The Unicorn Journey of FTX: $18 Billion Valuation in Two Years

TechFlow Selected TechFlow Selected

The Unicorn Journey of FTX: $18 Billion Valuation in Two Years

The birth of FTX did not come from a flash of genius "brilliant idea"

The crypto world never lacks geniuses or miracles.

In May 2019, cryptocurrency exchange FTX was born amid a bear market. In August 2021, FTX announced a $900 million Series B funding round at an $18 billion valuation, attracting over 60 investment firms including SoftBank Group, Sequoia Capital, and Lightspeed Venture Partners.

This fundraising became the largest private equity financing event in crypto industry history.

Sam Bankman-Fried (SBF), founder of FTX born in 1992, has accumulated billions of dollars in crypto assets and made it onto the Forbes Global Rich List.

How did this $18 billion unicorn rise so rapidly? What did it get right?

Note: Some friends previously "criticized" today’s internet and blockchain media content formats, arguing that most analyses are after-the-fact justifications—rationalizing outcomes that may have been coincidental. This criticism is worth accepting and reflecting upon. However, we also believe that while history doesn’t repeat itself, it often rhymes. Looking back helps us move forward more wisely and see further ahead. Moving forward, TechFlow will periodically publish its series on crypto unicorns.

The Birth and Rise of FTX

FTX did not emerge from a sudden flash of genius. According to the FTT whitepaper, FTX arose because unmet demands existed within the cryptocurrency industry:

At the time, we found many problems with existing leading contract exchanges. We submitted countless feedbacks to these platforms, yet no improvements were made. Rather than waiting for them to adopt our suggestions and improve their products and services, we decided to build our own product—one capable of directly solving these issues and changing the market landscape.

Driven by this idea, FTX—a digital asset derivatives trading platform entirely different from existing contract exchanges—was born.

Looking back at May 2019, most people didn’t think this was a viable startup direction—similar to how someone saying they’d build a public chain surpassing Ethereum might sound crazy.

OKEx, Binance, Huobi, Coinbase, and Bitfinex were then dominant giants in the industry, holding firm positions. Entering at that moment, what chance did FTX have against such titans?

“The exchange赛道格局已定,新交易所没有出头机会” (“The exchange landscape is already settled; new exchanges have no room to break through”) was why some investors dismissed FTX. In hindsight, however, this was a false premise—because FTX wasn't truly competing in the same赛道 as those above.

From day one, FTX positioned itself specifically as a cryptocurrency derivatives exchange. While spot trading and derivatives appear similar, they differ significantly.

Spot exchanges rely on relatively simple business models, depending heavily on team instincts about market trends. Derivatives trading, however, involves complex financial modeling and product design, demanding strong financial DNA and technical expertise from founding teams.

Take BitMEX—their founder Arthur Hayes came from Wall Street and leveraged perpetual contracts to become king of derivatives exchanges by 2019. Despite criticisms over poor UI, bad user experience, and lack of even a mobile app, his position remained unchallenged.

The primary users of spot exchanges are retail investors who value simplicity and ease-of-use.

Derivatives exchanges mainly serve institutions, followed by professional traders and knowledgeable investors. Thus, their goals extend beyond convenience—they demand professionalism and precision.

Therefore, at the time, FTX had only two real competitors: BitMEX and OKEx—and the market was still very early-stage.

Understanding this explains the rise of FTX and later entrants like Bybit—because the crypto derivatives space was far from saturated, with numerous needs still unmet.

So why was it SBF and FTX that succeeded?

In summary, two main reasons:

(1) Liquidity

As mentioned earlier, FTX emerged because Alameda Research—the market-making firm founded by SBF—had unmet trading needs. Therefore, FTX was born with a golden spoon—liquidity support from Alameda Research.

As early as 2019, Alameda Research was already one of the largest liquidity providers and market makers in the crypto market. Most notably, in July 2019, when Binance’s spot market suddenly saw a massive sell order of 7,500 BTC, Alameda digested the entire sell pressure within just 20 minutes.

At the time, the Alameda team recorded and tweeted the entire process, earning praise and a retweet from Binance CEO CZ.

For institutions and professional traders, liquidity—or trading depth—is the top consideration when choosing a derivatives platform, without exception.

Even during FTX’s initial launch phase, aside from BitMEX’s BTC perpetual contract, its liquidity surpassed all other contract trading platforms—an unmatched core advantage among new entrants.

(2) Innovation and Altruism

Warren Buffett often says, “Stay within your circle of competence.” Early FTX followed this principle—focusing solely on derivatives and innovating around them.

For FTX in 2019, innovation was the only path to breakthrough.

First came mechanistic innovations, including a loss-sharing prevention mechanism, centralized margin pools, and universal USD stablecoin settlement.

In 2019, contract liquidation events were a hot topic—liquidation refers to situations where futures traders lose not only their margin but owe money to the exchange. At the time, executives from major exchanges publicly criticized each other over this issue.

FTX introduced an original three-tier liquidation model to minimize losses from such incidents.

The first line of defense resembles most liquidation engines—real-time monitoring of user positions and margin ratios for risk control. The second line activates automatically during volatile markets—FTX’s liquidity providers step in to stabilize accounts at risk of liquidation. The third layer is a risk assurance fund designed to cover losses incurred by users due to liquidations.

Previously, users typically opened positions using individual coins—for example, depositing BTC as margin for BTC contracts—making position adjustments harder and increasing forced liquidation risks.

FTX introduced a novel approach: using stablecoins for settlement and allowing all contracts to share a single universal margin wallet.

This proved to reflect actual investor demand and has since been adopted by other exchanges.

On the product front, features now taken for granted—USD-margined stablecoin contracts and leveraged tokens—were both pioneered by FTX. Notably, the "never-liquidate" leveraged tokens have become standard offerings across major exchanges, contributing significantly to their profits.

Looking back at FTX’s innovations—from the three-tier liquidation system and universal margin settlement to USD-margined contracts and leveraged tokens—the underlying philosophy remains consistent: minimize investor losses and reduce liquidation risks as much as possible.

If some smaller exchanges design products aiming to “stimulate gambling tendencies and push investors into higher-risk scenarios,” FTX genuinely prioritizes investor interests in its product philosophy.

Perhaps this embodies SBF’s long-standing advocacy of “altruism.”

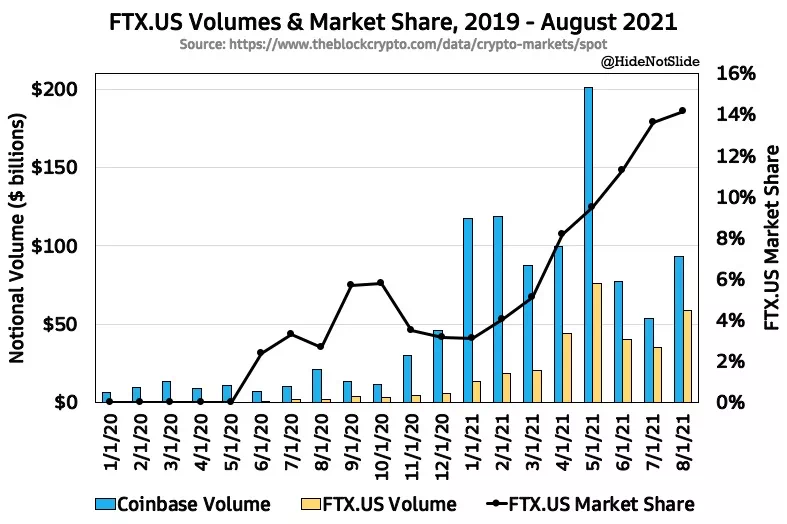

Expansion of FTX.US

To target the U.S. market, SBF launched FTX.US—a separate, independent trading platform not owned by FTX—with multiple U.S. regulatory licenses.

On September 1, FTX.US announced plans to acquire LedgerX, a cryptocurrency derivatives trading platform regulated by the Commodity Futures Trading Commission (CFTC). The acquisition was expected to close before October 2021.

SBF tweeted: “This could be one of our most exciting announcements ever.”

Most people likely underestimated the significance of this news.

Globally, cryptocurrency exchanges can broadly be divided into two categories: U.S.-based and non-U.S.-based.

This is because compliant U.S. exchanges command higher capital premiums.

Take Coinbase: On September 12, its daily trading volume ranked eighth globally at ~$2.9 billion, yet its market cap reached $50 billion.

In August, FTX.US President Brett Harrison said in an interview that FTX.US aims to offer crypto derivatives trading within less than a year. Upon completion of the acquisition and leveraging LedgerX’s longstanding relationship with the CFTC, FTX.US is highly likely to obtain relevant compliance licenses, enabling it to directly offer Bitcoin and Ethereum options and futures contracts to retail and institutional traders.

Additionally, since launching in May 2020, FTX.US trading volume has surged, hitting a record high of $790 million on September 9.

Meanwhile, to deepen its presence in the U.S., FTX.US has aggressively sponsored various sports events:

In September, FTX and FTX.US announced a long-term partnership with NBA superstar Stephen Curry, who led his team to three championships. Curry will receive equity in FTX and serve as its brand ambassador, with part of his salary paid in cryptocurrency.

FTX.US secured naming rights to the Miami Heat’s home arena via a 19-year, $135 million contract—one of the most expensive naming deals ever.

FTX partnered with esports team TSM in a 10-year, $210 million exclusive naming rights deal and collaborated with Riot Games—the developer of League of Legends—in a seven-year agreement, securing sponsorship visibility in the League of Legends Championship Series (LCS).

Compared to Coinbase’s market cap, once FTX.US launches derivatives trading and maintains current growth momentum, a new hundred-billion-dollar unicorn is rising.

The rise of FTX.US will also boost FTX’s overall brand value.

FTT Investment Analysis

FTT is the foundational value pillar of the entire FTX ecosystem.

When analyzing and discussing exchange tokens, I typically examine three aspects: exchange fundamentals, token value capture, and future expectations.

Trading volume is the strongest fundamental indicator for any exchange.

In April this year, SBF tweeted that FTX’s trading volume grew 8,000% year-on-year—the fastest growth rate among all platforms.

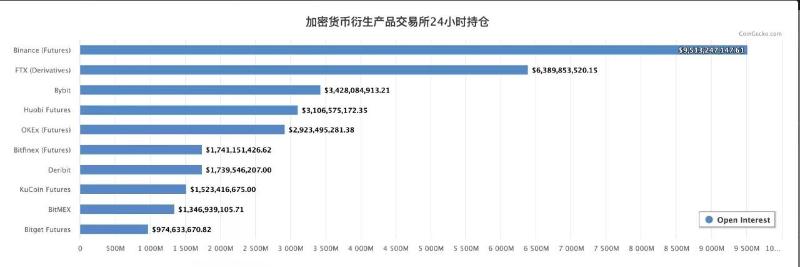

Currently, FTX ranks fourth in total trading volume industry-wide, with derivatives remaining its core business pillar.

According to Coingecko data, as of September 13, 2021, FTX ranks second globally in derivatives open interest, behind only Binance.

Regarding token value capture, platform tokens generally consist of two parts: financial value and practical utility.

On financial value, FTX employs a deflationary FTT burn strategy, which will continue until the circulating supply of FTT reaches 50% of the total issuance.

Per the whitepaper, starting July 29, 2019, FTX repurchases and burns FTT every Monday using funds from:

1. 33% of all platform fee revenues

2. 10% of net increases in risk margin ("socialized gains")

3. 5% of other platform revenues

Official figures show that by September 15, 2021, FTX had burned over 13 million FTT tokens, valued at over $1 billion.

In terms of practical utility, FTT serves multiple use cases:

1. Fee rebates: Staking FTT grants up to 0.003% maker fee rebate

2. Contract margin: FTT can be used directly as margin for contracts

3. Bonus airdrops: Stakers qualify for SRM airdrops (and future potential airdrops)

4. Token sale coupons: Stakers gain access to presale allocation coupons on FTX

5. Free withdrawals: Stakers enjoy daily free ERC20 token withdrawal allowances

Notably, prior to late February 2021, FTX offered free withdrawals—an effective fee subsidy totaling over $20 million in gas fees.

Later, frequent Ethereum network congestion caused gas fees to skyrocket, forcing FTX to adjust its free ERC20 withdrawal policy. Even so, withdrawal fees remain among the lowest globally—starting at just $10 USDT. With sufficient FTT staked, users can nearly eliminate ERC20 withdrawal fees altogether.

Overall, FTT’s value growth is closely tied to FTX’s fundamentals—primarily driven by actual trading volume, especially derivatives holdings and transactions, followed by increased investor demand driving both practical usage and investment demand for FTT.

How FTX Captures Value

One criticism regarding FTT’s valuation is that it’s merely a utility token for the exchange, lacking the value capture mechanisms of a public blockchain.

This view may be somewhat superficial. After all, for most exchanges, building an EVM-compatible sidechain is technically trivial. Perhaps a deeper question should be asked: What does a public chain actually mean for a centralized exchange?

In the past, centralized exchanges were nearly the sole gateway connecting investors and crypto assets—monopolizing listing rights and collecting passive fees.

With the arrival of the DeFi era, AMM-based DEXs like Uniswap introduced permissionless listings, decentralizing power and breaking the centralized exchange monopoly on listings.

Secondly, in the spot market, exchanges compete based on wealth effects generated by high-quality assets. As exchanges lose their listing monopoly, premium assets no longer depend entirely on centralized platforms.

Thus, in the DeFi era, centralized exchanges face two major anxieties: decentralized trading venues and access to premium assets.

Just as Tencent held WeChat as its ticket during the shift from PC to mobile internet, exchanges now need a “DeFi ticket” of their own.

FTX got there early.

SBF, FTX’s founder, is also a supporter of the high-performance Solana blockchain. As early as July 2020, he participated in developing parts of Project Serum’s decentralized exchange ecosystem.

Serum is a high-performance order-book DEX built on Solana and serves as a cornerstone of the Solana ecosystem. Other Solana-based projects can leverage Serum DEX’s matching engine, liquidity, and price data.

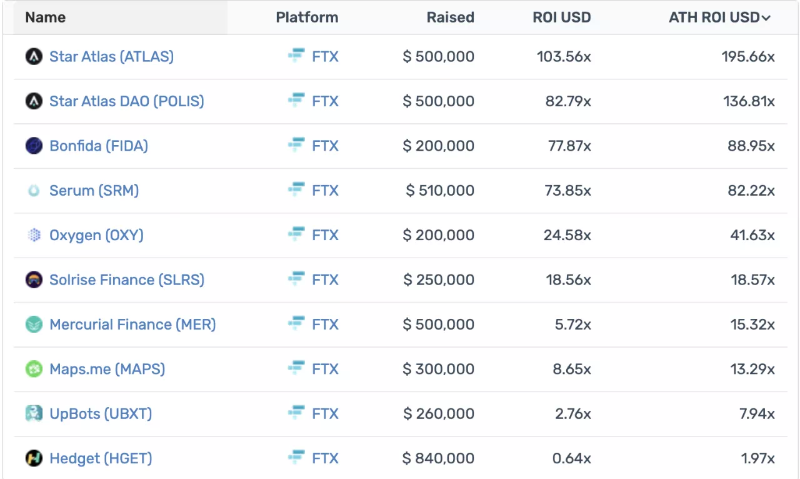

With DeFi covered, the Solana ecosystem also provides FTX with abundant quality assets—IEO being the clearest example.

According to Cryptorank, as of September 12, the average ROI (return on investment) for all IEO projects on FTX was 4,055%.

Therefore, FTX doesn’t need to build an EVM sidechain—SBF’s support and strategic positioning within the Solana ecosystem give FTX access to both promising DeFi trading scenarios and a pipeline of high-quality assets.

FTX’s Bottlenecks and Future

FTX’s strengths need no repetition—its bottlenecks are equally apparent.

Since FTX initially targeted professional derivatives traders, product design leaned heavily toward trader preferences—both web and app interfaces feel quite “trader-oriented.”

As FTX expands beyond niche circles and its user base grows, some investors—especially those from East Asia accustomed to simpler interfaces—may find FTX’s user experience inconvenient.

This一定程度 hinders adoption among certain user segments and limits expansion of FTX’s spot trading business.

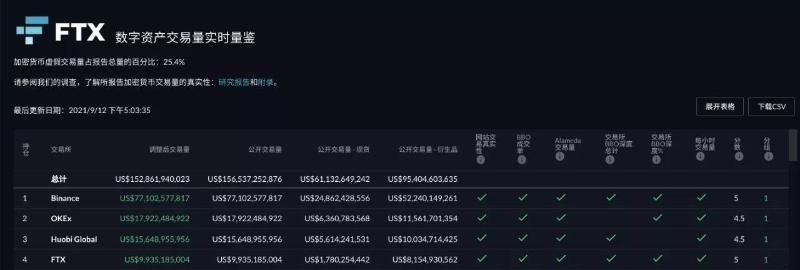

According to FTX statistics, as of September 12, FTX ranked fourth in total trading volume.

In terms of spot trading proportion, spot volumes accounted for 32%, 35%, and 36% of total volumes on Binance, OKEx, and Huobi respectively, whereas FTX’s spot ratio stood at only 17%.

This weakness could also become a new growth opportunity.

One area FTX prides itself on is:

FTX has shorter R&D cycles compared to peers, faster iteration speeds, and introduces new product features daily.

This means FTX can quickly and continuously optimize its products—especially its mobile app—based on market demand, supporting spot market development. A breakthrough here would unlock FTX’s second growth curve.

Therefore, key areas to watch for FTX’s future include:

Continuous innovation in derivatives

Product upgrades and optimizations

Expansion of spot markets as a potential second growth curve

Ongoing discovery of high-quality assets by FTX

Cross-industry brand synergy effects from rapid growth of FTX.US

Disclaimer

This article is for case analysis only and should not be considered as investment advice or recommendations for action.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News