How can a DAO raise funds and better optimize its balance sheet?

TechFlow Selected TechFlow Selected

How can a DAO raise funds and better optimize its balance sheet?

Providing DeFi protocol DAOs with recommendations and guidance on various tools available for managing balance sheets/national debt.

Author | Yuan Han Li

Translation | Anima

Various tools for managing balance sheets / national debt offer advice and guidance to DeFi protocol DAOs.

The purpose of any protocol DAO is to permanently manage and govern its protocol. Therefore, a protocol DAO must be capitalized in a way that not only ensures its continued operation but also enables investment in the future growth of the protocol—this is no different from how enterprises think about capitalization.

Much like traditional companies finance themselves through retained earnings, equity, and debt, DAOs have similar options:

-

Retain protocol income and non-operating income

-

Sell native tokens for stablecoins/ETH/BTC

-

Take on debt

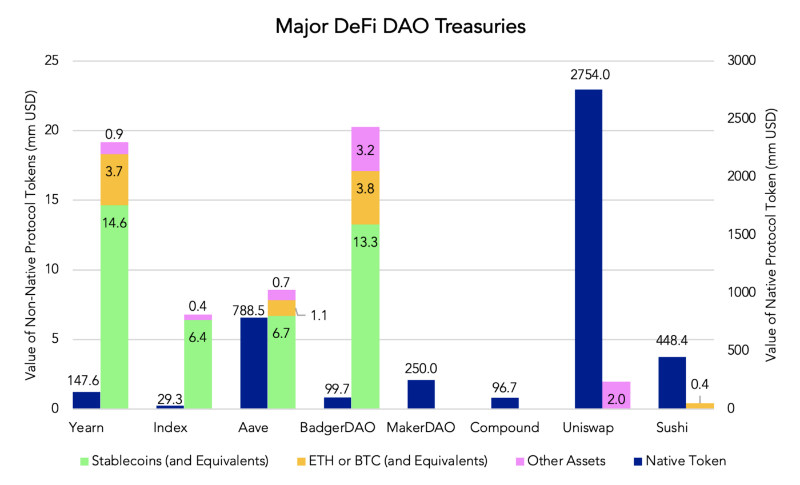

However, as shown in Figure 1, a large portion of assets held by some DeFi DAOs consists of their native tokens. Given that their operating expenses are priced in USD/fiat currency, a prolonged bear market could force DAOs to sell their native tokens at "fire-sale" prices to fund ongoing operations.

Therefore, DAOs should generate multiple revenue streams (i.e., protocol revenue and investment income) to cover these operating costs; however, since treasuries need an asset base to generate returns/non-operating income, DAOs should also consider conducting token sales or issuing debt to build such an asset base.

Retained Earnings:

Retained Earnings:

DAOs have two broad channels to generate income for retention: protocol revenue and non-operating income (i.e., investment returns).

Although many DeFi projects now understand the importance of retaining protocol-generated revenue as part of their token economics, not all DAOs retain fees/income generated by the protocol.

For example, while Aave, Yearn, BadgerDAO, and Index Coop retain generated protocol revenue within their DAO treasury, Sushi, Compound, Uniswap, and Maker currently do not.

Similar to high-growth companies, paying out "dividends" makes little sense when the return on investment into the core business exceeds the cost of capital. Additionally, DAOs should carefully consider the denomination of their earned income: most of Aave and Yearn’s income comes in high-yield stablecoins, whereas Index Coop's income is largely denominated in the high-risk products they create (e.g., DPI and leveraged “ETFs” on ETH/BTC).

Therefore, DAOs should retain at least some of the revenue generated by the protocols they manage and carefully evaluate in which units it is stored.

Especially given the size of many DAO treasuries, a significant portion of DAO income may also come from non-operating income/investment returns (at least until the protocol matures).

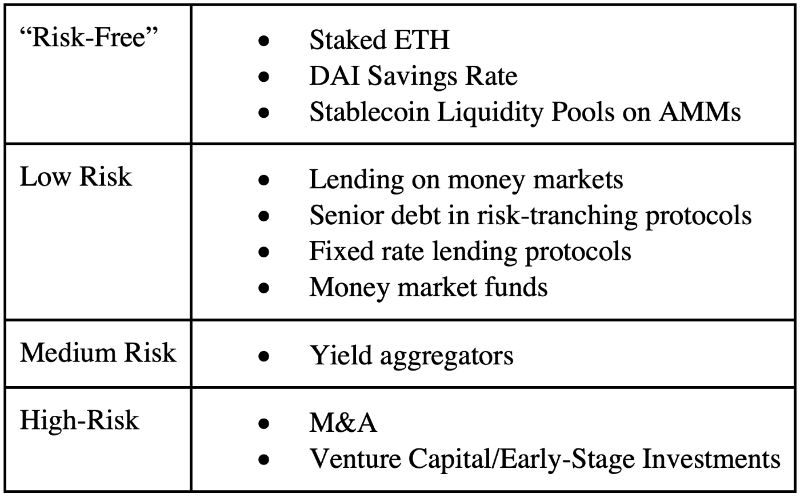

Just as traditional corporations categorize investments across varying risk profiles—from risk-free treasury bills and low-risk high-grade debt to high-risk M&A or venture capital—DAOs would benefit from identifying similar on-chain asset classes to diversify their balance sheets.

Currently, even some of the largest protocols cannot generate sufficient revenue to cover operating expenses (audits, salaries/payments to contributors, marketing, etc.).

For instance, Yearn operates at a loss even after accounting for non-operating income from yield farming. Thus, merely retaining protocol revenue might be insufficient to fund operations (at least until these protocols mature), meaning DAOs will likely need to raise additional funds to create a sufficiently large asset base capable of generating returns—this also provides guidance on how much treasury should be diversified: assume a reasonable and low-risk rate of return, then use budget projections to back into the "core" non-native-token holdings on the balance sheet.

Once a DAO establishes its reserve assets position, it can assess several tools based on its risk profile and decide on an allocation strategy that minimizes correlation and risk exposure to any single point of failure.

Raising Capital via Token Sales:

The best path toward balance sheet diversification and building substantial positions in reserve assets is through token sales. DAOs have only a few avenues to achieve this:

Open market sales at spot price; however, this could negatively impact the token price;

-

Off-market sales to strategically aligned investors (negotiate discounts to TWAP, lock-ups, etc.); however, a poorly negotiated deal may upset other token holders, and it can be difficult to selectively identify only those strategic investors who can become long-term partners to the DAO;

-

Auctions (can whitelist a group of buyers and impose lock-ups, or auction specially designed KPI options); however, auctions require careful design, especially if structures become complex, and marketing the auction could prove challenging;

-

Financial engineering (e.g., hedging, shorting futures/forwards/note issuance); however, these options ultimately equate to synthetic sales that will affect the token price at some point, and typically more exotic strategies require high fees paid to OTC desks (at least until the DeFi derivatives space truly matures).

Therefore, DAOs should carefully assess their specific needs to determine which method suits them best. For example, a particular DAO might ultimately choose a combination of options 2 and 3 to bring in value-added investors and incentivize existing token holders.

Financing with Debt:

In traditional finance, debt serves as an alternative—and potentially cheaper—form of financing compared to dilutive token sales.

Therefore, particularly for DAOs capable of generating substantial treasury income usable for amortizing/repaying debt, issuing debt could be considered as an alternative to token sales.

Currently, the dominant form of debt financing in DeFi is over-collateralized lending, and the vast majority of DAOs cannot simply open debt positions on platforms like Compound/Aave/Maker—even if their native tokens are accepted on services like CREAM or Unit Protocol, the borrowing power/debt ceiling is often insufficient to meet DAO needs.

As a result, most DAOs wishing to take on debt may have to issue bonds (zero-coupon and over-collateralized; using UMA's Yield Dollar) or convertible-like instruments (such as UMA's Range Tokens), then auction them off to obtain stablecoins.

While accepting undercollateralized debt (e.g., CREAM’s Iron Bank) is an option, this isn’t available to the vast majority of DeFi protocols. Even for the few fortunate protocols approved as borrowers on CREAM, these loans come with credit limits and are suitable only for short-term rather than long-term operational/capital expenditures typical of DAO-level needs. There’s nothing preventing a protocol from creating unsecured bonds and auctioning them off, promising to airdrop interest payments to holders at predetermined intervals.

However, as with all cases of DAOs obtaining unsecured/secured credit, creditors lack guaranteed processes or recourse for repayment under any circumstances. Unsecured/undercollateralized debt may become common only once standardized on-chain bankruptcy procedures emerge or another framework formalizing creditor rights on-chain develops. For example, TradFi creditors can initiate foreclosure proceedings against debtor companies, leading to Chapter 7/11 bankruptcy in the U.S., whereas DeFi lacks agreed-upon or established practices. Until chain-based “bankruptcy” mechanisms or a new system formalizing on-chain creditor rights emerges, undercollateralized/unsecured debt in DAOs is unlikely to surge.

Conclusion:

Given that DeFi DAOs are responsible for permanently supporting their protocols, managing their balance sheets according to their income and expenses is a critical activity. Most protocol DAOs currently hold only their native protocol tokens on their balance sheets.

Due to cryptocurrency volatility, this may mean DAOs are forced to sell their native tokens during prolonged bear markets—even at unfavorable prices—to fund ongoing operations. Therefore, DAOs should first ensure they have an optimal stream of income denominated in reserve assets. Then, if income proves insufficient to cover operating costs, DAOs should consider raising additional funding via token sales or debt to build up reserve assets.

Doing so will provide protocol DAOs with a substantial base of reserve assets on their balance sheets, which can be invested to generate additional non-operating income/investment returns—either closing the gap or providing a “buffer.” Following such a playbook will place any DAO in a stronger financial position to sustain its protocol even through years-long crypto bear markets.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News