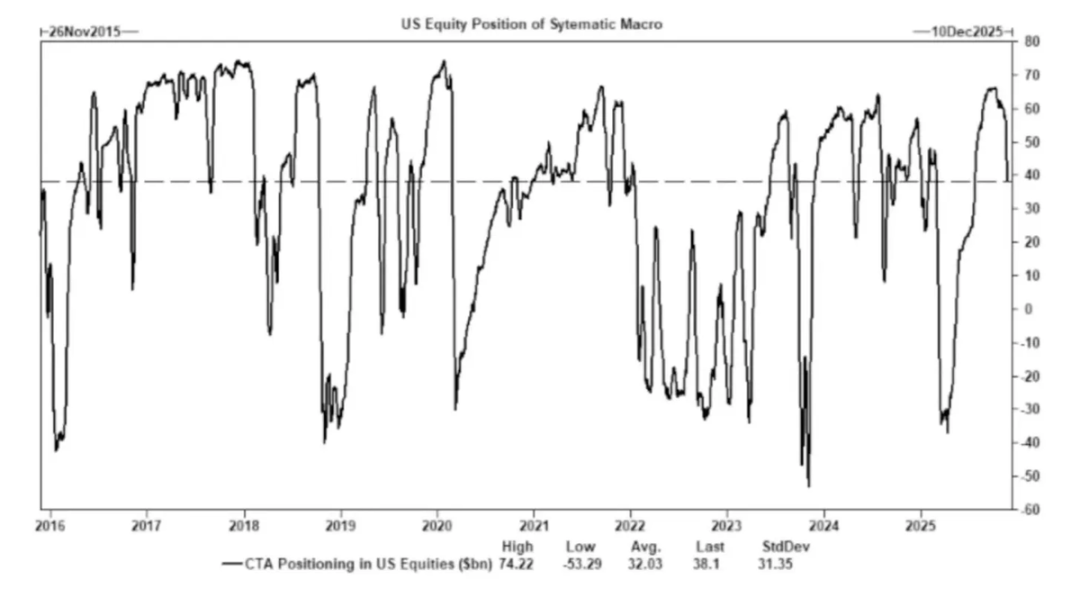

2) Commodity Trading Advisors (CTAs) switch long/short positions at preset trend levels, generating forced flows.

CTAs follow strict trend rules with zero subjective "opinions"—purely mechanical execution: buy when price breaks above a level, sell when it drops below.

When enough CTAs hit the same threshold simultaneously, massive coordinated trades occur—even without any fundamental change—potentially driving entire indices over multiple days.

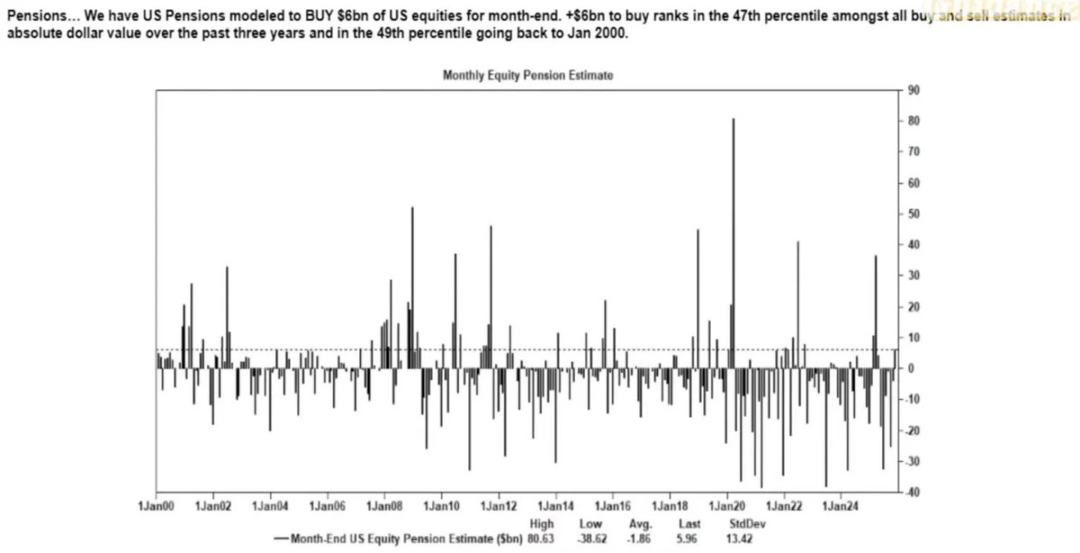

3) Share buyback windows remain the largest source of net equity demand.

Corporate share buybacks are the stock market’s biggest net buyers, surpassing retail investors, hedge funds, and pension funds combined.

During open buyback periods, companies inject billions weekly into the market, leading to:

-

Inherent upward momentum during buyback seasons

-

Noticeable market weakness once buyback windows close

-

Structural buying unrelated to macro data

This explains why equities can rise even amid poor sentiment.

4) An inverted VIX curve reflects short-term hedging imbalances, not “panic.”

Normally, long-term volatility (3-month VIX) exceeds short-term volatility (1-month VIX). When this reverses, people often assume “rising fear,” but today this is primarily driven by:

-

Short-term hedging demand

-

Options market makers adjusting positions

-

Weekly options fund inflows

-

Systematic strategies executing month-end hedges

This means: VIX spikes ≠ panic—they reflect hedging flow dynamics.

This distinction is crucial—volatility is now driven by trading behavior, not narrative logic.

Today’s market environment is more sensitive to sentiment and capital flows: economic data has become a lagging indicator of asset prices, while Fed communication drives volatility. Liquidity, positioning structure, and policy tone are replacing fundamentals in price discovery.

AI Is Key to Avoiding Full-Blown Recession

AI has become a macro stabilizer: it effectively replaces cyclical hiring needs, supports corporate profitability, and sustains GDP growth despite weakening labor fundamentals.

This implies the U.S. economy’s dependence on AI capex is far greater than policymakers publicly admit.

-

Artificial intelligence is suppressing labor demand among the lowest-skilled, most replaceable third of the workforce—the very group where recessions typically begin.

-

Productivity gains mask otherwise widespread deterioration in labor conditions. Output remains stable because machines absorb tasks previously done by entry-level workers.

-

Fewer employees mean higher corporate margins, while households bear the socioeconomic burden. Income shifts from labor to capital—a classic recessionary dynamic.

-

AI-related capital formation artificially sustains GDP resilience. Without AI capex, overall GDP figures would clearly be weak.

Regulators and policymakers will inevitably support AI capex through industrial policy, credit expansion, or strategic incentives—because the alternative is recession.

Wealth Inequality Has Become a Macro Constraint

Mike Green’s assertion that the poverty line ≈ $130K–$150K sparked intense backlash—an outcome that underscores how deeply this issue resonates.

The core truths are:

-

Childcare costs exceed rent/mortgage payments

-

Housing is structurally unaffordable

-

Baby boomers dominate asset ownership

-

Younger generations hold income but lack capital accumulation

-

Asset inflation widens wealth gaps year after year

Wealth inequality will force adjustments in fiscal policy, regulatory stances, and asset market interventions. Cryptocurrencies, as tools enabling younger generations to participate in capital appreciation, will grow in political importance—prompting corresponding shifts in policymaker attitudes.

The Bottleneck for Scaling AI Is Energy, Not Compute

Energy will become the central narrative: scaling the AI economy requires parallel expansion of energy infrastructure.

All the talk about GPUs overlooks a more critical bottleneck—power supply, grid capacity, nuclear and natural gas production, cooling systems, copper and critical minerals, and data center location constraints.

Energy is emerging as the limiting factor for AI development. Over the next decade, energy—including nuclear, natural gas, and grid modernization—will be one of the highest-leverage investment and policy areas.

A Dual-Track Economy Emerges, With Widening Gaps

The U.S. economy is splitting into two sectors: a capital-driven AI sector and a labor-dependent traditional sector, with little overlap and increasingly divergent incentive structures.

The AI economy continues expanding:

-

High productivity

-

High profit margins

-

Low labor dependency

-

Strategically protected

-

Attracts capital inflows

The real economy continues shrinking:

-

Weak labor absorption

-

High consumer stress

-

Declining liquidity

-

Asset concentration

-

Inflationary pressures

The most valuable companies over the next decade will be those able to bridge or exploit this structural divide.

Outlook

-

AI will receive policy backing, because the alternative is recession

-

Liquidity led by the Treasury—not QE—will become the primary policy channel

-

Cryptocurrencies will become a politically significant asset class tied to intergenerational equity

-

The real bottleneck for AI is energy, not compute power

-

Over the next 12–18 months, markets will continue to be driven by sentiment and capital flows

-

Wealth inequality will increasingly dominate policy decisions

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News